If You Missed the Best Recent Articles:

When French government bond yields surpass those of Greece - a country that defaulted and received a €289 billion bailout from Europe - this is no longer a routine warning signal - this is the market passing judgment on France.

For most of the past decade, Greece has been seen as the 'weak link' in the eurozone:

High debt

Low growth

Reliance on external support.

France, by contrast - the EU's second-largest economy, a founding member of the European Union, and a pillar of the region's financial system.

→ The inversion of these two yield curves is no technical blip. It is a shift in confidence.

Note that: the bond market does not price what is happening today - it prices what will happen in the future.

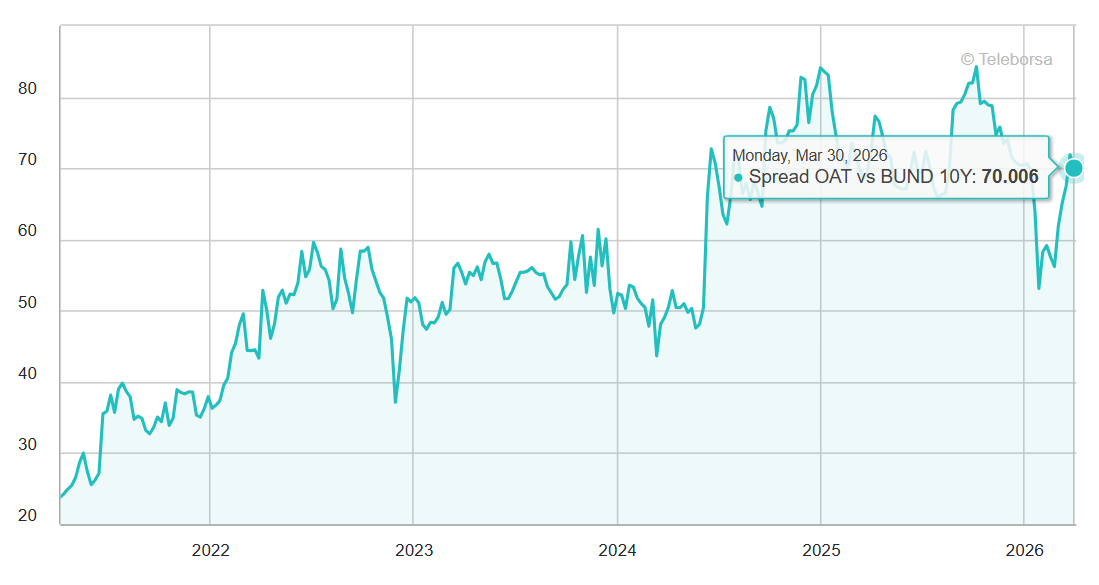

Looking at the OAT–Bund spread over recent years - from around 30 bps in 2021 to nearly 80 bps now - one thing becomes clear: every political crisis in France leaves a 'scar' on the yield curve.

Those 5–15 bps increases never fully revert.

This is no longer a short-term shock story. This is structural repricing.

France is not just facing a fiscal problem, France is facing an equation - and that equation no longer has a solution. Not because of a lack of policy tools. But because every viable option is blocked by the system's own constraints.

In today's article, Viet Hustler will dissect this equation layer by layer with readers - from the undeniable numbers, to the demographic roots, to the ultimate limits.

Macro Picture - The Indefensible Numbers

Population - The Time Bomb from the 1960s

Fiscal Equation Without a Solution

Labor Market Paradox

Public Debt Spiral

Any Exit for France?

Impact on Financial Markets