Articles fully unlocked for free this week:

“Nothing quite lines up perfectly in China, as the exact management of China’s reserves and the non-reserve foreign assets of the PBOC are treated as state secrets.” - Brad Setser, Whitney Shepardson Senior Fellow, Council on Foreign Relations.

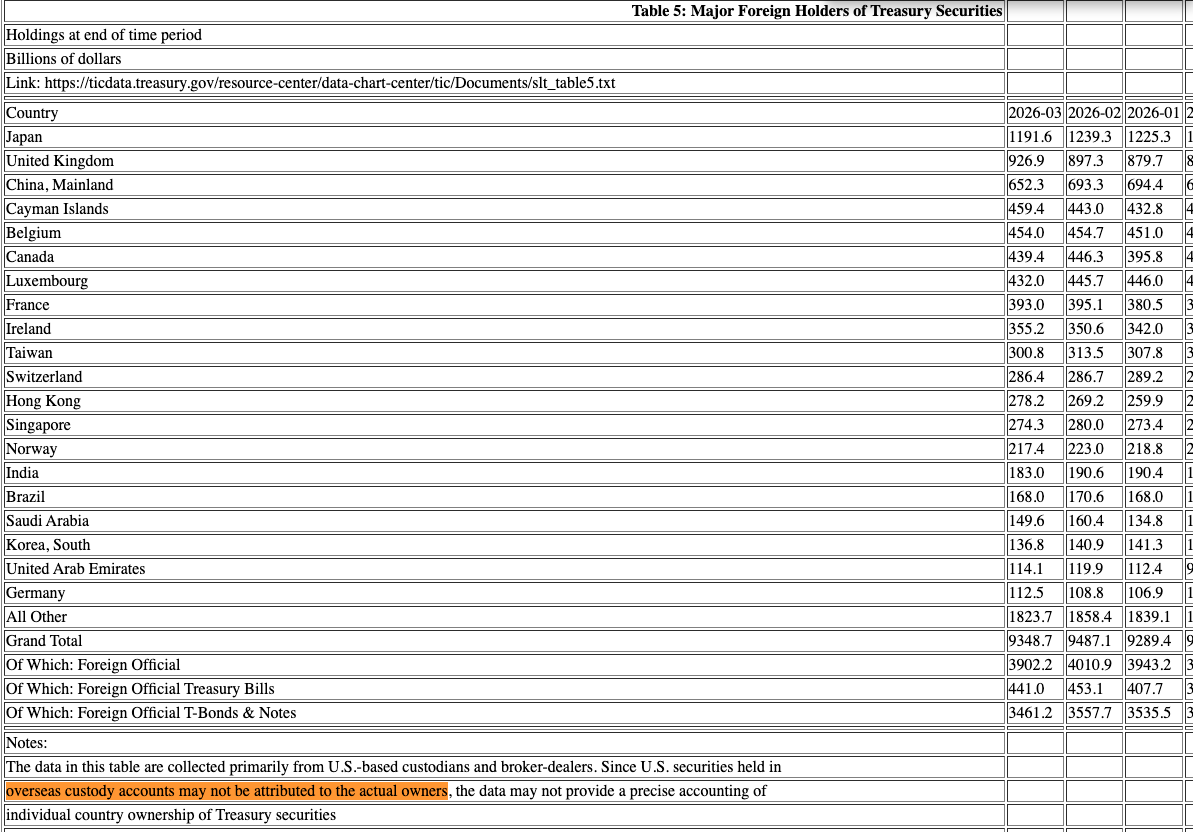

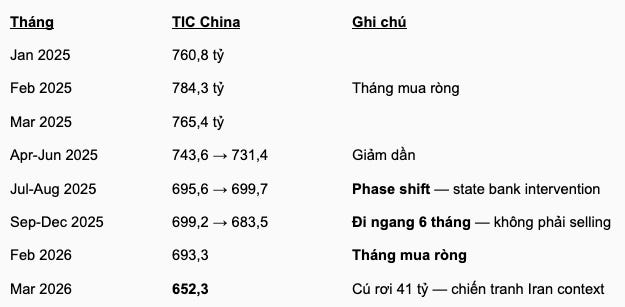

Some figures appear so regularly that the market begins to view them as truth. Each month, when the US Treasury releases TIC data, a small line is pulled from the statistical table and turned into a headline: China holds $652 billion in Treasuries - the lowest level in nearly two decades.

From there, a familiar narrative is constructed.

China is dumping US Treasuries.

China is moving away from the dollar.

China is preparing to use Treasuries as a “financial nuclear weapon.” And if Beijing decides to sell aggressively one day, the US bond market will be shaken.

The story sounds very plausible. It has data, geopolitics, US-China tensions, and the image of a giant creditor withdrawing from its rival's financial system.

But the problem is: the $652 billion figure is not wrong - it is just incomplete.

It measures the portion of Treasuries recorded directly under China's name within the custodial system visible to the US. It does not fully measure assets held through Brussels, Luxembourg, Paris, London, or Toronto. It does not fully capture Agency securities. It does not fully capture the role of state banks. And it certainly does not fully reflect the semi-official vehicles that sit between foreign exchange reserves, state investments, and geoeconomic policy.

In other words, what is disappearing may not be China's USD assets. What is disappearing is the ability to see them in US dataThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

This is the point that makes this week's story much more complex than the “China dumps Treasuries” headline.

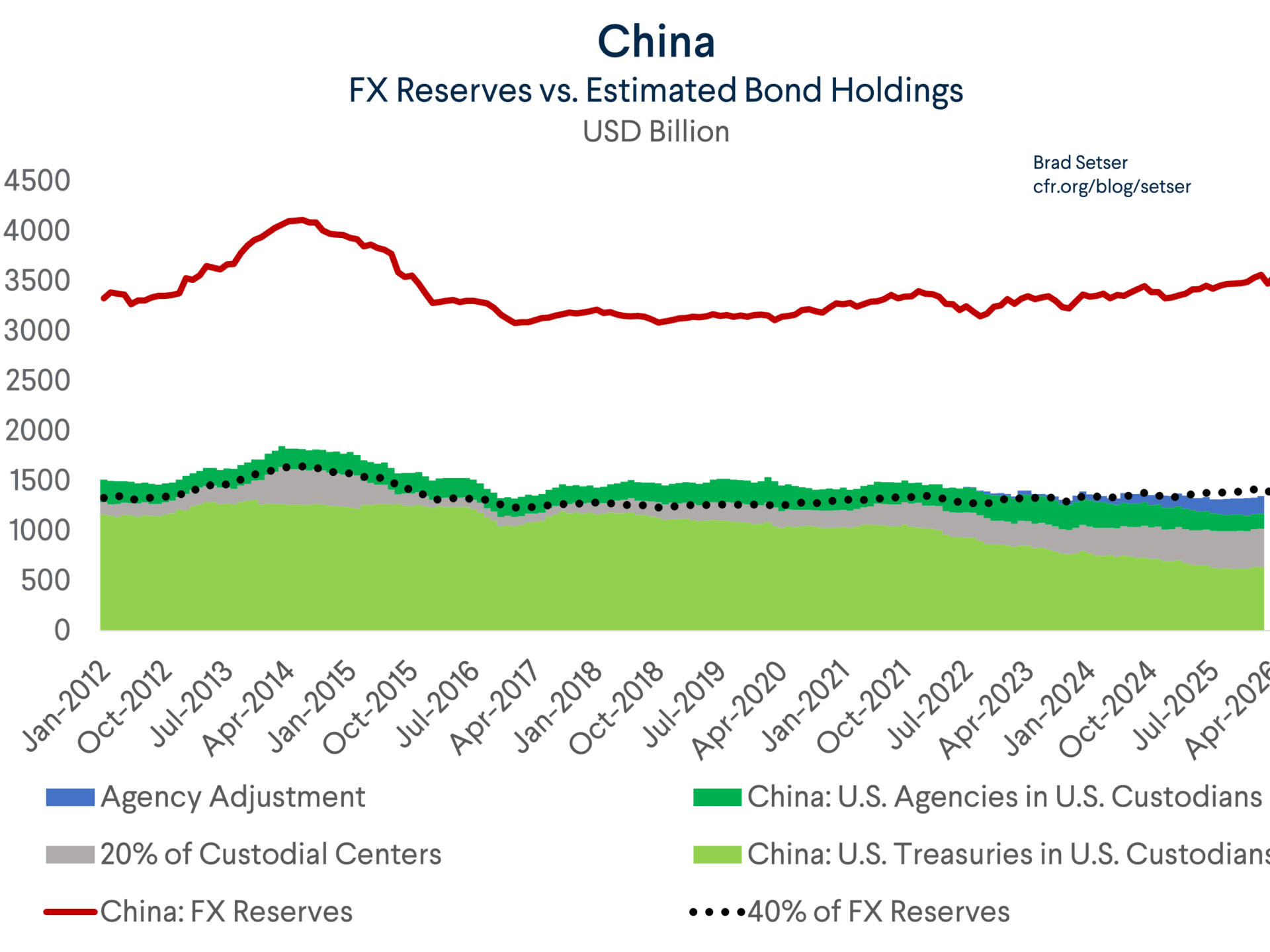

If China were truly abandoning the dollar, we would see a major shift in currency exposure: a sharp decline in USD reserves, with gold, the euro, or RMB assets increasing enough to replace it, and the national balance sheet becoming less dependent on the dollar ecosystem. But the data suggests otherwise: China remains deeply tied to USD assets; it is just that the method of holding them has changed - less visible, shorter-term, more dispersed, and less dependent on US custodians.

This is not de-dollarization in the classical sense.

This is PBOC swap lines are the most significant effort in that direction. In terms of scale, this network is not small. But empirical evidence shows that the market still clearly distinguishes betweenThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

And here lies the paradox: Beijing wants to reduce the risk of being seen by the US, controlled by the US, or in an extreme scenario, having its assets frozen by the US like Russia's were after 2022. But at the same time, China remains locked into the dollar system by its own massive trade surplus. Every year, trillions of dollars worth of goods flow out of China; that surplus must go somewhere. If it doesn't go into long-term Treasuries, it might go into T-bills. If it doesn't sit directly in New York, it might sit through Euroclear, Clearstream, Canada, or state banks. But it cannot simply transform into a fully non-dollar system yet.

Therefore, the right question is not just:

“How many Treasuries does China still hold?”

The crux of the entire article lies in the difference between

“How dependent is China still on USD assets - even if those assets are no longer in places easily visible to US data?”

And the more important question for the market is:

“Does the real risk lie in a dramatic sell-off, or in a quiet retreat from the role of marginal buyer just as the US must issue an additional $1.5–2.0 trillion in new Treasuries each year?”

This week's article covers seven layers of analysis:

Layer I - TIC: what this system measures, and why it does not fully measure the ultimate owner.

Layer II - Belgium and Treasuries: why the $652 billion figure is only the starting point.

Layer III - “Oh, Canada”: why Agency securities might be the piece of the puzzle the market is overlooking.

Layer IV - Institutional Architecture: USD assets are not kept in a single vault.

Layer V - Aggregating the Numbers: separating Treasuries, reserve-related assets, and broader USD exposure.

Layer VI - PBOC swap lines: the ambition to build a parallel liquidity network and its practical limits.

Layer VII - Why a sell-off is impossible: China is a prisoner of its trade surplus and USD balance sheet.

Layer VIII - The Real Risk: not a noisy sell-off, but a quiet reduction in buying.

By the end of the article, the answer will not be as simple as the headline.

China is not selling all its Treasuries. China has not yet abandoned the dollar.

is only the portion of Treasuries directly visible in TIC. The broader picture shows that China remains deeply tied to USD assets - perhaps around restructuring how it holds USD assets so they are harder to see, harder to freeze, and less dependent on the US custody system.

The risk, therefore, does not lie in a “dump Treasuries” button. The risk lies in the fact that the old marginal buyer is gradually stepping off the stage - just when the Treasury stage needs an audience more than ever.

