In case you missed our recent top articles:

“The factory of the world is now competing with the world’s factories - and winning in ways that were never supposed to be possible.”

“The world's factory is now not only producing for the world but is competing directly with the world's factories - and winning in ways that were previously thought impossible.”

- Michael Pettis, Carnegie Endowment for International Peace

Some economic stories unfold so slowly that people fail to realize they are reshaping the world order - until goods appear on their own streets, carrying absurdly low prices, surprisingly high quality, and a difficult question: is this driven by true market forces, or by a system where conventional market rules no longer apply?

They begin much more quietly: a Chinese SUV appears on the streets of London at a lower-than-expected price. A solar panel so cheap that European manufacturers cannot fathom where their rivals are making a profit. An EV sensor that once sold for 200 yuan, now squeezed down to 10 yuan. A container leaves the ports of Shanghai, Ningbo, or Shenzhen - carrying no weapons, but something with a more silent destructive power: overcapacityThis advantage is most evident in metal refining. China holds a very high share of many strategic materials such as

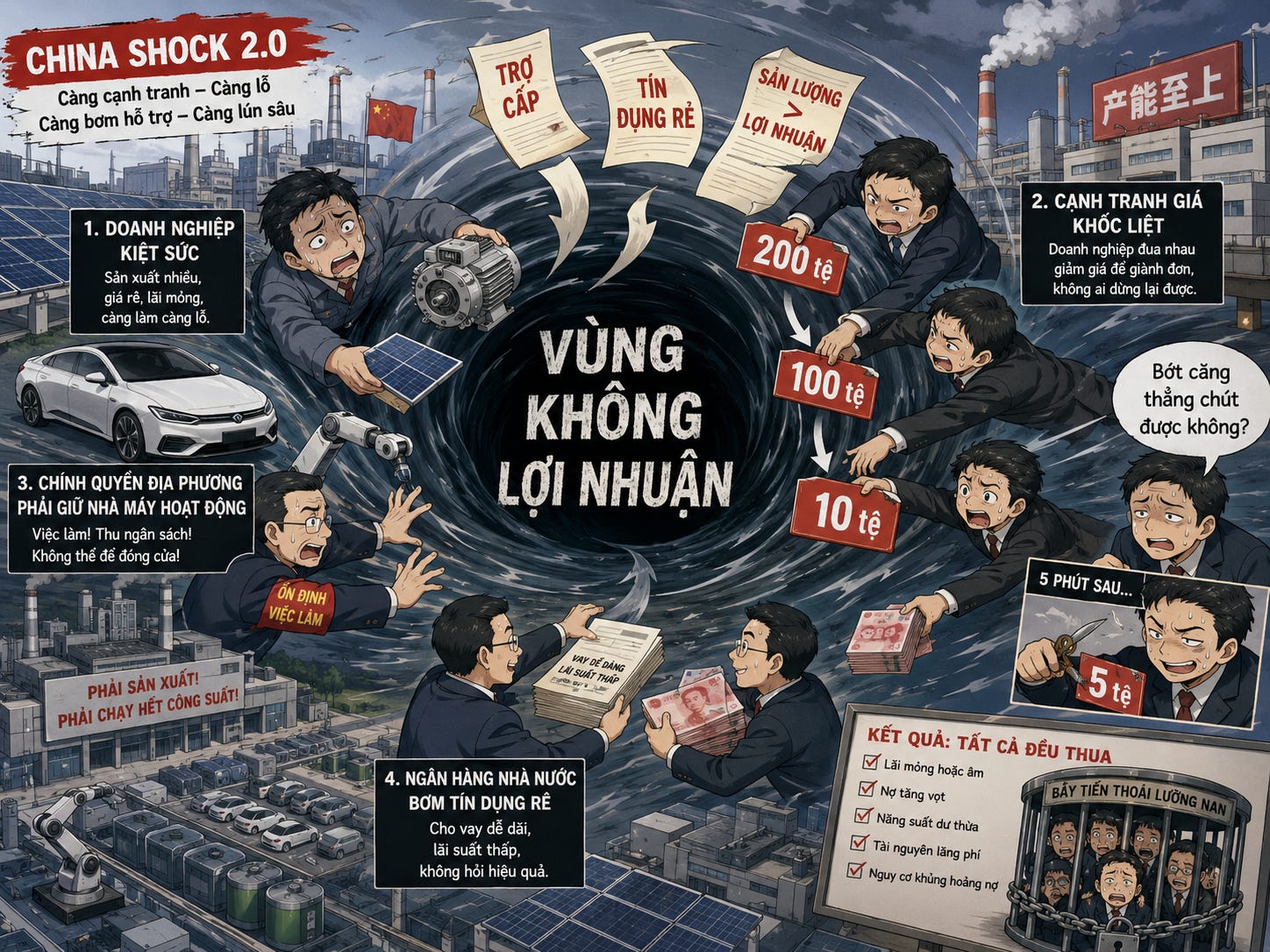

That is China Shock 2.0.

