Sunday Politics: What Does the Democratic Party Need to Change? Charlie Kirk and Gavin Newsom

Great PODCAST by Gavin Newsom and Charlie Kirk, discussing what the Democratic Party needs to change to succeed in 2028. This PODCAST clearly shows that even those who disagree can sit down to find common ground. Since the video was hit with copyright on Youtube, Steve uploaded it to X

“A strong currency can kill inflation – but it can also strangle the entire economy.” - Eduardo Levy Yeyati, Torcuato di Tella University (2025)

Argentina is walking on a bamboo bridge spanning the abyss: one side is the dollarization dream that Javier Milei promises will “liberate” the country from hyperinflation, the other is the ominous shadow of debt crisis and depleted reserves. Each step creaks with the bamboo, while below are waves of speculation and endless market skepticism.

In less than two years, the “liberty lion” has pulled CPI from 289% down to 5% - an unprecedented achievement. But the price is a peso overvalued by more than 40% of its real value, exploding imports, foreign reserves shriveled to 5 billion USD, and political trust crumbling after the Buenos Aires election defeat and Karina Milei scandal. Is the “Milei miracle” still a “miracle” now?

Washington extends the “protective umbrella” through Treasury Secretary Scott Bessent's promise: “The US will do everything necessary to stabilize Argentina.” But is the umbrella wide enough to shield from the storm, or just a thin tarp flapping in the wind?

In today's article, Viethustler will dive deep with you into:

From dollarization promise to retreat: why the “USD dream” turned into a castle in the sand.

Strong Peso – short-term miracle or long-term trap: lessons from exchange rate peg policy.

US Umbrella and the Trust Battle: April pivot, September election shock, and Washington's role.

Three layers of risk if dollarization fails: economic – financial, sovereignty – debt, social – political.

And the final question: Is Argentina being saved, or just breathing on expensive IMF–US oxygen tank?

Viet Hustler is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

1. Context: From political instability to hyperinflation

1.1 Argentina before Javier Milei: spiral of instability

Before 2023, Argentina went through more than a decade of macroeconomic instability, tied to three characteristics: chronic inflation, recurring debt crises, and loss of faith in the peso.

Inflation “erodes” social trust: For many years, Argentina was among the countries with the highest inflation in the world. During 2018–2022, inflation was consistently above 50%/year, and by 2023, it exceeded 100% then 200%, depleting people's purchasing power.

The peso continuously depreciated, making all social classes accustomed to measuring value in US dollars rather than the local currency.

In just 10 years, the peso has evaporated 99% of its value against USD, amid cumulative inflation over 300%. This is not just a crisis cycle, but a prolonged process of eroding trust, turning Argentina into a “dual currency economy” (dual currency economy), where people receive salaries in pesos but save and price assets in dollars.

Recurring debt crises: Argentina has defaulted multiple times in the 21st century (2001, 2014, 2020), causing international bonds to always be heavily discounted. The government continuously relies on issuing pesos and borrowing from IMF to finance spending, creating the image of an economy 'living on shaky credit.' Foreign exchange reserves frequently drop to alarming levels, making any shock easily trigger an exchange rate crisis.

Political trust crisis: Successive governments, mainly associated with Peronism (populism), are seen as 'spending addicts.' They prioritize energy, food subsidies, and public wages to maintain social stability, but this balloons the budget with constant deficits. People and international investors view Argentina's political system as a machine that reproduces crises.

As the 2023 election approached, this picture created a powder keg foundation: society exhausted by inflation, investors losing patience, IMF becoming a permanent 'midwife,' and the peso regarded as worthless paper. In that context, Javier Milei's radical message-closing the Central Bank, replacing peso with USD-became a promise to end the crisis cycle forever.

1.2 What is Dollarization?

Dollarization – or dollarization – means a country officially replaces its domestic currency with USD in payments, savings, and pricing. Argentina has flirted with this idea many times, and Javier Milei promised during the 2023 campaign that 'ditching peso, embracing dollar' would end the hyperinflation spiral.

But dollarization is not a magic wand. In theory, it has three main impacts:

Nominal stability : when people only trust USD, this currency will halt inflation expectations, bringing the economy under 'external discipline.'

Trade-off of monetary sovereignty : the country loses the tool of exchange rate devaluation and flexible response to shocks, because monetary policy is at the Federal Reserve (Washington) not Buenos Aires.

One-way street, no turning back : history shows that once dollarized, 'exiting' is nearly impossible. Ecuador after 25 years still struggles to return to the sucre, but in vain.

In practice, Argentina is already a dual currency economy: people receive salaries in peso but save, price assets, and trust in dollars. Due to trust in peso eroded by decades of crises, inflation, and defaults, 'running to USD' has become a survival instinct.

