Economic Consequences of the Trump Assassination Attempt, Views on Inflation, Recession, and the FED

In the latest PODCAST, Steve and Linh Hà will discuss the details of yesterday's world-shocking event when Trump narrowly escaped assassination and the market reactions and consequences following the event. Afterwards, Steve and Linh Hà will provide insights into inflation trends, recession, and possible FED actions in the next 2 meetings.

- Accurate account of the Trump assassination attempt

- What was the market's reaction after the Trump assassination attempt?

- Why is PPI diverging from CPI?

- Is the strong disinflation data from last week concerning?

- Is the job market showing signs of recession?

- Where are the banking crisis and debt?

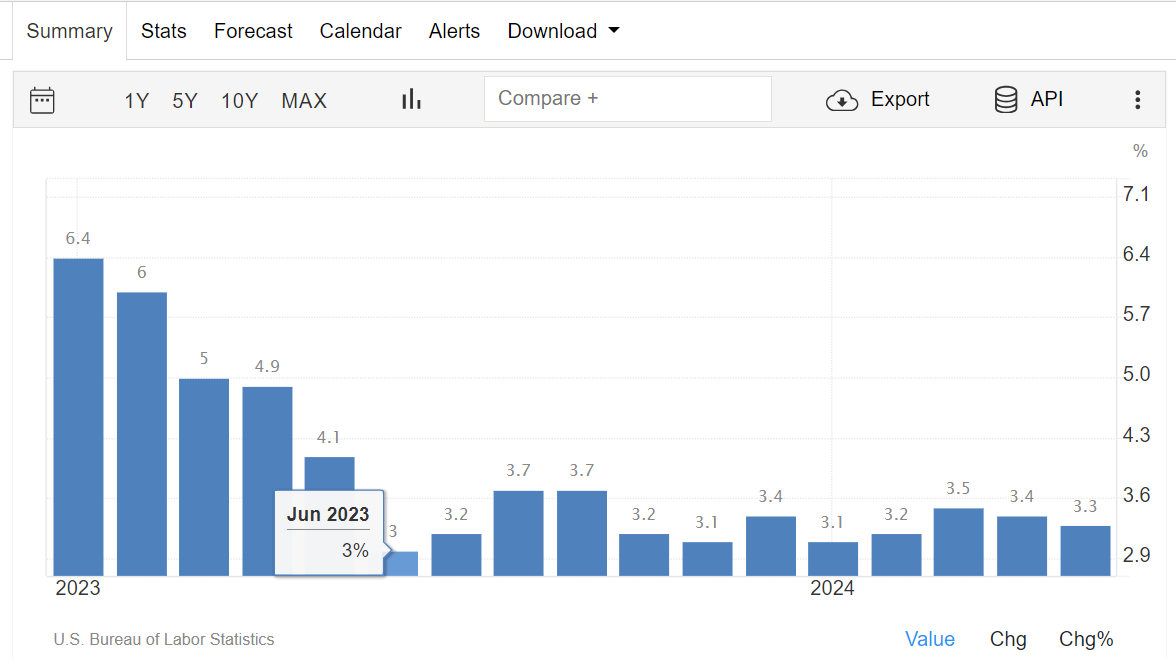

June CPI Growth surprisingly dropped sharply, causing the market to fear the possibility of deflation occurring due to sudden consumer spending cuts. However, service business profit margins remain high in PPI report which is also a factor curbing the economy's deflation risk. Therefore, the current disinflation trend is not guaranteed to cause a deflation shock.

In addition, last week's inflation figures, accompanied by the somewhat worsening labor report from the previous week, are two convincing pieces of evidence that the Fed may cut rates starting in September. In particular, Powell has also affirmed that the Fed is equally weighing 2 risks: escalating inflation VS recession from the labor market – indicating that the Fed is paying more attention to the labor market than in previous periods.

And ahead of the Fed (possibly) cutting rates in September, Viet Hustler will dedicate this week's macroeconomics article to reviewing the overall US financial market landscape – and market movements preparing for the upcoming Fed pivot.

In the final part of the article, Viet Hustler will also assess the sustainability of the current disinflation cycle.

Disclaimer: Some of the views below are the personal opinions of the author – and not investment advice!

