If you missed the best recent articles:

For investors, the eternal question is always:

How to find a multi-bagger – stock capable of multiplying its value many times?

Familiar principles are often mentioned: p

Must be a disruptive business in the industry…

… Or have diversification across industries

Run by the founder or family themselves.

But all that is just a measure to find a core factor: sustainable profit growth exceeding the market average.

However, hot growth doesn't always create multi-baggers.

Another less noticed path is companies with stable cash flow, solid positions that are hard to replace, but choose to continuously buy back shares.

Mohnish Pabrai - American-Indian entrepreneur, investor and philanthropist, specializing in “value investing”, calls these “Uber Cannibals”.

Suppose there is a business valued at 1 billion USD, corresponding to 10 times free cash flow.

Over 10 years, the company generates the same steady cash flow level.

If it does nothing else, market cap will naturally double after 10 years, because enterprise value (EV) remains at 1 billion USD, plus 1 billion USD in accumulated cash.

The stock will also double.

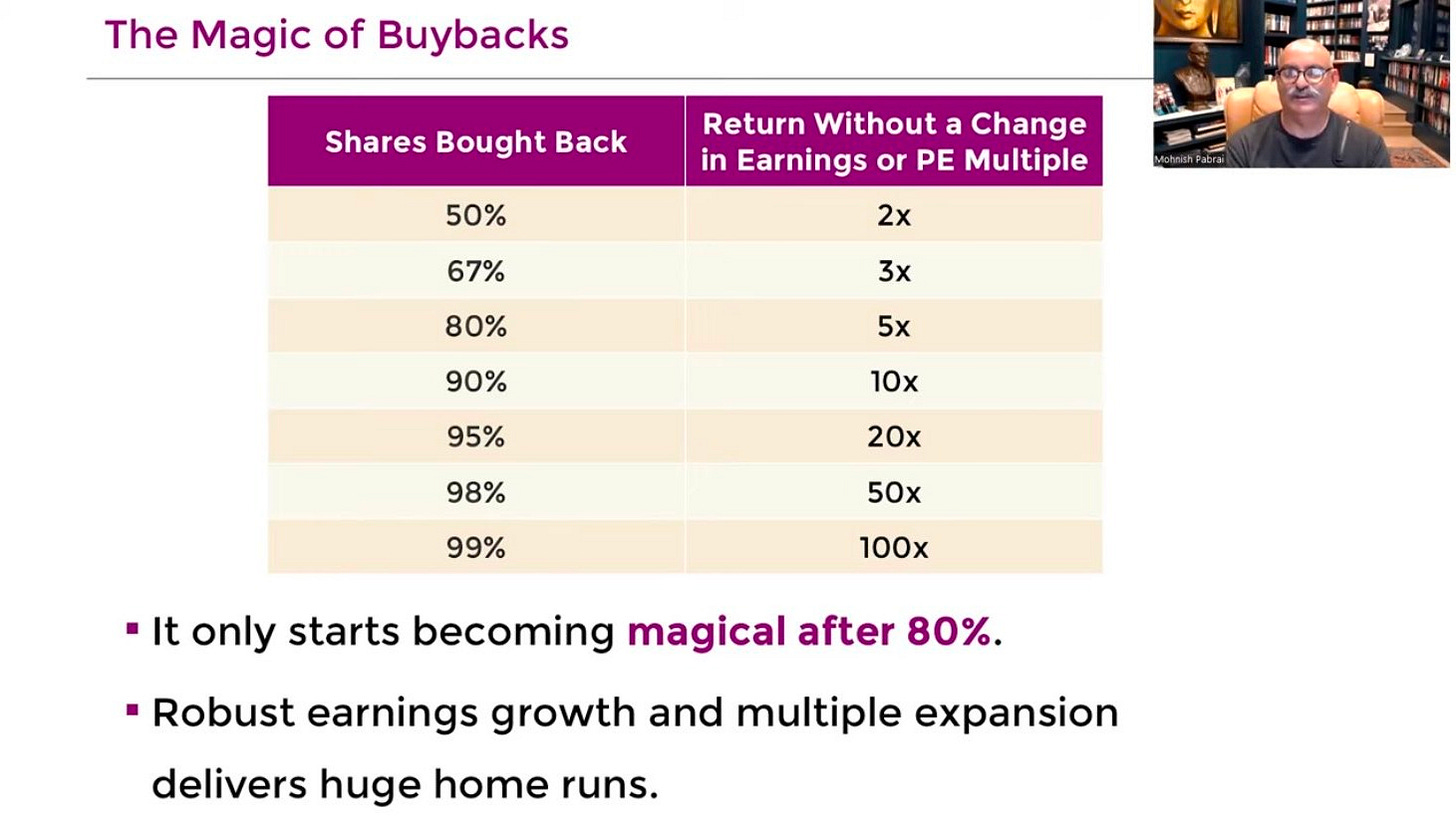

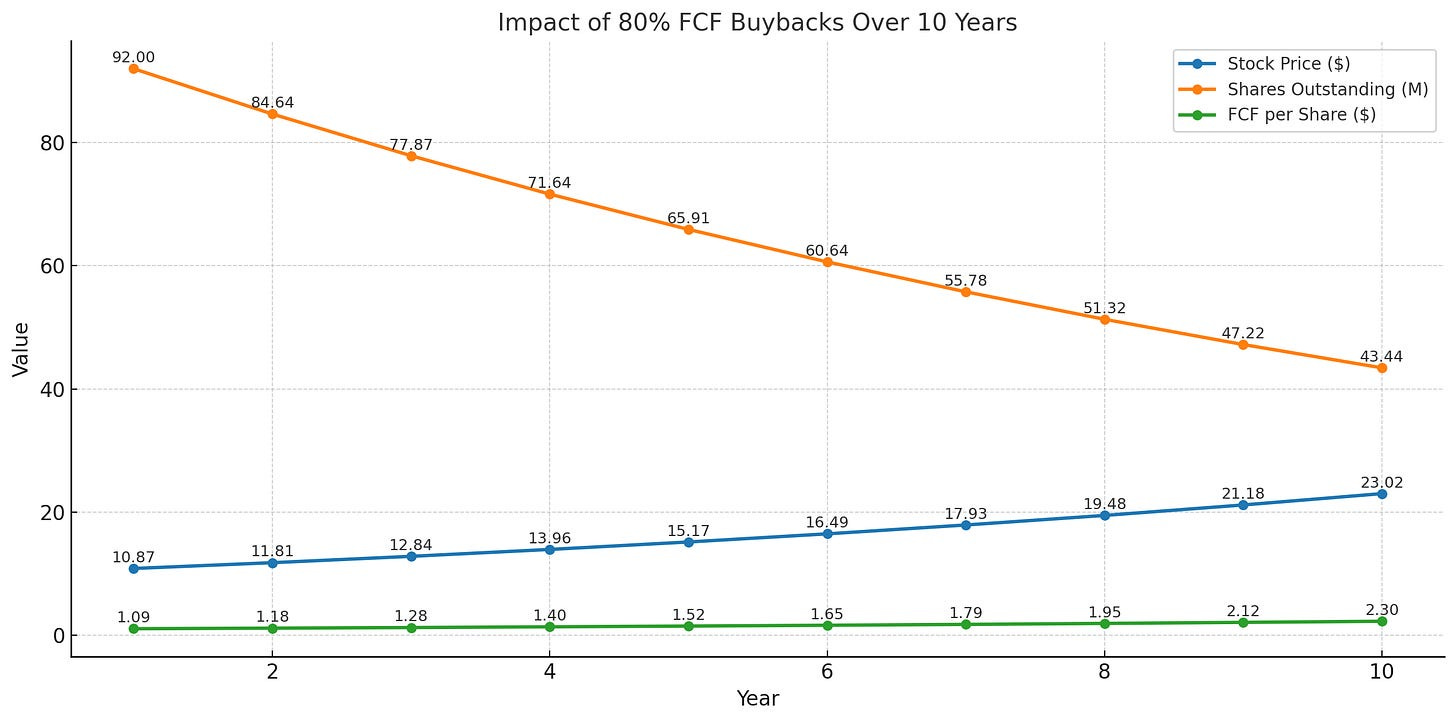

But if the company uses 80% of annual free cash flow (i.e., 80 million USD) to buy back shares?

