In case you missed our best recent articles:

A look at the German economy today:

Industrial production is down 15% from its peak.

Manufacturing value added has fallen 7% since 2017.

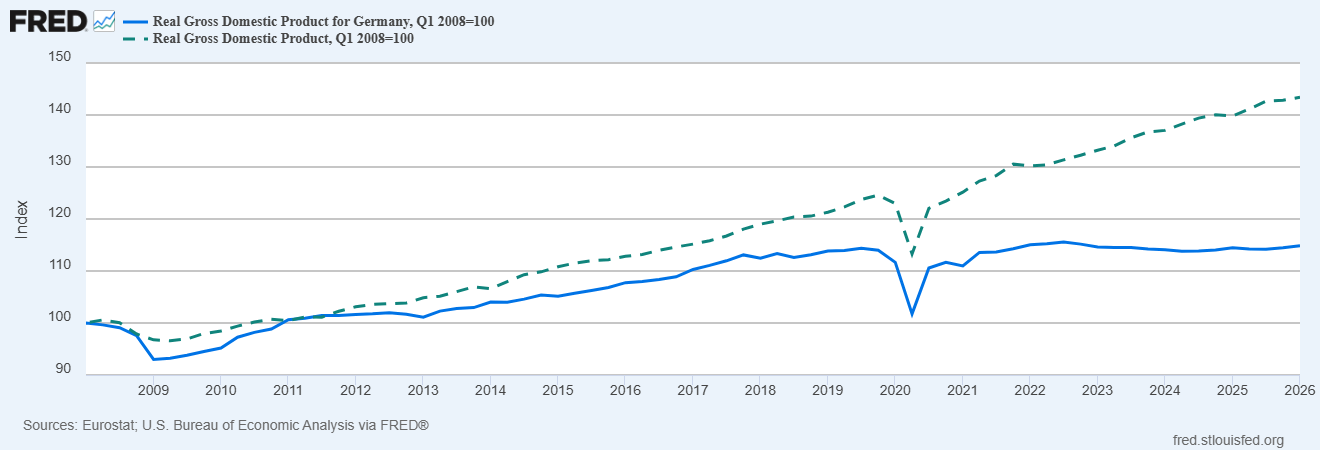

GDP was flat or declined in 9 of the last 12 quarters.

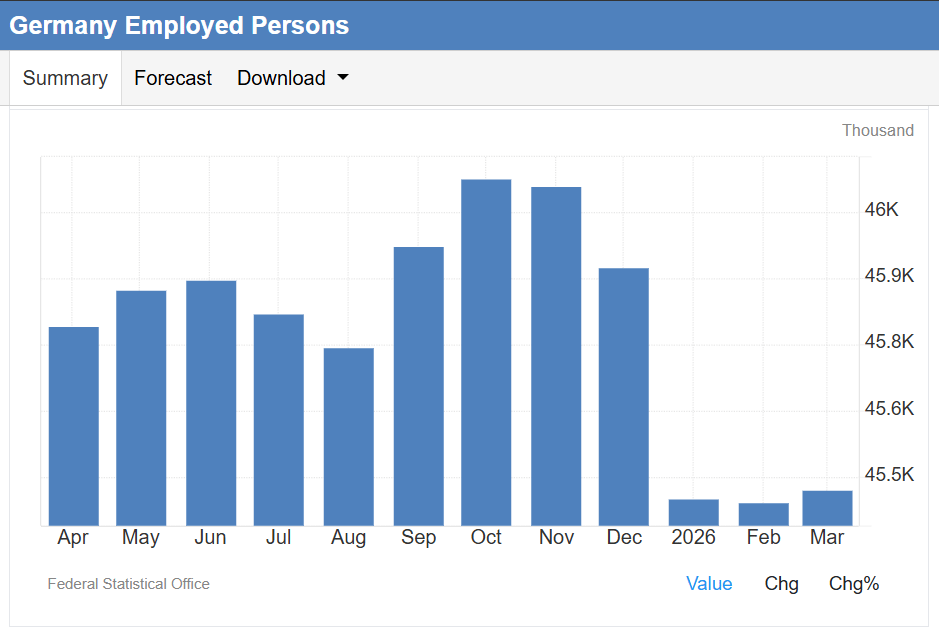

Hundreds of thousands of industrial jobs have been wiped out.

