If You Missed Our Best Recent Reads:

2026 doesn't kick off asking whether the global economy will recess - but the tougher question: how will the economy grow. After three years navigating the fuzzy borderland of sticky inflation, high rates and geopolitical volatility, the world enters 2026 with a familiar yet risky pattern: major economies sidestep cyclical plunges, but lack the spark for a breakout. Growth persists, but increasingly leans on fiscal stimulus, spending by high earners and “temporary boosters” like rearmament or AI investment - props that guard the floor, but don't unlock the ceiling.

In the US, the narrative shifts from recession fears to a prolonged soft landing: fiscal policy keeps the economy afloat, while weak productivity, high capital costs and uneven consumer spending cap growth potential. Europe inches ahead on policy tailwinds, but is held back by trade frictions and misaligned industrial structures. Japan has scant room left for monetary easing from its extreme stance. China dodges a hard landing, but reverts to its old export-and-state-investment playbook. Amid this tableau, India and the “emerging but not quite” economies shine as rare bright spots in a fragmented world.

Against this ground-level uncertainty, asset markets at higher altitudes follow simpler logic: USD enters an orderly weakening cycle, gold emerges as a defensive haven, and AI infrastructure remains a growth engine - even if it hasn't yet delivered productivity leaps matching the capital it's absorbing.

The common thread across 2026 economies boils down to one line: fiscal firepower is becoming the “anchor” of the economic cycle, shielding the world from crashes but also blocking a return to sustainable growth paths. Traditional recessions grow less likely, but erosion of policy room, institutional trust and long-term productivity emerges as the new core risks.

2026 thus isn't a year of extreme scenarios, but one of accumulating small deviations - flatter cycles on the surface, more complex undercurrents beneath. This sets the stage for our deep dives: US, Europe, Japan, China, India, USD, gold, AI, and fiscal as the pillar of a low-growth era.

In this piece, Viet Hustler unpacks the 2026 global economic picture, guiding readers through ten sections, each tackling a core question:

US: Why it avoids recession but hits a growth ceiling.

Stagflation-lite: Why inflation lingers without reigniting.

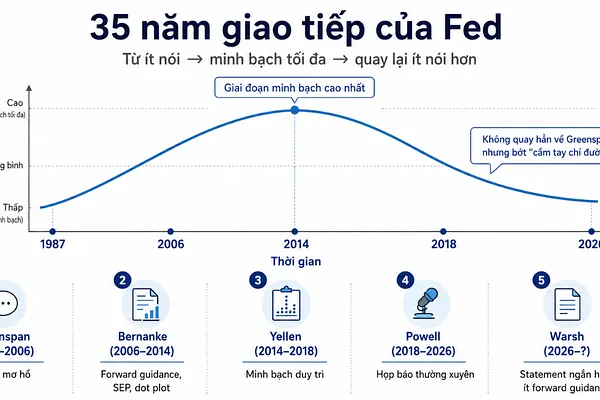

Fed: Why the Fed cuts rates despite not “winning” on inflation.

BoJ: Why Japan has room for just one small step.

USD & Gold: Why USD weakens orderly and gold trends stronger.

Europe: Why fiscal averts recession but trade caps growth.

China: Why it avoids hard landing yet leans back on exports.

India & Developing: Why inward focus becomes an edge.

AI: Why investment surges but productivity lags.

Fiscal – Cycle Anchor: Why fiscal becomes the default buoy for the cycle - while capping growth peaks and building long-term imbalances.