If You Missed Our Best Recent Articles:

“The dollar’s dominance is not a gift. It is a burden that must be constantly re-earned - or eventually surrendered.”

- Barry Eichengreen, Exorbitant Privilege, 2011

Some questions hit you with an obvious answer at first-then the deeper you dig, the more you realize you got it wrong from the start.

This Week's Question: Why is the UAE-a nation sitting on over $2 trillion in sovereign wealth, $300 billion in reserves, and tens of billions in US T-bills-begging the US Treasury Secretary for a swap line?

When the news leaked from Washington in mid-April, markets split into two extreme camps, both wrong in fascinating ways.

One side panicked: UAE out of dollars. Petrodollar dying. Renminbi set to replace the dollar in oil trades.

The other side shrugged: Just a standard liquidity tool. Nothing unusual. Carry on. Investment bank analysts churned out soothing notes.

Both are staring at the same event-but asking the wrong question.

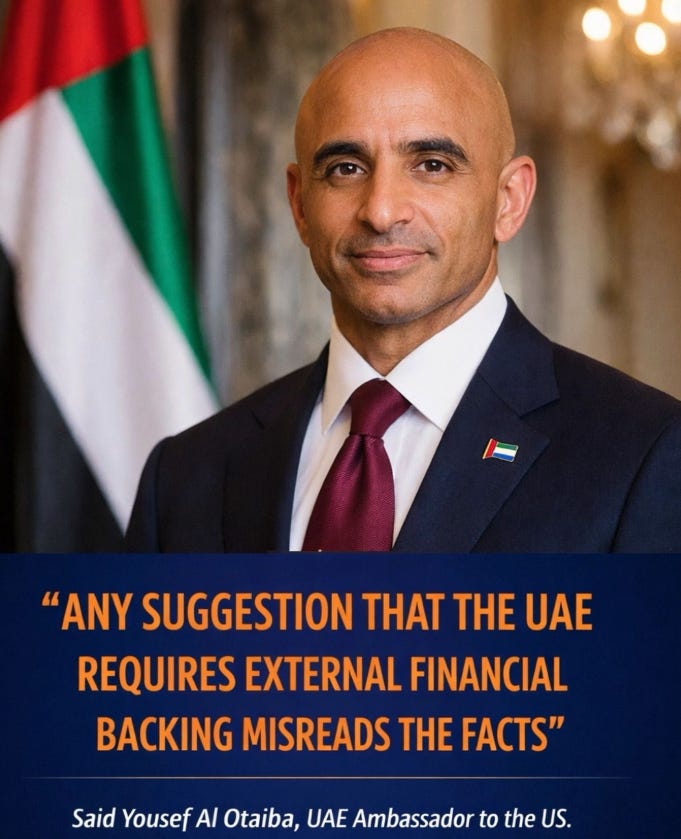

Because if UAE truly needed cash, they wouldn't need to ask the US. The UAE central bank holds more liquid T-bills than the entire US Treasury's Exchange Stabilization Fund-the tool Bessent is mulling to “rescue” them. It's one of 2026's most exquisite financial paradoxes: the beggar has more money than the begged.

And if it's not about money-what is the problem?

The short answer: status, leverage, and a silent restructuring of power dynamics in the global dollar architecture of which the UAE story is just the tip of the iceberg.

The long answer requires peeling back six layers-from the technical mechanics of swap lines, to oil and dollar flows disrupted by Hormuz, to the fierce market debate, to PIMCO's role as the unofficial lender of last resort, to a nightmare scenario few are discussing, and finally-to a power shift inside the US financial system that Kevin Warsh just publicly confirmed in congressional testimony.

The question “Will UAE get a swap line?” turns out to be the smallest in this saga.

The real question: when swap lines evolve from neutral technical tools into geopolitical weapons-who controls the global dollar system, and what happens in the next crisis when trust between central banks is no longer assured like in 2008?

In this week's dispatch, Viet Hustler breaks it down in six parts:

Part I - What is a swap line: mechanics, history, and why UAE was never in that club

Part II - How the Iran war disrupted Gulf dollar flows

Part III - Why UAE is asking-and why the real question isn't about money

Part IV - PIMCO and private markets: when lender of last resort isn't the Fed

Part V - Nightmare Scenario: Oil Rises Alongside a Stronger Dollar

Part VI - Three Things That Are Actually Happening-and No One Is Reading Them Right

PART I - WHAT IS A SWAP LINE: MECHANICS, HISTORY, AND WHY IT'S RARELY GRANTED

This is the part that most coverage this week glossed over too quickly-and that's precisely why most analyses got it wrong from the outset.

To understand why the UAE's request for a swap line is such an unusual event, and why the US response is far more complex than a simple 'yes' or 'no,' we need to properly grasp this tool-from its mechanics to its historical logic.

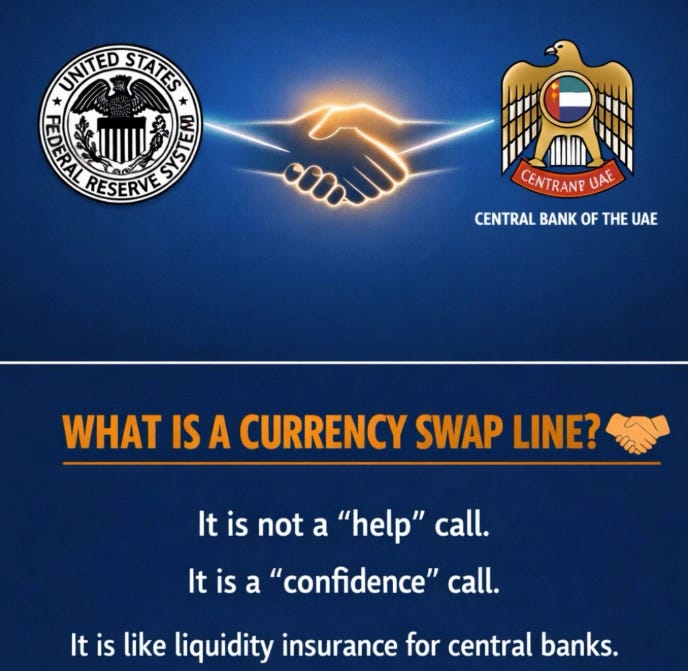

1.1. Swap Line Mechanics: Simpler Than You Think, More Important Than You Imagine

A currency swap line is a bilateral agreement between two central banks that allows each party to access the other's currency when needed. The diagram below is one of the most detailed depictions of this mechanism-mapping out the entire modern financial plumbing system behind swap lines and related tools.

The mechanism operates in four specific steps:

Step 1 - Initiation

The Central Bank of the UAE (CBUAE in this case) proactively contacts the Federal Reserve to signal it needs dollars.

The two sides agree upfront on:

Size: How many USD

Tenor: How long the drawdown (typically 7, 28 or 84 days)

CBUAE then holds a domestic dollar auction (for commercial banks), signaling that fresh USD liquidity is about to enter the system.

→ Simply put: CBUAE 'orders' dollars from the Fed, then prepares to redistribute them domestically.

Step 2 - Initial Exchange: Currency Swap at Market Value

This is the core of the swap:

CBUAE delivers dirhams to the Fed

The Fed delivers equivalent-value USD (at the prevailing market exchange rate)

In essence:

No traditional 'lending'

No financial leverage

No exchange rate risk (since the rate is 'locked in' upfront)

On the balance sheet:

Fed: Increases assets (dirham holdings) and liabilities (USD issuance)

CBUAE: Records the reverse

→ Think of it as a temporary currency swap, not borrowing in the conventional sense.

Step 3 - Deployment: Injecting Dollars Into the Economy

Once it receives the USD, CBUAE doesn't hoard them-it channels them straight into the domestic banking system.

How:

Relends USD to commercial banks

Via dollar auctions or repos (collateralized USD loans)

The actual flow: Fed → CBUAE → local banks → USD-needy businesses/investors

→ This is what the diagram calls the 'Global Dollar Bridge'-a direct conduit from the Fed to end-users, routed through the local central bank.

Implications:

Importers still have USD for payments

Banks avoid 'dollar thirst'

FX markets stay calm

Step 4 - Reversal: Closing the Pipeline

At maturity (7–84 days), the transaction fully reverses:

CBUAE returns USD to the Fed

Fed returns dirhams

At the original locked-in exchange rate

CBUAE pays a small fee (like a pipeline usage charge)

Key point:

No traditional interest rate

No exchange rate risk arises

No assets are truly "sold off"

→ The entire transaction is like temporarily borrowing dollars, using them, and returning everything to its original state.

The key is understanding what swap lines are NOT:

Not a loan - no debt is created, no interest in the conventional sense

Not a bailout - no economic reform conditions attached like IMF loans

Not a sign of weakness - many strong nations (Japan, UK, Canada) have standing swap lines with the Fed

Not an exchange rate guarantee - it doesn't commit to defending the dirham at any specific level

1.2. FIMA Repo Facility

In addition to traditional swap lines, the diagram mentions another key tool: FIMA Repo Facility (Cross-border Currency Repo). Simply put, this is a "liquidity escape hatch" for foreign central banks holding U.S. government bonds.

Instead of selling U.S. Treasuries into the market (which could roil prices and yields), they can:

Pledge Treasuries as collateral (repo) directly with the Federal Reserve

Receive U.S. dollars immediately

After a short period, repay the dollars and retrieve their bonds

Technically, this is an existing mechanism - no new negotiations needed, no special relationships required like swap lines. That means countries like the UAE can access USD liquidity anytime if they hold Treasuries.

That's why the UAE's pursuit of a direct swap line with the Federal Reserve is all the more noteworthy. For pure liquidity needs, they don't really need one, because:

FIMA Repo Facility provides quick USD without selling assets

No market risk from dumping Treasuries

No reliance on complex bilateral agreements

In other words, FIMA Repo addresses technical liquidity issues, so seeking an additional swap line suggests strategic or signaling objectives beyond short-term USD shortages.

The subtlest point: the greatest value of a swap line isn't in its use, but in its existence. The presence of a USD credit line from the Federal Reserve acts as a "psychological anchor" for the entire market:

Eases pressure on exchange rates and FX markets

Prevents expectations of fire sales or liquidity panics

Builds confidence that the system has a USD "lender of last resort"

This is why First Abu Dhabi Bank calls swap lines "dollar liquidity insurance" - not to handle crises after they erupt, but to prevent them from forming in the first place.

1.3. Usage history: a small club and crisis moments

Swap lines aren't new. The Fed experimented with them in the 1960s amid Bretton Woods strains. But their modern form was shaped by three major historical episodes.