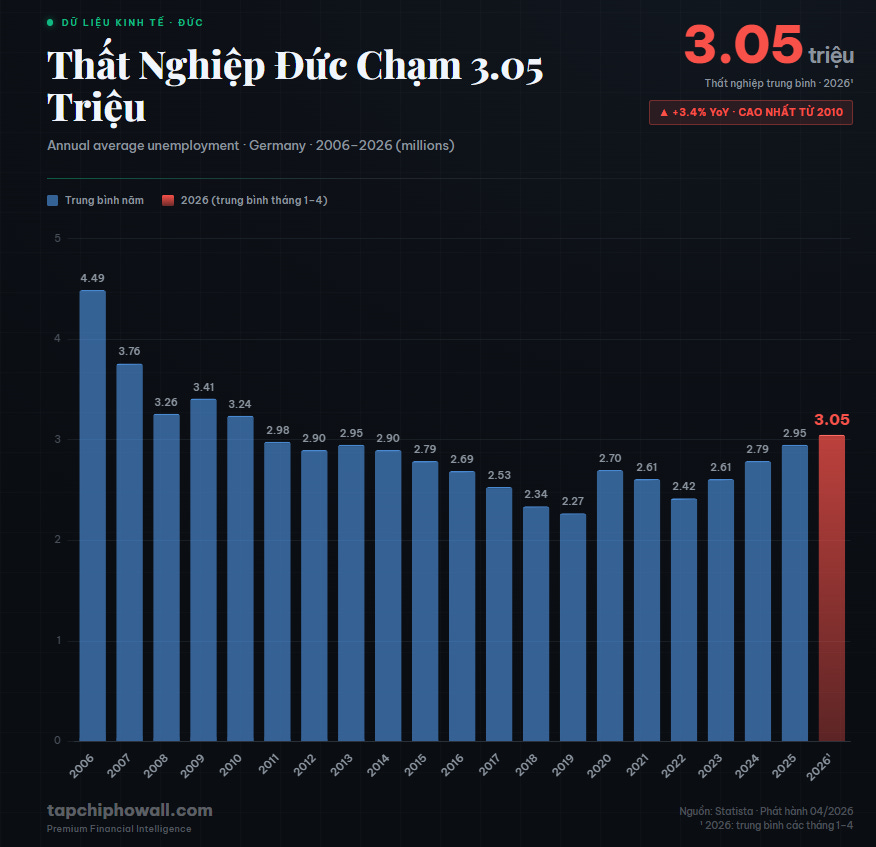

Unemployment has surpassed 3 million - the highest since 2011.

Peter Leibinger - President of the BDI, Germany's largest industrial federation - declared:

“The most severe crisis in the history of the Federal Republic.”

He emphasized: this is is not a cyclical recession. And he completely rejects the notion that this is only temporary.

At first glance, the story seems simple: Germany lost cheap Russian gas, lost the Chinese market, and was squeezed by US tariffs. Three external shocks hitting at once.

But looking closely, the story is much more complex - and more painful, because most of the wounds are self-inflicted.

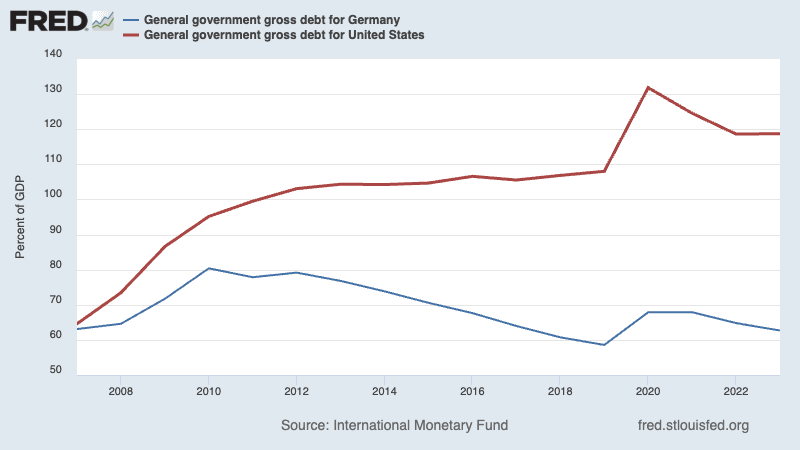

In 2007, Germany and the US started in the same position: public debt at around 63–64% of GDP. Since then, the two nations have taken completely opposite paths.