The chart below illustrates the gap between official exchange rate (black) and parallel market exchange rate (green) , along with the 'blue-chip' discount (right chart). As we approach 2025, this gap widens, showing trust in the official peso has seriously eroded.

But this very thing creates a self-destructive spiral: every time instability erupts (politics, corruption, deficits), people rush to withdraw dollars abroad, making peso collapse faster – just as PIIE noted, this is a 'self-fulfilling cycle.'

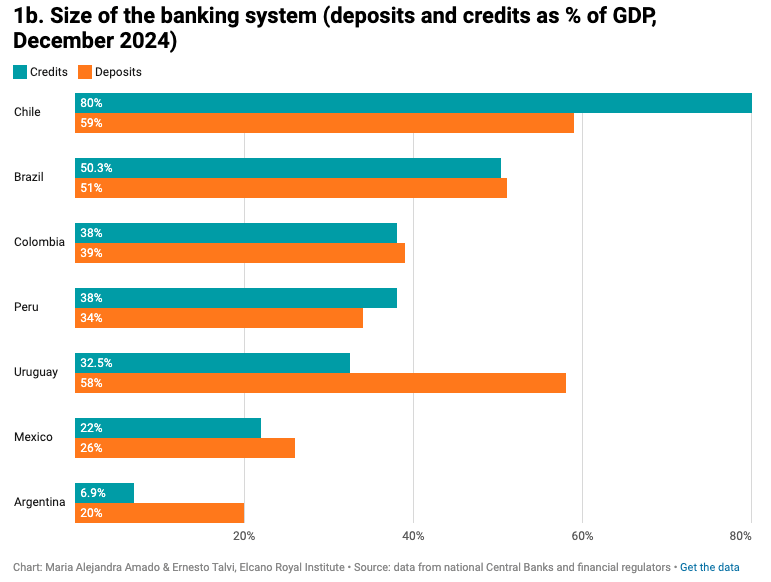

A currency is only strong when it can serve as a foundation for savings and credit. But in Argentina, 'dual currency' has completely eroded this function: people save in dollars, businesses borrow in dollars, and peso is seen as a temporary transaction tool.

The chart below shows the terrible disparity: bank credit in Argentina is only 6.9% GDP, while in Chile it's 80%, Brazil over 50%, and even Mexico over 20%. Deposits in Argentina are only 20% GDP, much lower than Uruguay (58%) or Colombia (39%).

This proves a bitter reality: no sufficiently deep domestic financial market , Argentina is forced to rely on external dollar flows and IMF. This is fertile ground for every exchange rate shock and why the 'dollarization dream' is as fragile as a castle on sand.

Dollarization is thus only truly sustainable if a country has stable foreign exchange revenue (like Panama with the canal, or Ecuador with oil). foreign currency liquidity trap Fixed USD debt obligations while revenues 'ebb and flow,' the risk of falling into

foreign currency liquidity trap

is hard to avoid.

If the US really backs dollarization, the price is not just economic. It will weaken IMF's role, put Argentina in a 'one-way-only forward, no backward' position, and even push the region into US–China confrontation as Buenos Aires is tightly bound to Washington's orbit.

In other words: dollarization may extinguish the inflation fire, but it could turn Argentina into a hostage of the greenback-where financial destiny no longer lies in Plaza de Mayo, but in Federal Reserve and US Treasury.

1.3 Why did Milei choose dollarization? When entering the 2023 campaign, Javier Milei built an image as a 'monetary revolutionary.' His central message: inflation results from reckless money printing to finance deficits, and only fully replacing peso with US dollar can Argentina escape the instability spiral. Dollarization became his symbol for three reasons:

Radical nature: In voters' eyes, especially the middle class exhausted by hyperinflation, dollarization brings decisiveness, completely ending politicians' money-printing right. This is not just policy, but a promise to 'cut the cancer at the root' haunting Argentina for decades.

Political symbolism: Milei pledged to shut down the Central Bank-the 'number one enemy' in his speeches. To him, the Central Bank is not independent but a printing machine for the privileged political class. 'Dissolving' it means a vow to eradicate macro corruption. Theoretical foundation:In the book

We miss you Uncle Milty | The Market Monetarist

1.4 Technical and Financial Barriers

Even ignoring theoretical debates, the path to implementing dollarization in Argentina faces almost insurmountable barriers in the short term:

Fragile foreign exchange reserves – an empty wallet before the dollarization dream

For true dollarization, the government must have enough USD to exchange all base money in circulation and simultaneously create a “buffer” to protect the banking system. But Argentina currently holds only a very small portion of usable reserves, while the actual demand reaches tens of billions of USD. This huge gap makes the dollarization promise more like a distant fantasy than a feasible plan.