Trends in the financial market before the Fed cuts interest rates

1. Debt market: Investors pour money into bonds to lock in high yields before the Fed cuts rates.

Previously, bonds and stocks were 2 alternative investment channels (correlation up to -0.6).

But now, the debt market is increasingly less affected by the stock market: correlation down to ~ -0.2

=> Despite stocks rising, demand for bonds remains strong!

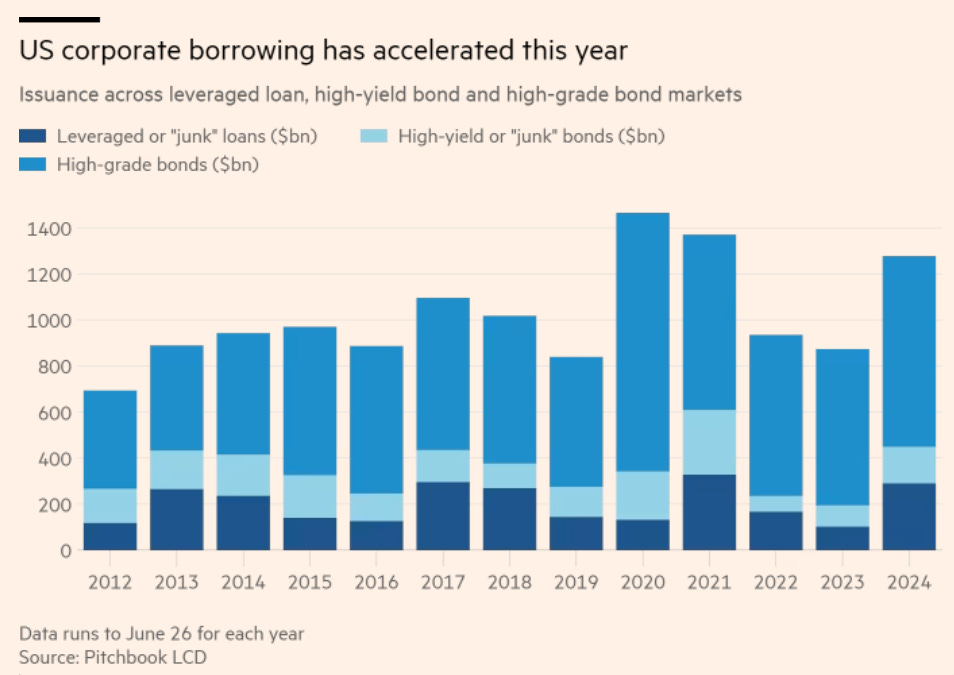

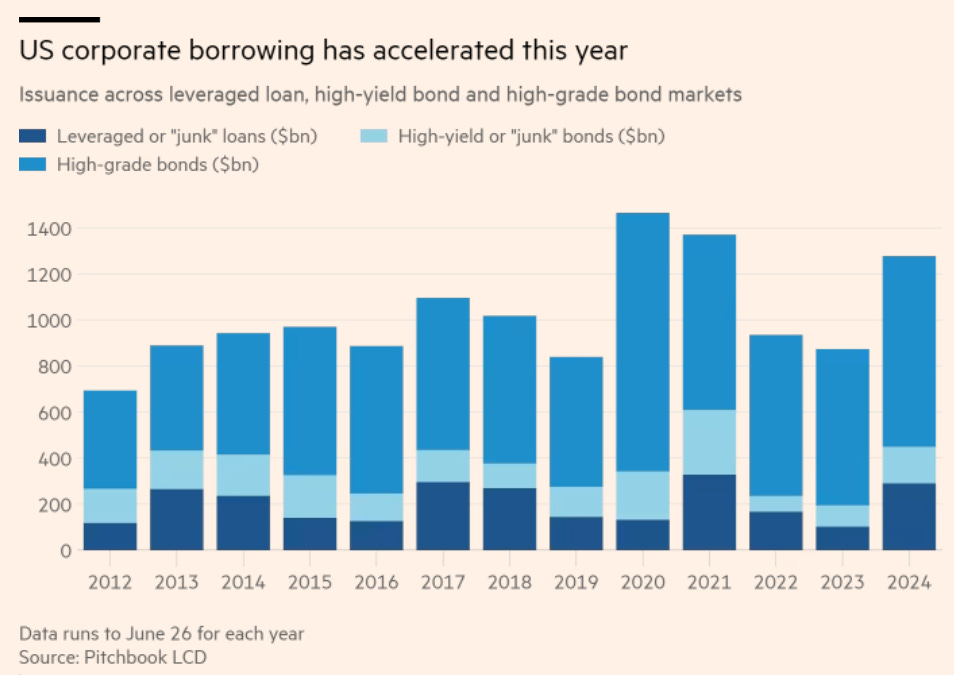

In the first half of 2024, businesses also ramped up borrowing activities:

Value of bond issuances (combining high-grade, high-graded, and low-quality, junk-rated) increased by about ~+50% Y/Y- to ~USD 1.3 trillion.

Corporate debt issuance is driven by high demand for US corporate bonds from investors (NĐT) worldwide.

Simply, investors want to lock in high yields before the Fed cuts rates later this year.

Especially foreign NĐT from markets with lower yields (China, Japan…)