LAYER I - THE TIC SYSTEM: DESIGN AND CORE LIMITATIONS

1.1. What TIC measures - and what it does not

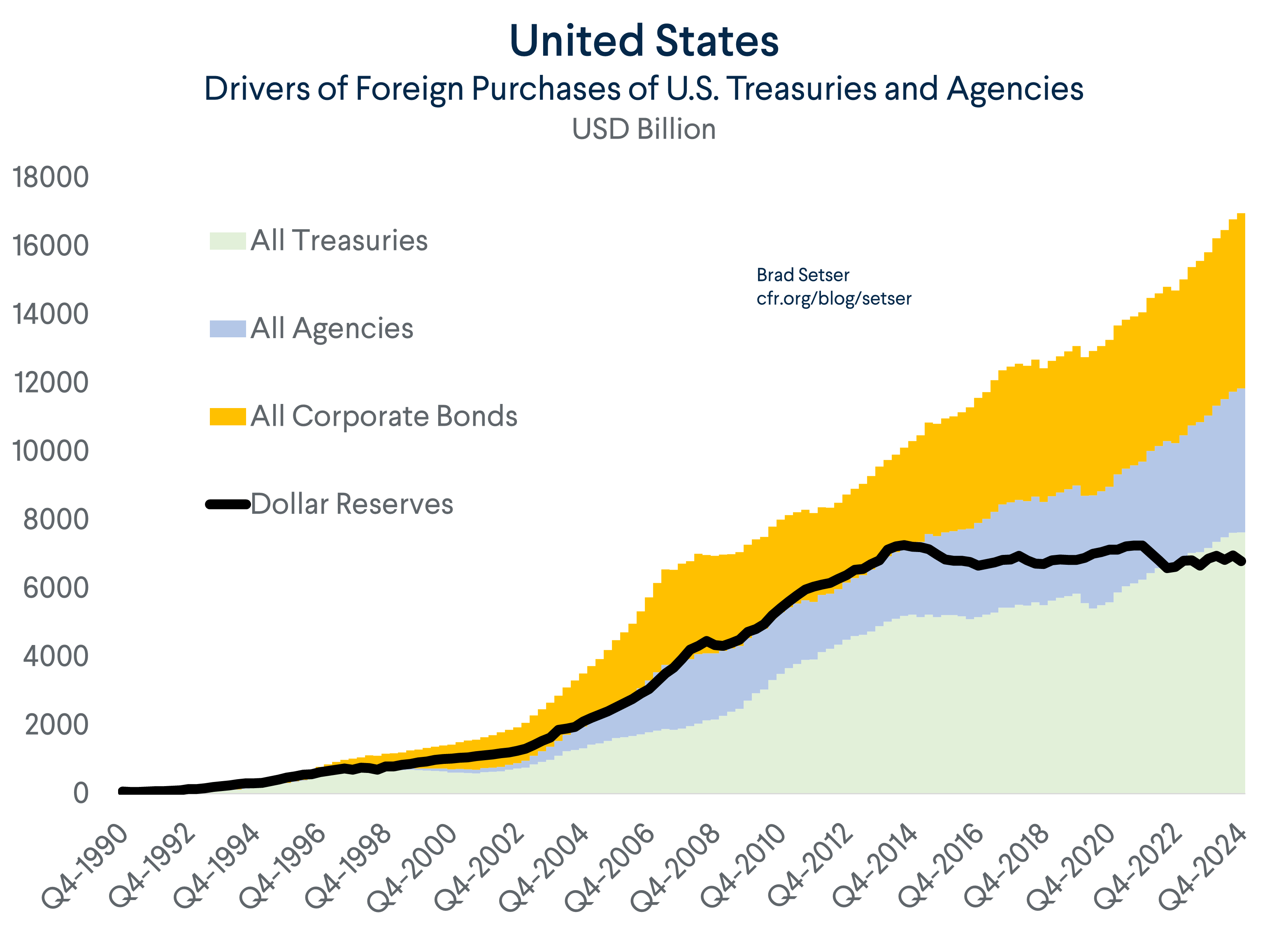

Treasury International Capital System - abbreviated as TIC, or the US Treasury's International Capital Data System - is a monthly reporting mechanism operated by the US Treasury since 1934 to track cross-border capital flows entering and exiting the US financial market.

The core principle of TIC is quite simple: US-based custodians. broker-dealers , and financial institutions must report the amount of US assets they hold on behalf of foreign investors. But the key point is: TIC primarily measures where assets are held - i.e., custodial location - and not necessarily the exact ultimate beneficial owner - i.e., beneficial ownershipThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

In other words, if a country holds Treasuries directly through the US custodial system, that asset may appear under that country's name in TIC data. But if the same amount of Treasuries is held through an intermediary custodian in Belgium, Luxembourg, the UK, France, or Canada, TIC data may record that asset under the name of the intermediary custodial country - even if the ultimate economic owner is a different entity.

This is the core limitation of TIC: it is very useful for tracking where US assets are held, but it is not always sufficient to know exactly who truly owns those assets.

If China buys Treasuries and has the Federal Reserve Bank of New York hold them, that figure appears in the “China” row of the TIC table. But if China buys Treasuries and has Euroclear in Belgium or Clearstream in Luxembourg hold them, that figure appears in the “Belgium” or “Luxembourg” row - even though the actual owner is still China.

The US Treasury does not hide this. In the TIC FAQ section, the Treasury clearly states:

“TIC data are organized by the country of the custodian, not the country of the ultimate holder.”

But that disclaimer is ignored every month when the headlines are written.

1.2. Why SAFE chooses foreign custodians - and the most important reason is February 2022

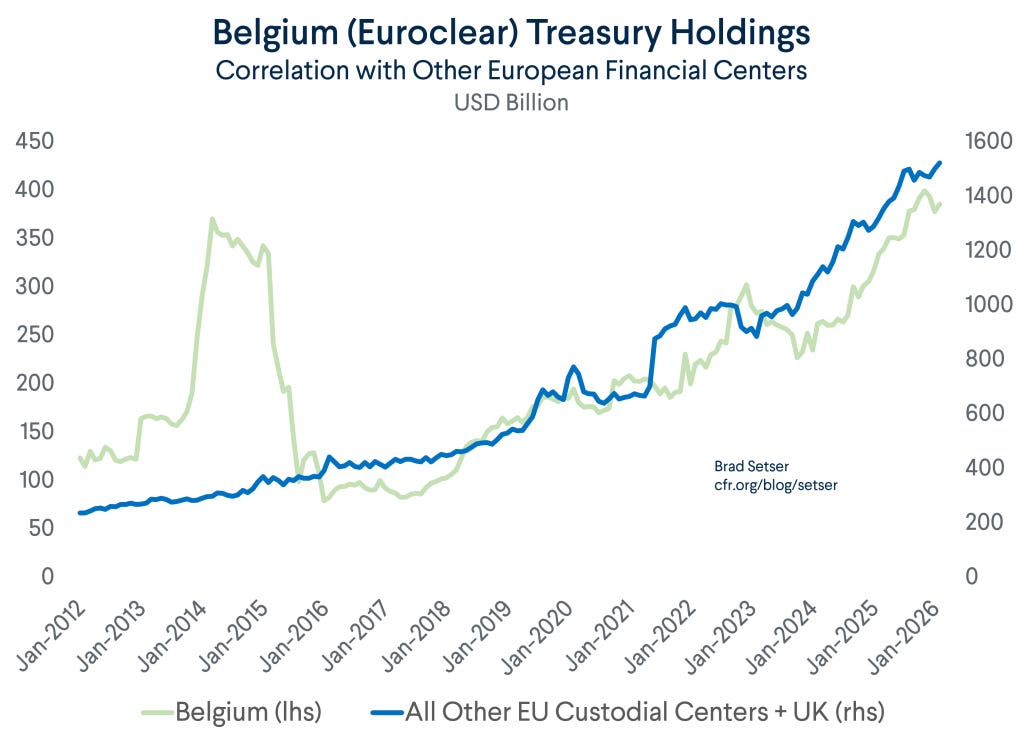

Euroclear in Brussels and Clearstream in Luxembourg are the two largest international securities depositories in the world, handling volumes of transactions reaching tens of trillions of dollars each year.

Major central banks often use these infrastructures because they offer many advantages: assets can be flexibly used as collateral, transactions between multiple asset classes can be netted more efficiently, transaction privacy is higher, and the European time zone is convenient for cross-market reinvestment activities.

Simply put, Euroclear and Clearstream are not just places to “hold” securities. They are a critical part of the global financial plumbing - where assets can be custodied, rotated, pledged, and reinvested more flexibly than by simply sitting directly within the US custody system.

More importantly: SAFE (State Administration of Foreign Exchange) holds a stake in Euroclear. This is direct institutional evidence of the connection.

But on February 26, 2022, that assumption changed completely. When the G7 announced the freezing of approximately $300–350 billion in Russian Central Bank reserves, the market realized one thing: foreign exchange reserve assets are not just subject to price risk, interest rate risk, or liquidity risk. They are also subject to custodial risk - meaning the risk that assets exist on paper, but the owner no longer has full control over their use.

The notable technical point lies with Euroclear. When Russian bonds frozen there mature, the principal and interest payments are not transferred normally to the owners. Instead, the funds are held in non-interest-bearing deposit accounts or are restricted from use. In other words, the assets have not been wiped out, but their economic function - generating liquidity, earning interest, and being reinvested - has been paralyzed.

For China, this is a very concrete lesson. If a central bank's reserves can be frozen through the custodian system, the issue is no longer just what assets to hold, but also where to hold them, through whom, and under which jurisdictionThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

That is why after 2022, diversifying assets across multiple custodians is no longer just a technical choice. It has become a geopolitical risk management strategy.

TIER II - THE REAL MAP: HOW MUCH CHINA ACTUALLY HOLDS AFTER THE BELGIUM ADJUSTMENT

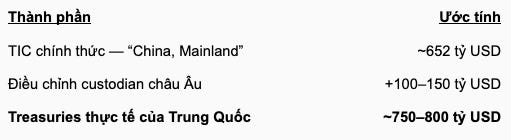

2.1. Why $652 billion is just the starting point

When the media says China holds $652 billion in Treasuries, that figure is not wrong. But it only measures a very narrow portion: the amount of Treasuries recorded directly under the name “China, Mainland” in the U.S. Treasury Department's TIC system.

The problem is that TIC primarily measures place of custody, not fully measuring the ultimate beneficial owner. If China holds Treasuries through New York, those assets appear under the China line. But if the assets are held through Euroclear in Belgium, Clearstream in Luxembourg, or a custodian in Canada, the UK, or France, they may appear under those jurisdictions - even if the ultimate beneficial owner remains China.

Therefore, the right question is not:

How many Treasuries does China still have in the TIC China line?

The crux of the entire article lies in the difference between

How many U.S./USD assets does China still have if we include those held through foreign custodians and other state institutions?

This is why the $652 billion figure is just the starting point, not the final answer.