With 100 million shares outstanding initially (price 10 USD/share), steady buybacks will sharply reduce the number of shares

EPS will rise and the stock price will more than double in the same 10 years

The key point is: very few businesses maintain stable cash flow long-term.

Most are eroded by competition reducing profits, or must reinvest to stay in the game.

However, some companies maintain sustainable positions, even if new growth opportunities are scarce. They are prime candidates to become Uber Cannibals.

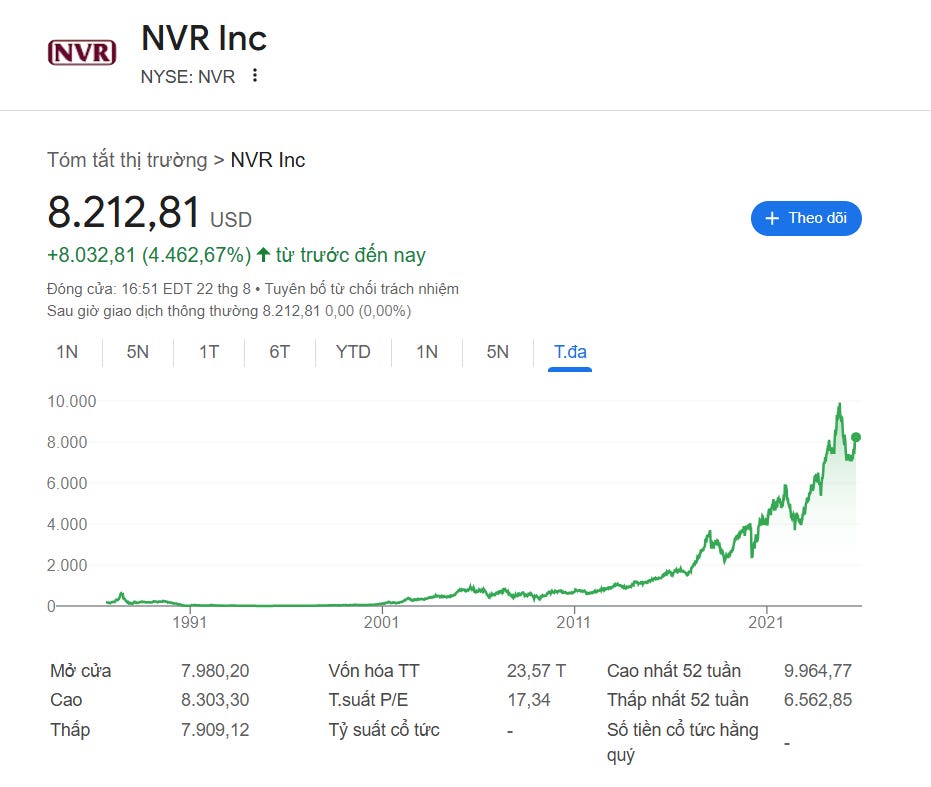

A prime example is NVR – US homebuilding company, with almost no new growth opportunities left. Yet, over the past 30 years, NVR stock has risen 236 times, thanks to the company buying back over 82% of outstanding shares.

Just in the last 5 years, shares outstanding have decreased another 25%.

When this buyback activity pairs with some profit growth, long-term results become superior.