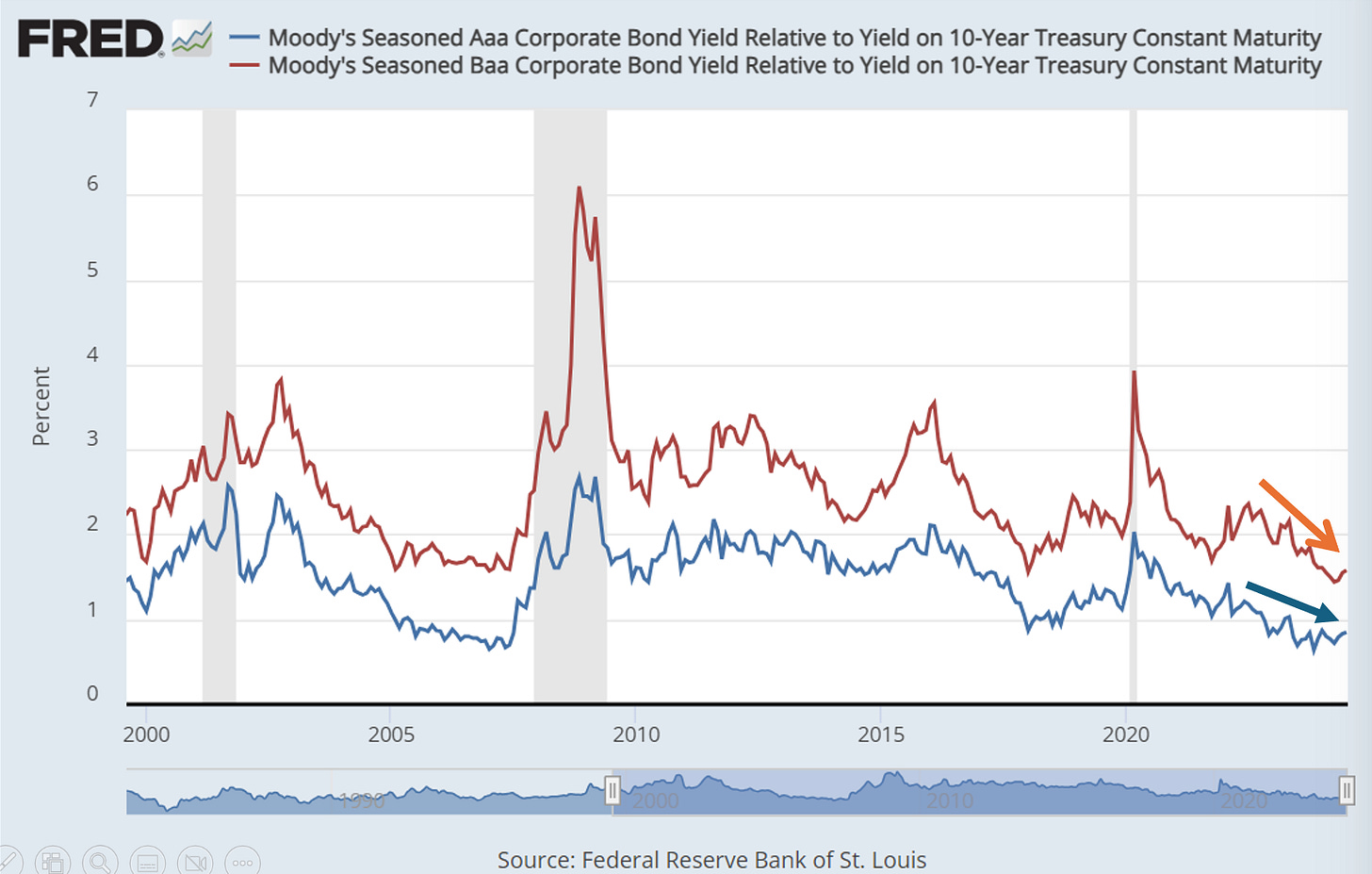

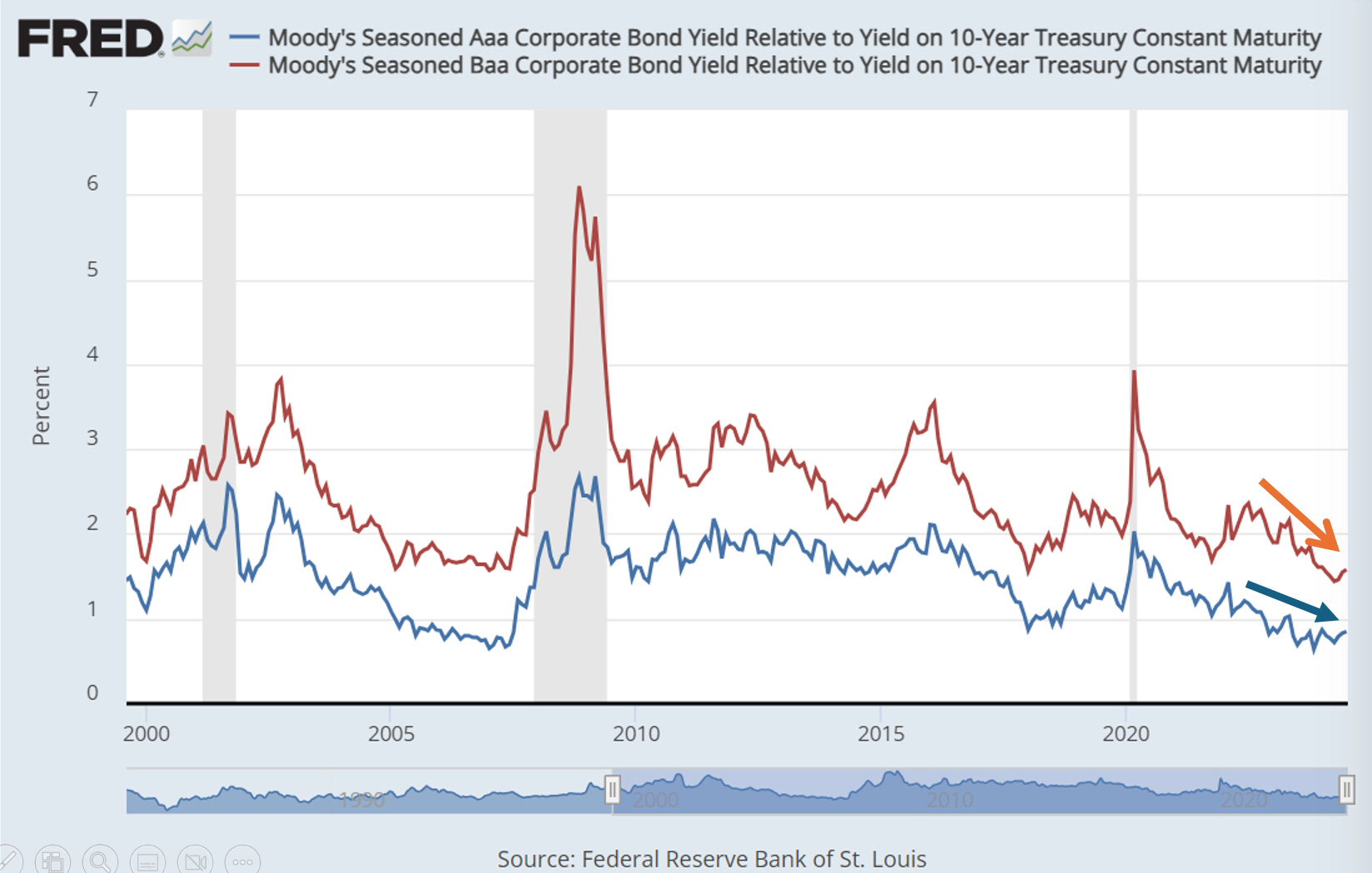

Meanwhile, businesses with ongoing borrowing needs want to issue more debt while lending demand is still high to secure lower costs:

Although corporate borrowing rates are still higher than the Fed rate, the risk premium has decreased:

Many large companies want to seize this debt-raising opportunity to acquire small companies struggling in the current environment. For example:

Home Depot issues 10 billion USD in debt to buy distributor SRS Distribution

AbbVie issues 15 billion USD in debt to buy ImmunoGen and Cerevel…

Small companies are raising junk-rated debt to refinance old debts:

Junk loan restructurings surged in the first 6 months of the year.

Therefore, the trend of investing in the debt market to lock in high yields will continue to be driven from now until September before the Fed cuts rates.

While businesses will still issue more debt at the current low premium (risk premium).