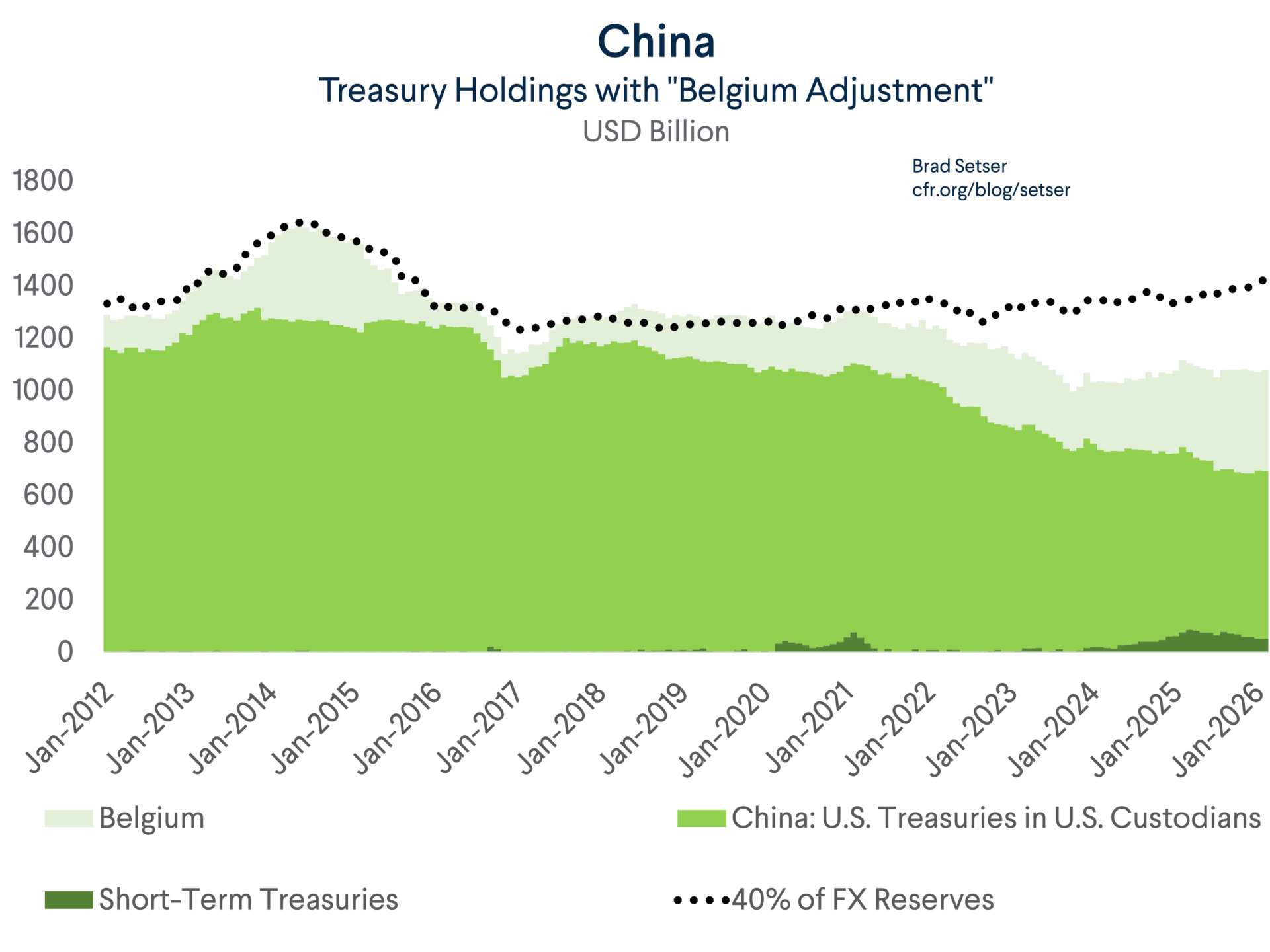

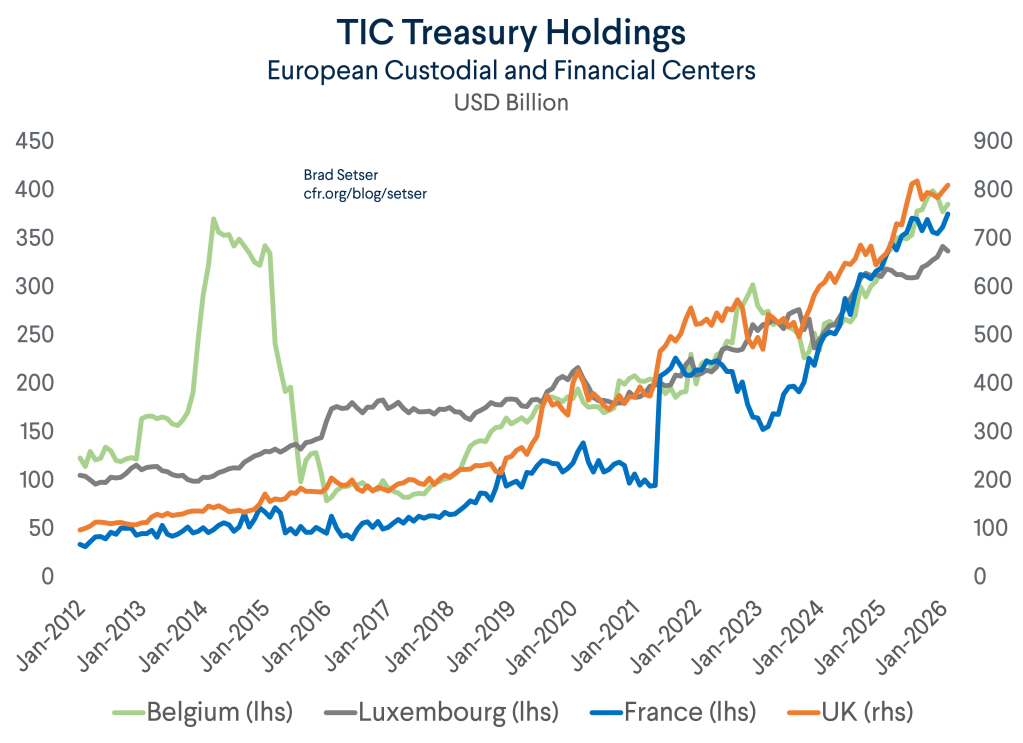

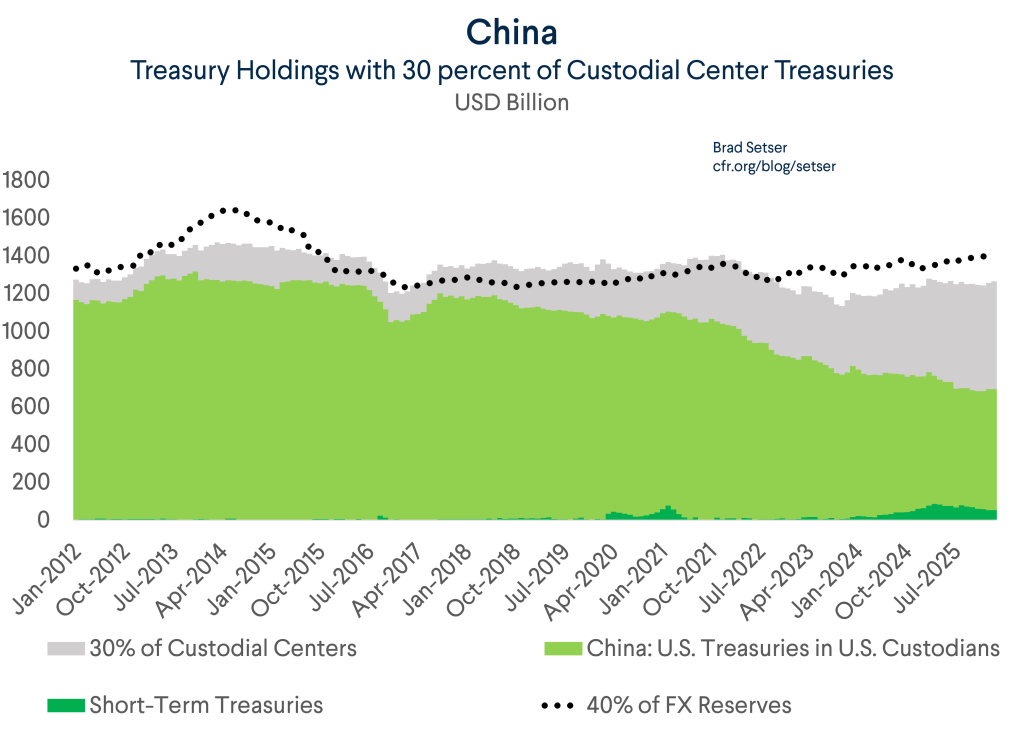

2.2. Actual bond holdings could be near $750–850 billion - Why Belgium was once the best trail

Previously, Belgium/Euroclear was the most important trail to read the Treasuries China held outside of U.S. custodians. During the 2014–2016period, holdings in Belgium moved quite closely with China's reserve fluctuations, especially when Beijing sold assets to support the yuan. Therefore, the “Belgium Adjustment” was once a reasonable way to estimate the portion of China's Treasuries not appearing directly under the T-bills line in TIC.

However, after 2020–2022, looking only at Belgium is no longer sufficient. The lesson from the G7 freezing Russian reserves has given major countries a clear incentive not to concentrate assets at a single custodial point. For China, this means Treasury assets may have been dispersed more widely across various European financial centers.

Data shows that holdings in Belgium, Luxembourg, France, and the UK have all increased sharply in recent years. Meanwhile, Treasuries recorded directly under China's name at U.S. custodians have decreased. This does not prove that the entire increase in Europe belongs to China, but it shows one important thing: the “China” line in TIC is increasingly insufficient to represent China's total Treasury exposure.

A personal conservative estimate is to add approximately $100–150 billion in Treasuries from this group of European custodians to the official TIC figure.

The important point is: China may have reduced its Section 5 - The real risk is not a dump, but a quiet retreat from the role of marginal buyer compared to the 2013 peak. But that does not mean they have abandoned USD assets. A portion of the assets may have shifted to foreign custodians, T-bills, short-term assets, or Agency securities.

The bigger, quieter, and more realistic risk is: China

China may be holding fewer long-term Treasuries, but not necessarily fewer dollars.

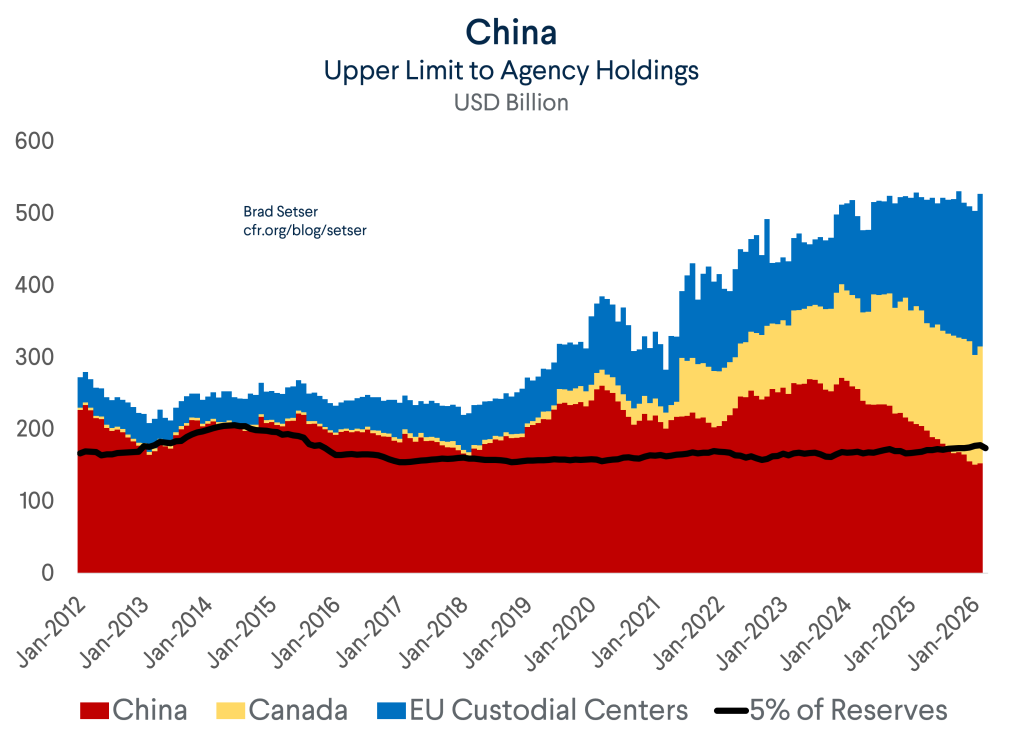

TIER III - “OH, CANADA”: AGENCY SECURITIES AND THE CANADA MYSTERY

3.1. The missing piece: Agency securities

If we only look at Treasuries, we are still missing an important part of the picture.

In the portfolios of major foreign exchange reserve managers, U.S. assets do not just consist of U.S. Treasury bonds. Another important asset class is Agency securities - meaning securities issued or guaranteed by institutions sponsored by the U.S. government, most notably Fannie Mae, Freddie Mac , and other government-sponsored enterprises .

Agencies are attractive because they sit very close to Treasuries on the safety scale: high liquidity, low credit risk, and an implicit U.S. government guarantee, but they often pay a higher yield than Treasuries of the same maturity. Simply put, if Treasuries are the safest zone of the USD system, Agencies are a way to earn a little extra yield without straying too far from that safe zone.

The important point is that the logic of shifting custody locations does not just apply to bonds. If U.S. Treasury bonds can be moved from the U.S. custodial system to Belgium, Luxembourg, France, or the UK, then Agency securities can also travel through a similar pipeline.

The only difference is that in the Treasury story, the prominent trail is Belgium/Euroclear. In the Agency story, the more notable name is Canada.These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

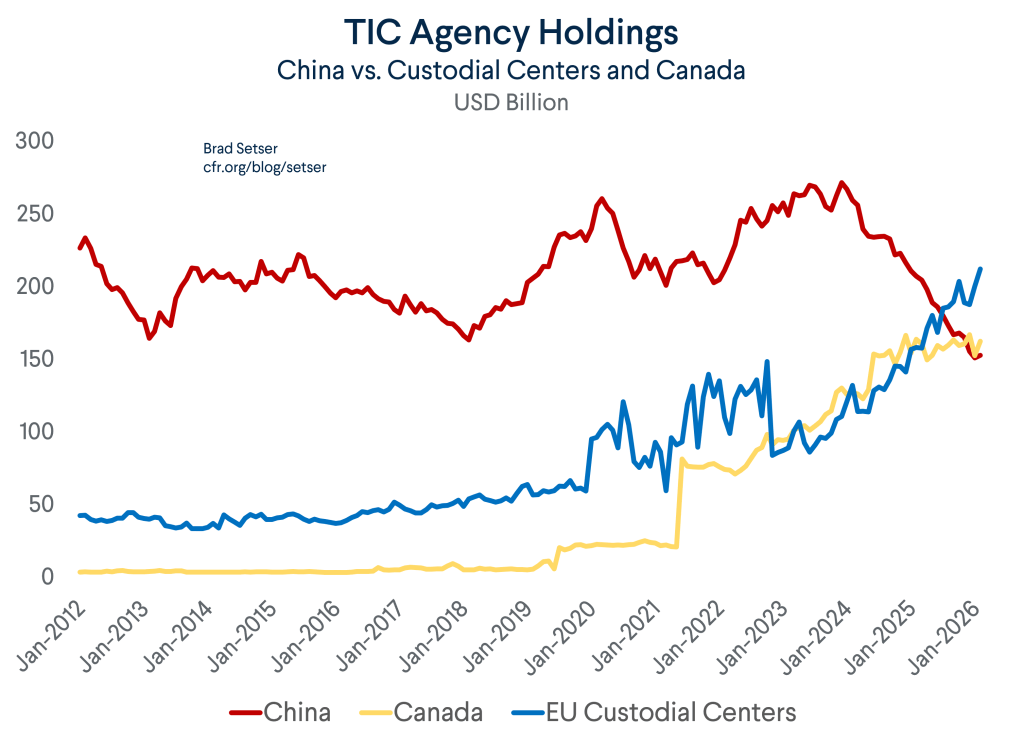

This is why Agency securities are a piece that cannot be ignored. China's Agency holdings in U.S. custodian data once reached over to approximately, then fell to about figure and conclude that China has exited the Agency securities market. after 2022. If we only look at the “China” line, we might conclude that China sold over $100 billion in Agencies.