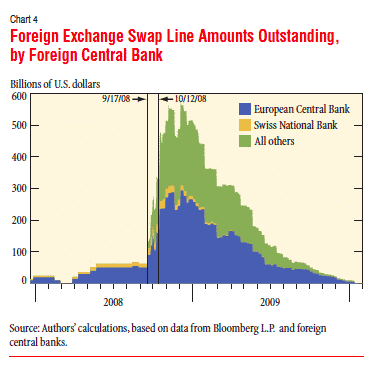

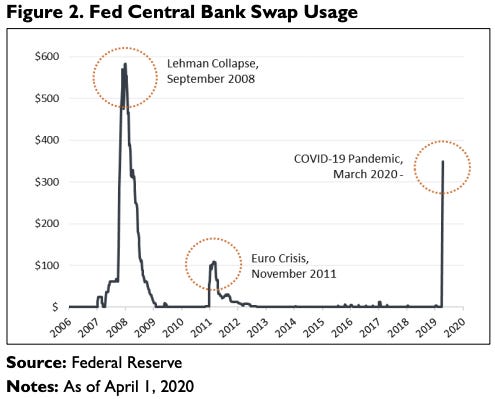

The 2008 global financial crisis was the first large-scale use. When dollar funding markets froze after Lehman Brothers' collapse, foreign banks - especially in Europe and Japan - faced acute dollar shortages from funding long-term assets with short-term dollar borrowing. The Fed activated swap lines with 14 central banks, peaking near $580 billion - unprecedented at the time.

The 2011-2012 euro crisis was the second. As eurozone breakup fears escalated and European banks lost dollar funding access, the ECB, Fed, and G7 central banks coordinated swap line activation, pushing balances to around $100 billion. Smaller than 2008 but enough to steady market nerves.

The COVID-19 pandemic in March 2020 was the third and most recent. As global markets seized up in a "dash for cash" - everyone needing dollars but no one willing to sell - the Fed activated swap lines with nine additional central banks beyond the five standing partners, surging total balances to nearly $450 billion in weeks.

After the May 2020 peak, swap line balances fell sharply to near zero and have stayed there - true to history: activated in crises, wound down when they pass.

1.4. The standing club: who gets in and why

This is the crux for contextualizing the UAE's request.

The Fed currently has five standing swap lines - unlimited in size, always ready to activate without further approval:

European Central Bank (ECB) - euro area

Bank of England

Bank of Canada

Bank of Japan

Swiss National Bank (SNB)

This is the G10 core - economies with financial markets most deeply integrated with the U.S., where dollar funding disruptions could quickly spill back into U.S. markets. Their common traits:

Developed, U.S.-integrated capital markets

Massive daily dollar trading volumes (their banks hold and lend dollars in the trillions)

Stress in their financial systems spills back to the U.S. almost instantly

Long-standing, transparent institutional ties with the Fed

Beyond the five standing partners, nine temporary ones were activated in COVID-2020 (now expired): Australia, Brazil, Denmark, Korea, Mexico, New Zealand, Norway, Singapore, and Sweden. These have financial markets large enough for dollar funding disruptions to cause significant spillovers.

The UAE has never been in either group. And that's where the story gets interesting.

1.5. Why the Fed Faces Challenges in Extending a Swap Line to the UAE

From the Federal Reserve's operational logic, the biggest hurdle isn't 'whether to help the UAE,' but that the UAE doesn't align with the Fed's longstanding unspoken criteria. Swap lines aren't a universal tool-they're designed for partners whose liquidity stress could spill back into the US financial system. Viewed through this lens, the UAE's fit is limited:

UAE banking system's integration with global dollar markets is significantly lower than G10 peers

Scale of USD holdings and lending isn't large enough to pose direct 'spillback risk' to the US

UAE's role is regionally central, not a core link in the global financial system

A second, technical but decisive barrier: data transparency. The Fed doesn't just provide liquidity-it needs a precise read on a partner's balance sheet. For the UAE, this creates substantial uncertainty:

Inconsistent data over time, with some series disrupted or revised

Key indicators on capital flows and sovereign wealth fund activity less clear than before

Difficulty accurately assessing true reserve scale, recent drawdowns and system liquidity

In a trust- and risk-pricing-based system, data gaps aren't just 'missing info'-they directly constrain the Fed's decision-making.

The final-and biggest-barrier lies in the principle of tool usage. The Federal Reserve's swap lines are designed to 'fix the dollar plumbing' when clogged, not to handle geopolitical shocks or prop up allies. Extending one to the UAE amid war and oil disruptions would set a hard-to-control precedent:

Other regional countries could make similar demands with the same rationale

Boundary between technical and geopolitical tools would blur

Fed's independence would be dragged into overlap with strategic policy

That's why, even with alternatives, the decision isn't straightforward.

More notably, the Federal Reserve hasn't yet been placed at the center of this process.

According to the Financial Times, Scott Bessent's exchanges with GCC and Asian countries occurred without formal Fed consultation. This highlights a clear misalignment in approaches:

Treasury prioritizes short-term market stability and geopolitical balancing

Fed prioritizes tool consistency and long-term systemic risk control

Swap line approval rests with the Federal Open Market Committee, so the Fed can't be 'railroaded'

In this context, the Exchange Stabilization Fund (ESF) emerges as a more executable option. This Treasury tool allows swift action without FOMC involvement:

Proven precedent, like Argentina in 2025 (~$20 billion)

Flexible process, no complex swap line structure required

Suited to political situations or rapid-response needs

Read more on Argentina and dollarization here

Yet this option exposes a structural paradox:

ESF holds only about $43.7 billion in actual resources

Source: https://home.treasury.gov/system/files/206/ESF-August-2025-FS-Trunc-Notes.pdf UAE holds about $70 billion in US T-bills

UAE's total reserves and sovereign assets run to hundreds of billions or trillions of dollars

→ The conclusion is clear: this isn't a liquidity shortage story anymore. The US is weighing support mechanisms for a partner whose financial firepower dwarfs the tool itself. This paradox reveals the issue's true nature-not money, but status in the dollar system, policy precedents, and power boundaries between Treasury and the central bank.

1.6. The Central Paradox: Why This Story Is Both Normal and Not

Putting it all together, the central paradox stands out:

Swap lines are routine for G10-but UAE isn't G10

Swap lines address US spillback risk-UAE has less integration than standing partners

Swap lines aren't bailouts-but UAE's liquid assets exceed US ESF

Bessent supports-but Fed wasn't consulted and may not approve

Trump says 'considering'-but FOMC operates independently of the White House

But one technical detail trumps all these, often overlooked in debate: GCC already has access to FIMA Repo Facility-they don't need a swap line for technical liquidity issues.

This means: if UAE's issue is 'needing dollars without selling Treasuries,' the solution exists. No new deal, no FOMC approval, no Bessent Senate declarations needed.

So why is UAE still asking? The answer isn't technical. It lies in a new use case Bessent is trying to shape for the tool.

1.7. When Swap Lines Become Geopolitical Weapons: Miran's Blueprint and Bessent's Ambition

This is the deepest layer of the UAE swap line story-and few read this far.

Stephen Miran and his controversial blueprint

Before joining the Fed, Stephen Miran authored a blueprint for overhauling US international trade-a document that later sparked fierce debate. In it, he proposed an entirely new use case for swap lines: not as a technical tool to ease dollar funding stress, but as a geopolitical reward for loyal allies.

Original quote: “The desire to maintain access to such swap lines will be a powerful long-term incentive for remaining inside the US security and economic umbrella.”

Translation: swap lines are no longer a neutral tool of the global financial system. They become the carrot-and implicitly the stick-in US foreign policy. Compliant countries get access; defiant ones risk losing it.

Bessent executes the blueprint

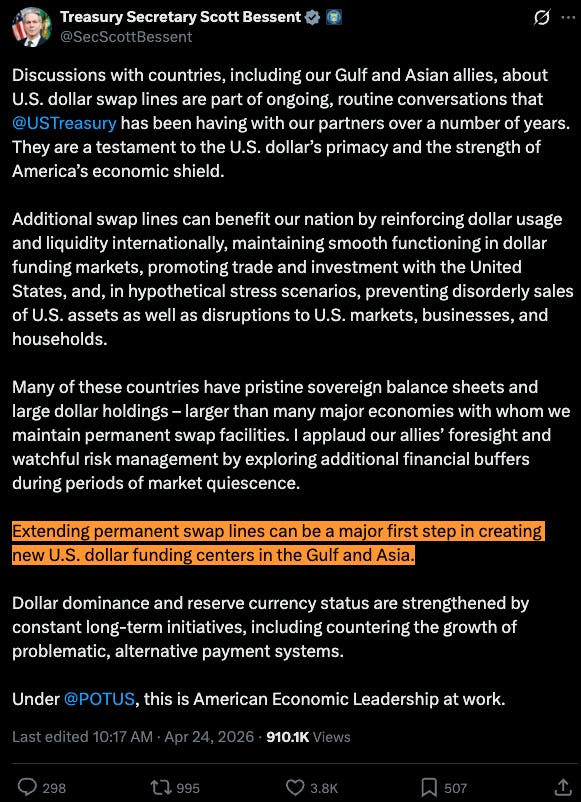

When Bessent told the Senate and later on X: “Extending permanent swap lines can be a major first step in creating new U.S. dollar funding centers in the Gulf and Asia” -this isn’t central bank speak. It’s the language of a geopolitical strategist.

If the goal is to create “new dollar funding centers,” markets have long since achieved that organically. Asia isn’t short of dollars. The Gulf isn’t short of dollars. The issue isn’t financial infrastructure-it’s who controls that infrastructure and by what logic.

Competing with China

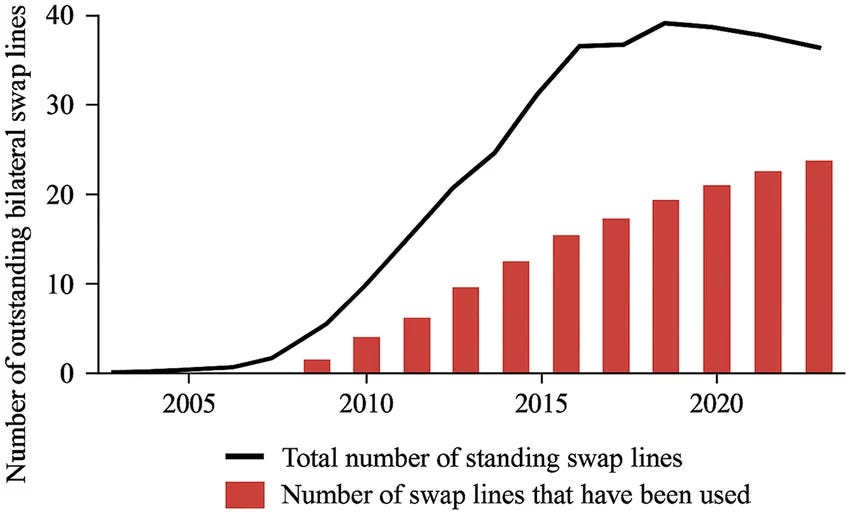

One unmissable layer of context: According to the CFR Swap Lines Tracker, China will have 36 swap lines by end-2025-far outnumbering the Fed’s five standing lines and nine temporary ones from COVID.

This is a parallel swap-line arms race to the geopolitical one. Beijing is using swap lines to expand renminbi influence and build its own financial network. Washington is countering by expanding the dollar network-not by the Fed’s technical logic, but by Bessent’s geopolitical one.

