“When monetary policy substitutes for fiscal discipline, inflation is no longer a mystery - it is a choice.”

“When monetary policy substitutes for fiscal discipline, inflation is no longer a mystery - it is a choice.”

- Kevin Warsh

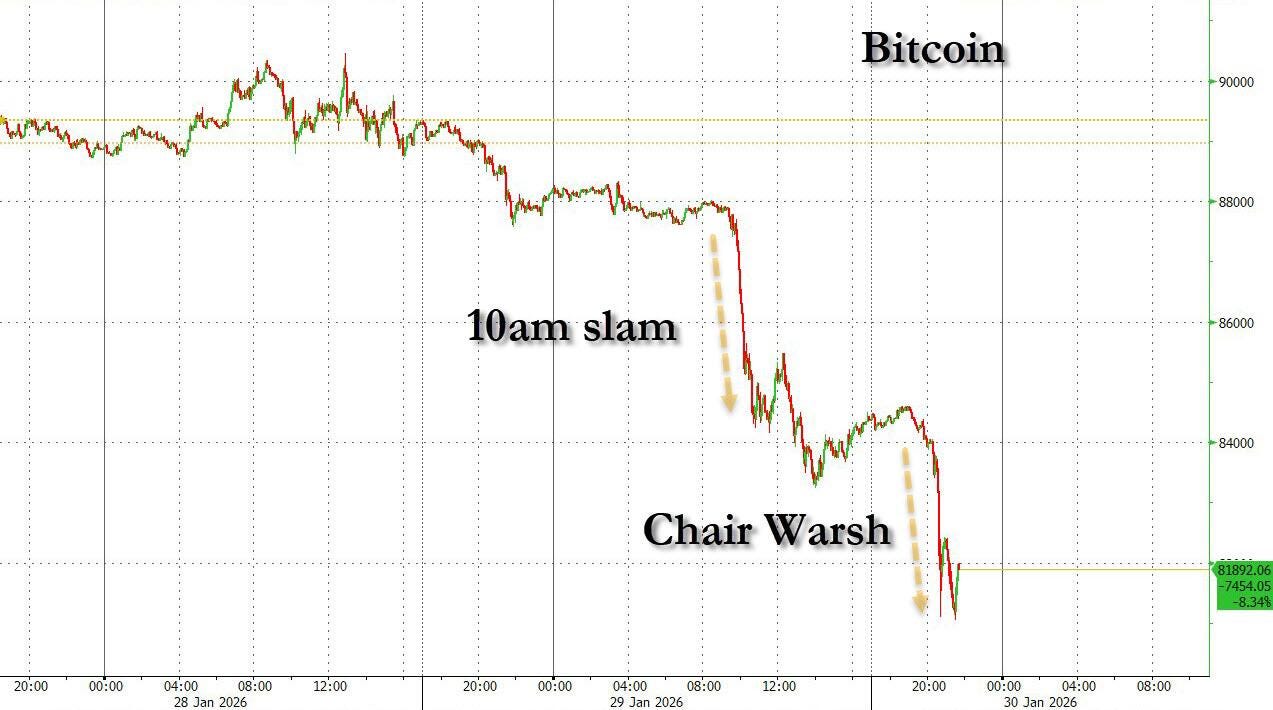

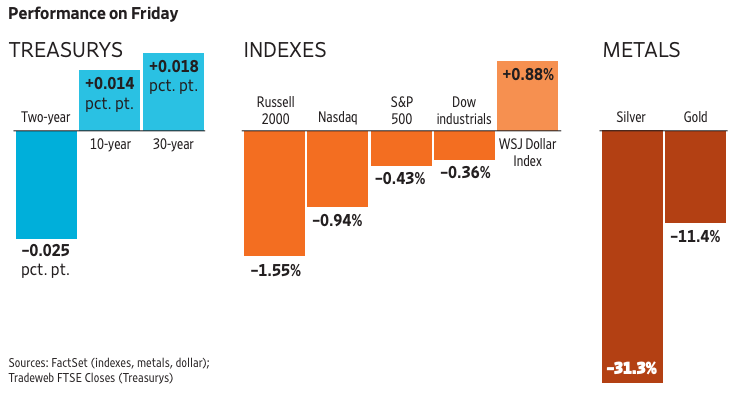

Last Week's Trading Session Captures Market Jitters Over Kevin Warsh.

Government bonds bought at the front end of the curve, long-term yields cool. USD strengthens. Equities slide, with Russell 2000 hit hardest, while Nasdaq and S&P 500 face milder pressure. Precious metals plunge, silver down over 30% in one swoop.

At first glance, it looks like technical reaction. But it signals something deeper: markets repricing the Fed's role in the US economic order.

For over a decade, investors grew accustomed to a clear playbook: whenever volatility spiked, the Fed expanded its balance sheet; whenever growth faltered, the Fed became the ultimate backstop for assets and fiscal policy.

Kevin Warsh doesn't deny the Fed's stabilizing role in crises. But he questions a baked-in assumption: should the Fed maintain that role as a permanent state?

Current market logic still seems sound: if Trump wants low rates, fast growth, Main Street support-why pick someone who shuns QE, rejects Fed put promises, and openly blasts balance-sheet bloat?

That logic holds only in a static model-where low rates, QE, and growth always align, and the cost of 'protection' is assumed infinite.

But the US economy under Trump 2.0 no longer runs on that model.

In a system where:

fiscal policy has crossed the pretend-it's-sustainable threshold,

the Fed's balance sheet has turned political,

and currency is viewed as national power,

...the question isn't 'cut rates or not,' but who bears the discipline after rates are cut.