But that interpretation might be too simple. During the same time that China's direct Agency holdings decreased in U.S. data, holdings in Canada and several European custodial centers increased significantly. This raises an important possibility: some Agencies did not disappear from China's portfolio, but were simply moved to be held through foreign custodians.

In other words, after Belgium in the Treasury story, it is now Canada's turn to become the trail to watch in the Agency story.

If Treasuries show that China may be making USD assets less visible through Europe, then Agencies show that the same logic may be playing out through Canada.

3.2. Canada and the unusual trail

The strangest point in the Agency holdings data lies in Canada.These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

Agency securities state banks $250 billion to approximately $150 billion figure and conclude that China has exited the Agency securities market. This pattern is highly notable. If one only looks at the “China” line, one might conclude that China sold over $100 billion in Agencies. However, when placed alongside Canada and European custodial centers, the picture becomes more complex: the decline in China's holdings almost coincides with the period when holdings in Canada and EU custodial centers surged.

Agency holdings - China versus Canada and EU custodial centers

Is China actually selling Agencies, or is it simply shifting its custody to Canada, Luxembourg, France, and other non-U.S. custodians? If it is indeed a shift in custodians, the TIC data would no longer record those assets under China's name. They would appear under Canada or European custodial centers, even if the ultimate beneficial owner remains a Chinese institution.

In other words, the story in Agencies is very similar to the story in Treasuries:

assets do not necessarily disappear from China's portfolio; they may simply be changing their custodial address. This is why headlines like “China cuts U.S. holdings” can be misleading if one only reads the China line in the TIC data. 3.3. Actual Agency holdings may be much higher

Based on direct TIC data, China's Agency holdings are currently only about

$150 billion figure and conclude that China has exited the Agency securities market.floor , not the full picture.The chart below illustrates the

upper-bound scenario : if we aggregate all Agency securities recorded under the names of China, Canada, and EU custodial centers, total holdings could exceed$500 billion .These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

not the primary benchmark . The reason is that we cannot assume all Agency holdings in Canada and Europe belong to China. A more reasonable interpretation is to view the levelabove $500 billion should only be viewed as a very broad upper bound, used to understand the maximum scale of the issue. upper bound - a maximum limit to visualize the scale of the issue, rather than a central estimate. China - upper bound of Agency holdings

estimated range , rather than an absolute figure.$150 billion figure and conclude that China has exited the Agency securities market. $300–400 billion is a more reasonable range if a significant portion of holdings in Canada and Europe are indeed assets that have undergone a custodian shift. Meanwhile, the level above $500 billion should only be viewed as a very broad upper bound, used to understand the maximum scale of the issue. The important point is not to select an exact number. The important point is:

China's actual Agency holdings are almost certainly far more complex than the China line in the TIC data suggests. If Treasuries can be underestimated because they are held through Belgium, Luxembourg, France, or the UK, then Agencies can also be underestimated because they are held through Canada and EU custodial centers. This is why one cannot simply look at the

$150 billion figure and conclude that China has exited the Agency securities market. 3.4. Conclusion: Don't just look at Treasuries

$150 billion is the visible portion. $300–400 billion may be closer to the actual picture. Above $500 billion is an upper bound that should be read with caution.

If one only looks at Treasuries, one will miss a large part of China's USD asset map. Agencies show that the story is actually much more complex: China may be reducing long-term Treasuries directly in U.S. data, but it still maintains exposure to U.S. assets through Agencies, T-bills, short-term deposits, and foreign custodians.

Therefore, the correct narrative is not:

China is dumping U.S. assets.

But rather:

China is restructuring how it holds USD assets - making them less visible, more dispersed, and harder to read in U.S. data.

This is why Agency securities are an indispensable piece of the entire “China dumping Treasuries” story.

TIER IV - INSTITUTIONAL ARCHITECTURE: USD ASSETS ARE NOT IN A SINGLE VAULT

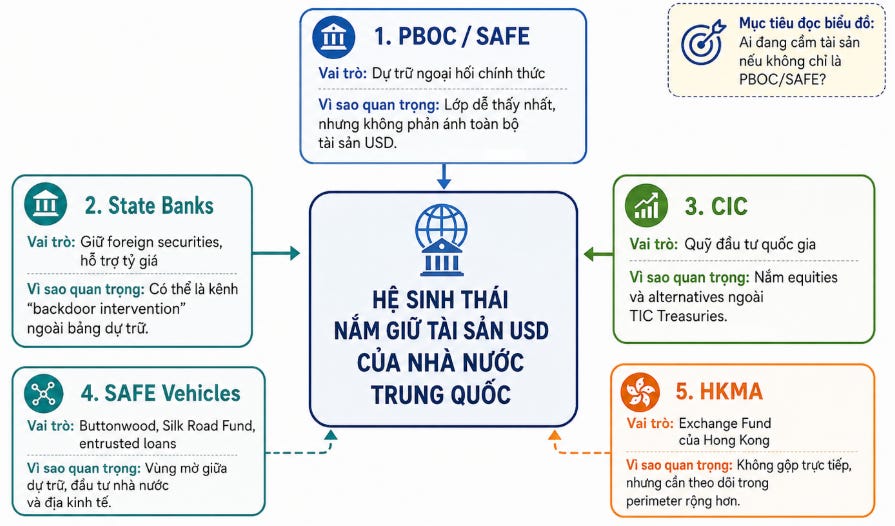

4.1 Not just the PBOC: USD assets reside in an entire ecosystem

To understand the extent to which China is still tied to U.S. assets, one cannot just look at the

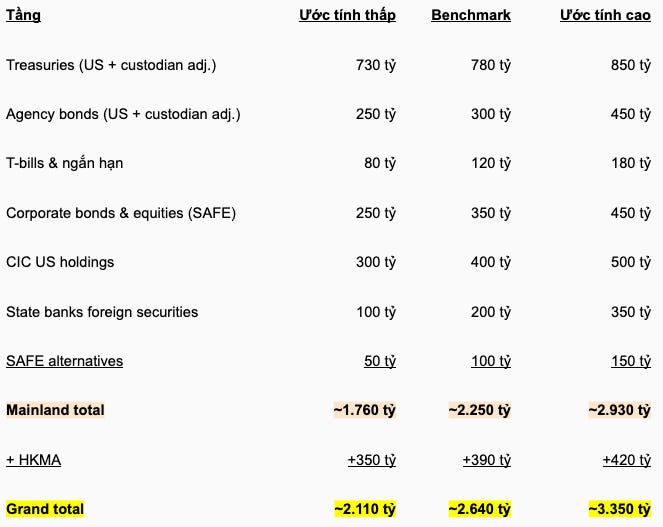

PBOC or SAFE . China's USD assets are not in a single vault. They are dispersed across many layers of institutions within the state financial ecosystem.Tier 1 - PBOC/SAFE: official reserves

Official foreign exchange reserves:

$3,410 billion (April 2026). If the dollar share is around 55% - a figure consistent with estimates from independent economists - then the USD asset portion in official reserves is approximately $1,870 billion. Key point: this 55% ratio does not indicate a clear move away from the dollar. Although China stopped publishing its reserve currency structure in 2020, independent estimates continue to suggest that the USD accounts for a share close to the global average (approximately 57–59% according to IMF COFER Q3 2025).

Tier 2 - State banks: the most important but least visible layer

This is the layer that the market is underestimating the most.

The state-owned banking group - including the Big Four (ICBC, Bank of China, China Construction Bank, Agricultural Bank) and policy banks such as the China Development Bank and Export-Import Bank - holds approximately

$400 billion in foreign securities December 2025 More importantly, there is the speed of change. In December 2025 alone, the net foreign assets of state banks increased by

$110 billion $120 billion China - CNY/USD exchange rate and USD settlement

This is a form of

“backdoor intervention”

- that is, exchange rate intervention through the back door. Instead of letting the PBOC directly buy USD and increase official foreign exchange reserves, the state-owned banks

can step in to absorb that USD and hold it on their own balance sheets. The result is that the policy objective is still achieved - reducing upward pressure on the CNY - but this asset flow does not appear clearly on the PBOC's balance sheet. And because those assets do not pass through the PBOC's official custody system, they do not necessarily appear in the “China”

line of the TIC data. In other words: T-bills Tier 3 - CIC: sovereign wealth fund CIC has total assets of

$1.57 trillion

(net assets of $1.37 trillion, according to the 2024 Annual Report published in December 2025), with a 2024 net profit of $140.64 billion - up 30.4%. This is a large sovereign wealth fund, not foreign exchange reserves in the narrow sense, but its roots are tied to China's process of reinvesting its foreign exchange surplus. Source: https://www.china-inv.cn/chinainven/Media/2025-12/1002912.shtml In the portfolio

of CIC, approximately 59% is allocated to US assets. If we use the size of CIC's international portfolio as a basis, a conservative estimate suggests that CIC may hold approximately $350–400 billion in US assets, primarily through listed equities, private equity, infrastructure, alternatives, and a portion of fixed income . The key point is: this portion almost completely disappears if we only look at Treasury flows in TIC. TIC may show that China is reducing its holdings of US Treasuries, but it does not fully capture the US assets held throughThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

, particularly investments in equities and alternatives. In other words, if the only question is “How many Treasuries does China still have?”, CIC is not very important. But if the question is “To what extent is China's state financial ecosystem still tied to US assets?”, then CIC is a piece of the puzzle that cannot be ignored.These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

SAFE has its own investment vehicles (Buttonwood Investment Company, entities related to the Silk Road Fund) along with foreign currency entrusted loans to domestic financial institutions. Under IMF standards, these entrusted loans are not counted as official reserves, but they are still foreign currency assets coordinated by the state system.

HKMA alone has a scale of approximately $490 billion, with more than 80% in dollar assets - roughly $390 billion. TIC counts this as separate from Hong Kong, not the mainland. But in terms of the strategic financial perimeter, this is a layer that needs to be monitored within the broader picture.

Aggregate estimate

The TIC figure often cited ($652 billion) is less than one-third of the benchmark estimate. And the central conclusion - confirmed by the CFR analysis in May 2026 when fully adjusted - is:

China's total US financial holdings still fluctuate around 50–55% of its reserve portfolio

, with no clear downward trend. Conclusion of this tier: de-visible-dollarization, not de-dollarizationThis is where most commentary confuses two very different concepts:

Currency exposure

- the proportion of dollar assets in the total portfolio

What is declining most clearly is not necessarily - the proportion of assets held at US custodians and observable in TIC

, but rather the portion of USD assets held in U.S.-observable custody channels. Assets can move from New York to Brussels, Luxembourg, Paris, London, Toronto, or Hong Kong. They can shift from long-term Treasuries to T-bills, Agencies, deposits, or the balance sheets of state banks. place of custody

has changed. That is exactly what China is doing on a national scale: maintaining dollar exposure, reducing US custodian exposure, shifting from long-term Treasuries to T-bills and Agencies, dispersing custody across Brussels, Luxembourg, Paris, London, Toronto - and using Hong Kong as a liquidity buffer before it finds its way to international financial assets. This is not monetary rebellion. This is

Among the institutional layers above,

state banks

are the most notable tier. , PBOC/SAFE

is the most visible place, but also the most heavily scrutinized. If official foreign exchange reserves rise sharply, the market will immediately ask: Is Beijing intervening in the exchange rate? Is the newly purchased USD being reinvested in Treasuries? And is this proof that China is still keeping the CNY weaker than the market level? “China, Mainland” state banks

- institutions that are less visible, but still within Beijing's policy orbit. , ICBC, Bank of China, China Construction Bank, Agricultural Bank of China

, along with policy banks such as China Development Bankand Export-Import Bank of China dollar liquidity It is noteworthy that state banks are estimated to hold approximately$400 billion in foreign securities

. In the month of December 2025alone, the net foreign assets of this group increased by approximately $110 billion; if forwards are included, the figure could reach $120 billionin a single month. This is too large a scale to be considered normal banking activity. But China reports a - A proxy for intervention based on forward-adjusted FX settlement shows that in late 2025–early 2026, China's banking system purchased a very large amount of foreign exchange, even though the PBOC's official reserves did not increase correspondingly. This reinforces the argument that USD is being absorbed through state banks, not necessarily appearing directly on the PBOC's balance sheet.

backdoor exchange rate intervention

. The intervention has not disappeared; it has just moved away from where the market is used to looking. The USD is still in China's state financial system, but it does not necessarily appear clearly on the PBOC's balance sheet or in the “China”flow of TIC. T-bills The PBOC does not need to hold all the dollars itself. As long as state banks hold them instead, the policy goal can still be achieved.

