In case you missed our recent top articles:

The $700 Billion AI Capex Race: Who Is Making Money and Who Is Burning It?

US Airlines Q1/2026: Sold Out Tickets, But Wiped Out Profits

Private Credit: Not 2008 - But the Most Dangerous Since 2008

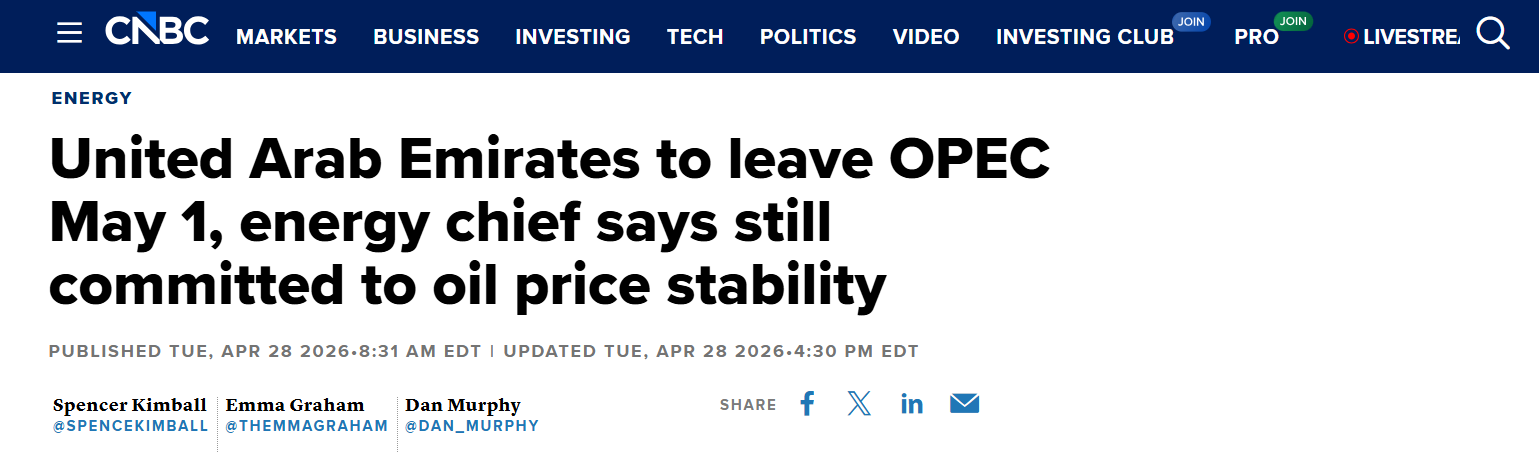

On April 28, 2026, the United Arab Emirates (UAE) officially announced its departure from OPEC, effective May 1, after 59 years of membership.

At first glance, this is just a bad headline for an organization that has been losing influence for decades. But upon closer inspection, this is the largest domino ever to fall:

The largest producer ever to leave OPEC

Accounting for approximately 12% of the cartel's total production

Actual capacity of 4.8 million bpd was suppressed under a quota of just 3.2 million bpd.

The double-edged sword here:

On the supply side:

The US, Brazil, Guyana, and Canada have pushed non-OPEC+ production to 55 million bpd.

The US alone produced over 13 million barrels of crude oil per day - more than any OPEC member.

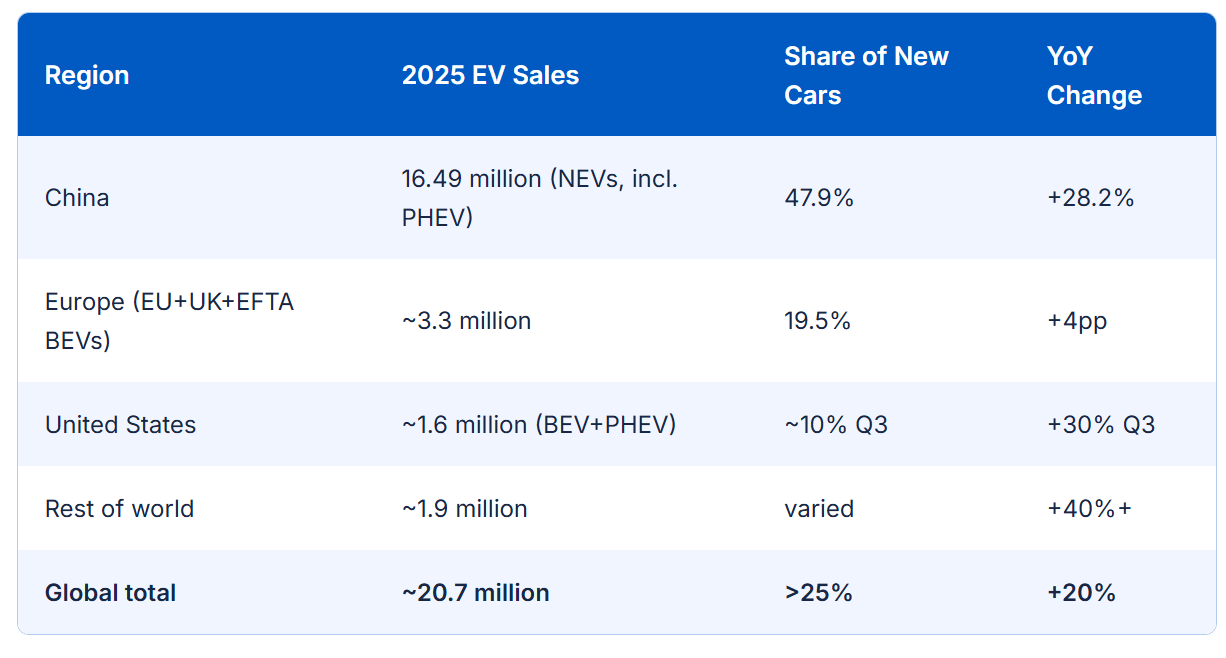

On the demand side:

EVs accounted for nearly 50% of new car sales in China in 2025.

The International Energy Agency (IEA) forecasts that global oil demand will peak around 2030.

EVs will displace 5.5 million bpd by the end of the decade - 5.5 times the 1 million bpd level in 2024.

Two blades cutting simultaneously, with OPEC caught in the middle.

Countries leaving OPEC is not the cause - but a symptom of a feedback loop that has been brewing since 2019.

As market share shrinks, the cost of membership rises, and the incentive to exit increases.

This is the Prisoner’s Dilemma playing out in real-time in the oil market.

The question is not whether OPEC will collapse - but at what speed it will do so, and who will be the next to walk out the door.

In today's article, Viet Hustler will dissect OPEC through three lenses: the game theory of cartel disintegration, intermarket transmission mechanisms, and the map of macro opportunities unfolding ahead.