The US borrowed heavily, spent heavily - and boomed: real GDP grew by about 40% over 18 years.

Germany chose the path of absolute fiscal discipline - a policy known as “Schwarze Null,” literally “black zero” - meaning the budget must be balanced or in surplus at all costs.

In 2009, Germany went further: enshrining a debt brake in its constitution, banning structural deficits exceeding 0.35% of GDP.

No other developed country in the world has tied its own hands so tightly.

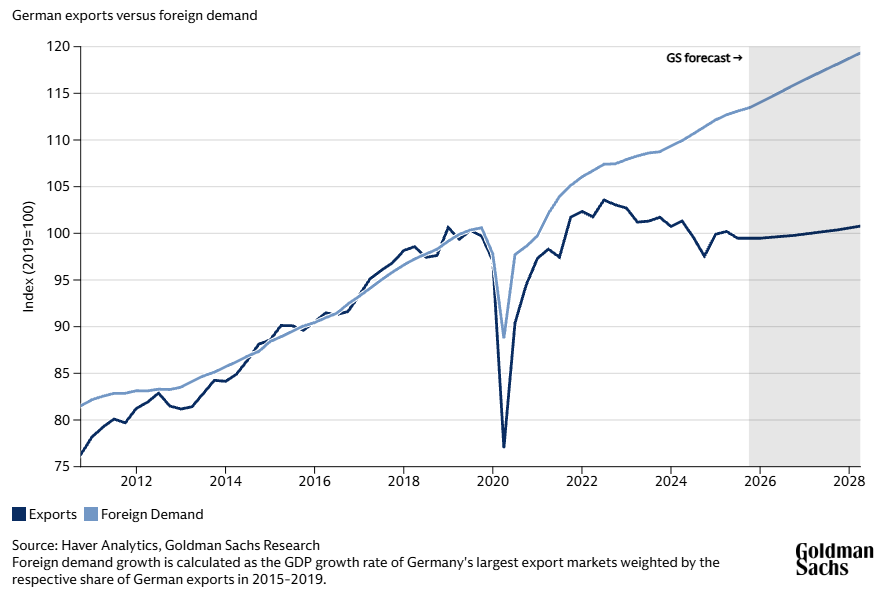

The result? The lowest debt in the G7. A massive trade surplus. And GDP has been virtually flat since before the pandemic.

Paul Krugman - the Nobel laureate economist - analyzed:

Germany, once a model for other countries to emulate, has now become a cautionary tale - a warning about the cost of rigid thinking.

He calls this the “price of Schwarze Null”: 15 years of worshipping fiscal discipline, cutting public investment, letting infrastructure decay, and allowing productivity to stagnate.

Then, when three external shocks hit, the foundation was too rotten to withstand them.

The three external shocks were merely catalysts. The foundation had been rotting for a long time - starved by the very fiscal discipline Germany was most proud of.

France is trapped in an allocation problem - a single spending item (pensions at 14% of GDP) locks up the entire system.

The UK is trapped in a growth problem - a multi-decade cycle of underinvestment.

Read our articles on the French and UK economies at:

Germany is trapped in the hardest problem of all: admitting that the very things it took pride in - savings, discipline, surpluses - have become its shackles.

In March 2025, Germany amended its constitution to borrow 500 billion euros outside the debt limit - breaking its own rule. This is an official admission: Schwarze Null was wrong.

The remaining question: will this reversal come in time?

Six months ago, the answer seemed favorable: three macro shocks - terms of trade, fiscal, and monetary - were reversing simultaneously. Germany was finally willing to spend. Optimists had a point.

Then the Strait of Hormuz went up in flames. The energy shock returned

The investment question is therefore no longer simply “will Germany recover.” The more accurate question is: are the other two reversing shocks strong enough to offset the one that turned back?

In today's article, Viet Hustler will unpack the German equation - from its self-inflicted roots, through three amplified external shocks, to the €500 billion gamble.

Schwarze Null - When Fiscal Discipline Becomes Shackles

Three Broken Pillars - Gas, China, Cars

Deindustrialization - Real or Illusion?

The Immigration Equation

The €500 Billion Debt Package - When Germany Finally Agrees to Spend

The Investment Landscape in Germany