The bigger, quieter, and more realistic risk is: China

easily readable balance sheet of the PBOC

to the less readable balance sheet of the state banks . 4.3. BOP as a system for “blurring” capital flowsThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

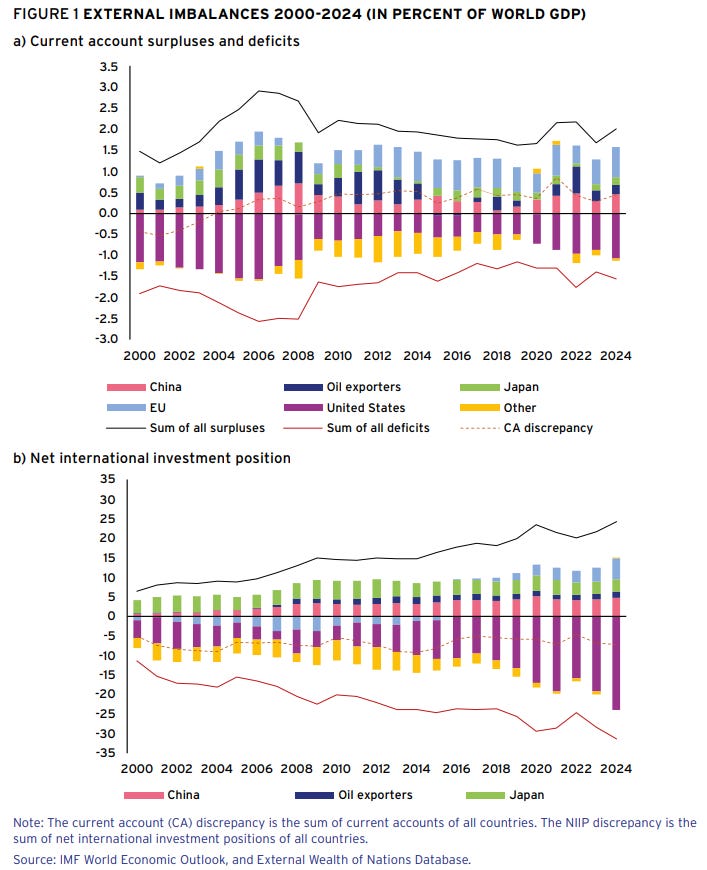

Global external imbalances, 2000–2024

- The chart shows that after 2020, global current-account imbalances and net international investment positions continued to polarize: the US is a major deficit pole, while China is one of the main surplus poles. This is the macroeconomic context for why China's foreign asset flows might be larger than what official data reflects.

$3 trillion

in foreign exchange reserves. With USD interest rates around 4%

, this reserve portfolio alone could theoretically generate more than $120 billionin income each year. But China reports a primary income deficit

, instead of a corresponding income surplus. The IMF also suggests that the yuan is undervalued by about16%

, partly because China's current account surplus is larger than what the IMF model considers normal. The Economist highlights the same paradox: income from China's massive foreign asset block is not increasing correspondingly even as global interest rates rise.This suggests that the story is not just about where China

keeps its assets

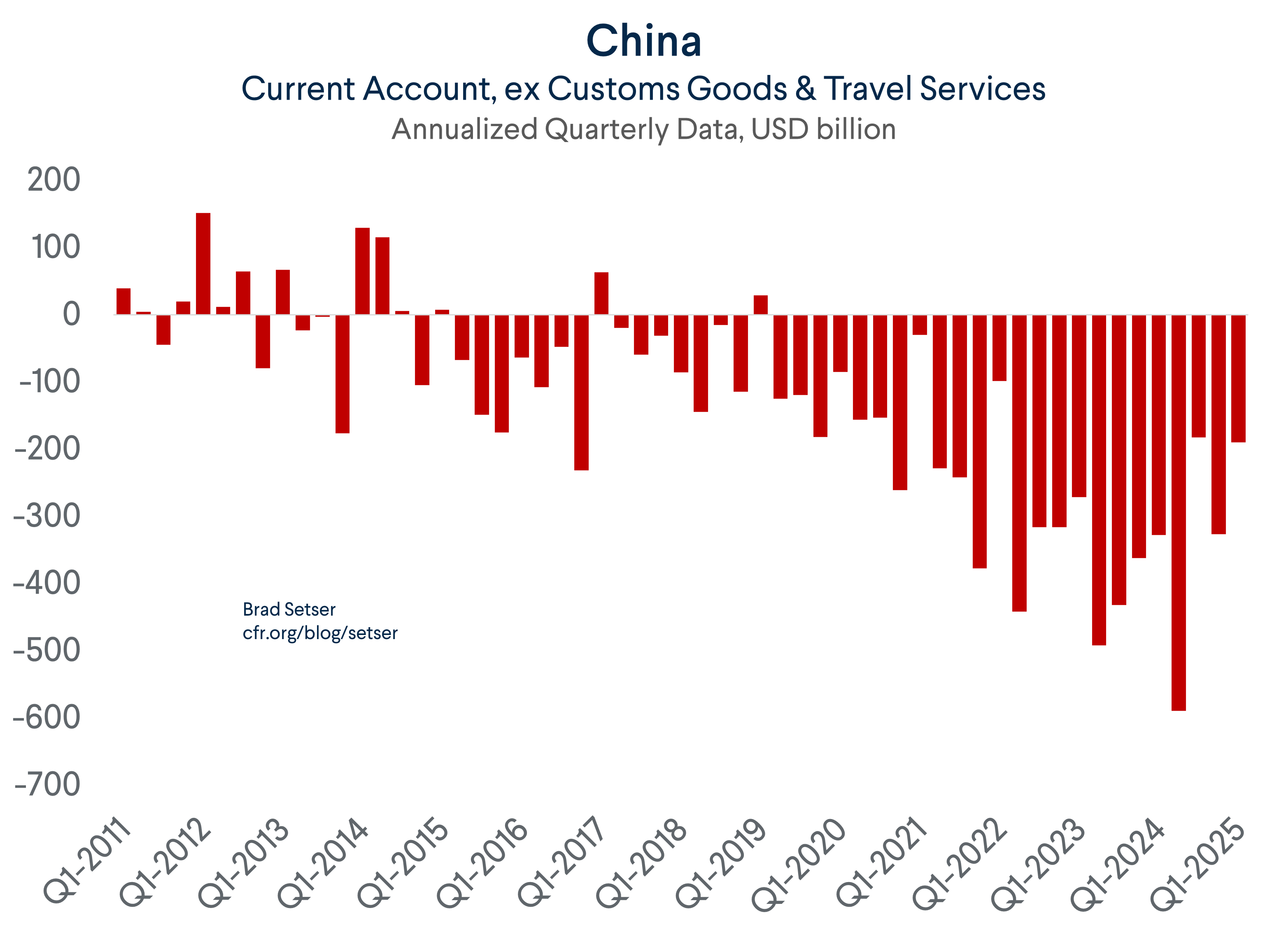

, but also about how China records its income and foreign asset accumulation flows. China - current account, excluding customs goods and travel servicesThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

versus the goods balance in the balance of payments . These two figures can differ due to accounting methods, timing of recording, global supply chains, or processing exports. But in the case of China, the gap has become so large that it raises the question: is the balance of payments understating the true scale of the external surplus?Hong Kong is the next piece of the puzzle. Hong Kong banking data reveals a notable pattern:

foreign currency deposits are rising sharply

, while liabilities to foreign banksare falling. This does not resemble a normal credit cycle. It looks like a system that is absorbing foreign currency liquidity rather than redeploying that capital externally. Image Image

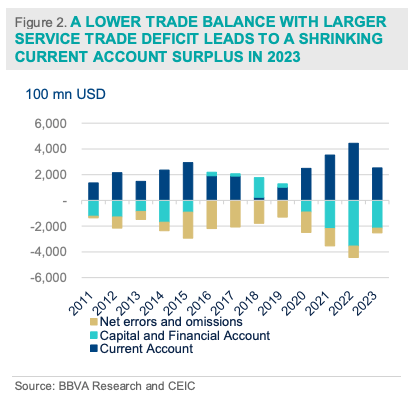

within the Chinese architecture: close enough to the mainland institutionally, but offshore enough not to appear directly in familiar data streams. Before 2022, the errors and omissions

item in China's balance of payments was often deeply negative - for many years in the $100–200 billion range - and was often read by analysts as a sign of unrecorded capital outflows. Recently, this item has almost disappeared, even though signs of private capital flows and unofficial channels have not. This suggests that a portion of capital flows may have been absorbed through other channels: state banks, Hong Kong deposits, offshore accounts, foreign custodians, or semi-official vehicles. China - current account, capital/financial account, and net errors and omissions - The chart shows that for many years prior to 2022, China's “net errors and omissions” were often deeply negative, reflecting a layer of capital flows that are difficult to observe in the balance of payments. By 2023, the current account surplus narrowed due to a lower goods surplus and a larger services deficit, suggesting that China's external balance picture is heavily dependent on accounting adjustments and flows outside easily observable channels.

absorbed a large portion of capital outflows, and recently this item has shrunk while signs of offshore capital flows persist, one should not be quick to conclude that those flows have disappeared. It is possible they have simply shifted to other channels: state banks, Hong Kong deposits, offshore accounts, foreign custodians, or semi-official vehicles . In short:These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

The bigger, quieter, and more realistic risk is: China

From Layer IV, one simple point can be drawn:

China is not a single investor, and its USD assets are not held in a single vault.

If one only looks at PBOC/SAFE

, one sees official reserves. If one only looks at the “China, Mainland”flow in TIC data, one sees even less. China's USD assets may reside in state banks, CIC, SAFE vehicles, Hong Kong, offshore accounts, or custodians in Belgium, Luxembourg, France, the UK, and Canada. The issue is not just about stock

- i.e., how many assets China currently holds. It is also about flow - i.e., how many foreign assets China is accumulating each year. If the balance of payments also shows signs of understating the true scale of the surplus, then both existing assets and new asset flows become harder to read. Therefore, de-dollarization

is a misleading term. It is not certain that China is sharply reducing its USD exposure. What is reducing more clearly is the Section 3 - China's alternative tools are not yet credible enough of U.S. and international data regarding China's true asset position. In other words: China's USD assets have not disappeared. They have simply moved from easy-to-read data tables to more balance sheets, more custodians, and more complex accounting layers that are harder to read.

Over the next few years, the U.S. may have to issue approximately

re-routing

: the assets are still in the dollar system, just moving through harder-to-see pipelines. The conclusion of Layer IV is:China is not just changing where it stores its USD assets. It is changing how those assets appear - or fail to appear - in global data.

And if China has not truly exited the dollar system, the next question is:

can they build a sufficiently credible alternative system?

