If you missed the best recent articles:

SUNDAY POLITICS: WHAT NEEDS TO BE DONE TO SAVE WESTERN DEMOCRACY? - RAY DALIO

“I used to think that if there was reincarnation, I wanted to come back as the President or the Pope.

But now I would like to come back as the bond market. You can intimidate everybody.”- James Carville, White House advisor during President Clinton, Wall Street Journal, 1993.

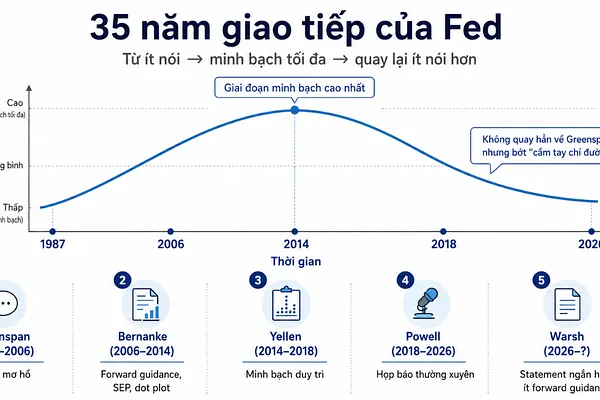

September 2024, Fed pulls a “jumbo” – cuts 50 bps. The whole market breathes a sigh of relief, everyone thinks mortgage will cool down. But looking back at the 30Y FRM chart (Fixed-Rate Mortgage - fixed-rate home loan): the 30-year rate slid gradually from ~7.0% to nearly 6.1% right before September 18, then turned around and rose after that cut, climbing to around 6.8% at the start of November (right when there was another cut) before easing slightly again. Two cuts to FFR (Fed Fund Rate - FED's overnight rate) failed to create a sustainable downtrend. That's the disconnect you're seeing, not an exception.

Why? Because the game now is not in the short-end (FED overnight Rate). Mortgage depends on the long-end of the yield curve: UST 10Y, term premium has turned positive, and MBS basis has widened as QT gradually withdraws the liquidity support. In summary:

Mortgage ≠ Fed Funds.

We are entering a different post-Covid interest rate era: bloated fiscal policy, QRA ramping up long-term issuance, tariffs fueling inflation expectations, and debates around Fed independence causing investors to demand higher risk premiums. The result is the yield curve becoming the noose tightening the housing market; each surge in 20Y/30Y issuance makes the “30-year fixed dream” one notch more expensive.

In today's article, Viethustler will decode:

(1) Cost of capital mechanism: why 30Y fixed sticks tightly to 10Y + two layers of spread.

(2) Decoding the disconnect: Fed cuts but mortgage doesn't fall-what gear is jammed.

(3) Trump 2.0: fiscal, personnel, tariffs, ratings-transmission channels to FRM.

(4) Three 12-month scenarios & quick reversal triggers.

(5) Checklist dashboard: QRA, term premium, MBS OAS, housing, bank stress, breakeven.

The goal is very clear: after reading, you'll have a pricing framework “cheat sheet” to scan the rate sheet, an if–then playbook to react to data, and a base case scenario for decisions. In 2008–2019, a “Fed cut” was enough to dream of a “housing boom”. In the fiscal dominance era, for cheaper mortgages, we need more than one FFR cut.