Thus, the central question isn't:

“Is Kevin Warsh dovish enough to please markets?”

But:

“Who can run a Fed when monetary, fiscal, and national security converge?”

At that level, monetary policy ceases to be a pure technical tool. It becomes power design: who gets protected, who adjusts, and where the ultimate costs land.

In that framework, picking Kevin Warsh isn't a personal gamble. It's a signal Trump seeks not a compliant Fed, but one willing to embrace conflict to restore order.

This Week, Viethustler Breaks It Down in 5 Parts:

Part I – Trump 2.0 and Why the Fed Became the 'Strategic Bottleneck'

Part II – Kevin Warsh Isn't a Personal Pick, But the Product of an Economic Coalition

Part III – How Warsh Differs from Powell: Not Hawk vs. Dove, But Power Philosophy

Part IV – AI, Productivity, and the Piece the Current Fed Is Missing

Part V – Fed Over the Next 4 Years: Interest Rates, Balance Sheet, USD and How Markets Must Relearn Pricing

The ultimate conclusion isn't whether Kevin Warsh will be a 'hawk' or a 'dove.' Nor is it whether Trump will respect the Fed's independence.

It's a colder reality of systemic economics:

In an order where currency determines resilience, power lies not in how well you soothe markets, but in who dares to withdraw the safety net when it has become the problem itself.

Note: This article is built primarily on economic analysis frameworks and systemic mechanics, deliberately minimizing speculation on political motives or backroom deals to focus on economic logic and policy structure.

Viet Hustler is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

PART 1 – U.S. ECONOMIC CONTEXT UNDER TRUMP: WHY THE FED HAS BECOME THE 'STRATEGIC BOTTLENECK'

Trump returns to the White House in a context utterly different from 2017.

Trump 2.0 does not face:

low inflation

expanding globalization

or ample fiscal space

Instead, Trump 2.0 confronts three structural constraints that make the Fed the epicenter of policy conflict.

1.1 – U.S. Fiscal Policy Enters the 'No Pretend' Zone

The core issue in the current U.S. economy isn't growth or the cycle-it's that fiscal policy has crossed the threshold where it can no longer be neutralized by monetary policy. When public spending and debt structure no longer respond to cycles, the Fed stops being a stabilizer and becomes a bottleneck that must be addressed.

Structural budget deficits, no longer elastic to recessions or recoveries

Public debt growing faster than nominal GDP, eroding the 'growth offsets debt' effect

Interest costs shifting from financial variable to rigid budget item

These three forces do one thing: lock in the inability to delay fiscal adjustments. In this structure, the Fed can't continue behaving like the post-2008 era, where bond buying and rate cuts could buy time without immediate political-market backlash.

With interest costs embedded in the budget, every Fed action becomes allocative:

unconditional bond buying legitimizes spending

rate cuts to 'cover' fiscal policy shift costs to cash holders

default last-resort buyer role erases market discipline

In this structure, a Jerome Powell-style Fed is no longer seen as neutral, but as a mechanism delaying systemic response. Too politically safe, too soft on fiscal, and too accustomed to extend & pretend -where problems aren't solved but shoved onto the central bank's balance sheet.

For Donald Trump, this is no longer a difference of views, but structural conflict. With fiscal in the 'no pretend' zone, a Fed that keeps absorbing imbalances won't stabilize the system-it will prolong them until adjustment costs spiral out of control.

In this structure, Trump doesn't need a 'cautious' Fed. He needs a Fed that doesn't legitimize bad spending, even if it forces markets to reset expectations.

→ In sum, fiscal can't self-discipline if there's always a balance sheet to shield it.

1.2 – Trump 2.0 Prioritizes Supply-Side Growth, Not Demand

The central White House-Fed conflict this term isn't about rate levels, but the growth operating framework. When growth is defined as a supply-side productivity puzzle, demand-based models become impediments.

Deregulation as the pillar to cut marginal costs and expand production capacity

AI and tech as long-term productivity engines, not short-term price pressures

Uneven growth accepted, as long as aggregate productivity rises

These forces redefine policy goals: expand supply first, regulate demand later. In this structure, growth isn't overheating-it's the precondition to absorb fiscal adjustment costs and reallocate labor-capital.

The problem: The current Federal Reserve still operates on demand logic:

CPI and PCE as core variables

Phillips Curve as warning framework

strong growth read as latent inflation risk

This mindset triggers mechanical policy reflexes: when growth accelerates, monetary policy tightens 'preemptively.' But in an economy driven by cost cuts and productivity gains, that reflex misdirects resources.

The result: direct conflict:

White House pursues industrial and supply-side policies

Fed manages via demand and price indexes

the same growth phenomenon, interpreted through opposing logics

In this structure, the Fed doesn't just lag-it opposes. Treating growth as risk makes monetary policy inadvertently punish forces reducing long-term inflation, while shielding inefficient cost structures.

For Donald Trump, this isn't academic debate-it's operational constraint. A supply-side growth strategy can't coexist with a central bank that views growth as sin.

When growth stems from productivity, the demand framework stops being a stabilizer-and becomes the bottleneck.

1.3 – Trump Wants Low Rates, But Not QE

The market's biggest mistake in reading Trump has been conflating low interest rates with comprehensive monetary easing. In the Trump 2.0 framework, these concepts not only diverge but produce opposing allocation effects.

Low interest rates are seen as a tool to support Main Street by cutting funding costs for labor and small businesses

QE is viewed as a mechanism to inflate financial asset prices, enriching asset holders

QE indirectly finances deficits, blurring the line between monetary and fiscal policy

These three forces delineate a clear boundary: Trump wants to lower funding costs but not expand the balance sheet to skew benefits toward assets.