That is where the story of PBOC swap lines begins. . The PBOC provides what China wants to internationalize: After four layers of analysis, it is necessary to separate the picture into two very different concepts to avoid confusion:

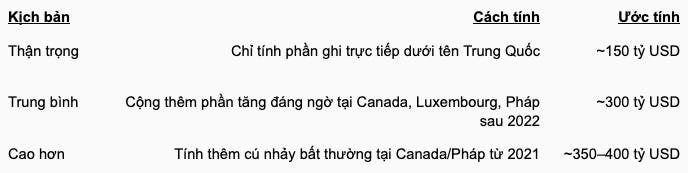

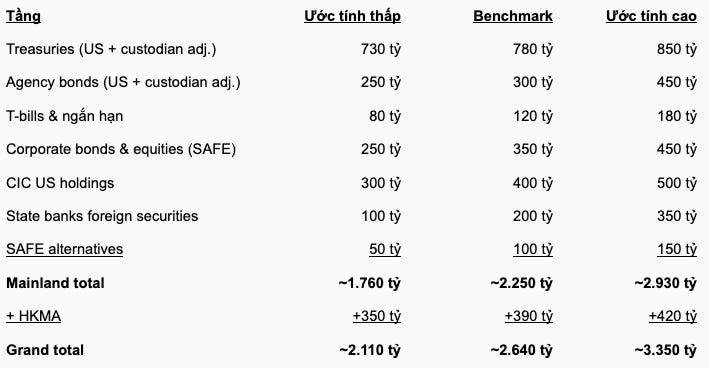

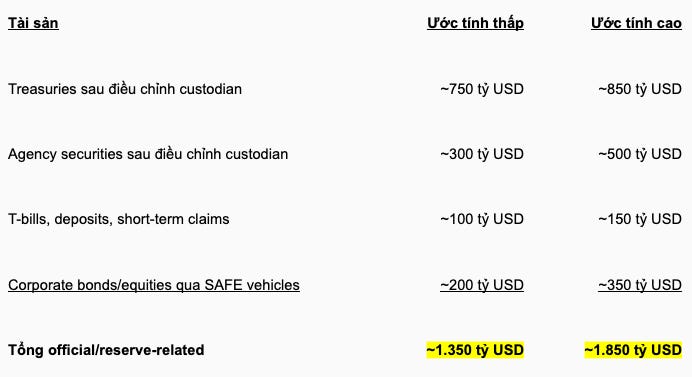

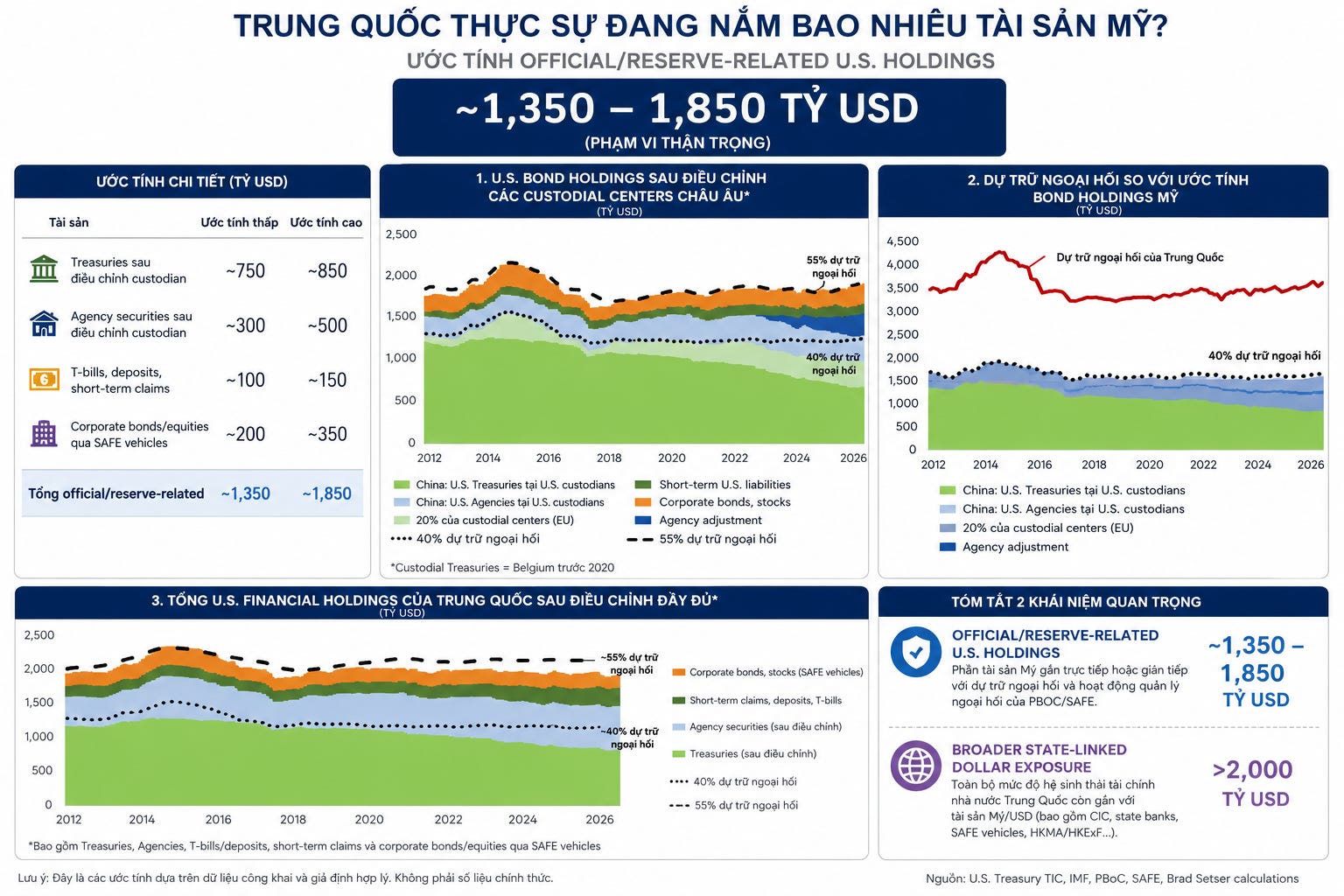

Concept 1 - Official/reserve-related U.S. holdings:

The portion of U.S. assets linked directly or indirectly to PBOC/SAFE reserves, after adjusting for custodians. This is the figure for the narrow question:

“If we only consider reserves and foreign exchange management, how many U.S. assets does China really still hold?” A reasonable estimate for the official/reserve-related U.S. holdings

layer could be in the If we go even further, including range. Therefore, the correct headline is not:These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

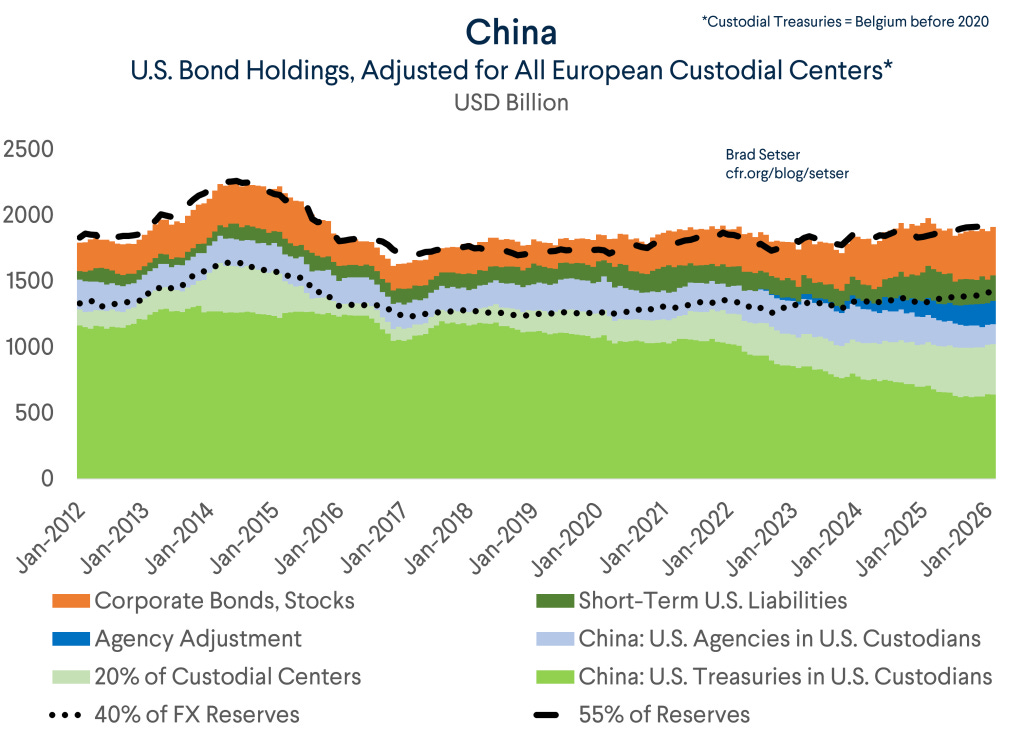

do not decline in the same way. It has fluctuated around nearly 40% of FX reserves for many years. In other words, China may be changing the custody, maturity, and structure of its assets, but the data does not show a simple abandonment of USD assets. A broader summary chart reinforces this point even more clearly. China - U.S. bond holdings after adjusting for European custodial centers

- After adding Agencies, short-term claims, corporate bonds/stocks, and assets held through European custodial centers, China's U.S. financial holdings remain around 50–55% of reserves.

still remain around the 50–55% of foreign exchange reserves range. Therefore, the story is not that China is suddenly abandoning USD assets. The story is more that those assets are becoming less visible in the “China” line of TIC data. Concept 2 - Broader state-linked dollar exposure:The full extent to which China's state financial ecosystem - including CIC, state banks, SAFE vehicles, Hong Kong, and off-channel flows - remains tied to USD assets.

This layer includes: CIC (China Investment Corporation)

, the sovereign wealth fund with significant exposure to equities and alternatives;

State Banks, which may hold foreign securities and participate in backdoor intervention;

SAFE alternative vehicles, such as Buttonwood, the Silk Road Fund, and entrusted loans;

Hong Kong Exchange Fund, if considering a broader strategic financial perimeter.

When expanding to this layer, exposure to US assets/USD could exceed$2 trillion

. However, one must be very cautious: this is no longer “official foreign exchange reserves.” This is The more accurate headline is:- meaning the broader dependency of the Chinese state financial ecosystem on USD assets. Therefore, the question is not: These two figures are related, but they are not the same. If we only look at

$652 billion

, we underestimate the picture. But if we call the entire $2,000 billionfigure “foreign exchange reserves,” we misjudge its accounting nature. The more accurate headline is: China remains deeply tied to USD assets, but that connection is increasingly dispersed across more institutions, more custodians, and more balance sheets.

From the data layers above, the central conclusion is: China is not abandoning the dollar in the sense of significantly reducing its USD asset weight. They are making their USD assets harder to see in US data.

To see the difference clearly, use a simple example: if you have $1 million deposited in New York, and then transfer $700,000 to a bank in Switzerland - you have not “de-dollarized.” You still hold dollars. Your assets are still dependent on the dollar financial system. Only the custody location

has changed. That is exactly what China is doing on a national scale: maintaining dollar exposure, reducing US custodian exposure, shifting from long-term Treasuries to T-bills and Agencies, dispersing custody across Brussels, Luxembourg, Paris, London, Toronto - and using Hong Kong as a liquidity buffer before it finds its way to international financial assets. This is not monetary rebellion. This is

geopolitical risk management

- a completely rational response following the lessons of Russia in 2022. The distinction between currency exposure

and currency exposure dollar liquidity Custody exposure = the proportion of dollar assets in the total portfolio -

What is declining most clearly is not necessarily Custody exposure = the proportion of assets held at US custodians, easily observable in TIC data -

, but rather the portion of USD assets held in U.S.-observable custody channels. Assets can move from New York to Brussels, Luxembourg, Paris, London, Toronto, or Hong Kong. They can shift from long-term Treasuries to T-bills, Agencies, deposits, or the balance sheets of state banks. If I had to summarize it in one phrase: this is not de-dollarization; this is de-visible-dollarization

. PBOC swap lines are the most significant effort in that direction. In terms of scale, this network is not small. But empirical evidence shows that the market still clearly distinguishes betweenThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

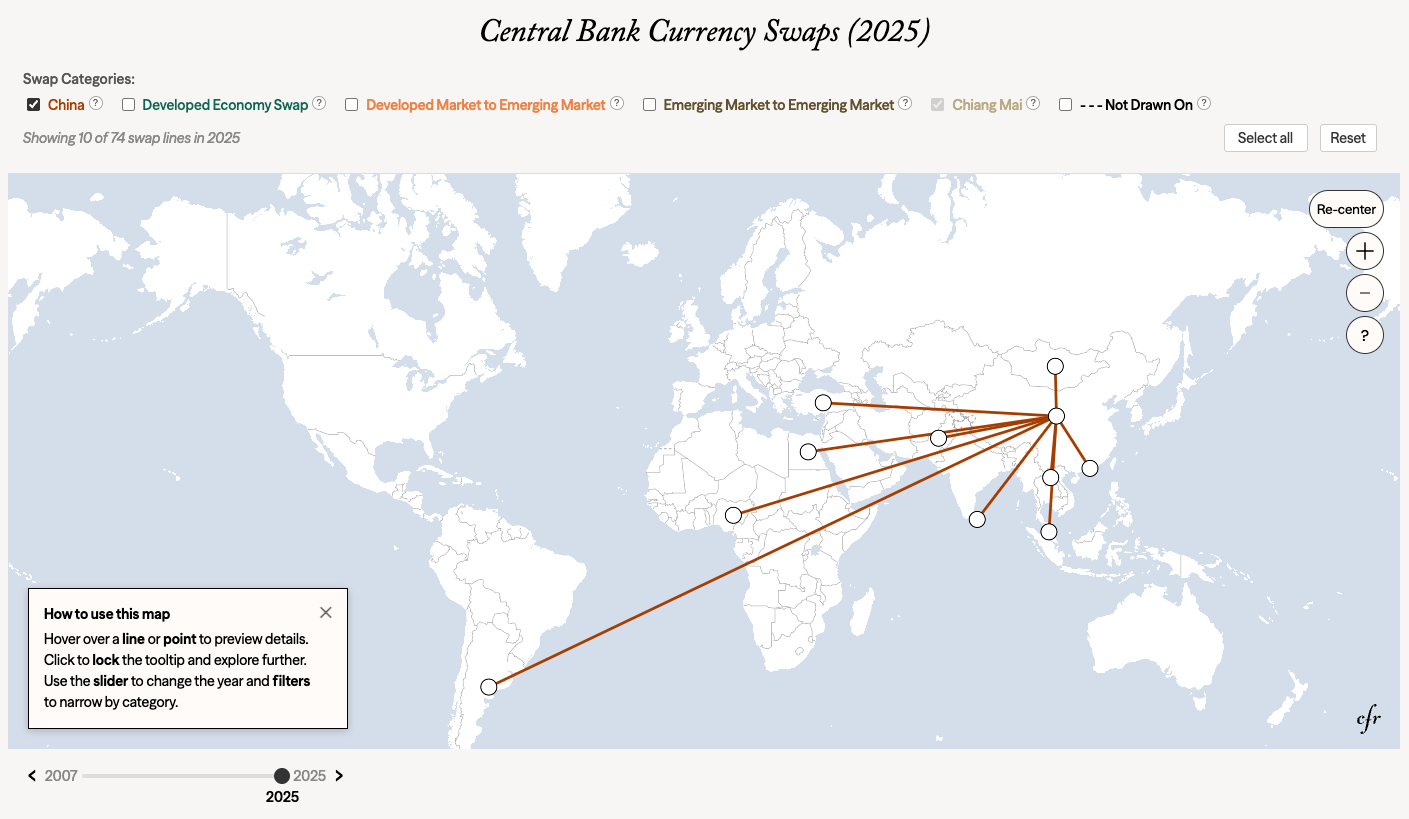

6.1. China is building a parallel liquidity network

The question about

US Treasury bonds

is not just: how much does China hold? The deeper question is: Does Beijing have tools powerful enough to truly reduce its dependence on the dollar system? The most important tool is the network of bilateral currency swap agreements