Current account: fragile surplus

Even as agricultural and energy exports generate significant goods surpluses, Argentina still cannot accumulate foreign exchange reserves sustainably. The cause lies in two chronic “leaks”:

Services (Services): tourism costs, card payments, and service imports continuously drain foreign currency outward.

Primary income (Primary income): the burden of interest payments on debt and dividends to foreign investors is regularly negative by over 1 billion USD per month.

The chart shows that after Javier Milei took office at the end of 2023, goods exports (green line) once brought in more than 3.5 billion USD/month, but outflows from services (red line) and primary income (purple line) immediately “erode” the gains, plunging the current account into deficit.

Foreign currency liquidity trap

The result is a paradox: trade surplus but no accumulation. Argentina is trapped in foreign currency liquidity trap, where USD debt repayment obligations are fixed like clockwork, while foreign currency inflows are erratic, prone to evaporating with seasonal and international price fluctuations. This is the fatal weakness of the dollarization dream.

The second chart shows it more clearly: from mid-2024, the foreign currency balance reversed sharply, with a string of monthly deficits over 1 billion USD. In other words, more dollars leave Argentina than flow in, depleting the ability to accumulate reserves.

Debt market strangulation: Argentina has defaulted multiple times, causing government bonds to trade at heavy discounts. To gather USD by issuing or selling more debt, the government would have to accept “usurious” interest rates. Thus, instead of reducing risk, dollarization could push the public debt burden to unsustainable levels.

Chaotic conversion risk: Dollarization requires absolute public trust. If citizens doubt the government has enough USD to back it, they will rush to withdraw pesos and switch to dollars, exploding the black market and sending exchange rates skyrocketing out of control. In that scenario, instead of extinguishing inflation, the conversion process would ignite a new wave of inflation, destroying trust in just weeks.

Internal resistance: Some ministers and economic advisors see the implementation costs of dollarization as too high compared to short-term benefits. They opt for a softer approach: easing controls, allowing dollar use in some transactions, and maintaining a “managed float” exchange rate mechanism instead of diving straight into “full dollarization”. This is why, after the first few months in power, Milei was forced to back away from the full dollarization promise, at least in the near term.

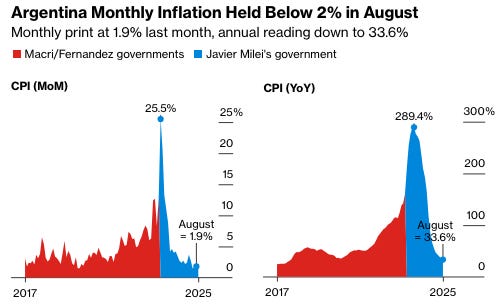

Case study 2024–2025 clearly shows implementation failure: Milei achieved initial successes – balancing the budget, pulling inflation from 289% (4/2024) down to 34% (8/2025). But due to an obsession with fighting inflation, he kept the peso too strong. Consequence: imports ballooned, foreign reserves were not accumulated, Argentina fell into a situation of “successful price holding but empty treasury”. This distorted exchange rate policy reveals a paradox: Argentina's problem is not only in extreme monetarism theory, but also in technical mistakes in management. Dollarization thus becomes even more distant – not due to lack of will, but because the financial foundation is insufficient to cross over.

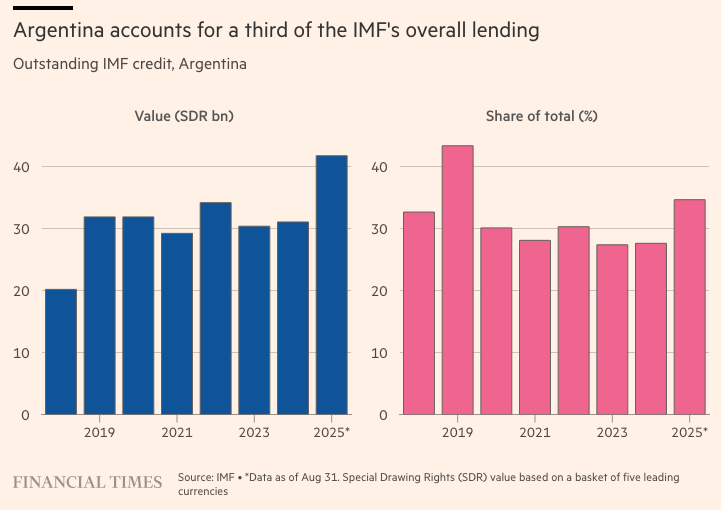

The chart below clearly illustrates this pressure: Argentina currently accounts for up to one-third of the IMF's total global debt. That means, not only thin reserves, but the entire national financial structure is heavily dependent on external bailouts. With borrowing over 40 billion SDR (2025), any shock could shake the entire dollarization foundation.