During Kevin Warsh’s hearing-the next presumed Fed chair contender-when asked about the dollar, Warsh said the Fed would

“play a supporting role in ensuring that the financial system is as safe as it can be and work with [Bessent and Rubio], because it’s outside of the conduct of monetary policy.”

Translation: Under Warsh, the Fed will back Bessent’s “economic statecraft” agenda. This is a structural shift- the Fed moving from neutral technician to foreign policy sidekick.

PART II - IRAN WAR AND THE SHOCK TO DOLLAR RECYCLING

2.1. Fifty years of accumulation and two months of reversal

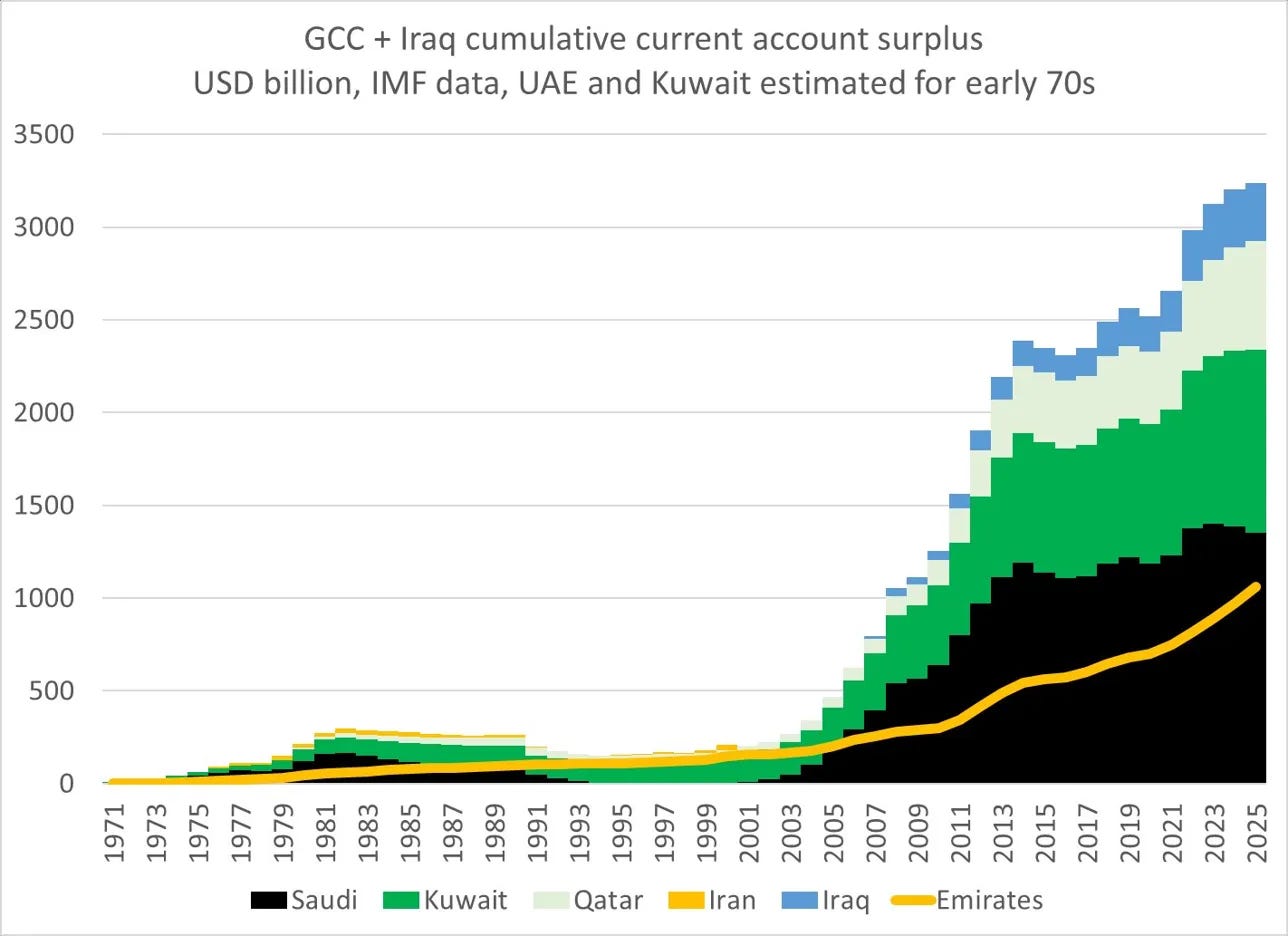

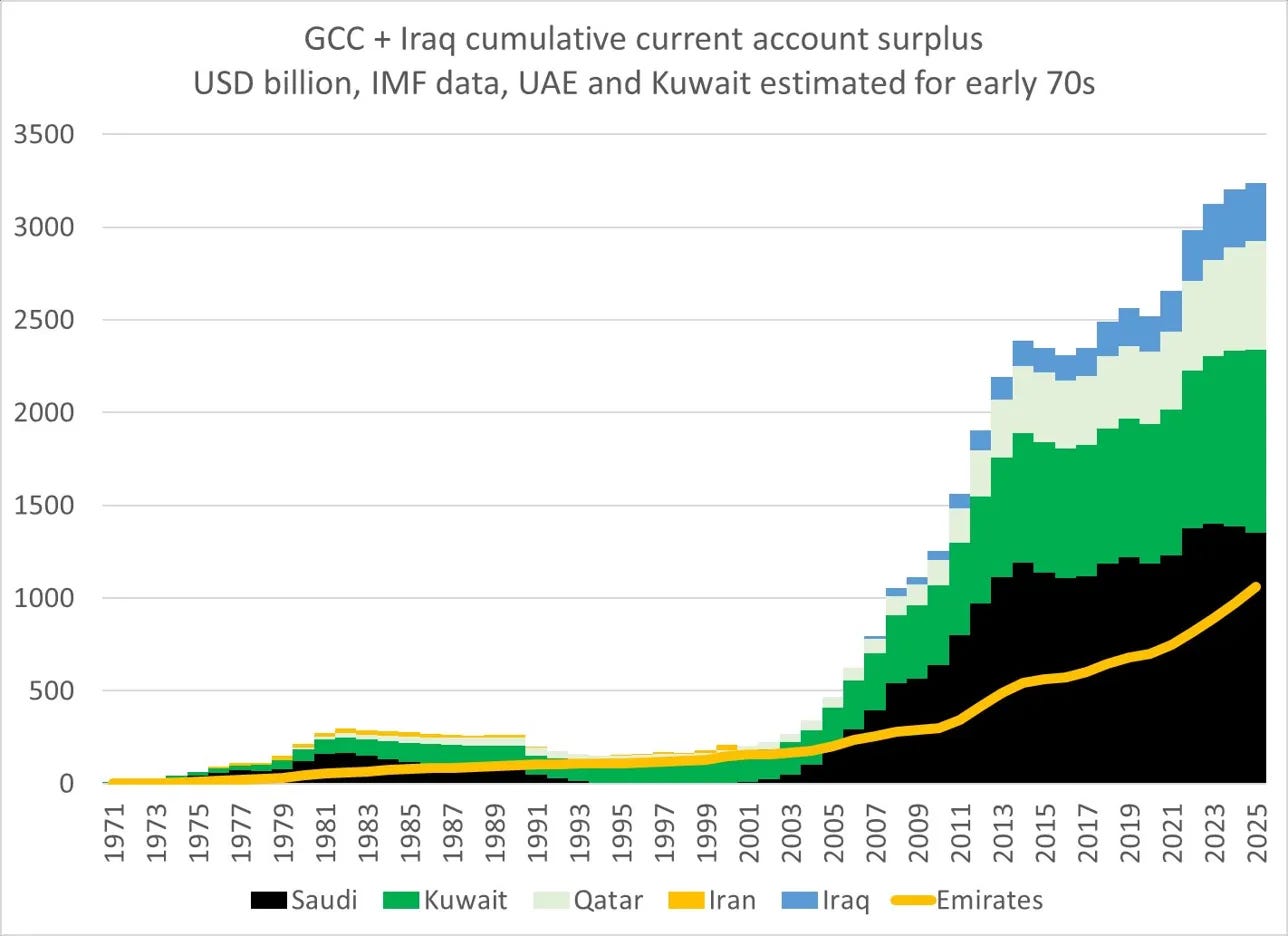

To grasp why swap lines are suddenly in focus, consider a chart few notice but that tells the entire story: the GCC + Iraq current-account surplus accumulation from 1971 to now.

From 1971 to 2000, the group’s total accumulated surplus was under $300 billion-essentially flat on a historical scale. Post-2003, as oil entered a super cycle, the curve steepened sharply. By 2025, the total has surpassed $3.2 trillion-with Saudi Arabia (black) taking the lion’s share, followed by Kuwait (green) and UAE (steady gold line).

That $3.2 trillion is the true source of Gulf financial power-not central bank reserves, but wealth accumulated over half a century from selling oil to the world and reinvesting in global assets.

But it’s also the vulnerability: The entire structure hinges on one condition-oil flows out, dollars flow in. When Hormuz closes, that cycle starts breaking link by link.

Gulf operating model for the past 50 years:

Oil exports → receive dollars

Reinvest dollars into Treasuries, sovereign wealth funds, global assets

Asset returns generate more dollar income

Self-reinforcing loop builds ever-greater financial power

When Hormuz is disrupted, the chain snaps at the first link:

Oil exports plunge → dollar inflows slow or halt for Qatar, Kuwait, Iraq

Government spending must continue → sell assets or borrow

Sell Treasuries → pressure on US bond market

Borrow → spike demand for dollars on international markets

This is why an Iran war isn’t just a Middle East geopolitical issue. It’s a shock to the dollar recycling system that’s hummed along for half a century.