In the Donald Trump administration's view, QE is no neutral technical tool:

QE politicizes monetary policy through asset selection

QE casts the Federal Reserve as a distributor of benefits, not a regulator

QE weakens the USD in an uncontrolled manner by decoupling rates from balance-sheet discipline

The crux is this: Trump doesn't oppose easing-he opposes easing via money printing and asset purchases. Low rates are a policy signal; QE is structural intervention. One adjusts the price of capital, the other alters ownership structures and expectations.

That's why Trump needs a narrow combination: low rates without QE. This isn't a common choice among central bankers, as it would force the Fed to:

abandon its default backstop role

accept markets absorbing volatility

use interest-rate tools within a balance-sheet discipline framework

Among the few at the Fed who have publicly endorsed this combination, Kevin Warsh stands out-not for promising low rates at any cost, but for sharply distinguishing between cutting funding costs and expanding balance-sheet power.

When rates are decoupled from QE, monetary policy no longer shields allocations-and that's what Trump is after.

1.4 – Geo-economics: The Fed Is No Longer a 'Non-Political' Institution

In Trump 2.0, the question isn't whether the Fed will be politicized, but that it's being thrust into a geo-economic space where 'non-political' status is no longer a viable operating state. When money becomes a national power tool, absolute neutrality ceases to be feasible.

USD is regarded as a geo-economic weapon, directly impacting trade balances, capital flows, and strategic positioning

Interest rates are seen as a tool for orchestrating cycles and national competitiveness, not just price stability

The Fed is embedded in national capacity structures, where money, fiscal policy, and industry are inseparable

These three forces don't demand Fed subservience to the White House, but they erase the presumption that the Fed can stand apart from national strategy. In a fragmenting world where money is tightly bound to geopolitics and supply chains, maintaining an 'ivory tower' image becomes institutional illusion.

This doesn't mean Trump wants:

direct control of the Fed

monetary policy as an electoral tool

or rate decisions dictated by political rhythms

On the contrary, Trump needs a more sophisticated structure:

a Fed independent enough not to bail out fiscal policy or endorse distortions

but aligned enough not to undermine the overall geo-economic strategy

In this setup, the issue isn't independence versus dependence, but alignment versus misalignment.

Jerome Powell: procedurally independent, but strategically misaligned

Pure dove: short-term aligned with growth, but unreliable on discipline

Kevin Warsh: between the extremes, preserving independence without neutralizing strategy

Example: Since 2018, the USD has become a central coercive tool in US-China competition-from sanctions and capital controls to supply-chain restructuring. Yet under Powell, the Fed has acted as if the USD were merely a neutral market variable, indirectly managed via CPI/PCE and 'non-targeted.'

The result: the 2022–2023 USD strength cycle became an unmanaged side effect: inflicting global stress and repatriating capital to the US, but not integrated as a disciplined geo-economic lever.

In a geo-economic world, the Fed can't be both absolutely neutral and effective. When money becomes national power, misalignment is the biggest risk.

Overall Assessment

Fed personnel decisions in Trump 2.0 are no longer matters of preference but compelled outcomes of locked-in systemic constraints. As foundational conditions shift, the space of viable options narrows automatically.

The QE space is exhausted, both economically and politically.

Fiscal Policy Needs Discipline to Avoid Shifting Costs to Currency

Growth Must Come from Supply Side to Absorb Structural Adjustments

AI Viewed as Productivity Deflation Force, Not Price Pressure Source

USD Needs Institutional Credibility Protection, Beyond Just FX Volatility

These Five Forces Simultaneously Rule Out Familiar Options. A “Compliant” Fed – Ready to Shield Markets and Fiscal Policy – Would Exacerbate Distortions. A “Pure Dove” Fed – Prioritizing Easing at All Costs – Would Shatter Balance Sheet Discipline and Currency Credibility. Conversely, a “Dogmatic Hawk” Fed Would Choke Off the Very Supply-Side Growth Strategy Pursued by the White House.

In This Framework, Donald Trump Doesn't Need a Market-Friendly Fed Chair. Trump Needs a Fed Willing to Embrace Conflict, Ready to:

Refuse to Legitimize Fiscal Profligacy

Reject Balance Sheet as Substitute for Reforms

And Force Markets to Reprice Risks

Kevin Warsh Fits Precisely at This Nexus: Preserving Institutional Independence Without Neutralizing Strategy; Accepting Rates as Tool But Rejecting QE as Escape Hatch; Protecting USD Through Discipline, Not Money Printing.

With Constraints Locked In, Choice No Longer Personal. In Trump 2.0 Framework, Warsh Isn't Optimal Option – He's the Only One Left.

PART 2 – WARSH ISN'T TRUMP'S PERSONAL CHOICE, BUT THAT OF AN “ECONOMIC ALLIANCE”

Placing Kevin Warsh at the Center of Monetary Power Doesn't Reflect Personal Favoritism, But the Needs of an Economic Power Axis Seeking Discipline Over Reassurance. In This Framework, Warsh's Background Isn't a Personal Plus, But a Prerequisite for Acceptance by Multiple Power Centers Simultaneously.

Warsh Understands Fed's Internal Crisis Mechanics, Not from Theory

Warsh Has Market Credibility from Wall Street Experience and Crisis Management

Warsh Isn't Locked into Academic Models or Post-2008 Consensus

These Three Forces Position Warsh as a Figure “Inside the System” Enough to Know Its Flaws, and “Outside” Enough Not to Defend It.

