In case you missed our recent top stories:

The $700 Billion AI Capex Race: Who is Making Money, Who is Burning Cash?

Private Credit: Not 2008 - But the Most Dangerous Since 2008

April CPI hit 3.8% - the highest since spring 2023.

Gasoline at $4.50/gallon nationwide, California above $6.

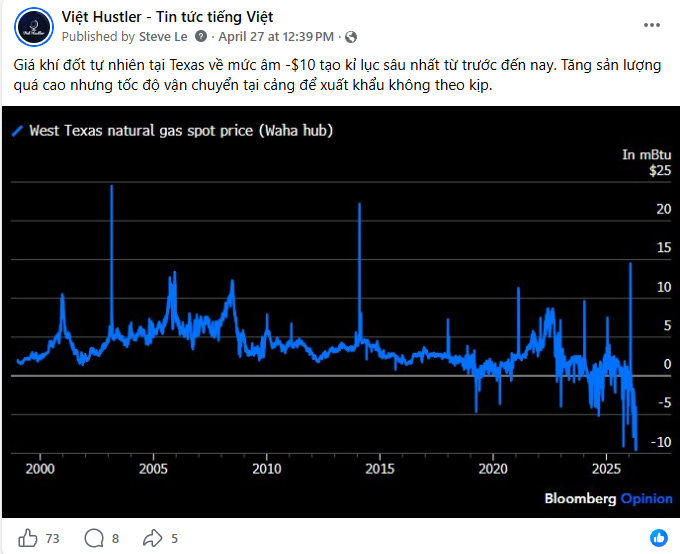

WTI oil at $101.50.

10-year bond yield at 4.45%, edging up from 4.36% in just one week.

Trump approval rating: 34-38%.

That is the backdrop Trump carried as he boarded Air Force 1 to Beijing yesterday afternoon.

He was accompanied by Boeing's CEO, Tim Cook, and Elon Musk. Beijing will likely offer to order Boeing aircraft - potentially up to 500 planes.

And then there will be state dinners, a 'Trade Council', an 'Investment Council'. The exact same playbook as 2017.

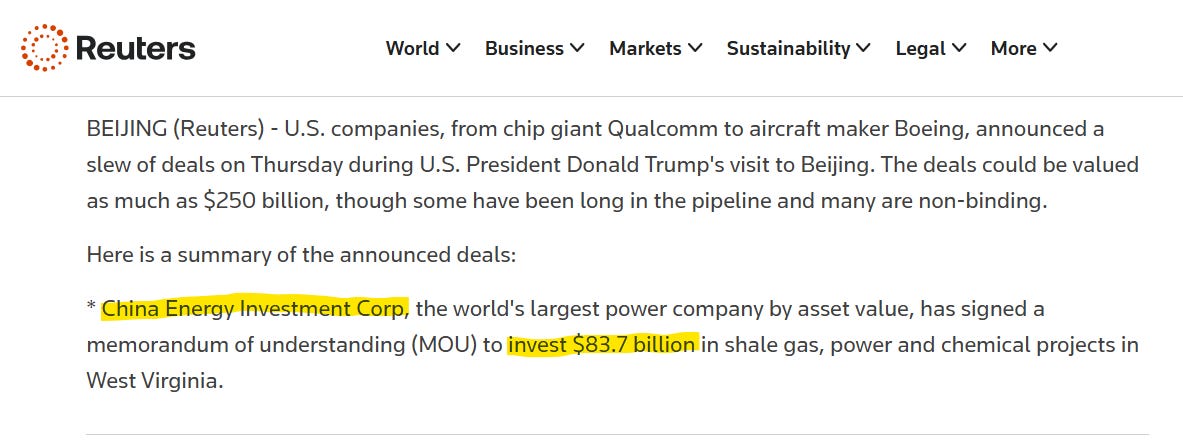

That year, China Energy Investment Corp signed a memorandum of understanding (MOU) to invest $83.7 billion in shale gas, power, and chemical projects in West Virginia.

The value of this MOU even exceeded West Virginia's GDP.

However, this deal never materialized.

Steve commented in his 05/11 video: this should be viewed as a 'checkpoint, not a reset or breakthrough.'

But the crux does not lie in what the cameras capture. It lies in two straits - one ablaze, one keeping Beijing awake at night - and how they are reshaping the global energy chessboard in ways the broader market has yet to price in.

In today's article, Viet Hustler will decode the strategic map behind the Trump-Xi summit - from Iranian oil to Greenland's rare earths, from the DFC's maritime reinsurance mechanism to the 2027 semiconductor race.

The Number Nobody Puts on the Front Page

The Flip Side - China Does Not Just Buy Oil

Two Straits - Proof of Concept & Application

US Energy - The Oil and Gas Divergence

The Resource Race - Locking Down the Backyard

TSMC, Anduril & The Countdown to 2027

Part I. The Number Nobody Puts on the Front Page

A single truth that most media outlets have buried:

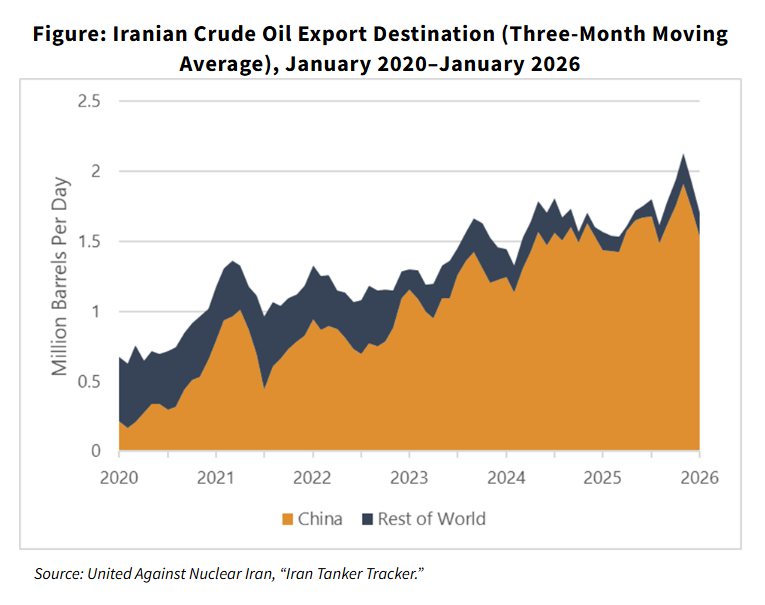

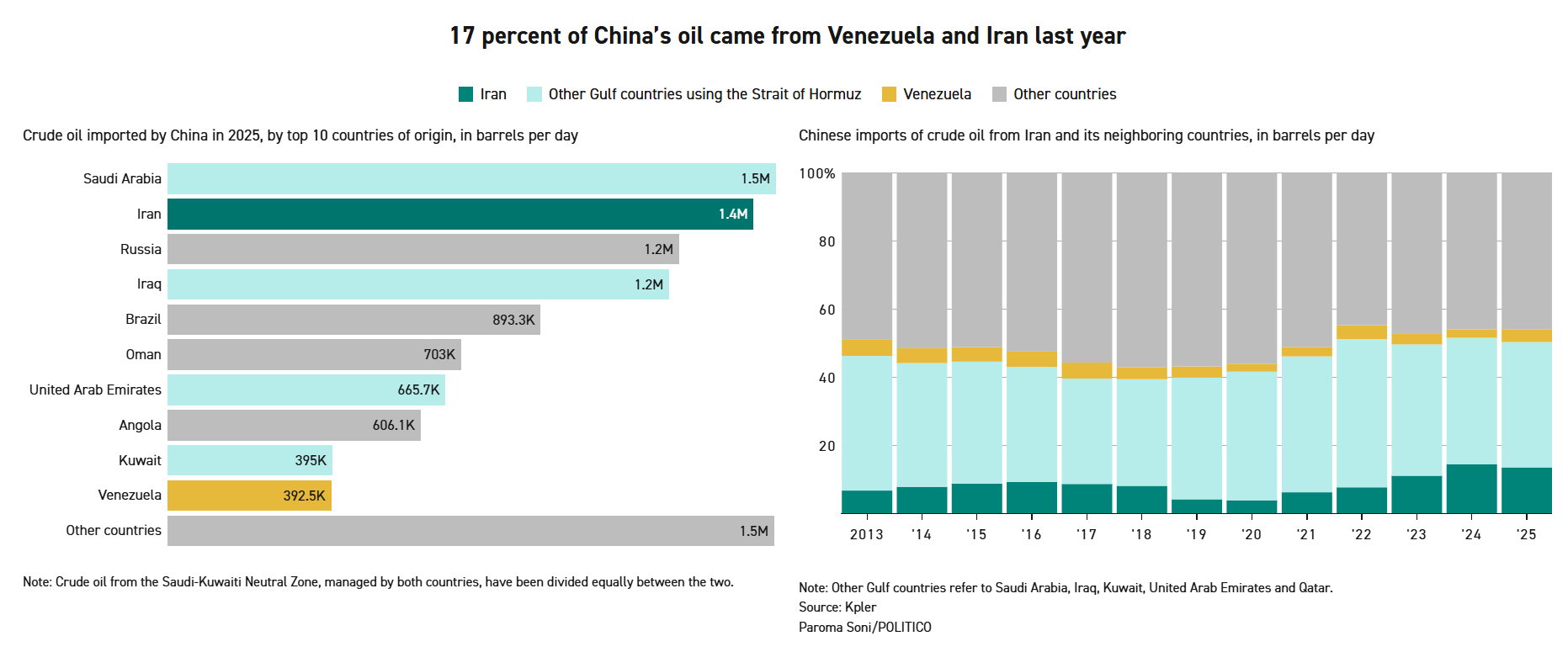

China buys 80-90% of Iran's oil exports.

Kpler's 2025 figure: an average of 1.38 million barrels per day.

The US-China Economic and Security Review Commission (USCC) puts it higher - 1.5 million - Accounting for about 13% of China's total crude oil imports.

This is not an arbitrage trade - it is a discounted feedstock source used to feed the private refinery system in Shandong.

A quick glance at the official trade figures: $9.96 billion in bilateral trade in 2025.

Looking closer: if adding the $31.2 billion in unreported crude oil (tracked by the Tehran Bureau and UANI), total actual crude transactions exceed $41 billion, accounting for over 75% of bilateral trade.

The legal framework on paper: The Comprehensive Strategic Partnership of March 2021. A 25-year agreement. A headline figure of $400 billion in investment.

Reality: almost zero disbursed. Sanctions blocked everything. What this agreement actually produced:

Yuan settlements via CIPS - a parallel payment system to SWIFT

Iran joining BRICS (1/2024) and the SCO (7/2023)

Political commitment to the de-dollarization bloc

The dependency runs both ways, but is asymmetrical:

Iran sells discounted raw commodities.

China sells high-value manufactured goods.

China is the price maker.

Iran is the price taker.

Before the war, Beijing squeezed increasingly larger discounts because Iran had nowhere else to sell.

When the US blockaded Iranian ports on 04/13/2026, the Islamic Revolutionary Guard Corps (IRGC) laid mines and patrolled Hormuz - the country losing 80-90% of its customers was Iran.

But the country losing 1.5 million barrels per day of cheap oil, plus 4-6 million barrels per day of Gulf oil through Hormuz - is China.

That is the truth reshaping everything at the negotiating table this week.

The black oil supply chain

Heavy crude from Kharg Island is too distinctive to be shipped as is - its chemical fingerprint, density, and sulfur profile all betray its Iranian origin.

Therefore, the actual route:

Persian Gulf Star Refinery (PGSR): 360,000 barrels per day, 3 construction phases - $3.4 billion.

The world's largest gas condensate refinery.

Blending crude oil into naphtha - a light hydrocarbon used as a blending component

The shadow fleet carrying both heavy crude and naphtha out of Iran

Ship-to-ship transfers off the coast of Malaysia/Indonesia: blending the two, labeling it 'Malaysia blend'

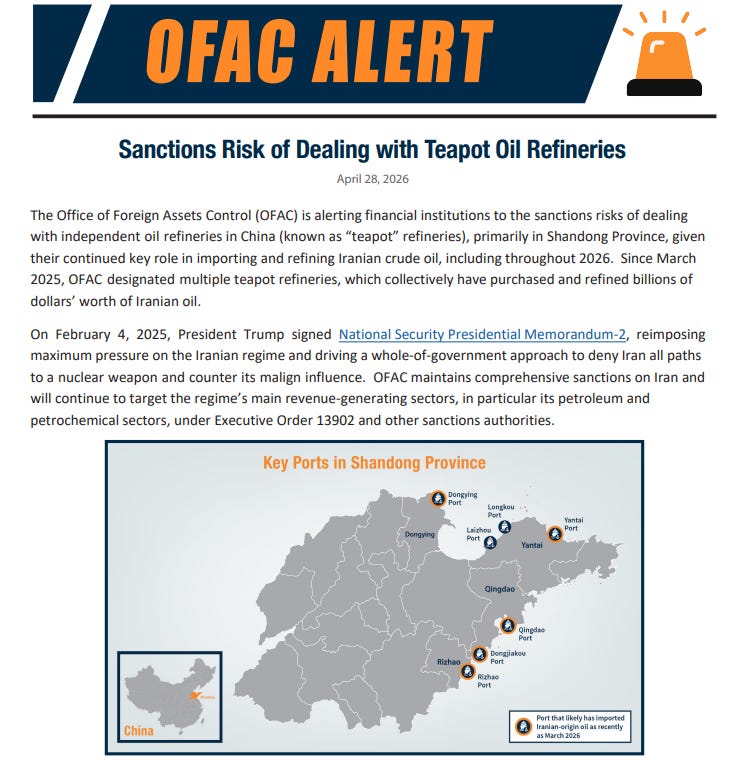

Spoofing AIS signals, ghost ships (scrapped vessels whose IMO numbers still broadcast), forged documents → OFAC issued a clear warning on 04/28

The product reaches Shandong private refineries under the guise of clean crude, free from sanctions

PGSR is 3-4 miles from the IRGC naval headquarters in Bandar Abbas. Khatam al-Anbiya - the IRGC's construction arm - built all three phases.