→ Since 2018, Argentina has continuously been among the largest IMF borrowers, and in 2025 it returns to a new peak. If dollarization requires a “buffer” of self-owned USD reserves, the harsh reality is that Argentina is living on “IMF oxygen”. This makes the dollarization ambition like building a castle on sand – beautiful in theory, but lacking the foundation to realize.

1.5 Strong Peso – the hidden cost in success:

With a valuation 40% higher than real, the peso helps curb import prices and slow consumer price increases. But the price to pay is lost export competitiveness, ballooning imports, and no USD reserve accumulation.

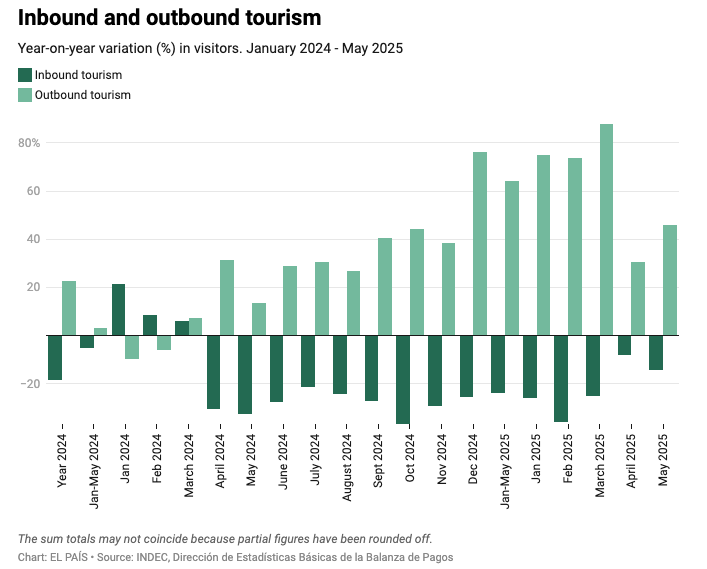

Social reality even more reflects this paradox. The peso is so strong that 8.4 million Argentines traveled abroad in just the first four months of 2025, up 68% from the previous year, turning trips to Brazil or Europe into “bargains”.

But the cost is a leaky current account balance, export businesses squeezed on profits, rising unemployment, and shrinking foreign reserves. Milei may win the psychological battle with voters with “strong peso = lower inflation”, but loses in accumulating financial strength to protect the dollarization dream.

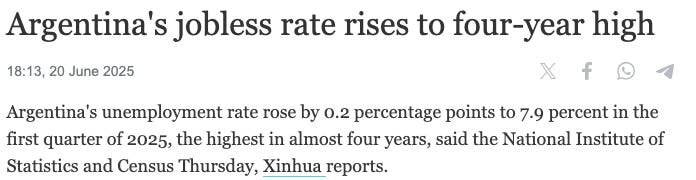

Domestic businesses struggling: exports squeezed on profit margins, cheap imported goods making small producers struggle, unemployment climbing to the highest level in 4 years.

Although Milei is seen as the most market-friendly president in decades, the business community still keeps wallets closed. A business leader bluntly:

“The business class has never been so satisfied with a president, but they still won't invest – except in energy and mining. As long as capital controls are not lifted and labor reforms are not passed, no one dares to take risks.”