2.2. Liquid asset picture: big but not infinite

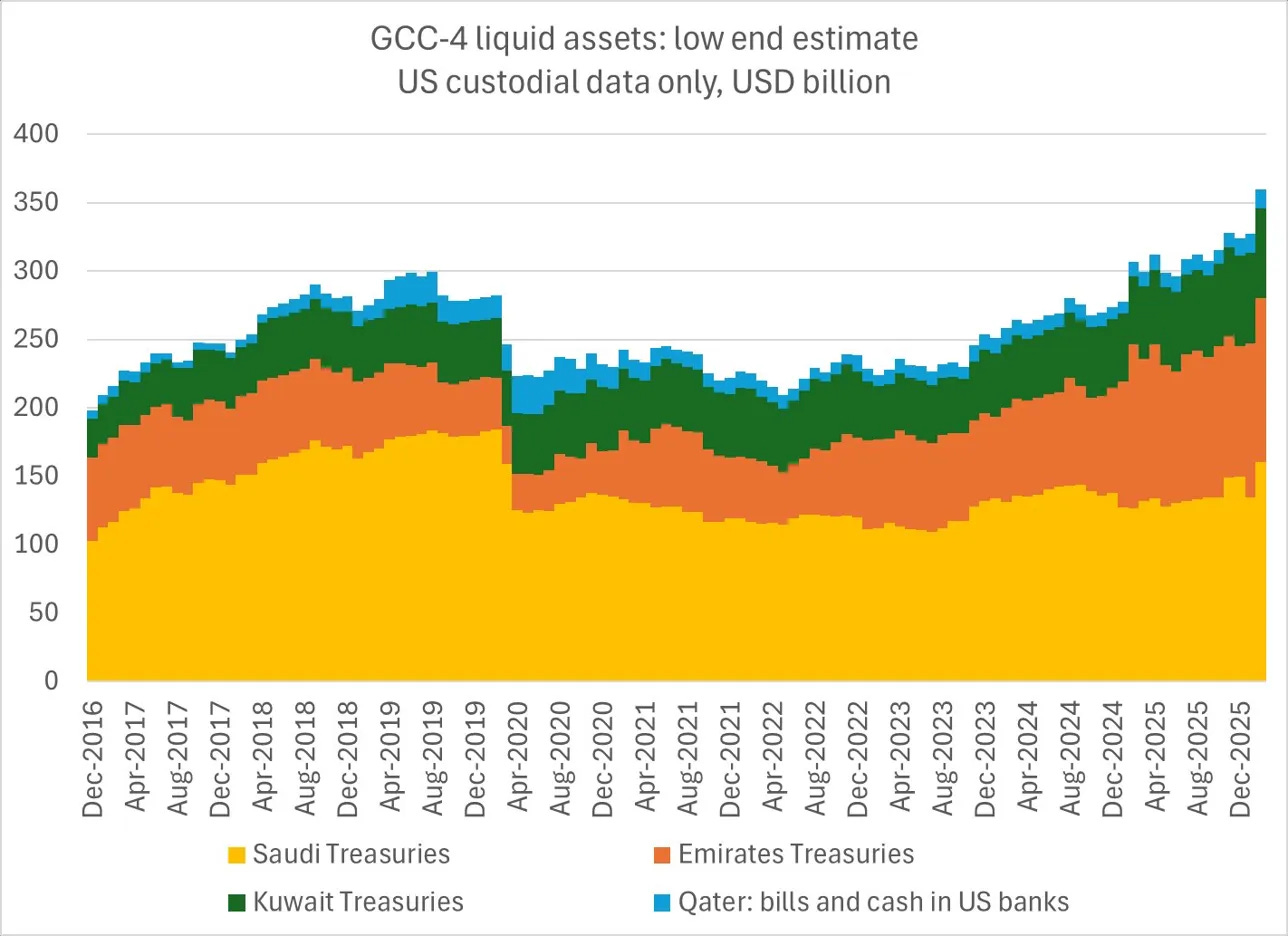

GCC-4 liquid assets-using only US custodial data, the lowball estimate-total around $355 billion at end-2025.

By country:

Saudi Arabia (gold): Largest share, $130-150 billion in Treasuries

Emirates (orange): ~$90-100 billion Treasuries in US custody

Kuwait (dark blue): ~$80-90 billion

Qatar (light blue): ~$20-30 billion in bills and US bank deposits

The total looks huge. But two deeper reads beyond the headline:

Layer one-liquidity structure:

Most of the $355 billion is in medium- and long-term Treasuries-not instantly withdrawable cash.

Only T-bills and short-term bank deposits are truly “liquid,” convertible to dollars in hours.

When GCC nations need dollars urgently amid slowing oil revenue, they sell Treasuries-pressuring the very US bond market Bessent aims to protect.

Layer two-burn rate vs. intake rate:

Few calculate this precisely. Pre-war, Saudi exported ~7 million bpd at ~$80/barrel-~560 million USD/day or >$17 billion/month in oil revenue.

If exports drop to 3.5-4 million bpd via Yanbu, revenue halves. That gap must be filled somehow-every month.

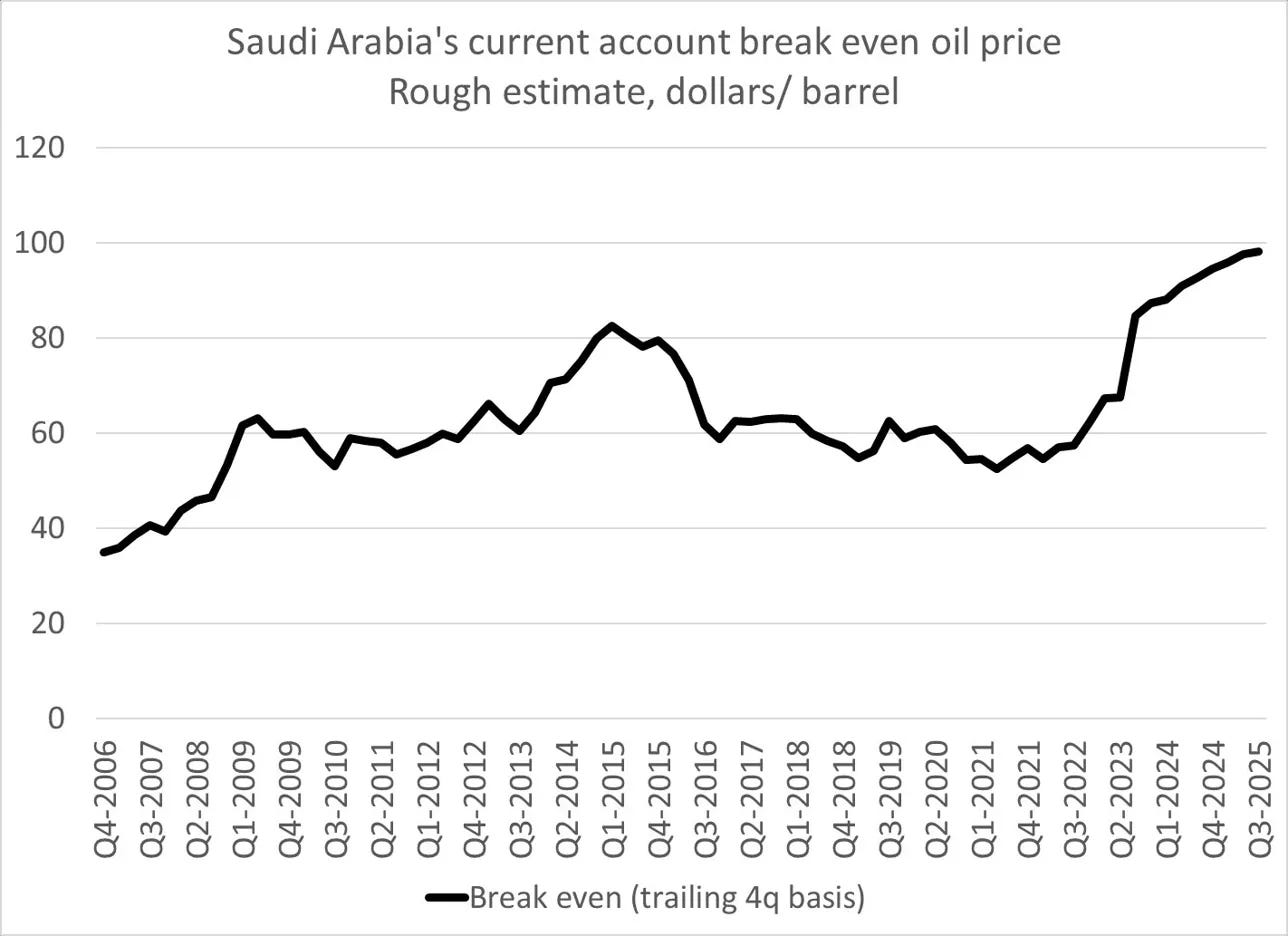

2.3. Saudi Arabia and the unsolvable break-even puzzle

Saudi Arabia’s current-account break-even oil price chart is one of the most alarming in this dataset.

The break-even price has climbed from around $35/barrel (2006) to nearly $100/barrel (Q3-2025)-nearly tripling over two decades. This is no coincidence:

Social welfare spending to maintain political stability after the Arab Spring

Vision 2030 with dozens of mega-projects-NEOM, Red Sea Project, Diriyah Gate

Military spending escalation, especially from 2015 (Yemen) to now (Iran)

Domestic energy subsidies remain high despite partial cuts

When Hormuz is disrupted and Saudi exports drop from 7 to 3.5-4 million bpd:

To fully offset that decline without cutting spending would require oil at around $170/barrel

An unrealistic number in the current environment

The gap must be filled by either (a) spending cuts, or (b) asset sales, or (c) borrowing

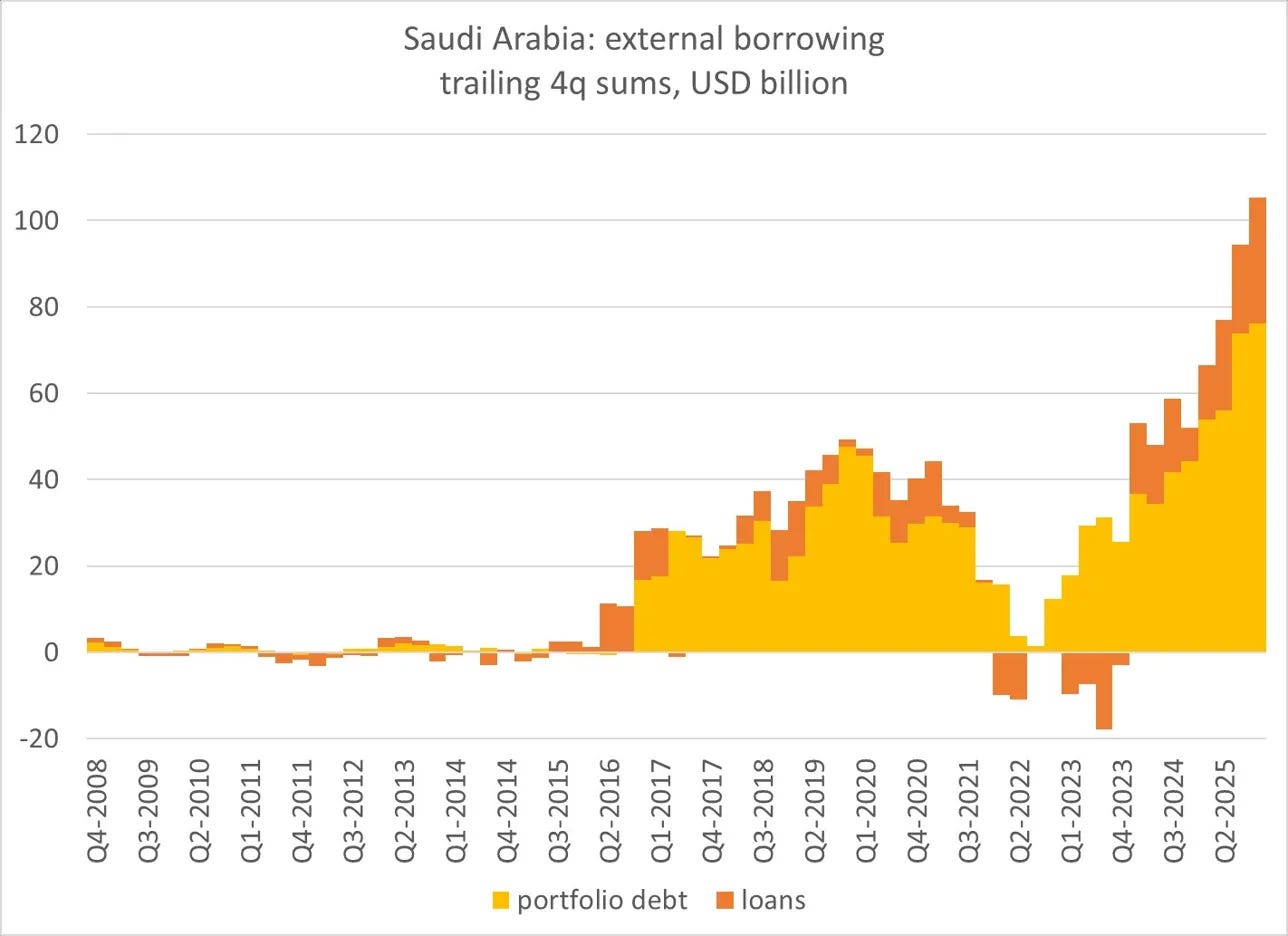

Saudi Arabia's external borrowing chart confirms the choice: From Q4-2022 to Q2-2025, total external debt (portfolio debt + loans) has surged from near zero to over $105 billion-the highest on record, far exceeding the 2015-2016 oil crisis.