The output supplies the IRGC fleet and the missile production chain.

Through ~2,500 airstrikes in Operation Epic Fury (US) and Operation Roaring Lion (Israel), the two countries struck Fordow, Natanz, Isfahan, the IRGC naval headquarters, Kharg Island, Iran's entire shadow fleet, and at least 16 underground missile facilities.

But absolutely did not strike PGSR.

The most plausible explanation is coalition politics.

PGSR supplies gasoline to 90 million Iranians.

Striking it crosses the line from military targeting to economic warfare against civilians - a line that Saudi Arabia and the UAE cannot publicly accept.

If the summit fails and the war continues, PGSR could very well make the target list.

The logic: simultaneously destroy Iran's domestic fuel supply and the naphtha blending operations supplying Shandong, sending Beijing an unmistakable signal.

Private refineries - and the rift within Beijing

Shandong's private refineries - the 'teapots' - account for about 25% of China's total refining capacity.

They exist to do what Sinopec, CNPC, and CNOOC cannot: process sanctioned crude from Iran, Russia, and Venezuela. The private sector absorbs the risk so state-owned enterprises can keep their hands clean. Plausible deniability at the state level.

The US Treasury Department's timeline says it all:

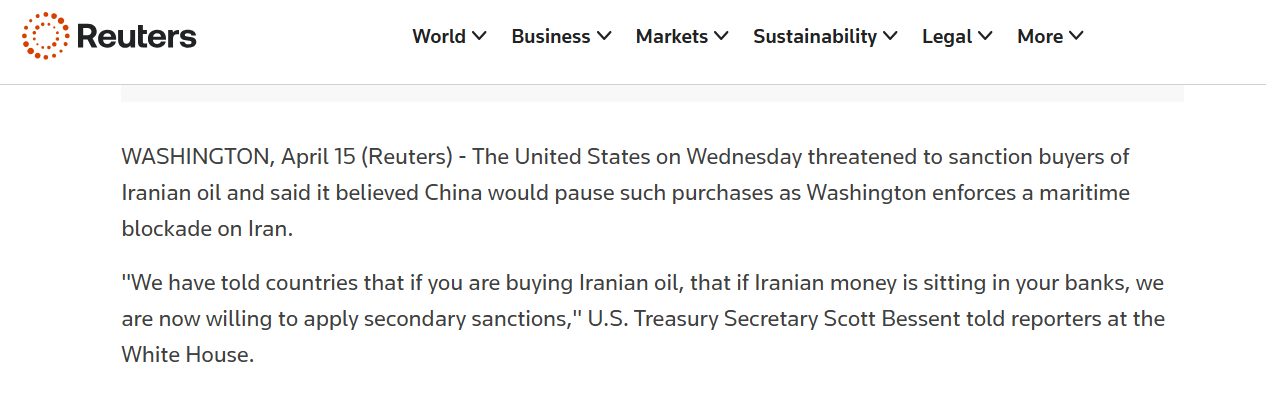

04/15: Secretary Bessent at the White House - 'If you are buying Iranian oil, we are ready to impose secondary sanctions.'

Warning letters sent to two unnamed Chinese banks

04/24: Hengli Petrochemical (~400,000 barrels per day) sanctioned along with ~40 shipping companies. Bessent named it: 'Economic Fury'

04/28: OFAC warned all financial institutions - specifically calling out Shandong province

05/08: Sanctioned two Chinese and two Hong Kong companies for supplying Iranian missile components. Six days before the summit.

Then Beijing made a move that triggered a perfect internal rift:

05/01: National Financial Regulatory Administration quietly issued internal guidance to banks: comply with US sanctions on named refineries

05/02: Ministry of Commerce publicly invoked the blocking statute for the first time in history: counter US sanctions

Private directive: comply. Public order: defy. China's entire stance on Iran compressed into two sentences.

Beijing wants discounted oil.

But Beijing does not want to be cut off from the dollar payment system.

Part II. The Reverse Flow - China Does Not Just Buy Oil

Oil is only half the equation. The other half is what flows back.

Evidence is mounting:

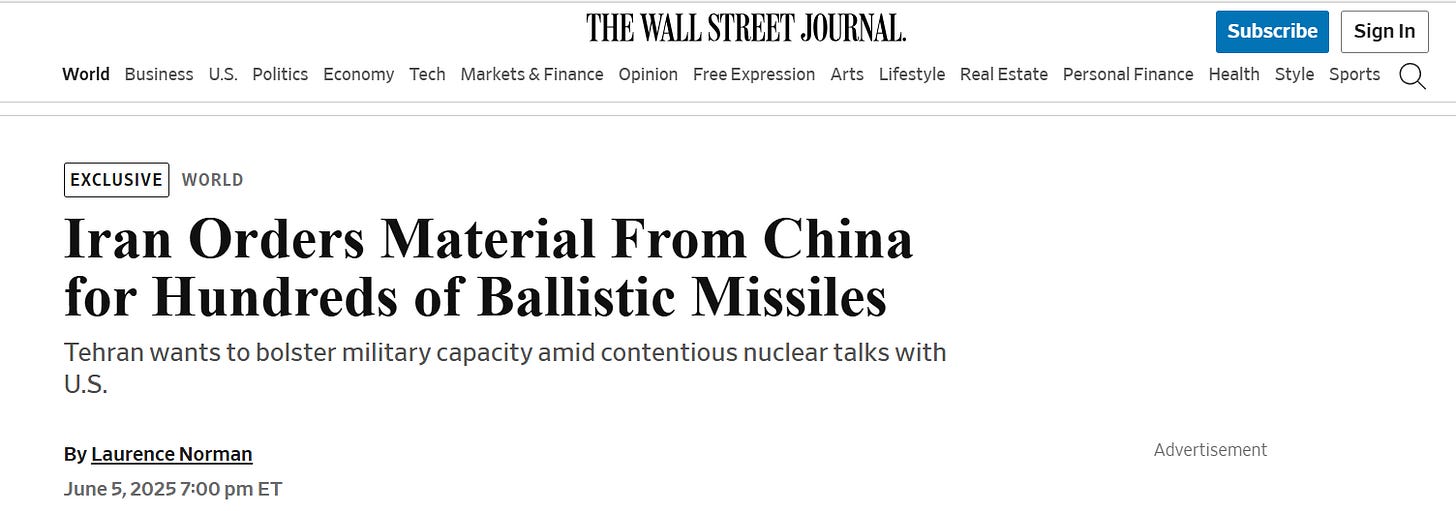

06/2025: Pishgaman Tejarat Rafi Novin Co. (Iran) ordered ammonium perchlorate from Lion Commodities Holdings (Hong Kong) - enough to produce about 800 ballistic missiles.

Early 2025: Two Iranian-flagged vessels (Golbon and Jairan) loaded about 1,000 tons of sodium perchlorate in Taicang, near Shanghai - enough for about 260 short-range missiles.