2. Latest developments: the US “protective umbrella” and the battle for market confidence

2.1 Short-term miracle: floating the peso and the downside of success

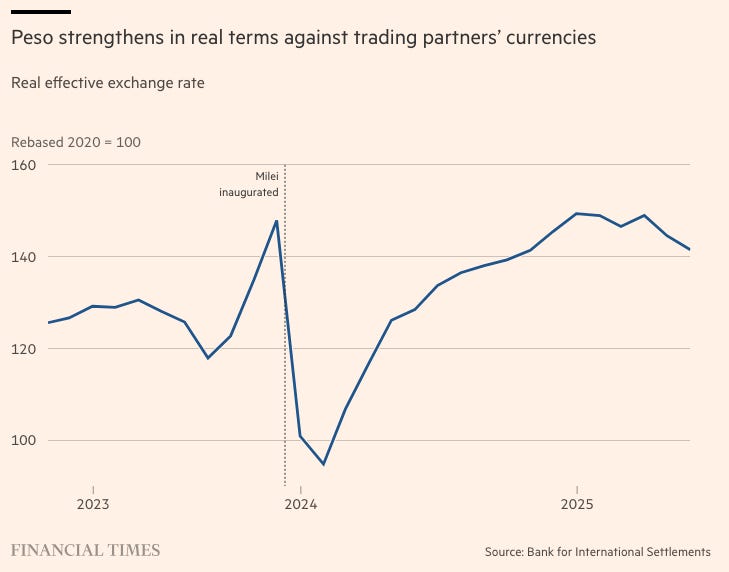

If 2024–early 2025 was the phase where Milei “held the fort” with a strong peso and capital controls, then April 2025 marked a turning point. Milei unexpectedly lifted part of the foreign exchange controls – a “double gamble”: both easing reserve depletion pressure and proving the political strength of reforms. With “jumbo loan” 20 billion USD from IMF (12 billion disbursed immediately), plus 5 billion USD extension from China and “full support” signals from Washington, Milei has extra oxygen to try floating the peso in a new band.

The chart below shows: after lifting controls (early April), the peso fell about 6% in the first week, but quickly stabilized around 1,100–1,200 ARS/USD, meaning it still below the 1,400 ceiling of the managed band. Milei sees this as a double win: reducing pressure to burn reserves, while maintaining the narrative “strong peso = dead inflation”. In reality, monthly CPI has fallen to the lowest level in 5 years.

But that “miracle” hides a hidden cost. Peso is kept ~40% above its real value, causing exports less competitive, imports ballooning, USD reserves not accumulating.

2.2 Election Shock and Crisis of Confidence

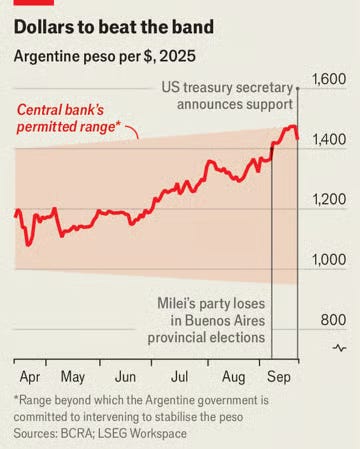

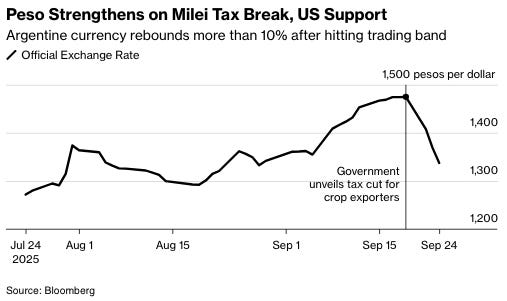

That weakness was exposed right when Milei needed political strength. In September 2025, his Liberty Alliance suffered a heavy defeat in the Buenos Aires local elections, which account for more than one-third of the national population and are seen as a “barometer” for mid-term elections. The Peronists won overwhelmingly, turning this election into a failed referendum on the Milei government.

At the same time, a corruption scandal involving Karina Milei, his sister and chief of staff, erupted, tarnishing the image of an “anti-privilege government”. Allegations claim she received bribes from a state contractor, while Karina is the second most powerful figure in Milei's political machine. This scandal deepened internal divisions: many moderate parties turned away, the congressional alliance cracked, and provincial governors began bargaining for more money from the central budget.

Immediate economic-financial consequences: peso lost nearly 10% in the two weeks after the election, Central Bank of Argentina (BCRA - similar to US FED) was forced to sell net 1.1 billion USD in just three days to hold the exchange band, causing net reserves to drop to 5 billion USD – an extremely fragile level for an economy of 45 million people.

USD bonds plunged, yields surged, and default risk flickered again.

The chart below clearly shows the peso's downward trend throughout Q2–Q3/2025, when the currency fell freely to nearly 1,500 ARS/USD before a slight recovery thanks to support signals from Washington:

Analysts call this a “wake-up call”: Milei, who likes to compare himself to an “invincible lion”, suddenly becomes a “lion doused with cold water”. The combination of exchange rate mistakes, election defeat, and political confidence crisis has turned the “Milei miracle” into a fragile battlefield – where any shock could trigger financial chaos.

2.3 US Intervention: Reassuring Signal or Real Bailout?

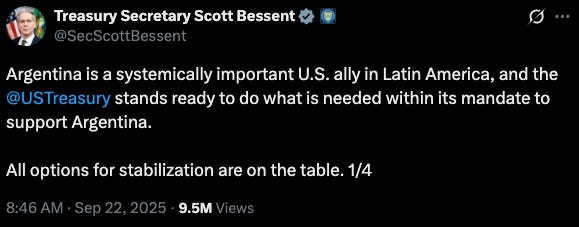

The pivotal moment happened in the early morning of 22/9/2025. Just 15 minutes before the Buenos Aires forex market opened, US Treasury Secretary Scott Bessent unexpectedly posted on X: “Argentina is a systemically important ally to the US. We will do whatever is necessary to stabilize.”