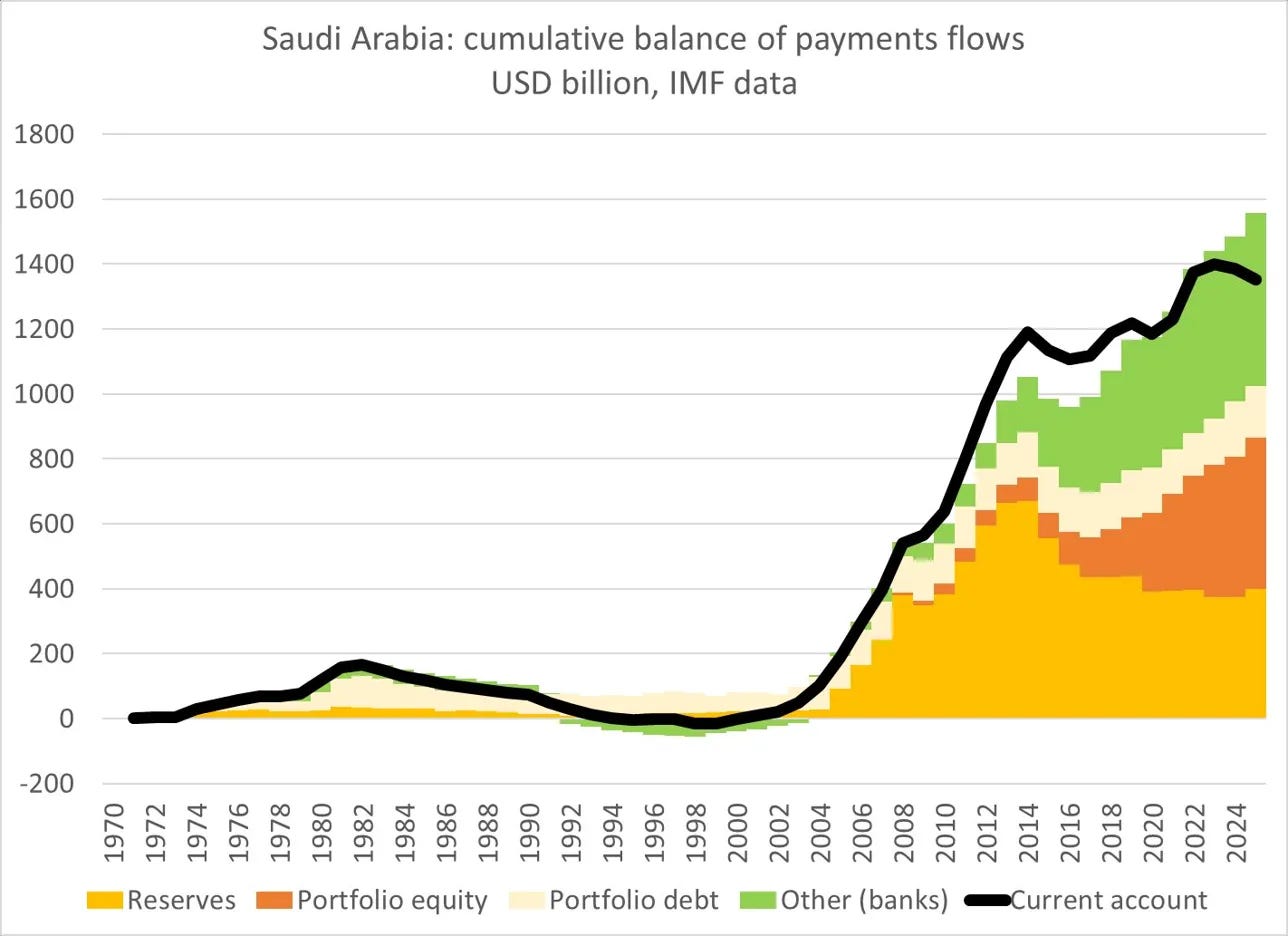

And the Saudi Arabia cumulative balance of payments flows chart puts this in longer historical context: The cumulative current account line (black) peaked above $1,200 billion in 2013, then flattened-and has recently begun showing signs of reversal. Allocations abroad in portfolio equity, portfolio debt, and other/banks will gradually need to be repatriated if financial pressures persist.

Key point: Saudi Arabia-the once-largest net lender to the global financial system-is becoming a net borrower. This reversal is not temporary if Hormuz does not fully reopen soon.

2.4. The Disrupted Cycle

Pre-war-GCC was a net capital provider:

Buying Treasuries → funding U.S. budget deficits

Depositing in London banks → lubricating the offshore dollar market

Investing in PE funds, Western infrastructure → recycling petrodollars into long-term capital

Post-Hormuz disruption-GCC is becoming capital-needy:

Selling Treasuries → pressuring U.S. yields

Borrowing from private placement markets → increasing competition for dollar funding

Requesting U.S. swap lines → requiring U.S. liquidity backstopping

In sum: Instead of quietly funding the U.S. Treasury as in the 1970s, GCC countries are now competing with the U.S. Treasury and emerging markets for dollar financing.