of the PBOC - that is, agreements between the People's Bank of China and the central banks of other countries, allowing both sides to swap their currencies for a certain period. In terms of scale, this network is not small. The PBOC has approximately $549 billion in committed resources

in swap agreements, roughly equivalent to the $565 billion in borrowing resources of the IMF as of 2020. This shows that Beijing is not just talking about reducing dollar dependence in theory. They are building a layer of financial safety net outside the Fed–IMF–dollar axis. But scale does not equate to reliability. This is the key point.These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

Fed swap lines

and PBOC swap lines dollar liquidity 54 countriesin the J.P. Morgan EMBIG index for the 2006–2020 period, combined with in-depth interviews and event studies around swap agreement signings, shows a clear result: Fed swap lines help reduce government bond yield spreads by approximately

30% , with high statistical significance. PBOC swap linesgenerally do not create a significant positive impact on the creditworthiness of the recipient country.

During the 2017–2020

period, PBOC swap agreements were even correlated with higher sovereign risk levels. Simply put: when a country has a swap line with the Fed, the market understands it as a reliable source ofliquidity insurance

. When a country has a swap line with the PBOC, the market does not price it the same way. The reason lies in the nature of the currency. The Fed provides what the market needs most in a crisis: dollar liquidity

. The PBOC provides what China wants to internationalize: The problem lies in three points: the convertibility of RMB to USD is uncertain, the swap terms lack transparency, and PBOC swaps are often tied to strategic goals rather than acting as a neutral backstop.Therefore, the paradox of de-dollarization lies here: Beijing wants to reduce its dependence on the dollar, but in a real crisis, the world still needs dollar liquidity - not yuan liquidity.Section 4 - “Sell-off” is too simple a description

. 6.2. Why the market does not yet trust PBOC swaps like Fed swaps - Three structural reasonsThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

PBOC swap lines

as equivalent to . The PBOC provides what China wants to internationalize: . The Fed provides what the market needs most during a crisis:These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

USD . Therefore, when a country faces a liquidity crisis, what they need most is usually not RMB, but dollar liquidity. The RMB received from a PBOC swap is only useful if it can be converted quickly, cheaply, and reliably into USD. In reality, this is not always true. Some cases like Pakistan or Sri Lanka show that RMB swaps do not necessarily solve the need for debt repayment or payments in USD. The second is the lack of transparency.The terms of many swap agreements with China are often not fully disclosed: what are the withdrawal conditions, what is the cost, can it be converted to USD, are there any political or commercial strings attached? When the market does not clearly understand how a backstop operates, they will not price it as a true backstop.

The third is the geopolitical context. Over time, PBOC swaps are increasingly viewed as part of China's RMB internationalization, Belt and Road, and financial statecraft strategy - rather than a neutral source of liquidity. This does not mean the tool is useless. But it makes the market ask: is this a reliable liquidity backstop, or a conditional political agreement?

This is the direct link to the Treasuries story. China may want to reduce its reliance on the dollar system, but its alternative tools are not yet strong enough to replace dollar liquidity during a crisis. If PBOC swap lines-a pillar of the yuan internationalization strategy-fail to alleviate market concerns regarding sovereign credit risk, then de-dollarization still lacks a critical foundation.

The paradox lies here:

Beijing wants to reduce its dependence on the dollar, but in a true crisis, the world still requires dollar liquidity-not RMB liquidity.

Therefore, PBOC swaps are a noteworthy strategic tool, but they are not yet a complete substitute for the Fed–IMF–dollar system. China is building a parallel liquidity network, but the market does not yet view it as a lender of last resort when financial stress occurs.

TIER VII - WHY CHINA CANNOT, DOES NOT WANT TO, AND SHOULD NOT SELL OFF

7.1. Prisoners of the trade surplus

This is the point that most narratives about a “financial nuclear option” often overlook: China cannot easily sell off dollar assets because it is trapped by its own trade surplus.

With a goods surplus of over

$1.2 trillion

in 2025, every excess dollar must go somewhere. But every option leads China back to the dollar ecosystem: Accumulating reserves: cash flows still return to Treasuries, Agencies, T-bills, USD deposits, or other short-term assets.

Allowing the CNY to appreciate: exports lose their competitive edge just as the domestic economy faces pressure from deflation, overcapacity, and “neijuan” (involutionary) competition.

Investing abroad: the absorption capacity is still too small compared to the surplus, and it is increasingly blocked by geopolitical barriers and investment security concerns. Keeping it offshore:These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

That is the fundamental paradox: China wants to reduce its dependence on the dollar, but its surplus-based growth model forces it to continue accumulating dollar assets.

The scale also makes comparisons to Russia flawed. China’s dollar assets are many times larger than Russia’s were before 2022. What Russia could do in a few years is not something China can easily replicate without damaging its own financial system and exchange rate. 7.2. The self-destructive logic of a sell-off

Suppose China decides to sell $500 billion in Treasuries

. The chain reaction is not simply “the U.S. collapses.”

First, an increase in Treasury supply would cause bond prices to fall and yields to rise. But higher U.S. yields would also make dollar assets more attractive, potentially driving the USD higher. In that scenario, China would receive a massive amount of USD from the bond sales. If it wanted to convert this USD into CNY, the buying pressure on the yuan would drive the CNY to appreciate sharply-the very thing Beijing is trying to avoid.

In other words, a large-scale sell-off could undermine China’s own exchange rate objectives. Furthermore, if U.S. financial markets experience significant volatility, China would not be immune to the damage. Beijing would face USD/CNY volatility, pressure on Chinese risk assets, capital outflows, falling Chinese ADRs, and tighter global credit conditions.Therefore, Treasuries are not a one-way weapon. They are like a double-edged sword: if activated, the U.S. gets hurt, but China also suffers.

7.3. The dollar ecosystem is too deep to exit quickly

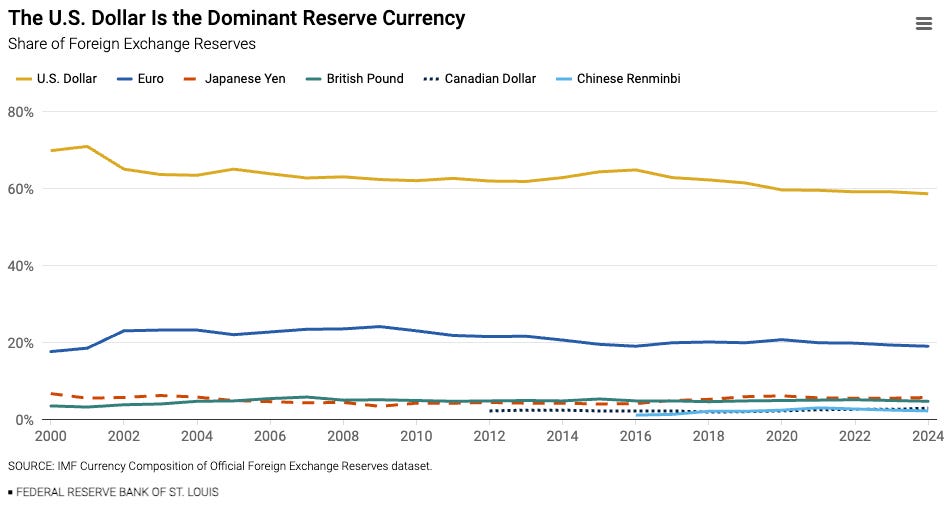

The final reason is the structure of the global monetary system.

The dollar still accounts for approximately

58% of global foreign exchange reserves

, about

54% of cross-border debt

, and appears in nearly 88% of international currency transactions. Meanwhile, the yuan still hovers around 2% of global reserves, having remained nearly flat since 2020. This means the alternative system is not yet deep, liquid, or credible enough to absorb the scale of assets that China needs to reallocate.More importantly, China is not just a dollar creditor. China is also a dollar debtor. The country has approximately $1.1 trillion in foreign debt denominated in dollars, while nearly

84% of its foreign currency debt

is denominated in USD. The banking system alone had about $418 billion in cross-border dollar debtas of Q4 2023. Source: SAFE published China's external debt data as of the end of September 2023 - https://www.safe.gov.cn/en/2023/1228/2157.html Therefore, attacking the dollar is not a cost-free strategy. China holds dollar assets, has dollar-denominated debt obligations, and needs dollars to manage its exchange rate and trade. A rapid exit would shake China’s own balance sheet. The conclusion of this tier is simple: China cannot easily sell off Treasuries, does not want the CNY to appreciate too sharply, and should not damage its own dollar balance sheet.

China is locked into the dollar system not because it believes in the dollar absolutely, but because its own surplus model still requires the dollar to function.

TIER VIII - THE REAL RISK: STRUCTURAL WITHDRAWAL AND THE ARITHMETIC PROBLEM

8.1 Distinguishing between “selling off” and “reducing participation”

An important point that most market commentary overlooks is the difference between

a sell-off

and

reducing the level of participation

. Demand for the U.S. Treasury market consists of two parts: dollar liquidity : buying new bonds when old ones mature.These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

: buying additional bonds issued by the U.S. Treasury.

The issue with China is not necessarily a dramatic sell-off. The issue is that it may beparticipating less in both channels

: reinvesting less in long-term bonds and buying less of the new issuance.With a trade surplus of about

$1.2 trillion per year , China is theoretically a massive natural source of demand for Treasuries. Previously, a significant portion of that surplus could be reinvested in long-term U.S. Treasuries. But if capital flows now shift towardT-bills

, Agency securities, state banks. state banksand offshore accounts, then China does not need to “sell off” to create a new gap in demand for long-term Treasuries. Therefore, the real risk is not that China wakes up one day and sells all its Treasuries. The real risk is that ChinaChina - Treasury holdings if calculating 30% of Treasuries at custodial centers - If looking only at Treasuries in U.S. custodians, China's holdings have dropped sharply. But when adding a portion of Treasuries that may be held at non-U.S. custodial centers-in this chart, a 30% scenario-total Treasury exposure is much more stable than the headline TIC data. This is a sensitivity case, not a definitive figure, but it helps distinguish between “selling off” and “shifting custody locations/holding tenors.” , the “China” line

in TIC data decreasing does not automatically mean China is dumping Treasuries. Part of it could be a reduction in holding

directly within the U.S. custodial system; part could be a shift to T-bills ; part could be a shift to non-U.S. custodians ; and another part could be sitting on the balance sheets of state banks. Therefore, the real risk is not that China wakes up one day and sells all its Treasuries. The real risk is that Chinabuys less ,These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

, and is less present in the demand side that the Treasury market has relied on. The U.S. still has to issue about$1.5–2.0 trillion in new Treasuries annually 8.2 The arithmetic of new issuanceThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

Over the next few years, the U.S. may have to issue approximately

$1.5–2.0 trillion in new Treasuries annually

. Previously, the foreign sector typically absorbed about

20–30%

of new net issuance. Therefore, if major creditors like China and Japan simply buy less, the shortfall is large enough to alter the yields the market demands. could rise, and U.S. long-term interest rates could face upward pressure even if the Fed does not change short-term rates.Foreign demand for U.S. debt assets remains significant, but it is increasingly tied to broader portfolio flows and private credit, rather than just foreign exchange reserve accumulation. This makes China's “buying less” more noteworthy. The risk, therefore, does not lie in a sudden sell-off. It lies in the fact that the structure of global Treasury buyers is changing

$200 billion/year to$100 billion/year

, and Japan does the same due to its own pressures from BOJ policy normalization, higher energy bills, or exchange rate pressures, the market must find an additional $150–250 billion/year from other buyers. The problem is that alternative buyers are typically more yield-sensitive. Ifmutual funds , pension funds

, insurance companies. term premium. This is the true transmission channel from the behavior of major foreign holders to U.S. borrowing costs. No noise. Not a financial nuclear weapon. Not necessarily a geopolitical shock.