The next day, he flew to meet Milei, committing to negotiate a swap line 20 billion USD with BCRA and ready to buy Argentina's USD bonds on the secondary market. Donald Trump also added fuel to the fire by declaring Milei “doing a fantastic job”.

This is an extremely rare move: The United States publicly backs a currency and a “junk-rated” debt market not because of a global crisis, but because of a domestic political risk of an ally. Symbolically, Washington is telling the market: “Argentina's exchange band ceiling now has the US behind it.”

The chart below illustrates: since April 2025, peso has been floating within a managed band defended by BCRA. But after the Buenos Aires election defeat (7/9) and Karina Milei scandal, the peso immediately hugged, even breached the upper ceiling at 1.475 ARS/USD. In the two days 17–18/9, BCRA had to sell more than 1 billion USD to stop the fall. Right at the “breaching ceiling” moment, Bessent's statement appeared, pulling peso back and cooling devaluation expectations:

Possible toolkit (technical):

USD swap line for BCRA: Short-term USD swap loan, renewable, relieves temporary liquidity thirst and helps BCRA avoid burning reserves on the spot. The key points are activation conditions (exchange rate level, volatility, trading volume) and committed interest/cost ratio.

Direct USD purchase in the market: US Treasury (via Exchange Stabilization Fund – ESF) can participate in buying/selling forex to “thin out” one-sided speculative attacks, creating a sense of “infinite buyer” behind. This method is immediately psychologically effective, but usually only used short-term as it easily creates dependency.

Repurchasing Argentina's USD bonds: If the US uses ESF or coordinates with multilateral institutions to suck risk out of the yield curve, the spread will fall, paving the way for smoother refinancing. However, this easily raises big moral hazard questions.

Immediate market impact:

Exchange rate: Peso rallied, escaping the “testing ceiling” zone of the managed band.

Assets: Bank – consumer stocks recovered first, then spread to cyclical tickers.

True scale of the support package: $10 billion is only enough for a “short blanket”; at least $15–20 billion is needed to create lasting confidence.

Attached conditions: Will the US attach support to fiscal discipline and reform progress as the IMF usually does?

Timeline & exit strategy: Is this a long-term commitment, or exactly as Bessent implied - just a “bridge to the election”?

Assessment: US sponsorship is likely hard to sustain long-term: peso is currently overvalued by at least 30% compared to reality, while the current account deficit balloons. As the October mid-term elections approach, sellers will test the resilience of the “US umbrella” again. If Milei fails politically, Washington will struggle to indefinitely prop up a currency anchored away from its fundamental value.

Strategic implication: Essentially, Washington is telling the market: “Argentina's exchange rate band ceiling is backed by the US.” If confidence in this statement is strong enough, the market won't require the US to fire many real bullets. If confidence is thin, people will test the resistance level – and then, bullet size becomes a matter of survival.

2.4 Indirect “dollar pumping”: trading taxes for liquidity

While waiting for the full US umbrella deployment, the Milei government rolls out another “temporary relief” move: waiving or reducing export taxes on key agricultural products (soybeans, meal, oil, corn, wheat, then expanding to meat and poultry) until the end of October, or until reaching the $7 billion registration milestone.

The mechanism is very simple: when taxes decrease, each USD of farmers' revenue can be exchanged for more pesos → they are willing to sell USD through official channels instead of hoarding. In the coming weeks, foreign exchange supply will be more abundant, creating an “oxygen breath” for peso.

But this oxygen comes at a price:

Budget bleeding: revenue from export taxes – which currently account for a large proportion – evaporates. If the government doesn't cut spending elsewhere, fiscal discipline is broken, and market confidence wavers again.

Misaligned expectations: farmers may hold back goods waiting for the “next incentive” every time a crisis returns.

Market fragmentation: privileged groups sell USD cheaper, others will try to anchor prices to the black market dollar. Latent inflation returns from there.

This is just a “trade time for space” measure, like staunching blood on the battlefield with bandages – not surgery.

3. Consequences if “dollarization” fails?

Milei đã chữa được “nửa” lạm phát. Nửa còn lại nằm ở tỷ giá và năng lực hấp thụ sốc.

Dollarization is portrayed by Milei as a “miracle drug” to cure chronic inflation. But in Argentina's political-economy, miracle drugs easily turn into poison. If this process fails, or is reversed in chaos, Argentina will face three layers of risk: economic-financial, sovereign-debt, and social-political..