PART III-WHY UAE IS ASKING-AND THE REAL QUESTION ISN'T ABOUT MONEY

3.1. UAE Reserves: The Story of a Nation That Doesn't Really Need Cash

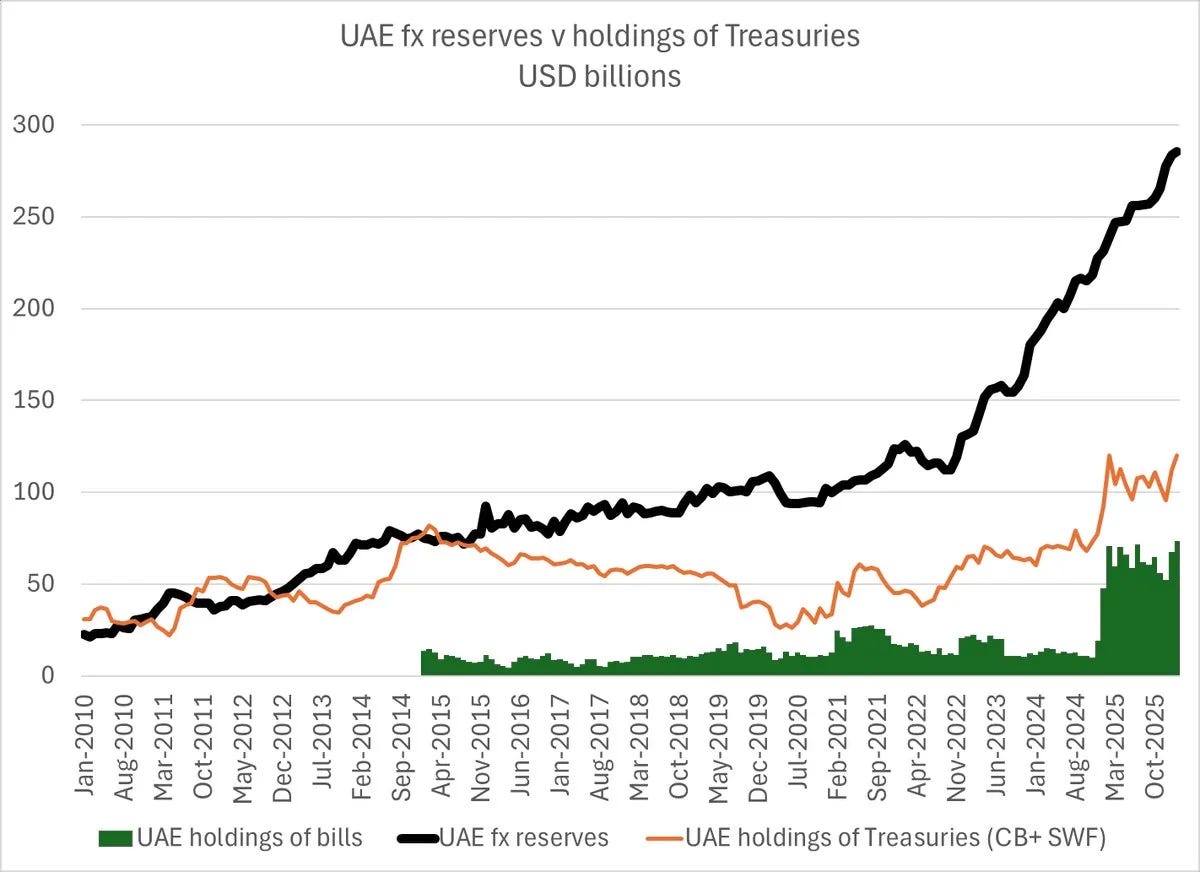

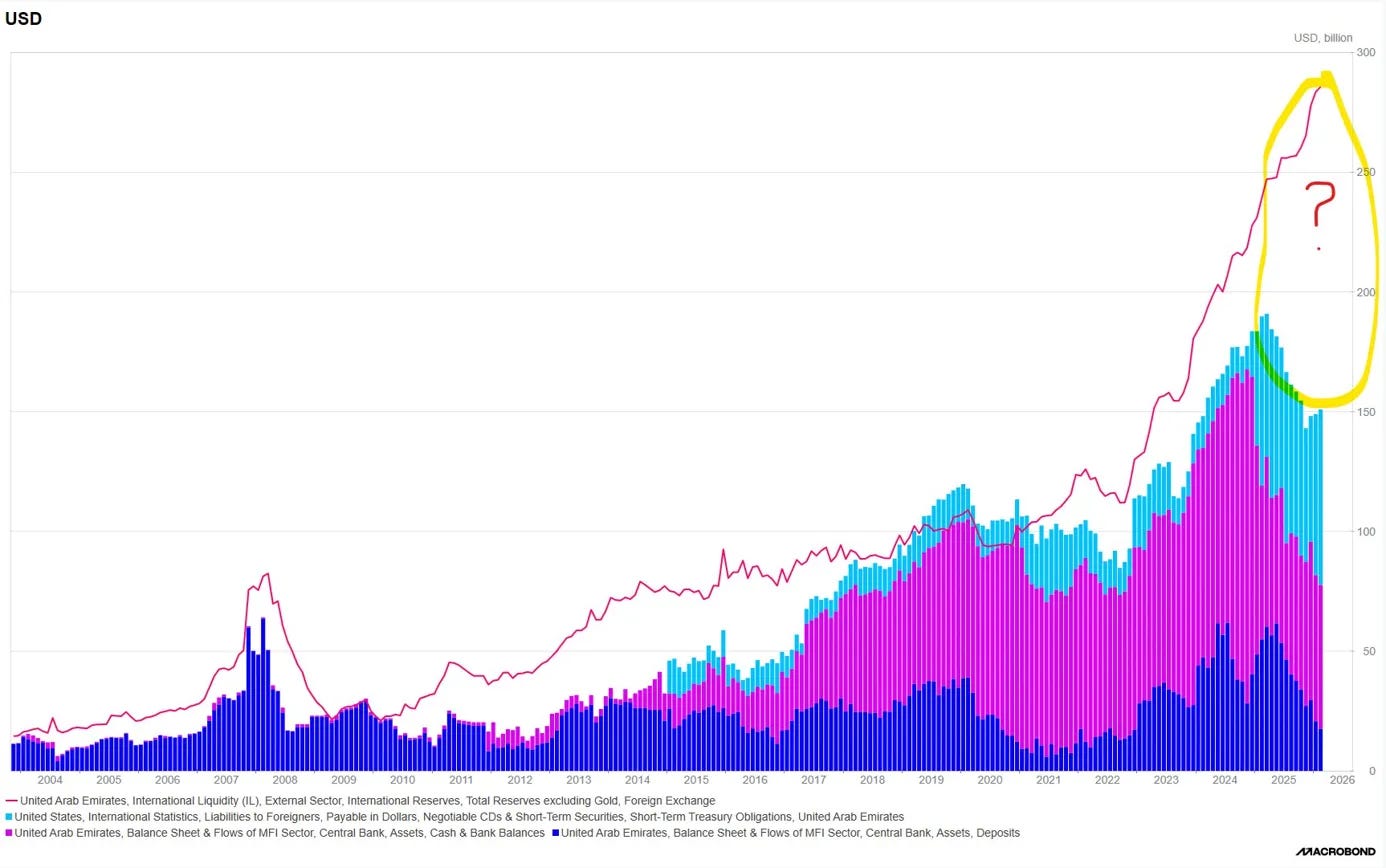

The UAE foreign exchange reserves chart poses a paradox that's easy to miss if skimmed-but explains nearly the entire story if read closely.

The black line-FX reserves-has risen almost uninterrupted over 15 years: from under $30 billion in 2010 to nearly $285 billion by end-2025. This isn't just growth; it's disciplined accumulation, reflecting a tightly managed financial system maximizing oil cycle gains.

In parallel, the asset structure tells a different story.

U.S. Treasuries holdings have fluctuated significantly-peaking early 2025 before dropping to ~$95–100 billion. But the most notable point isn't there.

It's in the T-bills.

From mid-2024 to early 2026, T-bills-the highest liquidity asset in the dollar system-surged above $70 billion, a record high. This isn't random portfolio tweaking. It's preparation: UAE is deliberately shifting from duration to liquidity, from yield to responsiveness.

If we stopped here, the conclusion would be clear: UAE is rich, liquid, and systematically defensive. They need no 'lifeline.'

But the second chart-with the question mark at the end-complicates the story significantly.

After peaking near $280–285 billion, the reserves line plunges sharply just as the Iran war escalates and Hormuz flows are disrupted. And crucially: Subsequent data turns opaque. No clear confirmation of the current position.

From here, three readings coexist-and none can be fully dismissed:

Official narrative: UAE still holds hundreds of billions in reserves and over $2 trillion in sovereign assets

Market narrative: System is stable, swap line is just 'insurance'

Cautious narrative: Data is missing, reserves are declining, and no one truly knows the current state

It's this overlap of the three narratives that is the problem.

In broader context:

~$70 billion in U.S. T-bills

~$300 billion in FX reserves

$2 trillion in SWF assets

→ On paper, UAE has liquidity far exceeding the scale of any U.S. support tool.

This creates an almost unavoidable paradox:

The U.S. is being asked to provide a 'backstop' for a nation with more liquid assets than the U.S. tool intended for support.

So why still need a swap line?

The answer lies in one subtle but decisive point:

A swap line doesn't solve a cash problem. It solves a confidence problem-in an environment where data is no longer absolutely reliable.

When markets aren't sure of true reserve levels, when data chains break, when SWF flows are no longer clearly visible-the very existence of a Fed credit line becomes an 'information proxy.'

It speaks for the data.

It substitutes for transparency.

And in a financial system that runs on expectations, that is sometimes more important than actual liquidity.

✮ This is the core paradox: The UAE may not need a swap line financially. But precisely because no one can confirm that with high certainty - they have reason to request it.

The swap line, in this case, is not a funding tool. It is a market perception stabilization tool.

3.2. When the IMF Says 'Fine'

In its most recent assessment before the conflict escalated, the International Monetary Fund offered a fairly clear verdict: The UAE has ample reserves, sufficient policy space and a flexible operating system to absorb adverse shocks. In other words, from the IMF's perspective, the UAE is not a short-term vulnerable economy:

High foreign exchange reserves, providing a 'buffer' against shocks

Fiscal and monetary policy room to maneuver

Central bank's operational capacity rated sufficient to handle volatility

However, delving into the data details reveals another layer of uncertainty - not about the size of assets, but about the quality and continuity of information. The UAE's balance-of-payments and capital flow data have characteristics that make assessment more difficult than for regional peers:

Irregular frequency and detail of data releases, lacking quarterly systematicity

Some data revisions creating 'series breaks,' disrupting time-series comparability

Some indirect indicators of sovereign wealth fund flows no longer maintained as before

The result is that while the big picture still shows a strong economy, the certainty about its current state is lower than the aggregate numbers suggest.

This information gap creates a systemic problem. When data is not clear enough, markets and policymakers must operate in an environment of more assumptions than confirmations:

Hard to pinpoint the exact reserve drawdown in the most recent period

Incomplete visibility into actual cash flows of sovereign wealth funds

Heightened 'information gap' risk in pricing financial stability

In this context, a mechanism like a Federal Reserve swap line is not just about liquidity - it is also a signal. It reduces the market's need to speculate on the system's true condition.

→ From this perspective, a paradox emerges: The UAE may not lack liquidity in the traditional sense, but data uncertainty creates demand for a tool to stabilize expectations. The swap line, therefore, is not just a financial instrument - it is also a tool to narrow information uncertainty in the system.

3.3. Signals, Market Structure and Geopolitical Factors

Putting the pieces together - large but volatile reserves, unconfirmed data, and a swap line request at a moment of tension - the most reasonable interpretation lies not in a single cause, but in a combination of drivers. A neutral view suggests this request may be systemic signaling, rather than reflecting urgent liquidity needs:

Bolsters market confidence amid incomplete data

Reduces market speculation on true reserve status

Positions UAE's role in the global dollar system at a higher level

In this context, the swap line can be seen as an 'expectation anchor,' not necessarily to be drawn upon but with significant market behavior impact.

Meanwhile, a key technical debate centers on risks to the U.S. bond market that must be properly framed. A common concern is that GCC countries might sell U.S. Treasuries for liquidity, pressuring yields and creating financial contagion. Mechanically, however, several factors substantially mitigate this risk:

Most liquid assets are in short-term T-bills that can roll off naturally without selling

FIMA Repo Facility allows direct dollar borrowing against Treasuries

Short-term liquidity needs can be met without disrupting long-term bond markets

This suggests that if risks exist, they are more likely in indirect channels like investment flows or deeper market structures than direct asset sales.

At the same time, geopolitical factors - especially the potential diversification to other currencies - play a key psychological role. Purely economically, shifting to other currencies does not solve dollar liquidity needs and adds FX risk. Yet its impact lies in perception:

Any signal of reducing the dollar's role in energy trade carries major symbolic weight

Existence of alternative financial networks heightens market sensitivity to policy signals

Policy responses may be driven more by systemic stability needs than actual liquidity demands

→ Combining these factors reveals the swap line request reflects not just a specific financial issue, but sits at the intersection of three layers: market expectations, technical financial system structure, and geopolitical context. This overlap makes the story complex - and not explainable by simple economic logic alone.

PART IV - PIMCO AND PRIVATE MARKETS: WHEN THE LENDER OF LAST RESORT ISN'T THE FED

4.1. Public Markets Shut - Private Markets Quietly Roll

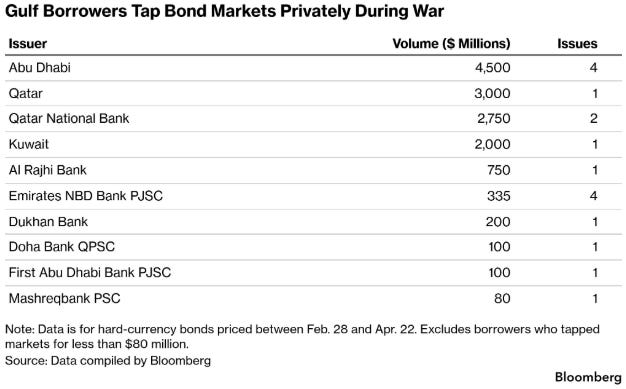

While the world debates swap lines, something more important is happening quietly: Private markets are resolving GCC liquidity issues themselves - faster, more discreetly, but at a higher cost than any official channel.

Pre-war: GCC sold about $50 billion in public bonds in just the first two months of 2026. This was the busiest Gulf bond market period ever.

Post-conflict start: Public markets nearly shut down completely. Not due to lack of demand - but because geopolitical uncertainty was too high for transparent, public risk pricing.

Alternative solution: private placement. Bloomberg data shows clearly from February 28 to April 22, 2026:

Total: over $13.8 billion in under two months.

4.2. PIMCO: The True Lender to the Gulf

The bulk of this capital-more than $10 billion-came from a single buyer: PIMCO, the world's largest bond fund with $2.27 trillion in assets under management.