2.1 – Warsh: Product of 2008 Crisis, Not QE

Warsh Joined Fed in 2006, Became Youngest Governor in History at Age 35 Under George W. Bush. He Served on Board of Governors Throughout 2006–2011, Coinciding with Fed's Unprecedented Power Expansion to Save Financial System.

Warsh Was Ben Bernanke's Right-Hand Man in 2008 Crisis

Directly Involved in Bank and Credit Market Bailouts

Played “Wall Street Bridge” Role Thanks to Morgan Stanley Background and Market Networks

But Key Point Isn't Whether Warsh Supported or Opposed Bailouts – It's That: He Witnessed from Inside How Fed Strayed from Traditional Role. This Experience Shaped His Consistent Stance: Saving System in Crisis Essential, But Turning Emergency Measures into Permanent State Is Structural Error.

Warsh Warned of Inflation Risks as Early as 2008, Despite Low Inflation Then

Opposed Prolonged QE and Near-Zero Rates as Default State

Not Because He Was “Right” Every Time, But Because He Rejected Extending Emergency Fixes

In Current Alliance Framework, This Is Critically Important: Warsh Doesn't Deny Fed's Crisis Role, But Refuses to Let Crisis Become Permanent Rationale for Balance Sheet.

2.2 – From Fed to Hoover: Warsh Breaks from Post-2008 Consensus

After Leaving Fed in 2011, Warsh Didn't Return to Central Banking or Official Policy. He Shifted to:

Research at Hoover Institution

Group of Thirty Participation

And Continuous Public Fed Criticism

These Three Forces Show Clear Shift: Warsh Positioned Himself Outside Post-2008 Consensus, Where QE, Ballooning Balance Sheets, and Academic Models Became Unquestioned Norms.

Criticized Fed Models as Outdated and Opaque

Blasted Balance Sheet as Default Policy Tool

Rejected “Rubber-Stamp” Role in Expert System

This Makes Warsh Rare Figure Who Understands Fed from Core Yet Isn't Bound by Its Interests. In Alliance Seeking to Reimpose Discipline, This Is Irreplaceable Trait.

2.3 – Scott Bessent: Architect Behind the Choice

Scott Bessent's Role Is Decisive Not for Pushing Specific Name, But for Reshaping Economic Alliance Axis: Fiscal No Longer Implicitly Backstopped by Monetary, and Market Stability No Longer Trumps Systemic Discipline.

Fiscal Discipline Prioritized Over Short-Term Asset Stability

Fed and Treasury Must Separate Functions, No Longer “Fused” Via QE

QE Not Viewed as Default Tool Every Time System Under Pressure

These Three Forces Form Iron Principle: Markets Must React Before Central Bank Intervenes. Under This Principle, QE No Longer Neutral Technique, But Replaces Price Mechanism with Administrative Decisions.

Here, Kevin Warsh Becomes Bessent's Natural Ally:

QE Distorts Price Signals and Destroys Capital Allocation Discipline

Fed “Rescuing” Every Downturn Cycle Eliminates Self-Correction Mechanism

Bond vigilantes need to be restored as a natural fiscal discipline mechanism

The intersection isn't about political views, but about understanding monetary power:

Trump may want low rates to cut funding costs

Bessent wants rates with discipline, not detached from the balance sheet

Warsh accepts using rates as a tool, but rejects QE as an escape hatch

In this structure, Warsh doesn't represent a faction, but an operating principle: cutting funding costs doesn't mean expanding the balance sheet's power. When two seemingly conflicting goals must coexist, the choice set narrows itself - and Warsh becomes the sole intersection.

What unfolds isn't just personnel selection, but an effort to redefine the Federal Reserve's role from within. Post-2008 and Covid, the Fed has faced criticism for mission creep:

Balance sheet expansion from emergency tool to permanent state

Monetary policy pulled into default fiscal support role, even if unnamed

Fed no longer just regulates cycles, but inadvertently flattens risks for both markets and government

In that structure, asset purchases and prolonged low rates are no longer technical choices, but economic power allocations: who gets protected, who gets shielded, and where adjustment costs are shifted.

This explains why Bessent sees Warsh not as a differently styled Fed chair, but as the central factor in a regime change. Changing the leader is just step one; the next adjustments target:

How the Fed operates and limits intervention scope

How the Fed models the economy and reads growth signals

How the balance sheet is used: infrastructure or allocation tool

In this logic, Warsh isn't picked for being “anti-QE”, but for questioning QE's legitimacy when it becomes the default state. When politicians spend freely knowing funding costs will be monetized, the boundary between monetary and fiscal blurs in substance, even if maintained on paper.

This isn't academic debate, but a power issue: who bears ultimate responsibility for resource allocation and economic adjustment costs.

In that context, internal Fed reform is the least conflictual option versus externally imposed reform - via Congress, legislation or direct political blows. If the Fed doesn't self-limit its role, the political system will force it to.

Warsh thus isn't an “anti-Fed” figure. He's the choice for the Fed to self-limit before limits are imposed from outside.

2.4 - Stan Druckenmiller: influence from thinking, not power

In this economic alliance structure, influence comes not from titles or institutional power, but from battle-tested thinking frameworks through cycles. Stan Druckenmiller embodies that influence precisely.

QE distorts price signals, leaving markets unable to discriminate risk

Prolonged cheap money destroys capital allocation, propping up inefficient structures

Inflation is a consequence of political choices – fiscal, not growth or productivity

These three pillars don't oppose easing in crises, but reject turning easing into a permanent state. When monetary policy flattens every cycle, markets learn no signals from prices.