3.1 Loss of policy flexibility – from nation to “peripheral province” of the Fed

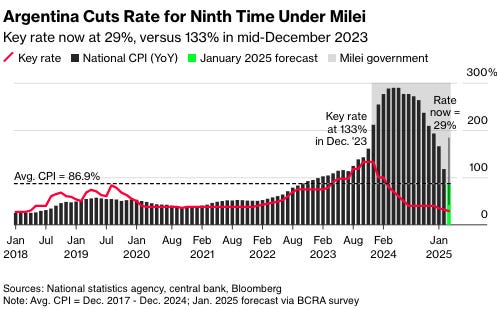

Milei has achieved what many previous presidents failed to do: cutting subsidies, streamlining payroll, balancing the primary budget, and forcing BCRA to stop printing money to finance deficits. Result: monthly CPI plummets from 12.8% (12/2023) to 1.9% (8/2025). He has addressed the biggest root cause of hyperinflation – the “money printing machine.” But inflation in Argentina has two roots, and Milei has only solved half.

The other half lies in the exchange rate anchor. BCRA maintains a “crawling peg” mechanism to avoid devaluation shock, but when domestic prices rise high, peso becomes artificially expensive: imports explode, exports shrink, USD reserves don't accumulate. In a politically unstable context, just one slip in confidence, and the peso flight spiral reappears. Milei has shut off the money printing tap, but the exchange rate wound is still open and reserve bandages are too thin.

Washington can cool things down with swap line, debt purchases, or ESF interventions – but that's only temporary USD bullets to douse the fire. Sustainable solutions must be clear:

One is, controlled exchange rate liberalization, allowing peso to return to a competitive level while maintaining expectations through fiscal discipline.

Two is, full dollarization, but then Argentina deprives itself of all shock-absorbing tools:

Cannot print money to bail out banks.

Cannot lower interest rates to fight recession.

Cannot devalue to support exports when commodity prices plummet.

In this scenario, 45 million Argentines will “depend on” Fed monetary policy – an institution concerned only with inflation, employment, and the US economic cycle. Then, Buenos Aires would be no different from a “monetary peripheral province” of Washington, and a sneeze from the US could turn into pneumonia in Argentina.

Regional history shows another way out. Mexico (1994–95) and Brazil (1999) all once broke the exchange rate peg, but they did not fall back into hyperinflation because they managed to establish three institutional pillars:

Independent central bank.

Transparent inflation targeting.

Strict fiscal discipline.

Thanks to that, from 2000 to now, both Mexico and Brazil have maintained single-digit inflation. Meanwhile, Argentina is still struggling around an average of 70% due to lacking the institutional foundation to protect expectations after abandoning the peg. In other words, the core issue is not choosing USD or peso, but whether Argentina has sufficient institutions to stand firm once the exchange rate peg is severed.

Washington's commitments (swap line, debt purchases, ESF interventions) may help cool short-term peso selling pressure. But that is only USD bullets to put out the fire, not a mechanistic solution.

Option A – Exchange rate flexibility: Let the peso fall to a competitive level, but anchor inflation expectations with fiscal–monetary discipline. Initial positive signal: the recent peso slide has not caused inflation expectations to explode. But if Milei loosens spending due to political pressure, the effect will reverse.

Option B – Full dollarization: easy to sell to voters and suits Trump's taste, but it will eliminate shock absorption capacity. Unable to devalue, the economy will only have wage cuts – accept unemployment to adjust competitiveness. A kind of “stability through pain,” with enormous social costs.

Washington can cool things down with swap lines, debt purchases, or ESF interventions – but that's only short-term USD bullets to put out the fire. A sustainable solution must be clear:

Controlled exchange rate float, to bring the peso to a competitive level while maintaining expectations with fiscal discipline.

CB independence, floating exchange rate, tax reform, and streamlined public spending

Or full dollarization, but then Argentina loses all shock absorption tools, left only with wage cuts and accepting unemployment.

Only then can Argentina restore investor confidence.

The chart below shows the current paradox: policy interest rates (red line) have been cut from 133% to 29% in the first few months of Milei's term, but CPI (gray bars) remains around 100%/year. This is precisely why a swap line from the US (5–10 billion USD) can only play a temporary “bridge” role. Market confidence will only return when Argentina establishes a credible macroeconomic policy framework.

Again, dollarization only makes sense when Argentina has stable dollar revenues to cover public debt and imports. But in reality, Argentina's exports (agricultural products, energy) fluctuate sharply with seasons and international prices. If foreign exchange revenues are uneven, while USD debt obligations are fixed, the country will easily fall into foreign exchange liquidity trap – a sophisticated version of default.