Why private placement-and why it's more expensive:

Public issuance requires roadshows, SEC registration, detailed disclosures-taking weeks and exposing financial stress to the market

Private placement can close in days, without broad disclosure, with flexible terms

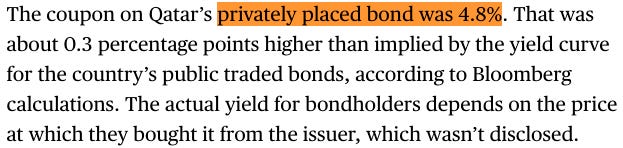

The trade-off: higher interest rates. Qatar's bonds were issued with a 4.8% coupon-0.3 percentage points above the benchmark yield curve

The significance of PIMCO's role:

PIMCO just opened its Dubai office in 2025-timing is no coincidence

This is a fund positioning itself as the Gulf's 'strategic lender' amid restructuring

With public markets closed and official channels still in talks, private capital is setting the terms

The worrisome precedent this sets:

The Fed's 'lender of last resort' function is being effectively privatized

GCC is paying a crisis insurance premium to private capital instead of receiving conditional support from public institutions

This is sustainable short-term-but creates new dependence on an actor without a system-stabilization mandate

✮ This is the week's least-reported story: While Bessent and US Congress debate swap lines, PIMCO has already filled the gap-on a larger scale, faster, but at a higher price and with less transparency than any official channel.

PART V - NIGHTMARE SCENARIO: WHEN OIL AND THE DOLLAR RISE TOGETHER

5.1. Historical inverse correlation and conditions for its breakdown

In modern economic history, the dollar and oil have trended inversely:

Weak dollar → higher oil as dollar-denominated commodities become cheaper for the rest of the world → rising oil demand

Strong dollar → oil typically falls by symmetric logic

This mechanism acts as a natural shock absorber in the system

But specific conditions can break this correlation-and we're closer than ever:

Dangerous chain reaction:

Hormuz disruptions continue → prolonged oil supply shock → oil prices surge

GCC sells Treasuries for dollars to cover deficits → US yields rise → dollar strengthens further

Strong dollar + rising oil simultaneously → double squeeze on every oil-importing country with dollar debt

Fed is trapped: can't cut rates with energy-driven CPI surge, can't hike further with weakening growth

5.2. Why 2026 is more dangerous than 2022

In 2022, oil and the dollar rose together briefly amid the Ukraine war-and that was enough to trigger a crisis wave in emerging economies. In 2026, the structure is far more perilous due to three factors resonating in ways 2022 never saw.

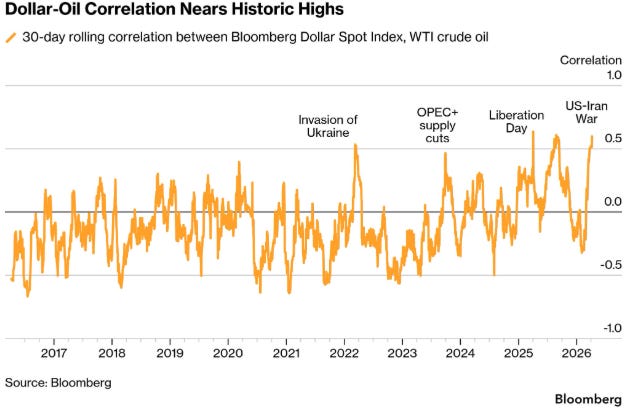

Factor 1-Much larger shock magnitude-and dollar-oil correlation approaching historical peak:

Bloomberg chart of 30-day rolling correlation between Dollar Spot Index and WTI crude tells a stark story of markets breaking historical rules.

For most of 2017-2021, this correlation hovered around zero and often negative-meaning a strong dollar meant weak oil, and vice versa. This was the natural shock absorber global finance relied on for decades.

But look at the points where correlation abruptly turned sharply positive-Ukraine Invasion (2022), OPEC+ supply cuts (2023), Liberation Day (2025), and especially US-Iran War (2026)-a clear pattern emerges: each was a geopolitical supply shock, not an economic demand shock.

And the most alarming point: correlation during the US-Iran War phase is nearing the highest in the entire dataset-close to 0.5, higher than Ukraine 2022.

What does this mean? The natural shock absorber is being disabled. Instead of a rising dollar making oil cheaper for the rest of the world, both are climbing together-a state economic theory deems temporary but which can persist when supply is controlled by geopolitics rather than markets.

IMF calls this the most severe oil supply shock in history

Hormuz isn't a temporary accident-it's a reusable geopolitical tool

No clear end timeline, no sustainable 'ceasefire rally' for markets to price in

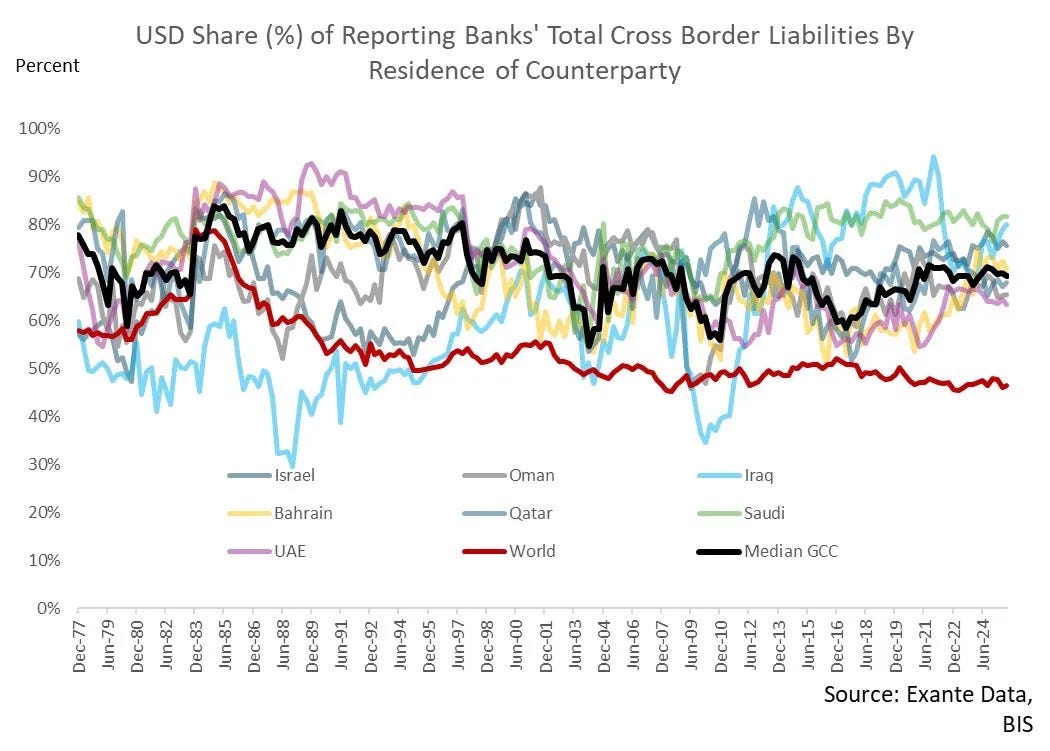

Factor 2-GCC's deeper dollar dependence than any region globally-and that complicates everything:

The chart reveals something anomalous: while the dollar's share in global transactions (red line-World) has steadily declined from around 58% to 47% over nearly 50 years-reflecting slow but steady global currency diversification- GCC median (black line) has held steady at 65-75% over the same period.

UAE and Saudi Arabia are even higher than the median-often in the 70-80% range.

What does this mean in practice?

When Hormuz closes and oil revenues drop, GCC doesn't just lack cash-they lack specific dollars, as most of their debt, contracts, and transactions are dollar-denominated

Switching to renminbi or any other currency doesn't solve this-it just adds FX risk atop liquidity risk

GCC's deep dollarization-far above global averages-is why Hormuz disruptions quickly translate into pressure on dollar markets themselves, not just a regional oil issue

This is also why the UAE's threat to 'switch to the renminbi' lacks economic credibility: a banking system where 70-80% of cross-border liabilities are in dollars can't de-dollarize anytime soon, no matter how much it wants to.

Factor 3 - The Fed is stuck precisely at the worst possible point:

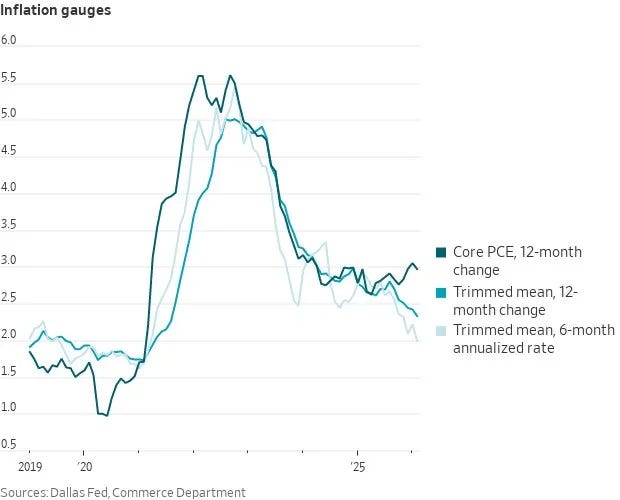

The chart below paints an uncomfortable picture for Fed policymakers. After Core PCE peaked near 5.5% in 2022-2023 and gradually eased to the 2.5-3.0% range, all three metrics - Core PCE 12-month, Trimmed mean 12-month, and Trimmed mean 6-month annualized - are starting to diverge in a worrying direction.

In particular, the Trimmed mean 6-month annualized rate - the most sensitive gauge to short-term inflation trends - had fallen to around 2% before the energy shock from the Iran war began to filter through. As oil prices surge, this indicator will be the first to reflect the new pressures - and it will drag Core PCE along in the months ahead.

This is the trap from which the Fed has no clean escape:

Can't cut rates: energy inflation is pushing CPI higher, and after the painful lessons of 2021-2022, no governor wants to be seen in hindsight as having 'pivoted too early'

Can't hike further: growth is slowing, credit markets are strained, and rate hikes amid a supply shock only deepen the recession without addressing the root of inflation

No 'pivot' in sight: this is exactly the trap seen in 1973-1974 and 1979-1980 - two episodes where the Fed reacted slowly to supply-driven inflation and paid the price with prolonged stagflation

The combination of these three factors sets off a chain reaction where the nightmare scenario isn't Hormuz closed forever - but Hormuz closed long enough to:

Drive the dollar and oil higher sustainably while the Fed is paralyzed

GCC - with 70-80% dollarization - forced to sell Treasuries to meet urgent dollar demand, pressuring US yields

Pressure on US yields → stronger dollar → self-reinforcing spiral

And all this unfolds just as the US needs the most stable Treasury market to fund its massive budget deficit

✮✮ This is the deepest reason why the UAE swap line story isn't really about the UAE. It's the story of how a geopolitical shock in the Middle East's 33-mile narrow strait can simultaneously trigger three structural vulnerabilities in the global financial system - persistent inflation pinning down the Fed, deep dollarization forcing GCC to dump Treasuries, and the US bond market under pressure from its former biggest buyers.