In that thinking framework, Kevin Warsh isn't “anti-Fed”, but rejects the Fed replacing market mechanisms. Druckenmiller calling Warsh a “trusted advisor” isn't political endorsement, but recognition of thinking alignment.

The key point: Druckenmiller's influence doesn't issue orders, but narrows the rational choice set. When a framework shows prolonged cheap money inevitably leads to misallocation and political inflation, default-QE options self-eliminate.

In that structure, Warsh isn't “pushed up” by connections, but fits squarely in the remaining choices after permanent cheap-money options are excluded.

When thinking locks the frame, power just executes.

PHẦN 3 – WHERE WARSH DIFFERS FROM POWELL? NOT HAWK VS DOVE

3.1 – Inflation philosophy difference: not hawk vs dove

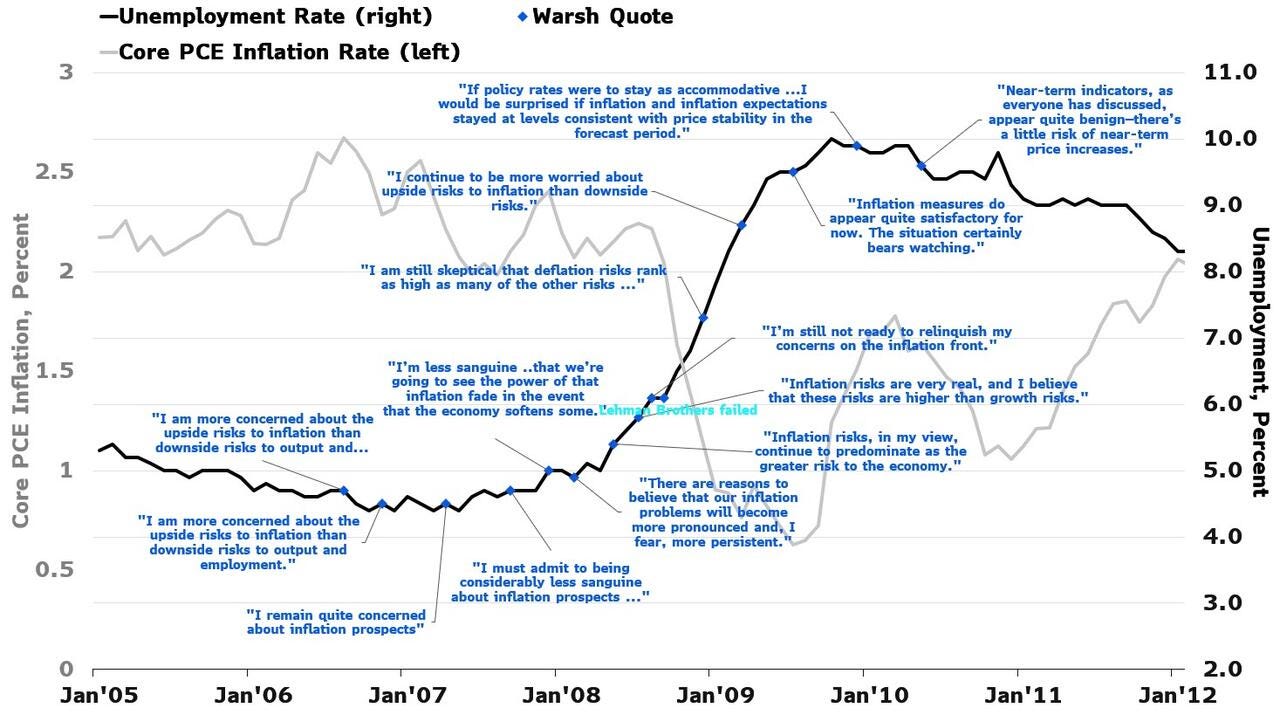

The difference between Jerome Powell and Kevin Warsh isn't about tightening or easing degrees, but how they define what inflation is and where it comes from. When a phenomenon is defined differently, every policy tool - no matter how sophisticated - pulls in irreconcilable directions.

In the current Fed thinking under Powell, inflation is read as demand outstripping supply in the cycle. When labor markets tighten, wages rise fast or consumption stays resilient, the default reflex is: financial conditions are too loose and need tightening to “get ahead of the curve”. The Phillips Curve, softened from the past, still serves as the implicit operating map: strong growth today is tomorrow's price risk.

PCE chart clearly shows the consequence of that thinking frame: under Powell, inflation overshot the target for extended periods, reflecting a policy reflex viewing inflation as demand-labor phenomenon with slow tightening response, while structural forces built up behind.

Kevin Warsh starts from an entirely different definition. For him, inflation isn't a spontaneous market phenomenon, nor a “natural punishment” when the economy grows too strong or workers earn high wages. Inflation, in Warsh's frame, is the accumulated result of policy choices - especially when prolonged fiscal expansion is shielded by monetary policy, budget discipline deferred, and the central bank's balance sheet substitutes for price mechanisms.

That's why Warsh openly rejects the core doctrine of Phillips-curve Keynesianism: the belief that “overheating” growth and tight labor markets are pathological states needing cooling. When he says the Fed must “abandon the belief that inflation arises because the economy grows too much and workers are paid too much”, it's not shocking rhetoric, but a direct strike at a thinking foundation dominating monetary policy for nearly a century.

This is particularly important when looking back at the history of economic thought. Keynes wrote The General Theory for a very specific context: the demand collapse and mass unemployment of the 1930s, when markets clearly could not self-correct.