China Shock 1.0, following China's accession to the WTO, was a story of cheap labor, low-cost consumer goods, toys, textiles, furniture, and electronics assembly. That shock redrew the global industrial map, but the West still had a comfort zone to reassure itself: they could lose the bottom of the value chain as long as they held the higher ground - automobiles, machinery, chemicals, industrial equipment, and green technology.

China Shock 2.0 strikes directly at that very comfort zone.

This time, China is not just exporting t-shirts, toys, or assembled phones. China is exporting EVs, batteries, solar panels, robots, sensors, industrial equipment, refined materials, and all the input layers underlying the green economy. This is no longer a story of a country selling cheaper goods. This is the story of a massive industrial ecosystem - fueled by cheap electricity, cheap credit, multi-tiered subsidies, favorable exchange rates, large-scale metallurgy, and state industrial policy - colliding with the rest of the world.

And the pace of change is far exceeding market expectations.

In March 2026, China's Jaecoo 7 SUV - with a starting price of approximately £29,000 - became the best-selling car in the UK. By April 2026, China exported In April 2026, China exported in a single month, up , up 51% year-on-year. In the first four months of the year, total vehicle exports reached, with a value of year-on-year. Export value reached. If this pace continues, China could export more than 10 million vehicles in the full year 2026.

To put the scale of the shock into perspective: Germany - Europe's historic automotive powerhouse - net exported about 1.5 million vehicles in 2025. China could exceed that figure by 6–7 times in just one year.

Not with warships.

Not with missiles.

Not with diplomatic pressure.

Only with cars, batteries, solar panels, robots, and the supply chains that the rest of the world still relies on.

But if we only view China Shock 2.0 as an export offensive from Beijing, we miss the most important paradox: those operating the machine are also being crushed by itThis advantage is most evident in metal refining. China holds a very high share of many strategic materials such as

Chinese enterprises do not always win. Many companies are selling more but earning less. Output is rising, prices are falling, and profit margins are being eroded. Founders who once dreamed of technological innovation are now dragged into an inescapable price war. Local governments want to keep factories open to protect GDP, VAT, and jobs. Banks continue to extend credit to avoid a wave of bankruptcies. And Beijing, despite understanding the problem of neijuan - the race-to-the-bottom competitive spiral - still cannot easily stop the machine it has built.

This is what makes China Shock 2.0 different from a typical trade war.

In a classic market economy, oversupply self-corrects: prices fall, weak firms exit the market, capacity is cut, and a new equilibrium forms. But in China, that feedback loop is distorted by a much more complex system:

VAT is tied to the place of production, giving local authorities an incentive to keep factories running;

cheap credit from state-owned banks extends the life of weak enterprises;

multi-tiered subsidies prevent excess capacity from being quickly shut down;

exchange rates and domestic deflation make exports cheaper in real terms;

cheap electricity, metallurgy, and refined materials create supply chain advantages deeper than the final product.

The result is a strange machine: the more the overcapacity, the more they must produce; the more the losses, the more they need to export; the stronger the exports, the more the world builds protectionist walls; and the more they are blocked, the greater the internal pressure of overcapacity within China becomes.

EVs are only the most visible front. Behind them lies a larger structure: China is not just manufacturing final products, but controlling multiple layers of materials beneath them - from batteries, graphite, rare earths, gallium, silicon, cathode materials, and permanent magnets to machinery and intermediate components.

This is why 'diversifying away from China' sounds much simpler than it actually is. A company can move an assembly plant to Mexico, Vietnam, or Eastern Europe. But if the backbone of the supply chain still comes from China, the world is only moving the surface - while the foundation remains within the Chinese ecosystem.

This week's question, therefore, is not just: “Are Chinese cars too cheap?”

The bigger question is:

Why can't this overcapacity machine stop itself? What keeps it running even when profits vanish? And as that machine crashes into the geopolitical walls being built from Washington and Brussels to New Delhi - what will happen to global trade for the remainder of this decade?

This week's article will cover five parts:

Part I - Neijuan: Anatomy of the overcapacity machine and why it cannot stop itself.

Part II - Real Data, Real Paradoxes: Correctly reading the Chinese EV landscape.

Part III - Batteries, the Electro-state, and the Weaponization of Supply Chains: Why China's advantage lies deeper than the final product.

Part IV - The World's Response: The new map of a bloodless war.

Part V - Three Scenarios for the Rest of the Decade: From prolonged overcapacity and restructured competition to the risk of disruption.