The chart below shows the harsh picture: in 2025 Argentina only has to pay about 5 billion USD in foreign debt, but this jumps to 15 billion USD in 2026 and exceeds 20 billion USD in 2027. In the structure, not only IMF but also private bonds, other international financial institutions, and short-term repo agreements – i.e., capital flows that can reverse easily when risks rise.

This turns Argentina into a hostage of foreign exchange liquidity: just one political shock or commodity price reversal, and the country will fall into a state of “chronic USD shortage” – a sophisticated version of default. And even more worrying: “US umbrella” is not permanent. An election in Washington or a political change in the White House could shut off the dollar tap overnight. Then, Argentina will be stuck in a state of “no peso – not enough dollars”: a leaderless monetary economy, with nothing left to support it.

3.3 Political–social risks: loss of sovereignty, loss of patience, loss of confidence

Currency is not just an economic tool, it is also a symbol of sovereignty. When the peso disappears, people may easily feel “forcibly Americanized”. In a society already full of scars from austerity, this feeling can quickly turn into a fire of resistance.

Austerity policy: cut subsidies, raise prices of electricity – water – public services to keep the budget balanced in USD. The poor and middle class, who have already suffered enough from hyperinflation, will have to bear another cost-of-living shock.

Opposition politics revived: Peronists, masters at exploiting social outrage, will not miss the opportunity to portray Milei as “the president selling the nation's soul to Washington.”

Double crisis of confidence: when people lose faith in the peso and also lose hope in dollarization, they will seek personal defenses – hoarding gold, black-market dollars, real estate – instead of entrusting their faith to the system. At that point, not only the currency, but social contract also breaks.

4. Scenarios ahead

4.1 “Breathing room” scenario

If the US pours in a sufficiently large aid package (at least two-digit billions USD), with transparent conditions and fiscal discipline from Buenos Aires, the peso has a chance to stabilize. BCRA will not have to burn reserves daily, and Milei can extend the “honeymoon” of reforms. In that context, indirect dollarization – where USD circulates in parallel with the peso – can continue to operate as a “testing step” instead of jumping straight into the abyss of full dollarization.

4.2 “Default” scenario

If Washington's aid package is just a promise or too small to put out the fire, peso-selling pressure will reignite. Forex reserves depleted, the government forced into a sharp devaluation, fueling the spiral exchange rate → inflation → interest rates → recession. Argentina, instead of entering a period of stability, will write another chapter in its chronicle of crises.

4.3 “Dollarization failure” scenario

Worst case is Milei rushes dollarization without accumulating enough USD, without building political consensus. An unprepared switch could cause bank panic, shatter system confidence, and end with reverting to the peso in a state of exhaustion. At that point, not only the economy but also political institutions will bear another scar of trust.

4.4 Assessment, what Milei should do

Politics first, technique later: Milei needs to expand alliances, increase congressional seats, strengthen capacity through policy. Without a “political stage,” all reforms are just rehearsals.

Transparent rules of the game: With the US and IMF, need to clearly announce the scale, conditions, activation mechanisms for aid. Markets fear ambiguity the most.

Three pillars of discipline: maintain primary budget surplus → rebuild forex reserves → curb expectations of spontaneous dollarization spreading.

Diversify USD sources: besides agricultural products, stimulate FDI, energy, resource extraction to create “sustainable dollar flow.”

Contingency scenario: if the “US umbrella” shrinks, need a domestic defense package: prioritize bank protection, maintain social safety, transparent communication to avoid panic.

Conclusion

Dollarization may be the dream Milei brought to the ballot box, but Argentina's reality exposes it as a gamble placing the entire nation on the red

Dollarization was once preached by Milei as a promise to save the nation, ending the inflation disease forever. But the reality of recent weeks shows this path is no different from walking a tightrope: one side financial abyss, the other political storm.

Washington has opened the “protective umbrella,” but whether the umbrella can withstand the storm or is just a thin tarp, no one knows yet. Argentina is living in a fragile moment, where every decision – from swap line, agricultural tax policy, to the October voter ballot – could pivot the entire economy.

If Milei knows how to use this “breathing space” to consolidate politics, make the rules of the game transparent, and build a sustainable dollar flow, he can dodge a historic fall. But if relying only on painkillers from Washington without treating the root, dollarization will not be “salvation,” but a historic trap.

Argentina has fallen into debt traps, inflation traps, political traps many times before. This time, if they stumble, they could fall into the most dangerous trap: absolute loss of trust trap. And once society no longer believes in either the peso or dollarization, no aid package will be large enough to buy back the lost trust.

. He inherits 'extreme monetarism': no domestic currency means no inflation tool. In that logic, dollarization is the only cure.")

. He inherits 'extreme monetarism': no domestic currency means no inflation tool. In that logic, dollarization is the only cure.")

, by lender showing Argentina's financing needs")