He did not write it as a “macroeconomic operating system” for every circumstance-from the 1970s stagflation and supply shocks to Covid and 2026 geoeconomic competition. Even Keynes himself was skeptical of the word “general,” yet later generations turned a situational framework into timeless dogma.

It is this stretching that led to Warsh's deepest critique: the Fed has gradually become an unelected economic government, where monetary policy not only regulates cycles but also shields fiscal policy, props up assets, and indirectly intervenes in capital allocation. QE and the ballooning balance sheet are no longer emergency tools but a permanent state- a form of monetary politicization through asset allocation, where benefits tilt toward asset holders and adjustment costs are shifted to cash holders.

By contrast, in Powell's framework, QE is viewed as a system-stabilizing tool: when markets falter or recession risks rise, expanding the balance sheet is a technical measure to keep monetary transmission from clogging; inflation, if it emerges, will be addressed later via interest rates.

For Warsh, QE is never neutral. When the Fed buys assets on a massive scale and keeps rates low for extended periods, it does not just affect financial conditions-it redistributes income, risk, and economic power from market discipline to the central balance sheet.

From these two definitions, interpretations of growth diverge entirely.

In Powell's framework, strong growth and a tight labor market are signals for caution.

In Warsh's framework, growth-if driven by productivity-is the prerequisite for absorbing fiscal adjustment and capital reallocation. Without productivity growth, any attempt to tighten fiscal policy merely shifts costs to monetary policy or erodes real incomes.

Thus, Warsh does not believe:

growth inherently causes inflation,

rising wages are the enemy of price stability,

or technology is a source of inflation risk.

On the contrary, he views technology-especially AI-as a structural disinflationary force. AI lowers marginal costs, boosts capital and labor efficiency, and expands the noninflationary growth boundary. In this structure, tightening monetary policy to “get ahead” of an assumed inflation risk is not only misguided but suppresses the very force driving down long-term inflation.

The irreconcilable point lies here:

Powell combats inflation by suppressing demand.

Warsh argues inflation must be addressed by restoring discipline where it originates-fiscal policy, balance sheets, and allocation mechanisms.

When inflation is seen as a policy phenomenon rather than a cyclical one, the proper reflex is no longer more monetary medicine but shrinking monetary policy's role to force other constraints into view. Misdiagnosing inflation's source makes any policy dosage-hawkish or dovish-beside the point.

And that is why the difference between Powell and Warsh is not one of style but a fundamental divergence in viewing monetary power within the modern economic structure.

3.2 – Focus: the Fed's Balance Sheet

The core difference between Kevin Warsh and the current Fed is not about the direction of interest rates but a bigger question: What role should the Fed play in the economy's resource allocation? When the balance sheet becomes the default policy tool, monetary policy is no longer neutral-and that is the institutional distortion Warsh sees.

Over the past decade-plus, the Fed has shifted from regulator of financial conditions to central capital allocator:

Paying IORB on massive excess reserves, fixing capital costs and blurring market signals

Using QE to buy bonds on a massive scale, thereby lowering government funding costs

Maintaining a buyer-of-last-resort role as a permanent state, not just in crises

→ These three mechanisms combine to create a structural outcome: the Fed's balance sheet supplants price mechanisms, with short-term stability bought at the expense of long-term distortions.

Warsh's view-and the key reason he was chosen-is not to deny the Fed's crisis role. On the contrary, he was at the core of power in 2008 and knows when intervention is essential. But that experience makes him oppose turning emergency mechanisms into permanent fixtures.

Warsh's argument is clear on political-economy grounds: when governments can spend more easily knowing monetary policy will absorb funding costs, the boundary between monetary and fiscal policy ceases to exist in practice. QE then becomes not a stabilization tool but a covert deficit subsidy.

The key point: Warsh does not see the problem in balance-sheet size but in its allocation structure and the incentives it creates. A large balance sheet does not necessarily cause instability-but misallocated one surely will.

He examines how the system actually operates:

Reserves distributed extremely unevenly across institutions

Some banks face local reserve shortages → liquidity stress

Most of the system has idle excess reserves that fail to translate into credit or stability

In this structure, expanding or contracting the overall balance-sheet size does not address the root. What matters is who holds reserves, with what incentives, and in what operating framework. Thus, Warsh avoids dogmatic QT or a return to QE-instead seeking to rebuild market incentives.

His toolkit reflects this philosophy:

Tiered IORB to distinguish necessary from excess reserves

Regulatory tweaks to free trapped liquidity in the system

Forcing markets and banks to resume the backstop role the Fed has held too long

In this approach, the Fed steps back from picking winners and losers via asset purchases and timing. The balance sheet returns to infrastructure, not allocation. Stability comes not from “buying to save” but from resetting operational discipline.

This is precisely why efforts to shrink the balance-sheet role always provoke fierce market backlash. But for Warsh, that reaction is not a reason to stop-it is evidence the system has depended too long on monetary backstops.

When the balance sheet becomes the condition for smooth fiscal operations, it has exceeded monetary bounds. And when the Fed has done the market's job too long, the market must relearn-however bumpy the process.

Balance sheet size doesn't create stability. The allocation structure and discipline it imposes do.

(Hoping for a detailed article on this in the future)

PART 4 – AI: THE MARKET-OVERLOOKED PIECE

The biggest divergence between Kevin Warsh's framework and the current Fed's lies not in interest rates or the balance sheet, but in their reading of technology's role in inflation dynamics. When AI is viewed as a supply-side productivity shock, many current policy reflexes become outdated.

