Note: Recently, many readers have not been receiving Viet Hustler articles as the automated email system has been flagging them as Spam due to declining engagement rates. Viet Hustler and Tạp Chí Phố Wall continue to operate in parallel with no changes.

Account migration portal from Viet Hustler to Tạp Chí Phố Wall:

Enter your Viet Hustler account email

Receive a coupon via email for the unused balance from Viet Hustler

Use the coupon to register for a Tạp Chí Phố Wall account

You must manually cancel/turn off auto-renew for Viet Hustler on Substack

https://tapchiphowall.com/viethustler

If you missed our best recent articles:

The AI Token Economy, Tokenmaxxing & The AI Physical Bottleneck

6 Signals to Determine the Strength of the U.S. Economy in 2026

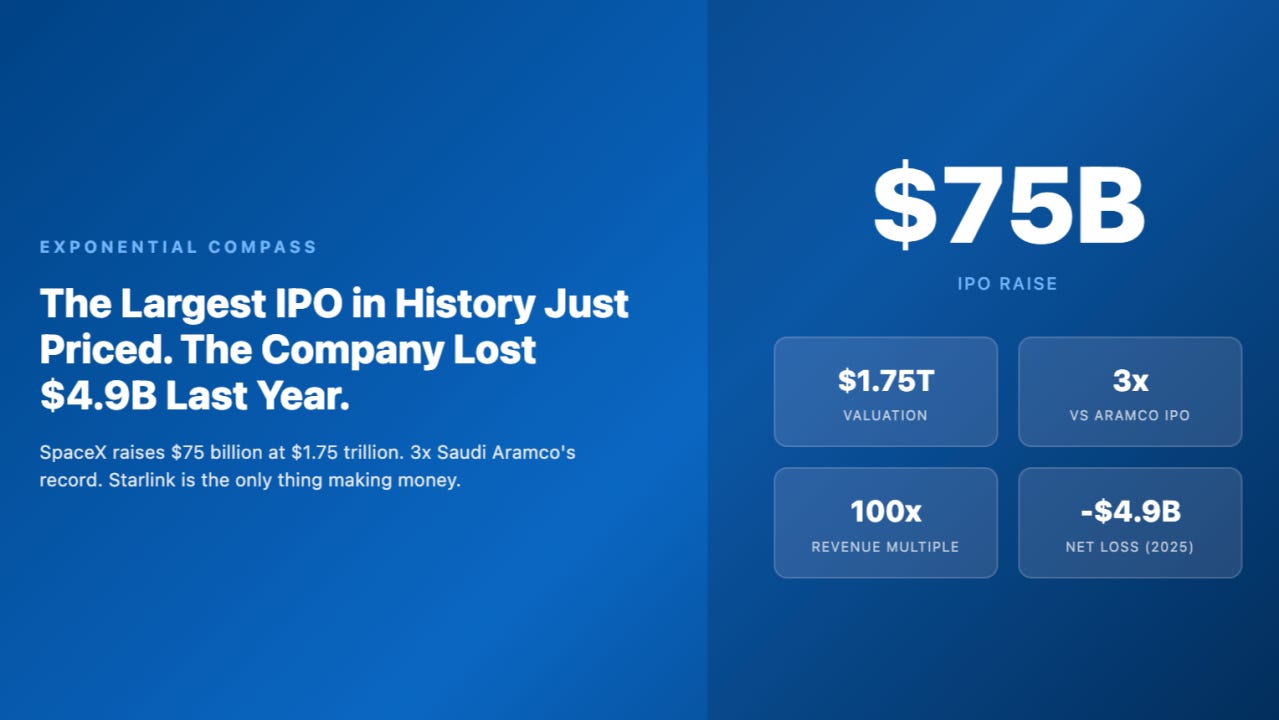

$2 trillion is the price tag for SpaceX-a company that just lost $4.9 billion last year.

The figure sounds absurd, but the most absurd part isn't the loss-it's the reason for it.

SpaceX was profitable in 2024.

Then it merged with xAI-Musk's own AI company-in February 2026, and xAI brought along a $6.4 billion operating loss, double its own revenue.

Full-year negative free cash flow: $13.9 billion.

In Q1 2026 alone, it posted a net loss of $4.28 billion-in just one quarter.

To put the $2 trillion into context:

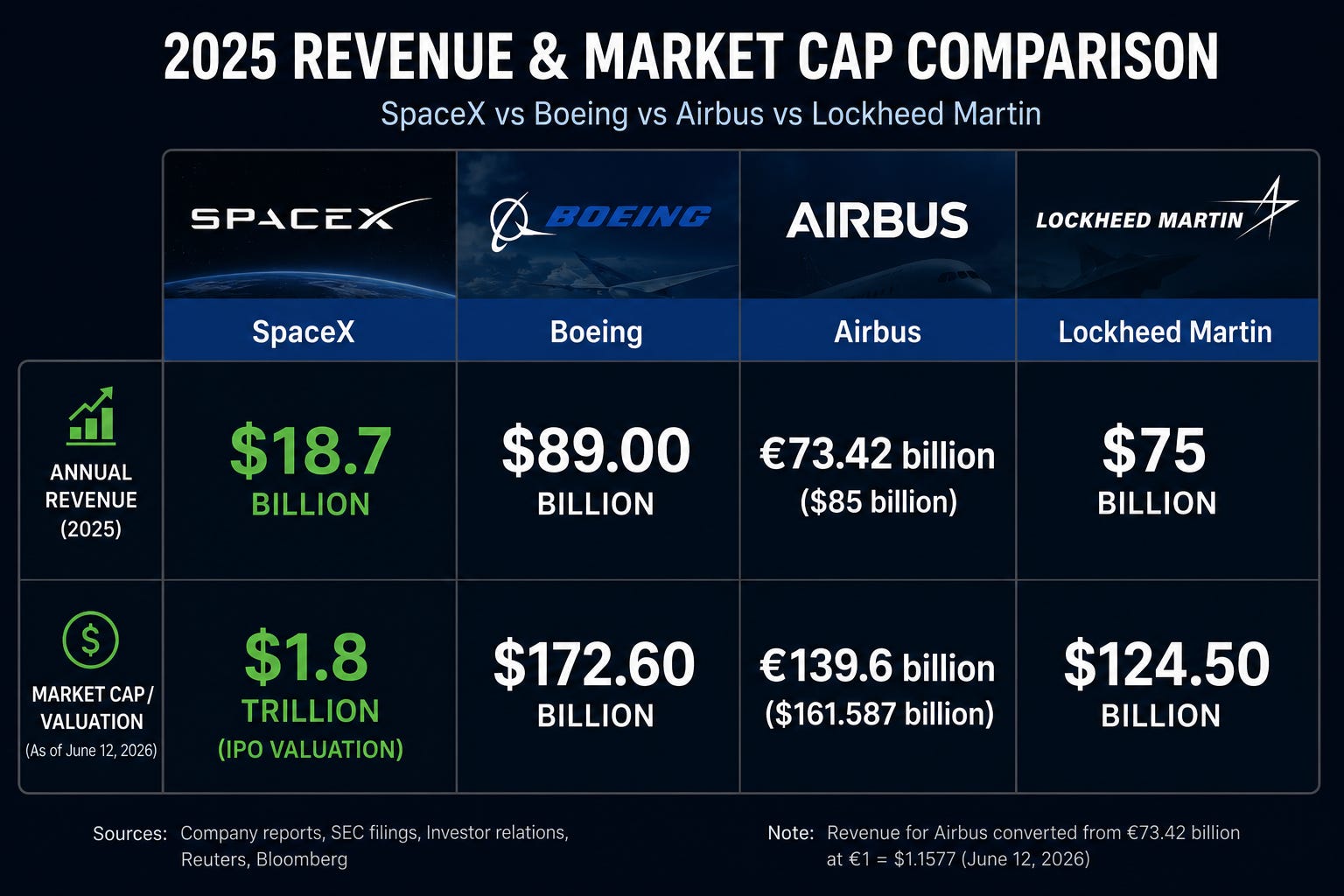

SpaceX is currently more expensive than the combined market cap of Boeing ($172.6 billion), Airbus ($161.6 billion), and Lockheed Martin ($124.5 billion).

The three aerospace/defense giants generated approximately $249 billion in combined revenue in 2025-13 times that of SpaceX-and still only account for 22% of its market value.

Valuation metrics make the story even more unusual.

EV/Revenue is around 107x. Hyperscalers typically trade around 8-15x.

Even the most expensive SaaS companies at their peak only reached about 30-40x.

Most mature industrial businesses trade at just 1-5x.

EV/EBITDA is around 310x.

Net profit shifted from profitable the previous year to a $4.9 billion loss.

But looking deeper, this is an AI business burning cash at one of the fastest rates in the world, while the Starlink satellite division must constantly generate cash flow to fund that entire ambition.

Aswath Damodaran-the finance professor dubbed the "Dean of Valuation"-calls it "an all-in bet on AI and Elon Musk" and places the fair value at $1.25–1.35 trillion, 30-35% lower than the current level.

This is also the central thesis of this week's analysis.

SpaceX is not merely a business. It is Starlink generating cash flow to feed two massive megaprojects simultaneously, while the rest of the valuation primarily reflects optionality for future scenarios.

At an equity value of around $670 billion, the intrinsic value could still be defended.

But at over $2 trillion, almost all the upside has already been priced in.

Our SOTP yields ~$1.2 trillion. The market is paying $2.04 trillion-170% of that figure.

To achieve an 8% market-equivalent return from this price over 5 years, SpaceX must grow EBITDA at ~67% per year-from $6.6 billion to nearly $86 billion.

Apple, the most profitable company on the planet, has a total EBITDA of ~$145 billion. SpaceX must reach nearly 60% of that figure in 5 years just for you to break even against the S&P index.

This price leaves no room for "very good"; it demands "unprecedented in history."

In today's article, Viet Hustler will dissect each layer of SpaceX's value with you to answer the question: at the current price, even if everything goes according to plan, does SpaceX still offer an attractive enough return for investors?

Decoding the $2 trillion-Three re-ratings in 6 months

Three businesses, three economic natures

Starlink-The cash cow carrying the empire

xAI-The most controversial part of the valuation

Starship & Billion-dollar dreams

SOTP Valuation-What is SpaceX really worth?

Investment Strategy-What price is worth buying?