The Shahid Rajaee port explosion in April 2025 was caused by the IRGC mishandling perchlorate from the same supply chain.

04/2026: US intelligence indicated China was preparing to ship FN-6 man-portable air defense systems to Iran via Pakistan and the China-Pakistan Economic Corridor (CPEC).

The New York Times later confirmed at least one shipment may have arrived.

03/04/2026: A US F-15E Strike Eagle was shot down near Isfahan - almost certainly by a MANPAD. The timing is highly notable.

BeiDou integration: Shahab-3 and Fattah missiles are hitting targets they would have certainly missed five years ago.

According to a consensus among analysts at CSIS and IISS: BeiDou navigation signals (China's satellite navigation system, equivalent to GPS) are being integrated into Iranian missile tail kits.

Trump posted on Truth Social on Aug. 4: threatening a 50% tariff on any country supplying weapons to Iran. He specifically named China.

Public reaction: silence. Actual reaction: the Treasury Department sanctioned two Chinese and two Hong Kong companies on Aug. 5 - six days before the summit. A calculated insult.

China is not a passive buyer. China is an upstream supplier - providing missile chemicals, targeting infrastructure, and anti-aircraft and anti-ship weapons currently aimed at US military personnel in the Persian Gulf.

Part III. Two Straits - Proof of Concept & Application

Hormuz - Proof of Concept

Pre-war: 33-45% of China's crude oil imports passed through Hormuz (4.6-5.8 million barrels per day).

China received 37.7% of the total oil passing through the strait - the most in the world.

The Persian Gulf supplies half of China's oil imports and a third of its liquefied natural gas (LNG).

Malacca - Application

Hu Jintao coined the “Malacca Dilemma” in 2003:

80% of imported oil and about 66% of China's maritime trade pass through a strait that is 2.8 km wide at its narrowest point.

The US operates from Guam, Diego Garcia, Okinawa, the Philippines, and just signed a defense pact with Indonesia in April 2026.

Chee Meng Tan wrote in Foreign Policy (Nov. 5): the Iran war could have greater consequences than a physical blockade.

The US does not need to block a single ship; it only needs to do two things:

The Joint War Committee at Lloyd’s adds destination ports to the high-risk list → war risk premiums surge 10-50 times → pushing China out of the insurance market.

Warn coastal states: facilitating oil bound for China will come with its own price.

=> The price of oil heading to China and insurance premiums will skyrocket to extremely high levels.

The Hormuz equation in this war has proven the mechanism: war risk premiums jumped from 0.25% of hull value to 3-10%.

Commercial operators halted transit due to insurance, even before naval intervention.

CENTCOM intercepted over 70 ships.

20,000 sailors were stranded in the Gulf as of Sept. 5.

Hormuz is the proof of concept. Malacca is the application.

The DFC tollbooth - a permanent architecture

This is the most crucial part that few publications mention:

03/03/2026: Trump's directive → DFC and Chubb announced additional US reinsurance partners and expanded coverage to $20 billion for the maritime reinsurance sector.

03/04: Doubled → $40 billion. Chubb leads. Six US insurers: Travelers, Liberty Mutual, Berkshire Hathaway, AIG, Starr, CNA.

Mechanism: Ships seeking war risk insurance in the Gulf → go through Lloyd’s syndicates → Lloyd’s reinsures through DFC → DFC only approves US-permitted voyages → every application = a complete picture: who owns the ship, who owns the cargo, who finances it.

But there is a harsh reality: insurance does not steer the ship. Crews steer the ship. And no insurance policy in the world can convince 20 sailors to sail through a minefield.

$40 billion worth of insurance has not brought a single ship through Hormuz on a commercial scale.

But the architecture is the key point. The DFC tollbooth is portable.

If the Joint War Committee simply adds Ningbo-Zhoushan, Qingdao, and Yantai to the high-risk destination list, insurance premiums on shipments to China will immediately surge 10-50 times.

Insurance becomes a blockade. No shots fired. No boardings. A legal architecture built on US-controlled financial infrastructure.

China's defense - and why it is not enough

China has a defense line:

Strategic petroleum reserves of about 1.4 billion barrels - the world's largest, enough for 110-180 days of net imports.

Overland pipelines: Myanmar, Kazakhstan (Atasu-Alashankou), Russia (ESPO, Power of Siberia 1, Power of Siberia 2 under negotiation) - totaling about 1.5 million barrels per day.

Russia ramps up 300,000 barrels per day in early 2026 → totaling about 2.1 million. But Ukrainian drone strikes reduced Russia's seaborne oil export volume by 24% in April. ESPO is near maximum capacity. Power of Siberia 2 has not broken ground - 2030 at the earliest.

Simple math: total Russian capacity to China maxes out at about 2.5 million barrels per day under ideal conditions.

China imported 10.5 million barrels per day pre-war.

An insurmountable gap.

But there is a deeper structural issue: crude oil is not usable military fuel.

Without specialized hydrocracking units, it is impossible to produce the JP-5, JP-8, and F-76 consumed by Chinese military aircraft and warships.

Reserves full of unrefined crude oil are just inventory, not capability.

Hydrocracking infrastructure is centralized and easily identifiable.

In a conflict scenario - they become targets.

In a prolonged siege: China has about 4-6 months at maximum consumption before rationing causes political instability. That is the timeframe the Pentagon is studying.

Part IV. US Energy - Oil and Gas Divergence

The UAE left OPEC on Jan. 5. This is not a side note.

59 years of membership.

Capacity of nearly 5 million barrels per day, capped at around 3.6 million under OPEC.

After leaving: the cap disappears.

The trump card: the 370-km Habshan-Fujairah pipeline (ADCOP), completely bypassing Hormuz without crossing a single meter of the strait - capacity of 1.5-1.8 million barrels per day.

Saudi Arabia also has a similar East-West pipeline with a capacity of 3-5 million barrels per day, discharging oil into the Red Sea instead of through the Persian Gulf.

Combined: Gulf producers can export 3.5-5.5 million barrels per day without passing through Hormuz - permanently.

Iran understands this calculus perfectly. That is why they attacked Fujairah on April 5 - not targeting the US Navy, but the infrastructure that allows Gulf oil to flow to the world without Tehran's permission. If oil has a bypass, Hormuz loses its leverage. And the Hormuz leverage is the only thing Iran has left.

The Paradox of Energy Dominance

At first glance, Energy Dominance sounds like a policy to lower gas prices for Americans. Looking closer, it is a market share doctrine: dominating global production and pricing so that no rival can buy the marginal barrel of oil on the market.

Steve predicts: regime change in Iran → WTI below $60 in the future.

But this doctrine contradicts itself: dominating production requires prices high enough for US oil wells to be profitable. Blocking rivals requires prices low enough that they cannot afford to buy.

Those two goals pull in opposite directions - and with oil, there may be no price level that satisfies both simultaneously.