AI reduces marginal costs in production, logistics and management

AI generates good deflation through productivity gains, not demand weakness

The current Fed still treats AI as a neutral variable, not a structural force

These three forces redefine the relationship between growth and price stability. In Warsh's structure, inflation isn't managed by suppressing demand, but by expanding the productivity frontier to absorb it. When technology lowers system costs, tightening monetary policy to “get ahead” of inflation risks means penalizing the very force driving down inflation.

The key intersection of this framework is Palantir. Not because Palantir represents “glamorous” AI, but because it's deployed directly into the core operations of the state:

AI is used to detect fraud, waste and overspending

Data is integrated across agencies, reducing lag and duplication

Public spending is brought back to efficiency logic, not just scale

In this structure, AI doesn't inflate asset prices, but strikes at the root of inflation in Warsh's view: undisciplined spending and misallocation. This isn't an AI bubble, because it doesn't require balance sheet expansion to generate effects. This is fiscal discipline AI, where productivity substitutes for easing.

When Scott Bessent puts fiscal discipline at the center, Warsh restructures monetary policy to not mask distortions, and AI is used to cut operating costs, these three forces lock in inflation from the root, not from demand.

Inflation can't be sustainably controlled by crushing demand if cost and spending structures don't change. When productivity rises, policy must step back-not double down.

PART 5 – FED OUTLOOK FOR THE NEXT 4 YEARS UNDER WARSH

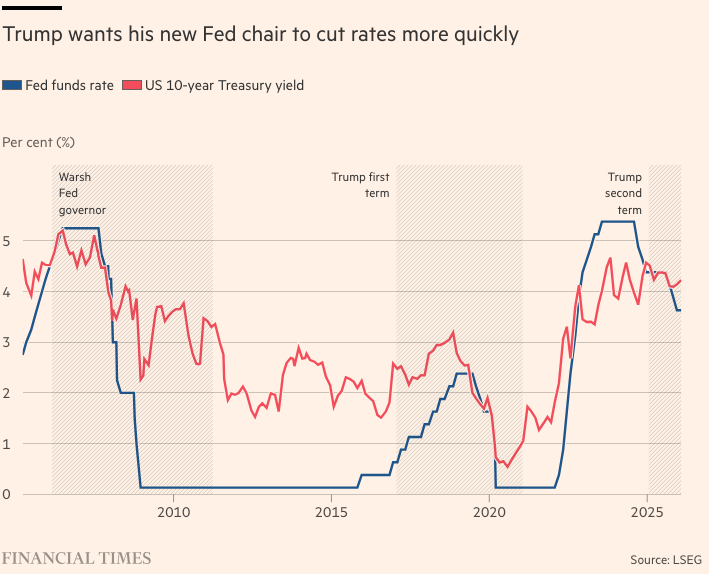

5.1 – Interest rates: lower, but not back to zero

The interest rate path under Kevin Warsh isn't dictated by stimulus desires or market-pleasing, but by disciplined tool use. When rates are decoupled from shielding fiscal policy and propping up asset prices, monetary policy escapes its narcotic role and returns to its core function: pricing capital costs according to real cycles.

This explains an apparent paradox that's structurally consistent: Trump may want faster rate cuts-but not a permanent return to cheap money.

Across all three episodes of political pressure on the Fed (pre-2008, Trump term one, and Trump 2.0), there's a common thread:

Policy rates can fall sharply when economic conditions allow

But aren't anchored at zero as the default state

And don't come with QE commitments to force down the entire yield curve

Under Warsh, this principle is elevated to an operating framework:

Rate cuts to reflect real capital costs, business cycles and adjustment needs

No return to zero, because zero rates destroy risk signals and encourage distortion buildup

Neutral rate lower than now, but left to form through markets-not forced by the balance sheet

These three forces establish a clear boundary: rates are the price of capital, not a backstop promise. Cuts may happen faster than markets are used to, but without the implicit promise that all tail risks will be absorbed by the Fed.

In this structure, the Federal Reserve stops “front-running” markets with preemptive easing, and isn't forced to hold unusual rate levels to shield fiscal and asset distortions. The neutral rate isn't “chosen,” but revealed through the real economy's operations.

The expectations implication is key:

Lower capital costs no longer mean leverage expansion

Growth isn't insured by prolonged ultra-low rates

And risk returns to its proper place-in pricing, rather than offloaded to the Fed's balance sheet

This is where markets often misread Trump and Warsh. Faster rate cuts don't mean a return to unconditional cheap money. On the contrary, it's an effort to separate rates from QE, allowing monetary policy flexibility without eroding systemic discipline.

Interest rates are a pricing tool, not a painkiller. When tools are abused, the system loses sensation-but problems don't disappear.

5.2 – Balance sheet: smaller in role, not necessarily in size

Under Kevin Warsh, the Federal Reserve's balance sheet isn't used to suppress volatility, but to restore functional boundaries. When its role shrinks, size becomes secondary.

Fed does less “buy to bail,” avoids intervening to flatten every shock

Backstop role gradually shifts to banks and markets

QT is technical, aimed at correcting allocation and incentives-not dogmatic about size

These three forces redefine the balance sheet as infrastructure, not an allocation mechanism. The Fed steps back from picking winners and losers via assets and timing; markets must reclaim risk pricing; the banking system re-assumes liquidity absorption under discipline.

The upshot is shifting expectations: no default “Fed put”; volatility is allowed within technical bounds; and stability comes from proper allocation, not backstop buying. QT thus isn't a signal of political tightening, but an operational maneuver to return functions to markets.

Balance sheet size doesn't create stability; its role determines how the system operates.