Just the arithmetic of supply and demand:

If the old marginal buyer buys less, the new buyer will demand a higher yield.

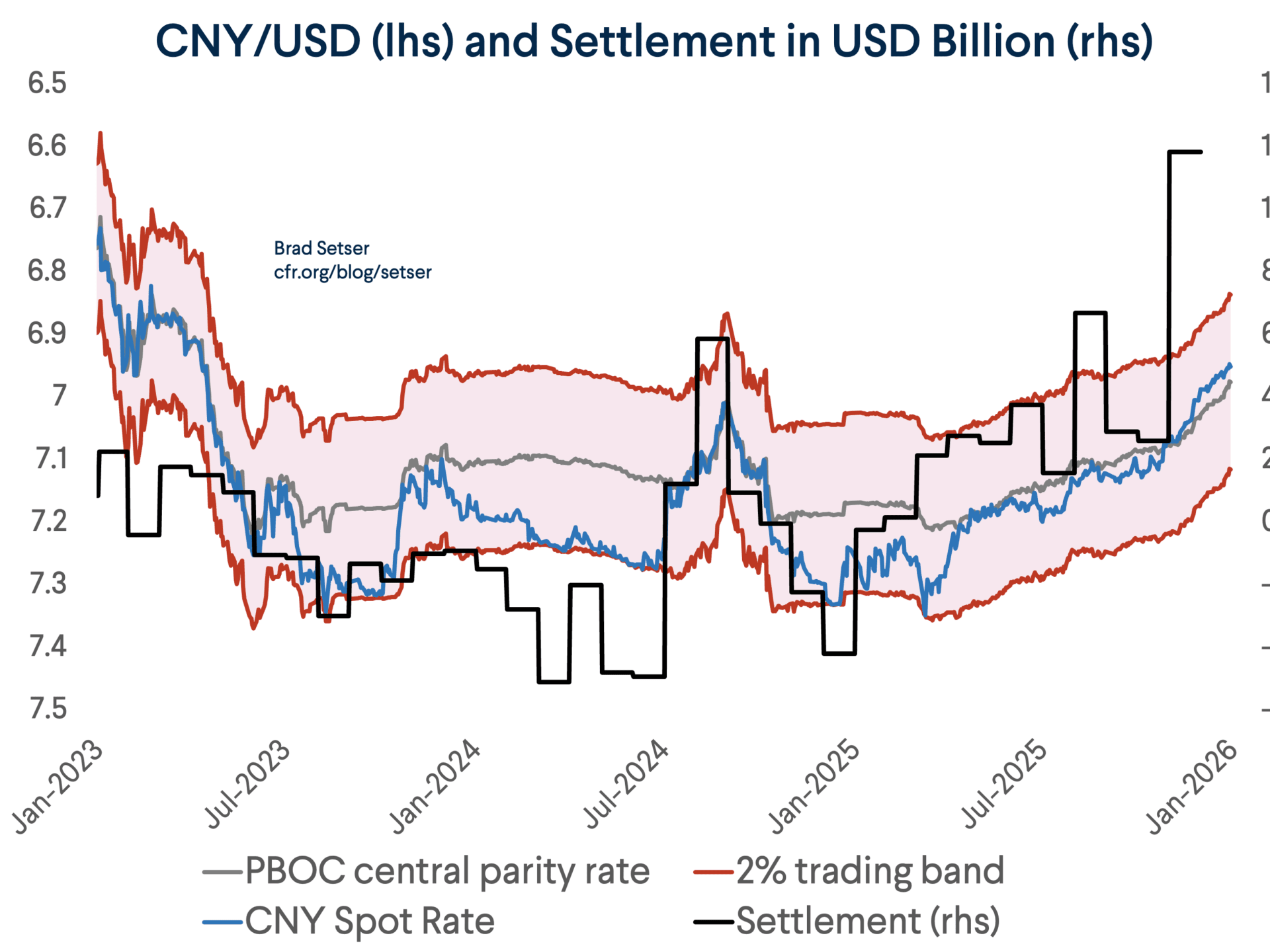

8.3 Reading the 2025–2026 TIC data correctly

China is not selling off all its Treasuries.

China has not truly abandoned the dollar either.

.

Pattern 1 - Shift in July–August 2025:

holdings of China, Mainland fell from $731.4 billion to $695.6 billion, a decline of approximately -$35.8 billion. This is a significant drop, but it should not be simply read as a “sell-off.” In a context where state banks are absorbing more USD and assets may be held through non-U.S. custodians, part of this volatility may reflect a shift in custody location or holding durationThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

Pattern 2 - Flat in June–September 2025: from September to December 2025, holdings fell from $699.7 billion to $683.5 billion, a decline of approximately -$16.2 billion over four months. This is a moderate decrease relative to the portfolio size, more consistent with a state of passive maintenance / portfolio adjustment, not a systematic exit from Treasuries.

Pattern 3 - Net buying month in January 2026: from December 2025 to January 2026, holdings rose from $683.5 billion to $694.4 billion, an increase of +$10.9 billion. This is a key point because it refutes the narrative that China is selling steadily, continuously, and intentionally every month. Pattern 4 - February 2026 nearly flat:February 2026 saw a very slight decline from $694.4 billion to $693.3 billion, or -$1.1 billion. If there were a systematic dumping campaign, one would expect a more consistent and sharp decline. But the January–February data does not show that.

Pattern 5 - The March 2026 drop: March 2026 saw a decline from $693.3 billion to $652.3 billion, or -$41.0 billion. This is the largest drop in the recent series. Reuters also noted that March 2026 was the month when Japan and China led the decline in foreign holdings of Treasuries, while total foreign holdings fell from their February record. This is more consistent with selling driven by liquidity pressure (

liquidity-driven selling ) during a period of market stress, rather than evidence of a linear and prolonged sell-off strategy.

The conclusion of this series is: The TIC data does not show a straight line of “China is dumping Treasuries.” It shows a more complex picture: sharp declines in some months, flat in others, months of net buying, and a large drop during a period of stress.Therefore, the correct reading is not systematic dumping

, but rather:

portfolio rebalancing + custody shifting + liquidity management.

portfolio rebalancing + custody shifting + liquidity management CONCLUSION: FIVE THINGS ACTUALLY HAPPENINGAfter eight layers of analysis - from TIC data, European custodians, Agency securities, state banks, balance of payments, PBOC swap lines, to the supply-demand arithmetic of the Treasury market - five central conclusions can be drawn.

Point 1 - The $652 billion figure is not wrong, but too narrow

held directly in U.S. custodians. But that does not mean they are leaving the USD ecosystem. A portion may be shifting to T-bills. A portion may be held in Agencies. A portion may be moving through foreign custodians. Another portion may be absorbed by state banks or offshore accounts.

$652 billion

often cited only measures a very narrow portion: the amount of

Treasuries recorded directly under the name China, Mainland in the TIC

within the scope of official/reserve-related U.S. holdings, and over $2,000 billion $750–850 billion range.These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

official/reserve-related U.S. holdings - including Treasuries, Agencies, T-bills, short-term deposits, corporate bonds/equities, and assets related to SAFE - the reasonable scale may lie in theThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

range. If we go even further, including CIC, state banks, SAFE vehicles, and the Hong Kong Exchange Fund Therefore, the correct headline is not:These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

, the figure could exceed $2,000 billion . Therefore, the question is not: Does China still hold $652 billion or $2,000 billion? The more accurate headline is:These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

If these three scopes are not separated, any debate about “China dumping Treasuries” easily becomes a conversation with the wrong denominator.

Point 2 - This is a shift in custody location, not an abandonment of the dollar

The crux of the entire article lies in the difference between

currency exposure

and

custody exposure

. currency exposure dollar liquidity Custody exposureThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

What is declining most clearly is not necessarily USD assets

, but rather the portion of USD assets held in U.S.-observable custody channels. Assets can move from New York to Brussels, Luxembourg, Paris, London, Toronto, or Hong Kong. They can shift from long-term Treasuries to T-bills, Agencies, deposits, or the balance sheets of state banks. In headline terms, this looks like:

China is divesting from U.S. assets. But in structural terms, it looks more like:China is making its USD assets more dispersed, shorter-term, harder to freeze, and harder to track directly.

This is not

de-dollarization

in the classical sense. This is

de-visible-dollarization

. Section 3 - China's alternative tools are not yet credible enough If China truly wants to reduce its dependence on the dollar system, it needs more than just changing custodians. It needs an alternative liquidity system that is deep enough, credible enough, and sufficiently accepted by the market. PBOC swap lines are the most significant effort in that direction. In terms of scale, this network is not small. But empirical evidence shows that the market still clearly distinguishes betweenThese buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

and

PBOC swap lines

. The Fed provides what the market needs most during a crisis: dollar liquidity . The PBOC provides what China wants to internationalize:These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

. These two are not equivalent. The problem lies in three points: the convertibility of RMB to USD is uncertain, the swap terms lack transparency, and PBOC swaps are often tied to strategic goals rather than acting as a neutral backstop.Therefore, the paradox of de-dollarization lies here: Beijing wants to reduce its dependence on the dollar, but in a real crisis, the world still needs dollar liquidity - not yuan liquidity.Section 4 - “Sell-off” is too simple a description

The 2025–2026 TIC series does not show a straight line of “China is selling off Treasuries.”

The data reveals a more complex picture: some months show sharp declines, some periods are nearly flat, some months show net buying, and there is a large drop during periods of market stress.

A more reasonable interpretation is:

portfolio restructuring + shifting custody locations + liquidity management

.

China may be reducing its share of

long-term Treasuries held directly in U.S. custodians. But that does not mean they are leaving the USD ecosystem. A portion may be shifting to T-bills. A portion may be held in Agencies. A portion may be moving through foreign custodians. Another portion may be absorbed by state banks or offshore accounts.These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

China is not necessarily selling off all its U.S. assets. They are restructuring how they hold USD assets. Section 5 - The real risk is not a dump, but a quiet retreat from the role of marginal buyer The biggest risk is not that China wakes up one morning and sells all its Treasuries.

The bigger, quieter, and more realistic risk is: China

buys less

,

reinvests less in long-term maturities

, and is less present in the demand side that the Treasury market has relied on. The U.S. still has to issue about$1.5–2.0 trillion in new Treasuries annually over the next few years. If major creditors like China and Japan gradually reduce their role in absorbing new issuance, the shortfall must be shifted to other investors: bond funds, pension funds, insurance companies, banks, or domestic U.S. investors.These buyers are typically more yield-sensitive. They will demand a higher risk premium to absorb additional duration. In that case,

term premium could rise, and U.S. long-term interest rates could face upward pressure even if the Fed does not change short-term rates. This is the real transmission channel from the behavior of foreign holders to U.S. borrowing costs.

No noise. Not a financial nuclear weapon. Not necessarily a geopolitical shock.

Just a supply and demand arithmetic problem:

If the old marginal buyer buys less, the new buyer will demand a higher yield.

The most concise answer

China is not selling off all its Treasuries.

China has not truly abandoned the dollar either.

China is doing something more sophisticated:

restructuring how it holds USD assets so they are less visible, more flexible in terms of maturity, more dispersed in terms of custody, and less dependent on the U.S. custody system.

The figure of

$652 billion

is only the portion of Treasuries directly visible in TIC. The broader picture shows that China remains deeply tied to USD assets - perhaps around $1,350–1,850 billion

within the scope of official/reserve-related U.S. holdings, and over $2,000 billion if all state-linked dollar exposure is included. Therefore, the correct headline is not: China is selling off Treasuries and abandoning the dollar. The more accurate headline is: China remains in the dollar system, but is learning to navigate that system through less visible pipelines.

The real risk, therefore, does not lie in a dramatic sell-off. The risk lies in a slower but deeper change:

the old marginal buyer is gradually stepping off the stage, just when the Treasury market needs more buyers than ever.

Headline đúng hơn là:

Trung Quốc vẫn ở trong hệ thống đô la, nhưng đang học cách đi trong hệ thống đó bằng những đường ống khó nhìn hơn.

Rủi ro thật vì vậy không nằm ở một cú bán tháo kịch tính. Rủi ro nằm ở sự thay đổi chậm hơn nhưng sâu hơn: người mua biên cũ đang lùi dần khỏi sân khấu, đúng lúc thị trường Treasury cần thêm người mua hơn bao giờ hết.