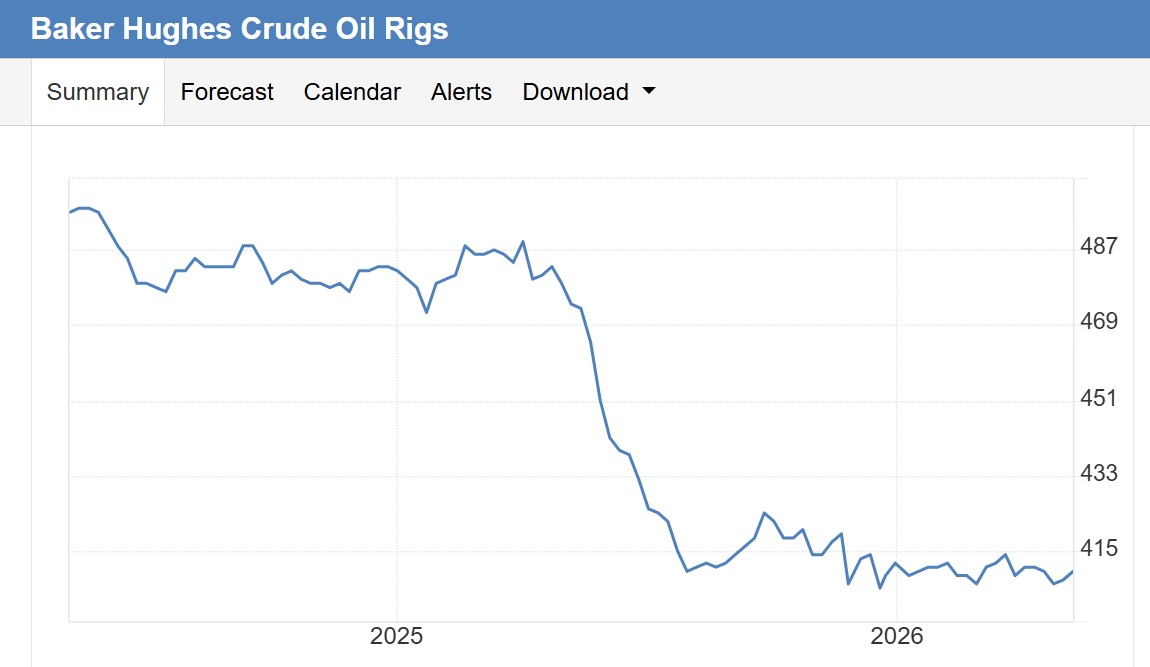

The Baker Hughes rig count is sending a clear signal:

Oil rigs: from nearly 500 → 408, down 20%

Gas rigs: up 21 rigs year-over-year

Steve's logic: if Hormuz opens, the UAE floods the market, OPEC countries follow suit → oil prices collapse → The rational move = pivot to natural gas. Rig count data is confirming exactly that.

With natural gas - the paradox resolves itself

US natural gas has two structural demand drivers that did not exist 5 years ago:

Driver 1 - Europe:

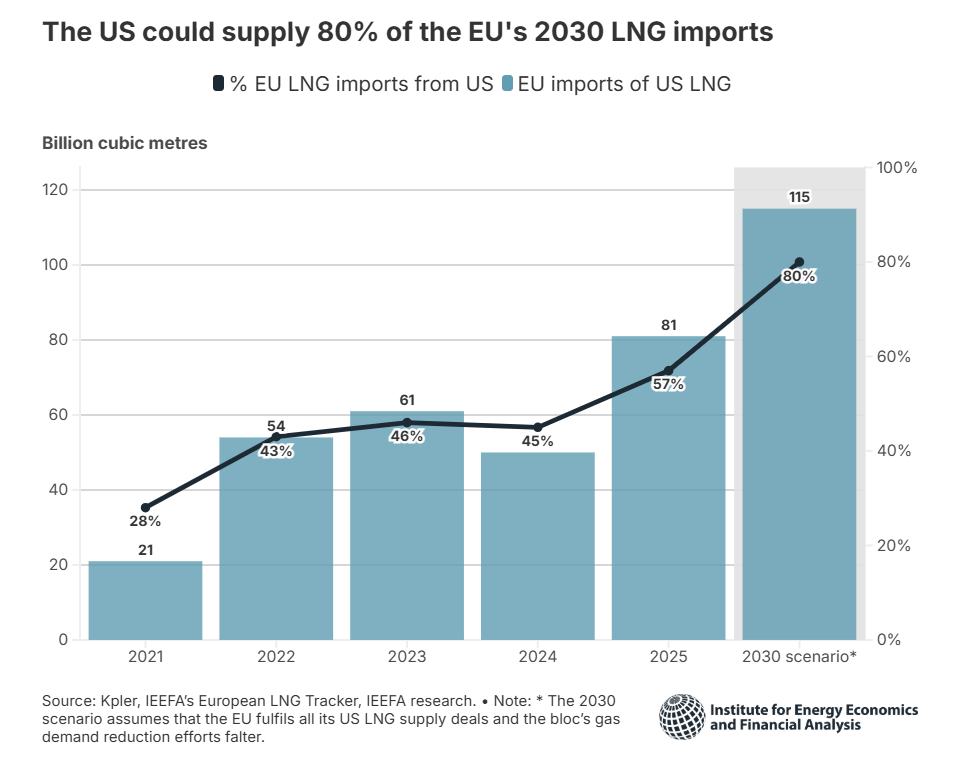

US LNG exports to the EU reached 81-83 billion cubic meters, accounting for about 57% of the EU's LNG imports (compared to 21 billion cubic meters in 2021).

Institute for Energy Economics and Financial Analysis (IEEFA): could reach 80% by 2030.

European wholesale electricity prices are 2-4 times higher than in the US (Eurelectric).

After Russian pipeline gas was cut off in 2022, Europe shifted its energy dependence from Moscow to Washington.

Arms imports from the US: 64% of the total (2020-2024).

NATO targets defense spending of 5% of GDP.

This is the structural consequence of losing a primary energy supplier and replacing it with the very country you are competing against in technology.

Driver 2 - AI data centers:

Electricity demand to rise 17% in 2025 (IEA), expected to double by 2030.

The top five tech companies are spending over $400 billion on data center infrastructure in 2025, with plans to increase by another 75% in 2026.

Natural gas capacity for data centers is set to increase by 71% from 2025 to 2026, while renewable energy will only grow by 2% (American Action Forum). Gas turbine costs have surged 66% in two years, with waitlists extending into the early 2030s.

Antero Resources - a proof point: Q1/2026 adjusted EPS reached $1.72 versus the $1.22 consensus, beating estimates by 41%.

Revenue of $1.95 billion, +44% Y/Y.

Record production of 3.9 billion cubic feet equivalent per day.

CEO Paul Kennedy in the earnings call: "increasing interest from global LNG buyers looking to increase their exposure to US supply."

Neither of those two drivers is going away.

Part V. The Resource Race - Locking Down the Backyard

The Iran campaign does not stand alone. It is a piece of a broader strategy: cutting China off from critical resources across the Americas, the Arctic, and the global mineral supply chain.