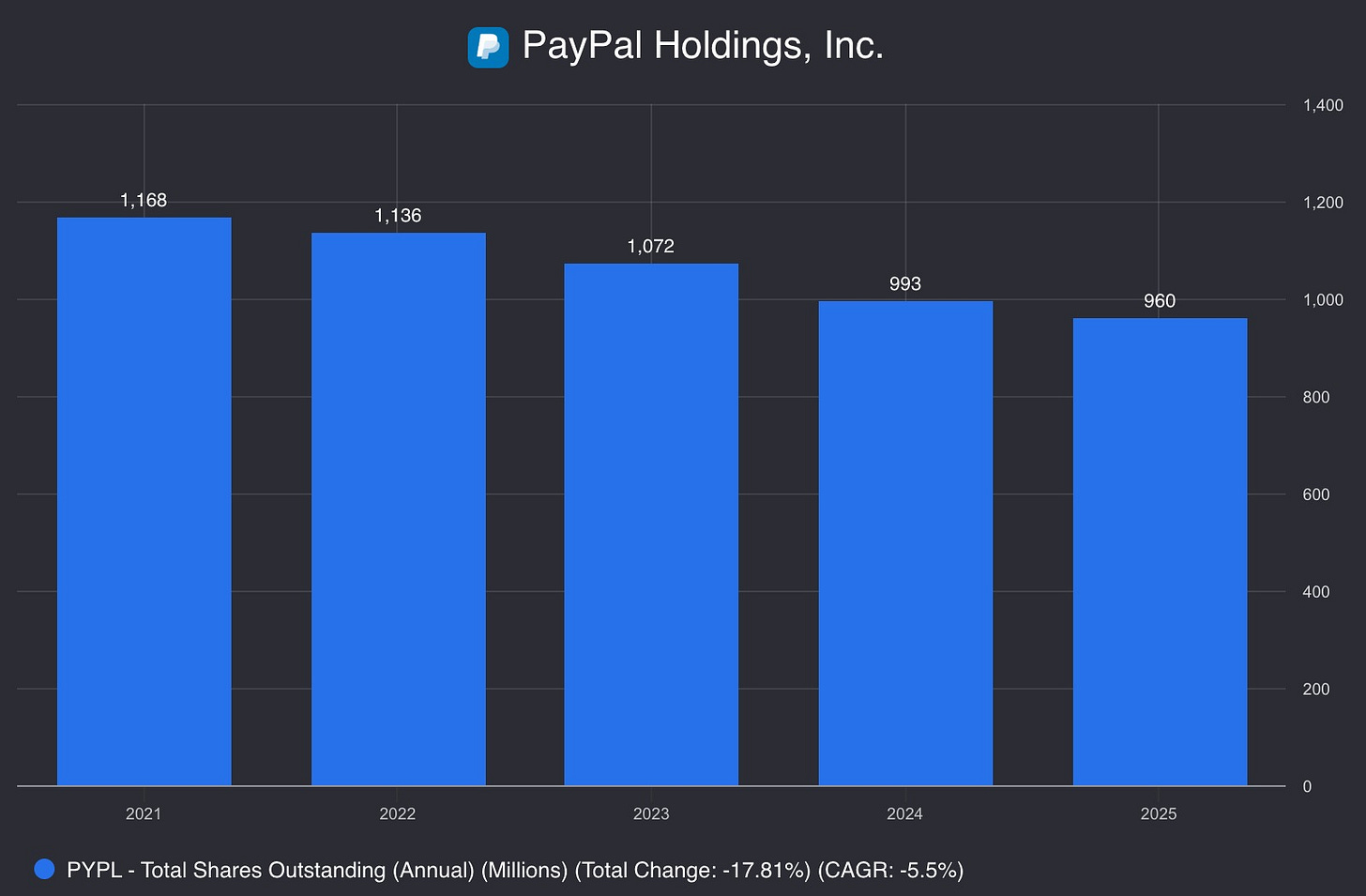

PayPal is on this path.

In the past 4 years, the company has reduced outstanding shares by 18%, while maintaining high single-digit profit growth.

With current P/E <15 valuation, the EPS growth potential from share buybacks is unmissable.

One year ago, Viet Hustler had an analysis on PayPal – where Steve posed the big question of whether the company is stagnating or still has growth potential.

Revenue and profits are still rising, but the stock price has dropped more than 60% over 5 years.

And the risk mentioned at the end of the article has occurred exactly as predicted:

“The key issue with this stock is that investors need to feel confident about PayPal's growth potential to elevate its valuation back to that of a growth stock.”

Investors do not see growth and the stock price has barely moved after 1 year:

The question now is: Is PayPal truly transforming itself into a “Uber Cannibal” – another kind of multi-bagger, no longer relying on explosive speed, but on the durability of cash flow and smart capital allocation strategy?

In today's article, Viet Hustler will join readers in finding the solution to this puzzle.

Overview of the business model

Changes under new leadership

Core of PayPal's business model

Competitive advantages

Business results & financial health

Future prospects

Preliminary valuation