If You Missed Our Best Recent Articles:

Tesla's Q4/2025, on the surface, wasn't a bad quarter:

Gross margin rebounds to 20.1%

Balance Sheet Remains Rock Solid

Balance sheet remains robust with over $37 billion in cash.

But behind those figures lies an undeniable reality:

Vehicle deliveries decline -15.6% Y/Y

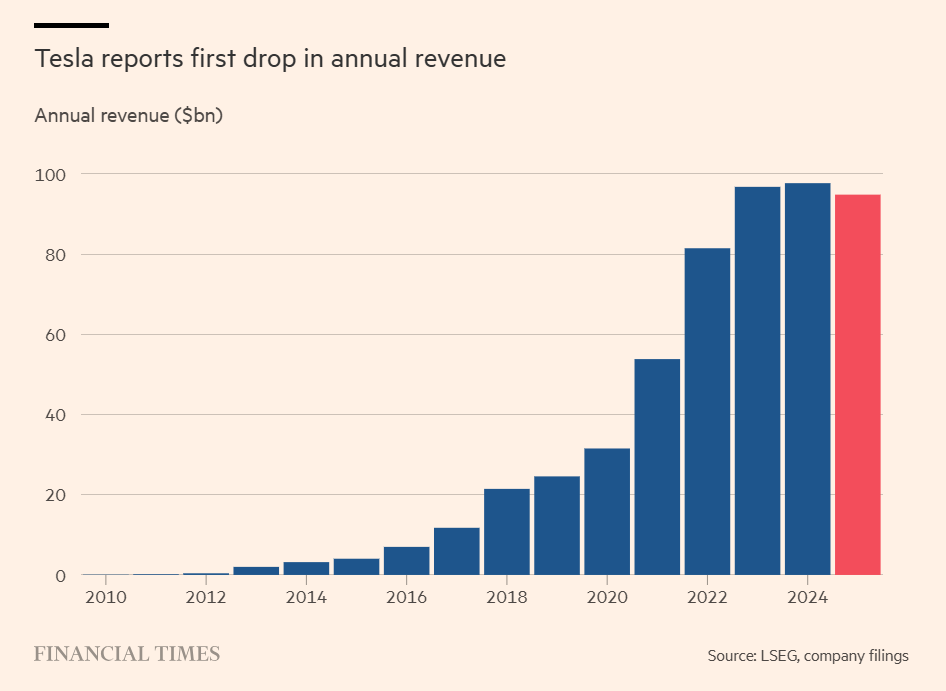

Full-year 2025 revenue falls -3% Y/Y – Tesla's first annual contraction since going public.

The auto segment, which accounts for over 70% of revenue, is clearly slowing amid intensifying competition

All market expectations are now pinned on the 'future': Robotaxi, Optimus, AI and a vision far beyond an EV maker.

Thus, Tesla's Q4/2025 is no longer just an earnings puzzle, but a litmus test of whether those grand promises can offset the weakening traditional car sales engine fast enough.

In this week's article, Viet Hustler dissects Tesla's Q4/2025 earnings report with readers and assesses where the growth story stands in its new cycle.

Q4/2025 Earnings Overview

As China Rises and Politics Turns Away: Tesla Losing Ground in EU, Canada, California

Repositioning the EV Business: Ditching 'Premium Automaker' to Pave Way for Autonomous Era

Robotaxi: Ready But Not Yet Scalable

Optimus & Potential SpaceX M&A – Story or Real Strategy?

Biggest Promise: Optimus & Potential SpaceX Merger – Narrative or Strategy?

releases Q4 2025 financial results: slight beat on earnings | Electrek")