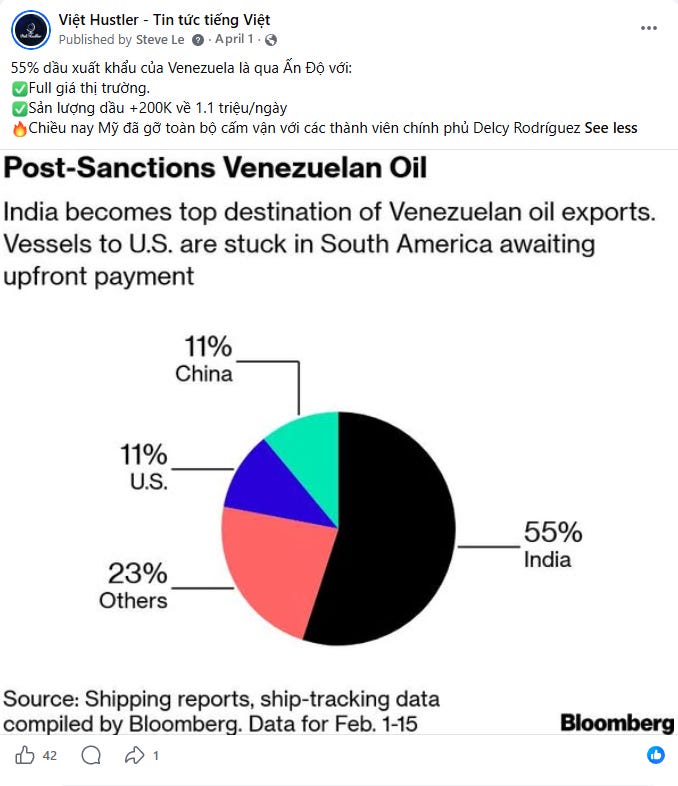

Venezuela

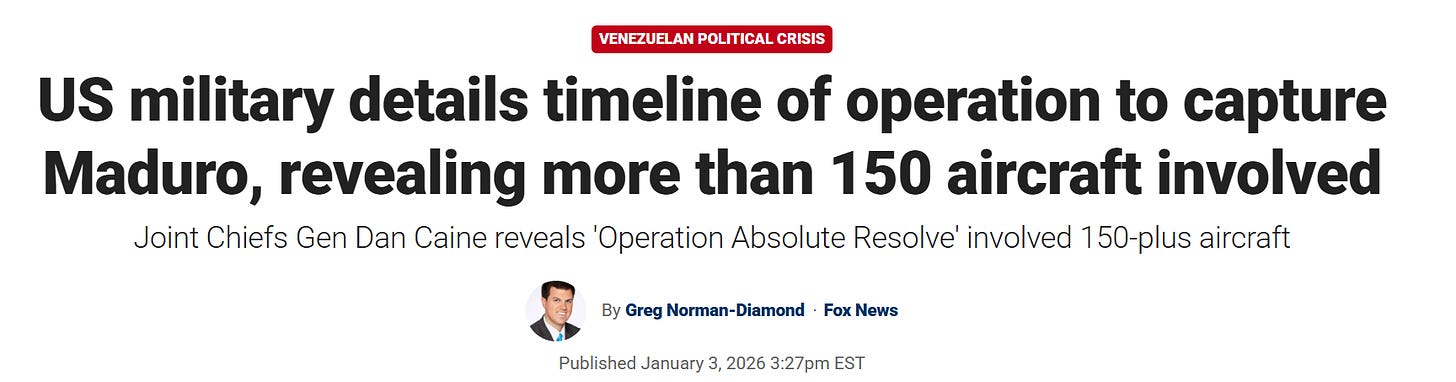

01/03/2026: Operation Absolute Resolve

Maduro was captured in 2 hours and 28 minutes.

Trump invoked the Monroe Doctrine - the 1823 principle asserting that the Americas are a US sphere of influence and no outside power may intervene.

Why does Venezuela matter? Look at the treasure underground: 303 billion barrels of proven reserves (17% of the global total) along with 300,000 tons of rare earths, 408,000 tons of nickel, and 7,000-10,000 tons of gold.

Before the campaign: China was the primary customer, paying in yuan, with Chinese state banks holding over $100 billion in oil-backed loans.

After the campaign: the cash flow stopped. The world's largest oil reserves and a massive rare earth mine are no longer within Beijing's reach.

Greenland

Critical Metals Corp (CRML) closed on 92.5% of the Tanbreez project in southern Greenland (04/39/2026).

European Lithium holds 7.5%.

Submitted a letter of intent to acquire the remaining stake

4.7 billion tons of resources, approximately 27% heavy rare earth oxides - among the highest grades in the world.

To put it in perspective: every F-35 fighter jet contains about 920 pounds of rare earth magnets. No rare earths, no modern fighter jets.

US Export-Import Bank (EXIM Bank): a $120 million letter of interest - the first overseas mining investment under the Trump administration.

Saudi Arabia signed a term sheet for cooperation.

Offtake agreements have been arranged: Ucore 10%, REalloys 15%, Saudi joint venture 25%

05/12: The US is negotiating three military bases in southern Greenland - the same area as the Tanbreez project. A rare earth mine, a new airport, and military bases converging in one place. Not a coincidence.

Pilot plant to launch in May 2026. First ore production: targeted for Q4/2028 - Q1/2029

Breaking the rare earth monopoly

China controls 60-70% of mining, 88-91% of processing and refining, and 94% of permanent magnet production - the type of magnet found in all modern weapons from missiles to radars.

Beijing has used this position as leverage.

April 2025: export controls on 7 medium and heavy rare earths.

October 2025: issued Notice No. 61, mandating that any foreign product containing more than 0.1% Chinese-origin rare earths requires an export license from Beijing - an extraterritorial application mirroring the very technology control rules the US uses to block chips to China.

Currently suspended until November 2026.

The US is counterattacking on multiple fronts simultaneously:

MP Materials: The Department of Defense bought a $400 million stake (July 2025), becoming the largest shareholder.

Committed to a 10-year price floor: $110/kg for NdPr - nearly double the spot price in China (around $60).

The US is paying a strategic premium to ensure non-Chinese supply survives.

USA Rare Earth: $1.6 billion in federal support, acquiring the Serra Verde mine in Brazil for $2.8 billion. DFC financing of $565 million. A 15-year offtake agreement with guaranteed price floors: NdPr at $110, dysprosium at $575, terbium at $2,050.

Project Vault: A $12 billion critical minerals stockpile ($10 billion from EXIM Bank + $1.67 billion private) - modeled after the Strategic Petroleum Reserve, but stockpiling minerals instead of oil.

Chile: Joint statement on March 12, 2026 - Chile produces 23% of the world's copper and holds the largest lithium reserves.

The model is the same everywhere: Venezuela, Greenland, Brazil, Chile.

Secure supply. Lock in price floors. Block rivals' access.

Timeline: supply autonomy could begin in 2028. But until then - every F-35, every Tomahawk, every Apache, every Aegis radar still runs on magnets with neodymium separated in Sichuan.

Part VI. TSMC, Anduril & The Countdown to 2027

Palmer Luckey - founder of Anduril Industries - on the Joe Rogan podcast in October 2025:

"Whatever we are doing, whatever we are investing in, needs to be built on the assumption that around 2027, China will attack or blockade Taiwan."