5.3 – USD: strong through discipline, not money printing

Kevin Warsh's approach to the USD isn't based on exchange rate targets, but on the institutional foundations that generate currency strength. In this structure, a strong USD isn't the result of intervention, but a consequence of discipline.

USD strength is anchored in fiscal discipline, not speculative capital flows

Strong USD Reflects Monetary Discipline, Not Bloated Balance Sheet

Currency Credibility Protected by Structure, Not Short-Term Manipulation

These Three Forces Eliminate Familiar Logic: Weakening USD to “Export Inflation” or Support Nominal Growth. For Warsh, a Strong Currency That Way Only Generates Higher Nominal Income but Lower Purchasing Power, Ultimately Eroding Confidence.

In This Framework, the Federal Reserve Has No Mandate to Manage Exchange Rates, But a Duty Not to Destroy the USD's Foundation. When Currency Is No Longer Used to Shield Fiscal Policy or Prop Up Assets, a Strong USD Becomes the Natural Consequence of Discipline, Not a Coerced Target.

Very Clear Allocative Consequences:

No Exporting Inflation to the Rest of the World

No Trading Household Purchasing Power for Short-Term Stability

Real Income Protected by Institutional Stability, Not Nominal Exchange Rates

A Currency Is Sustainably Strong Only When It Doesn't Bear the Burden of Policy Distortions Others Refuse to Address.

5.4 – Asset Pricing: Valuation Returns to Fundamentals, No Default QE

When the Balance Sheet Is No Longer an Allocation Tool and Interest Rates No Longer Provide a Backstop, Asset Pricing Mechanisms Automatically Shift Axes. Under Kevin Warsh, Markets Won't Lose Liquidity - But Will Lose the Privilege of Being Supported by Liquidity.

Less Liquidity-Driven Multiple Expansion as “Fed Put” Is No Longer Default

Valuation Returns to Cash Flow and Productivity, Not Easing Expectations

Gold and Crypto No Longer Benefit from QE as Baseline

These Three Forces Force Valuation to Reanchor to Cash Flow Generation and Productivity Gains. When Cost of Capital Is Priced Correctly and the Balance Sheet Doesn't Provide Cover, Multiples Can't Expand Just on Policy Expectations. Risk Premium Returns to Its Role.

Very Clear Tiered Consequences:

Assets with Sustainable Cash Flows and Productivity Growth Are Rewarded

Assets Reliant on Cheap Liquidity Are Discounted

Currency-Hedge Assets Lose “Tailwind” Without QE Baseline

In This Structure, Volatility Isn't a Signal of Instability, But a Screening Mechanism. Valuation Isn't Forced Down or Up; It Self-Adjusts to Fundamentals.

When Liquidity Withdraws from Its Backstop Role, Asset Prices Must Learn to Reflect Value Again.

CONCLUSION – TRUMP DIDN'T PICK WARSH TO BE “DOCILE,” BUT TO END AN ERA

A Seemingly Minor Detail That Says Volumes About the Power Structure Trump Wants to Rebuild.

When Asked If Kevin Warsh Would Commit to Cutting Rates, Donald Trump Responded Directly:

“I don’t want to ask him that question. I think it’s inappropriate… I want to keep it nice and pure. But he certainly wants to cut rates.”

This Isn't the Language of a President Seeking to Directly Dictate Monetary Policy. And Certainly Not of Someone Looking for a “Docile” Fed Chair to Execute Orders.

The Message Lies Elsewhere.

Trump Wants Lower Rates, That Hasn't Changed.

But Trump Refuses to Turn Rate Cuts Into a Personal Political Commitment or Hiring Condition. He Deliberately Maintains Distance - Not Out of Respect for Formal Independence, But Because He Understands Institutional Independence Has Value Only When Paired with Operational Discipline. This Is Where Kevin Warsh Fits Perfectly.

If Trump Only Wanted:

A Fed Ready to Cut Rates on Demand

QE Continuing as Default Backstop

Markets Appeased by Cheap Liquidity

→ Warsh Would Be a Poor Choice.

But Trump 2.0 Faces a Different Equation:

Fed Must Stop Legitimizing Fiscal Excess

Rates Can Fall, But Not Detached from Balance Sheet Discipline

Growth Must Come from Deregulation and Productivity, Not QE

AI Used to Cut Costs and Distortions, Not Inflate Asset Prices

In That Equation, Not Asking Warsh “Will You Cut Rates?” Isn't Evasion, But Intentional. Because If a Fed Chair Is Chosen for a Rate-Cut Commitment, That Moment the Fed Loses Credibility as an Independent Institution - Becoming an Extension of Fiscal Policy.

Trump Doesn't Need That.

Trump Needs a Fed Independent Enough Not to Bail Out Distortions, But Aligned Enough Not to Undermine Supply-Side Growth Strategy. Warsh Isn't Chosen Because He “Promises” Rate Cuts.

He's Chosen Because He Can Cut Rates Without Turning It Into a Backstop. The Fed Over the Next 4 Years Thus Won't Be Hawk or Dove.

The Fed Becomes the Architect of a New Regime, Where: Inflation Seen as Consequence of Political, Fiscal Choices

Growth No Longer a Sin When Driven by Productivity

And Markets Forced to Relearn Risk Pricing Without the Soft Landing Escape

If Trump Really Wanted to Control the Fed, He Would Have Asked Warsh That Question.

His Deliberate Omission Signals the Opposite: Trump Isn't Seeking a 'Docile' Fed.

Trump không tìm một Fed “ngoan”. Trump tìm một Fed đủ cứng để chấm dứt một kỷ nguyên.

showing Warsh has called for the Fed to cut its holdings of US Treasuries")