PART VI - THREE THINGS THAT ARE REALLY HAPPENING AND NO ONE IS READING

6.1. The petrodollar is being renegotiated - not broken

Since the 1974 Nixon-Saudi pact, oil priced in dollars has been a given of the world economic order. This underpins what Barry Eichengreen calls America's 'exorbitant privilege.'

But 2026 marks the first time in modern history that a Gulf state has publicly wielded a shift to the renminbi as leverage in negotiations with the US. Not because they truly want the renminbi - but because they are repricing the relationship.

The GCC's cumulative current account surplus chart reveals the essence of that negotiation: Gulf states have amassed over $3.2 trillion in surpluses over 50 years - largely recycled into US assets, funding America's budget deficits, and sustaining dollar dominance.

That relationship isn't as asymmetric as Washington often assumes:

GCC needs dollars for oil trade → true

US needs GCC to buy Treasuries to fund deficits → also true

GCC needs US security guarantees → true

US needs military bases in the Persian Gulf → also true

This is mutual interdependence - not a one-way patronage. And GCC states are learning to wield their leverage.

The petrodollar isn't dead. But it's being renegotiated at a higher price - and America will have to pay it somehow.

6.2. Global capital flows are reversing - and few are noticing

This is the most important structural shift of the decade - and it's happening quietly, without full reflection in any headlines.

This reversal wasn't planned by anyone. It's the natural consequence of a war disrupting the central link in the petrodollar recycling loop.

6.3. The gap between 'asking' and 'getting' - and who really decides

One key detail overlooked in most coverage: The Fed and Bessent don't fully agree on the UAE swap line.

Bessent: Supports it. Argues from the angle of protecting Treasury markets and dollar funding stability. A reasonable priority from a Treasury perspective.

Fed's FOMC: Multiple signals suggest reluctance to approve. Reasons:

UAE lacks the market integration with the US of standing partners

Dangerous precedent: If UAE gets one, Kuwait, Qatar, Iraq have similar claims

Fed doesn't want swap lines to become a geopolitical or oil-deficit funding tool

UAE financial data lacks Fed-standard transparency

Trump: Wants to help for strategic reasons - and possibly personal business ones (UAE invested $500 million in the Trump family's World Liberty Financial). But can't order the FOMC.

Real-world implications:

ESF is the most legally feasible path - Bessent can deploy it without FOMC approval

But ESF has only ~$44 billion in actual resources - smaller than UAE's T-bills held in US custody

A symbolic swap line carries geopolitical value even if never drawn - this could be the endgame

6.4. What Bessent Wants - and Why the Answer Is More Worrying Than the Question

This is where all the arguments in today's piece converge.

When technical issues already have technical solutions but Bessent still wants swap lines

GCC doesn't need to sell Treasuries to get dollars (FIMA Repo and bills roll-off solve that). UAE isn't short of liquidity by any financial metric. ESF is smaller than UAE T-bills held at US custodians. The Fed hasn't been consulted and isn't enthusiastic.

So what is Bessent trying to do?

The answer lies in a statement he made on X after being questioned: “Extending permanent swap lines can be a major first step in creating new U.S. dollar funding centers in the Gulf and Asia.” And in his Senate hearing: “I applaud our allies’ foresight in exploring additional financial buffers during periods of market quiescence.”

Asia doesn't lack dollar funding centers. China has trillions of dollars in its state banking system. TSMC and Samsung are generating dollars at a blistering pace at current chip prices. Hong Kong is one of the world's largest offshore dollar centers.

The issue isn't a lack of “dollar funding centers.” The issue is that Bessent wants dollar funding centers under US influence - not market-natural dollar funding centers.

Bessent's Three Parallel Ambitions

When reading Bessent's statements on swap lines as a whole, three ambitions emerge clearly:

Prevent uncontrolled Treasury sales: The technical reason stated publicly - swap lines to avoid GCC selling Treasuries and pressuring markets. Setser points out this has been addressed by FIMA Repo. But the reason is still used because it sounds convincing.

Reward allies and sustain dollar hegemony: This is Miran's blueprint - swap lines as an incentive to stay under the “US security and economic umbrella.” Bessent is executing it by expanding the swap network to GCC and Asia, directly competing with China's 36 swap lines.

Restructure Fed-Treasury power dynamics: This is the deepest layer. Bessent has criticized the Fed for expanding its “supervisory footprint” post-2008. White House executive orders have already curtailed the Fed's bank supervision role. Now, by using ESF instead of FOMC to issue swap lines, Bessent is taking another tool from the Fed's hands - and turning it into a Treasury weapon.

6.5 Who Will Coordinate the Global Response in the Next Crisis?

Looking back to 2008, the answer was almost undisputed: The Federal Reserve played the central role, swiftly coordinating with a slew of major central banks to provide dollar liquidity to the global system. That was feasible not just because of the Fed's financial firepower, but more importantly because of trust:

Central banks viewed the Fed as a neutral technical referee

Swap lines were seen as systemic stability tools, not political ones

Coordination happened fast because there was no doubt about motives

This “neutrality” was the foundation enabling efficient crisis response.

In the current context, if swap lines increasingly become selective tools - extended to some partners and potentially restricted from others - that perception could shift. Then, the question moves from liquidity mechanics to institutional trust:

Will major central banks like the European Central Bank, Bank of England, or Bank of Japan still see the Fed as a neutral referee?

Will swap lines be viewed as common stability mechanisms, or conditional tools?

And if there's doubt about the tools' consistency, how will coordination speed and effectiveness suffer in a crisis?

This isn't theoretical - it's a question about the architecture of the global financial system - where trust among central banks matters as much as balance-sheet size.

From this perspective, the UAE swap-line story is no longer confined to one country. It reflects three coexisting logics in the system:

Technical logic: existing tools (like repo or market mechanisms) can already handle short-term liquidity needs

Strategic logic: swap lines can expand the dollar system's sphere of influence

Institutional logic: control and use of financial tools are shifting between power centers

These three logics don't exclude each other - they coexist and shape how the system operates.

→ Thus, the core question is no longer “whether one country gets a swap line,” but: when a tool once seen as neutral becomes more policy-dependent, how will the global financial system coordinate in the next crisis - when trust levels aren't what they used to be?

CONCLUSION: THE DOLLAR, THE WHIP, AND THE 33-MILE STRAIT

The UAE swap-line story, when read correctly through layers of data - from tool mechanics, to GCC reserve structures, to private placement flows, to Saudi Arabia's break-even math - isn't about one country needing cash.

It's a story about three major shifts happening simultaneously - and a fourth, quieter one, reshaping who controls the global dollar system in the decades ahead.

First - The petrodollar cycle is being disrupted for the first time in 50 years:

GCC accumulated $3.2 trillion in surpluses over half a century → now it's reversing

Saudi Arabia Borrows Record Foreign Currency → From Creditor to Debtor

Break-even Chart at $100 and Climbing, External Borrowing at Peak → Not a Good Sign if Hormuz Doesn't Open Soon

Monday - The 'Lender of Last Resort' Function Is Being Effectively Privatized:

PIMCO Pumps Over $10 Billion via Private Placement → Faster, More Discreet, but Costlier

While Official Channels Are Still in Discussions, Private Markets Have Already Solved It

Sustainable in the Short Term but Creates New Dependencies and Dangerous Precedents

Tuesday - The Petrodollar Is Being Renegotiated, Not Broken:

UAE Doesn't Want Renminbi - They Want Recognition on Par with Japan, UK, EU

This Is a Negotiation Over Sharing War Costs and Geopolitical Status

The US Is Paying the Price for Its 'Exorbitant Privilege' - By Guaranteeing the System Even for Countries Richer Than Its Own ESF

Wednesday - And Here's What Few Are Talking About - The Power Architecture of the Dollar System Is Changing from Within.

In Congressional Testimony, Kevin Warsh - Who Is All but Certain to Become the Next Fed Chair - Said Something Most Media Overlooked Amid Focus on the 'Is He a Trump Sock Puppet?' Question: The Fed Will 'Play a Supporting Role in Ensuring That the Financial System Is as Safe as It Can Be and Work with Bessent and Rubio, Because It's Outside of the Conduct of Monetary Policy.'

This Isn't Polite Talk. This Is an Institutional Commitment.

In Every Major Financial Crisis Since 1987 - From LTCM to 2008 to COVID - The Federal Reserve Played a Central Role Not Because of Balance Sheet Size: Trust in the Neutrality of Its Tools. The ECB, Bank of Japan, and Bank of England Coordinated with the Fed in 2008 Not Because They Were Asked - But Because They Believed the Fed Was 'Fixing the Plumbing,' Not Playing Geopolitical Chess. Swap Lines Were Extended to 14 Central Banks in Weeks Because No One Doubted the Motives Behind Them.

If Warsh Is Confirmed and Executes That Commitment - The Fed Becomes a Strategic Partner in the Bessent-Rubio 'Economic Statecraft' Agenda - The Nature of the System Changes in a Way No Single Presidential Term Can Reverse.

The Bessent-Warsh Duo Would Create an Architecture That Has Never Existed Before:

Treasury Controls Swap Lines via ESF - No FOMC Approval Needed

The Fed, Under Warsh, Is No Longer an Independent Counterweight but a 'Supporting Actor' for Foreign Policy

Swap Lines Become a Two-Way Tool: Rewards for Loyal Allies, Implicit Threats to Those Challenging Washington

China, with 36 Separate Swap Lines, Is Building a Parallel Network - And the US Is Responding by Expanding the Dollar Network on Geopolitical Rather Than Technical Logic

That Could Be Effective in the Short Term. Bessent Has Market Credibility. Warsh Understands Financial Mechanics. And in a World Where China Uses Swap Lines as Geopolitical Weapons, Responding in Kind Isn't Unreasonable.

But Gillian Tett's Question - 'Who Will Organise a Collective Global Response if Another Financial Crisis Hits?' - Has No Clear Answer in This New Architecture.

In 2008, Washington Could Coordinate Because Other Central Banks Trusted the Fed. Will They Still Trust It When the New Fed Chair Publicly Declares Coordination with Bessent and Rubio? When Swap Lines Could Be Withdrawn from Countries Challenging Trump? When the Line Between 'Systemic Stability' and 'Geopolitical Rewards' Is Blurred?

No One Knows the Answer - Because There's No Precedent.

✮✮✮ The Answer to 'Will the UAE Get a Swap Line?' Won't Come from Any Washington Meeting Room - And That Question Is Now the Smaller One.

The Bigger Question Is: Once Warsh Is Confirmed and the Bessent-Warsh Duo Starts Executing 'Economic Statecraft' with Swap Lines as a Geopolitical Weapon - How Will the Global Financial System Coordinate in the Next Crisis, When Trust in the Fed's Neutrality Is No Longer Assured as in 2008?

The UAE Swap Line Story Is the First Spark. Warsh Could Be the One Holding the Torch That Turns It into a Restructuring of the Global Financial Architecture Whose Consequences We Don't Yet Fully Grasp.

The Rest of That Sentence - As Always in Financial History - Will Be Decided by Geopolitics, Not Economics. And This Time, Geopolitics Is Entering the World's Largest Central Bank.