Anduril: America's 2nd Most Important Private Company

This is not the assessment of an outsider.

Luckey sells weapons to the Pentagon. Anduril has an internal policy called "China 27": every product, every feature, every investment decision runs through a single question - will this be ready before 2027?

If not ready, scrap it.

And it is not just Anduril thinking this way - the Heritage Foundation, the Hudson Institute, and planners in the Pentagon's Joint Staff are all planning based on the same assumption.

What is Anduril building?

The $22 billion IVAS contract - taken over from Microsoft (April 2025). Integrated Visual Augmentation System

EagleEye helmet - in partnership with Meta. Extended reality: real-time battlefield intelligence and drone control

Arsenal-1 in Ohio - manufacturing autonomous systems at industrial automation scale. The name alludes to Roosevelt's "Arsenal of Democracy."

Ford's Willow Run plant during World War II took 3 years to reach maximum capacity, producing one B-24 Liberator every 63 minutes.

Arsenal-1 went from an empty lot to producing Fury combat drones in less than a year.

Series F funding round: around $1.5 billion, valued at $12.5-14 billion

China sanctioned Luckey and Anduril on December 26, 2025, for selling weapons to Taiwan. Luckey: "A Christmas present."

Tech-defense integration

At the peak of the Iran war: SpaceX waived Starlink service fees across Iran, bypassing the IRGC's telecommunications blockade.

This enabled civilian coordination, street-level protest organization, and independent media distribution.

Tehran declared US commercial satellites a "legitimate military target."

Starlink for communications. Tesla manufacturing methods for drones. Meta virtual reality hardware for battlefield awareness.

US commercial technology repurposed for strategic competition - at a pace that China's state-directed innovation model is struggling to match.

The Pentagon has also approached General Motors and Ford about converting automotive assembly lines to military production.

The vulnerability: TSMC

TSMC produces 90% of the world's most advanced logic chips (under 7 nanometers), about 60% of advanced chips overall, and 70% of global foundry revenue. Its top 10 customers represent $14 trillion in market capitalization.

Disruption simulation models are severe:

US: a $2.5 trillion loss in GDP (down 11%) - double the 2008 financial crisis

Global: a $10.6 trillion loss (down 9.6% in first-year GDP) - worse than COVID and 2008

China: a $2.8 trillion loss (down 16%). Secretary Bessent: "economic armageddon"

Arizona Fab 21 Phase 1 is operational - but:

When Taiwanese engineers arrive: yields improve.

When they leave: yields drop.

Phase 2 equipment installation is set for Q3/2026, with 3nm chip mass production targeted for 2027.

Total Arizona investment: expanded to $165 billion.

CoWoS advanced packaging - which Nvidia and Apple rely on - is almost entirely in Taiwan.

US costs are 5-20% higher per wafer.

The loop

Taiwan imports 97% of its energy. Most of it is LNG. Most LNG passes through Hormuz. The island producing 90% of the world's best chips relies on a chokepoint that the IRGC is mining.

Taiwan will expand US LNG imports starting in June.

The circle closes: US natural gas → Taiwanese fabs → semiconductor chips → US weapons systems.

Hormuz disruptions create Taiwanese energy dependence on US exports. The same disruption cutting off Chinese supply anchors Taiwanese chip fabs to US gas.

VII. The Petrodollar - Assuming It's True

Steve has explained extensively why the Petrodollar theory is largely misunderstood:

PETRODOLLARS ARE DEAD, WILL VIETNAM AND ASIA RESCUE THE DOLLAR?

Iran-China oil trade has shifted to yuan settlements via CIPS - China's proprietary payment system, running parallel to SWIFT without touching the dollar.

Iran holds a $7 billion currency swap agreement with the PBOC.

mBridge - a digital currency project led by the Bank for International Settlements (BIS) in Hong Kong, involving China, Thailand, the UAE, and Saudi Arabia - is building a cross-border payment infrastructure entirely independent of the USD.

→ The Petroyuan structure is essentially a sanctions-evasion system.

Can the yuan replace the dollar? No - China still maintains capital controls, and the yuan is not freely convertible, so it cannot become a global reserve currency. But it doesn't need to. It only needs to be a medium of exchange for sanctioned trade - and that is happening.

The Iran war is the first time this entire alternative system - CIPS, yuan swaps, mBridge - is being tested under maximum pressure simultaneously. Whether it holds or breaks is one of the most important financial questions of the decade.

The US response is clear: make anyone using that alternative system pay a heavy price.

The precedent exists: in 2012, the US Treasury sanctioned China's Bank of Kunlun for processing Iranian oil payments, cutting it off from SWIFT.

The model Bessent is building now is an expanded version: any Chinese bank involved in Iranian cash flows risks suffering the same fate.

Read more about the currency war: WHY DID THE UAE ASK FOR A US SWAP LINE?

VIII. Professor Jiang - Who Is The Iran Trap For?

Jiang Xueqin is a familiar name, and one that Steve has criticized quite a bit.

Jiang Xueqin was born in Guangdong in 1976, immigrated to Toronto at age 6, earned a BA in English Literature from Yale in 1999, worked on Chinese education reform throughout the 2000s, and since 2022 has taught philosophy at Moonshot Academy in Beijing. His YouTube channel, Predictive History, has about 2.5 million subscribers. Western media has dubbed him the "Nostradamus of China." He has appeared on Tucker Carlson, Piers Morgan, Breaking Points, and Diary of a CEO.

In May 2024, during a lecture titled "The Iran Trap" (Geopolitical Strategy #8), Jiang predicted:

Trump's reelection in November 2024.

The US becoming increasingly deeply involved in a conflict with Iran over a three-to-four-year timeframe.

He predicted a "Technate," a North American economic fortress built on energy self-sufficiency, control of critical minerals, and technological dominance, designed not to consume the world's resources but to allocate them.

→ The professor was right on the first two predictions. The third is exactly what is unfolding this week in Beijing.

Jiang's parallel is the Athenian expedition to Sicily, 415 to 413 BC. Greece's most powerful city-state launched the largest naval expedition in Greek history against a wealthy and distant target. The expedition was annihilated. This defeat marked the beginning of Athens' permanent decline. Jiang argues that the US military possesses unparalleled hubris and believes it can win any war. Iran wants to provoke a protracted conflict because wars of attrition collapse overextended empires. The petrodollar relies on Saudi participation. Prolonged chaos in the Persian Gulf will ultimately sever the dollar's tether.

Steve has criticized this video multiple times for numerous flaws that time has proven wrong:

Military disparity

The GCC's response

Impact on the US economy

But most importantly in terms of game theory:

Jiang views the Iran war as a trap for the US → in reality, it is a trap being set against China.

The Iran war is a fierce but brief military campaign followed by an indefinite naval and financial blockade.

→ China is exposed as being strategically overextended. It has investment capital, debt traps, and buys oil in far-flung places, but lacks the capability to deploy troops to protect distant national interests.

Jiang's prediction assumes the US will wage the kind of war it used to fight in the past-bogged down, dragging on for decades without clear objectives. On the contrary:

A 12-hour preemptive decapitation strike

5 weeks of high-intensity airstrikes destroying critical targets

Followed by a blockade

→ This is not a war of attrition. This is a war to dismantle a nation's structure from its economy and politics to its military.

Professor Jiang was right about the trap, but wrong about who would fall into it.

"merely surviving" ≠ "winning"

"disrupting trade" ≠ "controlling maritime trade"

"capable of causing danger" ≠ "military threat"

VIDEO: IF THE US DOES NOT STRIKE IRAN AND VENEZUELA

IX. The Summit - Four Issues, One Real Negotiation

The game has changed

Comparing 2025 and 2026:

2025 - The US comes to the table with a weak hand:

China controls 88-91% of rare earth processing

TSMC's monopoly provides implicit leverage for Beijing

The petroyuan is gaining traction. The dollar's share of reserves is falling

Iran sells oil to China with impunity

China holds the Panama Canal ports

China's economy is gradually emerging from deflation

2026 - a different game:

The US takes Panama

The US economy continues to grow, cutting imports from China by 30%

China's economy remains in deflation

Chinese weapons face major questions in Venezuela and Iran

Hormuz is blockaded. China loses 1.5 million barrels/day of Iranian oil and faces restrictions on 4-6 million barrels/day of Gulf oil. The DFC facility turns restrictions into structure

Venezuela's 303 billion barrels of reserves and rare earths fall under US management

Tanbreez, Serra Verde, and Project Vault begin breaking the rare earth monopoly. The timeline: shortened from "someday" to 2028

The UAE leaves OPEC - unlimited production awaits the reopening of Hormuz

US LNG to the EU: 81-83 billion cubic meters, 57% of total imports. Complete energy dependence

Four issues on the negotiating table

1. Trade mechanism (the easiest): China will commit to purchasing 25 million tons of soybeans per year and ordering up to 500 Boeing aircraft.

This is the price of admission for a photo op.

But in 2017, Trump also brought home an $83.7 billion memorandum from Beijing - exceeding the GDP of West Virginia - and not a single penny materialized.

2. Rare earths: China's rare earth export ban (Notice No. 61) is suspended until November 2026 - and is highly likely to be extended.

China holds this card and could trade it for tariff reductions or an easing of the US chip export ban.

Both sides need a truce.

But what China demands in return will reveal its most painful vulnerability.

3. Taiwan (the most sensitive): CFR/CSIS: Beijing wants to shift from 'not supporting' to 'opposing' Taiwan independence. It sounds simple, but it is not.

'Not supporting' is passive. 'Opposing' is active - Taipei would interpret this as the US leaning toward Beijing's stance that Taiwan's political future is not for Taiwan to decide.

Bonnie Glaser (German Marshall Fund): Trading language on Taiwan for concessions on Iran is 'the most destabilizing outcome.'

But according to the logic of this article, this is also the least likely outcome. The entire strategic architecture - the 2027 ticking clock, semiconductor dependence, the rare earth counter-offensive, the DFC - exists because the administration views Taiwan as the endgame.

No one trades the endgame for an opening move.

4. Iran (the real negotiation): Bessent confirmed that Iran dominates the discussions.

US stance: China must force Tehran into a permanent peace - reopening Hormuz, nuclear disarmament, and dismantling the IRGC's offensive capabilities.

Implicit threat: 'Project Freedom Plus' - breaking the Hormuz blockade by force.

Iranian Foreign Minister Araghchi visited Beijing on June 5, with Wang Yi urging Iran to open the Strait.

CSIS explains: China is 'creating the optics of having tried' before the summit begins.

→ Steve's take: The Iran-China relationship also faces major question marks, as Chinese ships cannot freely navigate Hormuz, and statements from Iran indicate a fracture in relations, meaning even if China makes a request, Iran may not necessarily agree.

Media fact-check

The Trump administration claims to have destroyed the majority of Iran's military power: 96% of air defenses, 90% of ballistic missiles, and 78% of naval vessels.

But the US press tells a different story:

Iran still retains about 75% of its mobile launchers and 70% of its missile stockpile.

Iran has restored underground storage facilities, repaired damaged missiles, and assembled new ones.

The CIA also assesses that Iran can withstand the blockade for another 3-4 months.

A notable detail: Mojtaba Khamenei - the Supreme Leader's son and designated successor - has not appeared in public since September 3.

He could be severely injured, or he might not be.

But his prolonged absence suggests the regime is fracturing from within.

The gap between the administration's optimistic narrative and the press's assessment is the actual risk that the market needs to price in.

Arguments from both sides

Xi Jinping is betting on time. The November 2026 midterms will erode Trump's political capital. The 2028 succession is uncertain. China only needs to avoid losing over the next two years. Sit tight. Wait.

Trump is betting on speed. The blockade is tightening. The rare earth counter-offensive is accelerating. The defense tech ecosystem is expanding. The Iranian regime is fracturing. Every month that passes without a deal is a month the US grows stronger and China grows weaker. If Xi fails to deliver Iranian compliance at the summit, the US will escalate.

X. What Is the Market Waiting For?

Trump and Xi have two days to talk.

Topics to watch:

Energy - oil and gas are heading in opposite directions: US drillers are pulling oil rigs and pivoting to natural gas.

LNG companies are benefiting from two new sources of demand: an energy-hungry Europe and AI data centers.

When Hormuz reopens, the UAE will flood the oil market with unlimited production - oil prices could collapse, but natural gas will not.

Rare earths & defense tech: It will be 2-4 years before processing capacity outside China reaches sufficient scale.

In the meantime, every F-35 still relies on magnets from Sichuan.

The counter-offensive is accelerating - but the clock is also ticking.

Maritime insurance architecture: The $40 billion DFC reinsurance facility will outlast any ceasefire.

And it could be applied to Taiwan with just an executive decision.

This is a fundamental shift in how the US controls shipping lanes - using insurance instead of warships.

Semiconductors: The yield gap between TSMC's fabs in Arizona and Taiwan, the concentration of CoWoS packaging, and Taiwan's energy vulnerabilities create an unprecedented risk cluster for the global tech industry.

Currency & interest rates: A 3.8% CPI ties the Fed's hands - it is hard to cut interest rates when inflation remains high. The 10-year yield is at 4.45% and climbing. The petrodollar is gradually eroding; the question is whether the alternative CIPS system can withstand pressure from the US Treasury.

The Iran war is not an isolated conflict. It is a testing ground for an entirely new method of control - the US does not need warships on every shipping lane to dictate who gets to pass and who does not. It only needs to control the insurance system, the payment system, and the sanctions regime - infrastructure the US has already built and is currently operating.

Want to ship oil through Hormuz? You must buy insurance through the US's $40 billion DFC fund.

Want to pay for that oil? You must go through the banking system overseen by the US.

It is an invisible tollbooth - and it will remain there after the bombs stop falling, after the ceasefire is signed, and after the cameras leave. May 14 and 15 will begin to give us the answer: whether Trump's playbook is bold, or reckless.