2. Stock market: corporate profit margins are still high – boosting investor confidence in US stocks

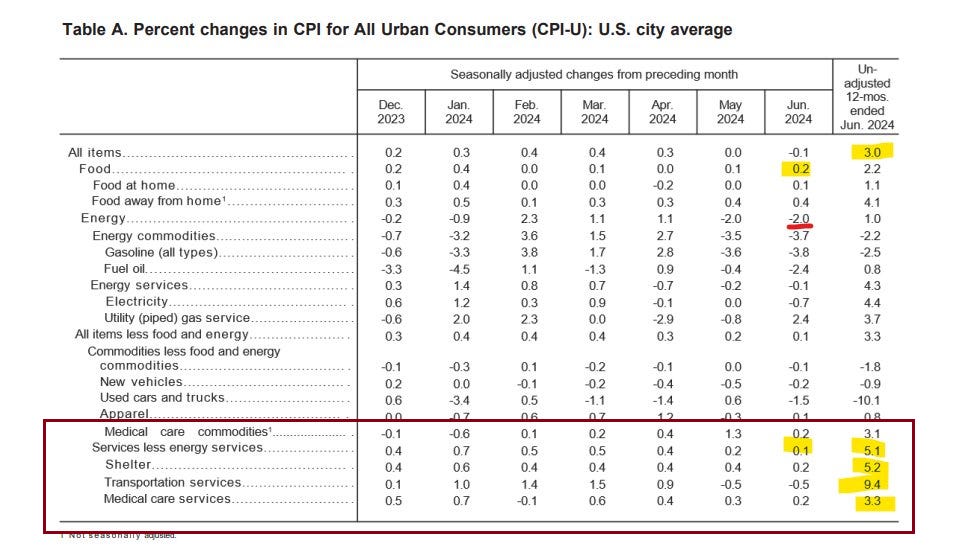

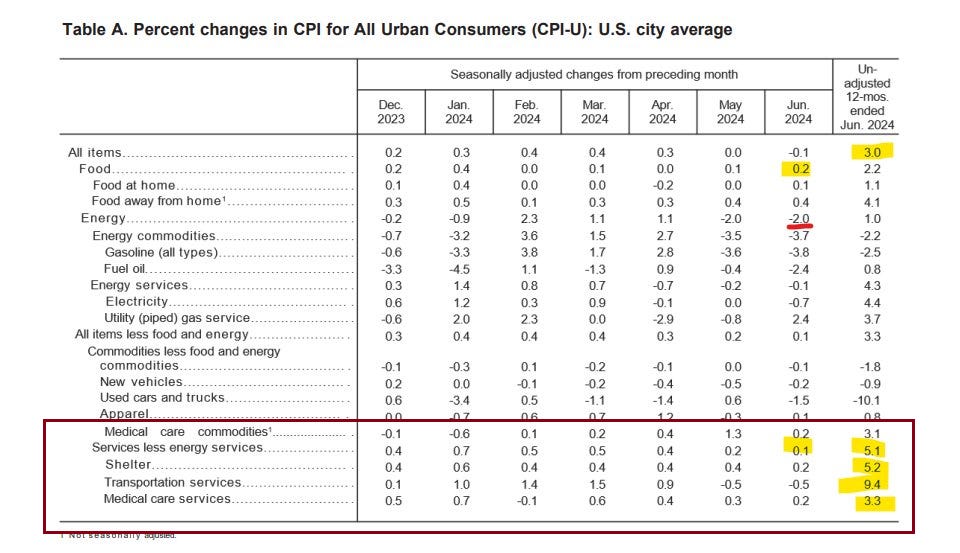

The June CPI report shows that service inflation remains high:

And the current high service inflation comes from service companies' profit margins still being too high.

Read more: Details of the June 2024 PPI report

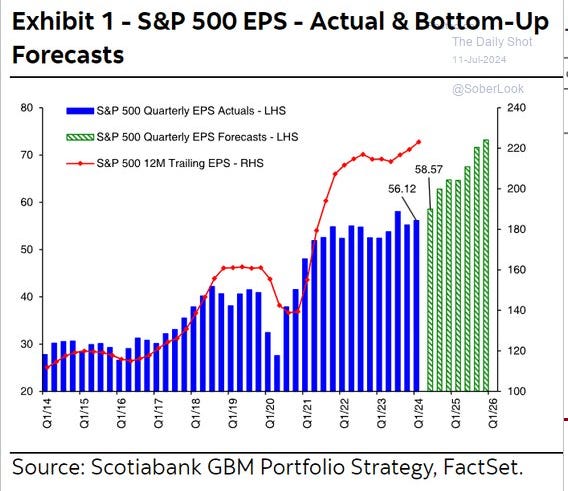

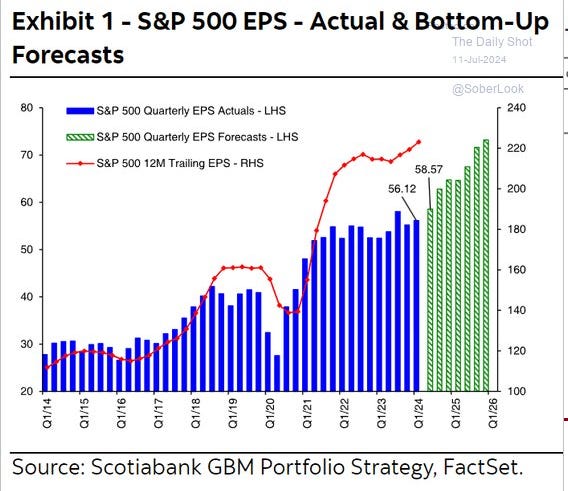

Forecasts for US corporate earnings growth will continue to improve in the Q2FY2024 earnings season starting next week:

Bloomberg Intelligence's forecast for S&P500 corporate earnings growth:

Profits of companies outside the Mag-7 group will also grow.

Forecast EPS will also increase:

And Q2 (fiscal 2024) forecast will also be the first quarter where the S&P 493 group's EPS grows:

=> This boosts the likelihood that the stock market will hold steady amid the disinflation storm – and even deflation in the near future.

… unless a major recession occurs!

Even if the profit cushion is large enough, large companies (S&P500) can still weather a recession!

Additionally, amid a volatile global economic outlook, investors are betting even more on the US economy:

IMF says the concentration of capital into the US market has increased post-Covid.

3. US banking system: waiting and hoping the Fed cuts rates soon enough… and fast enough

The banking system is still suffering large unrealized losses in Q1/2024:

However, from now until the Fed cuts rates, banks will try not to sell the US Treasuries they hold….

…. to avoid recognizing those losses.

This is also a bright spot for the US Treasury: Yellen won't need to worry about any major Treasury sell-off coming soon, at least from banks.

Even though bond losses are unrealized, other losses have started to be recognized by major banks in financial reports:

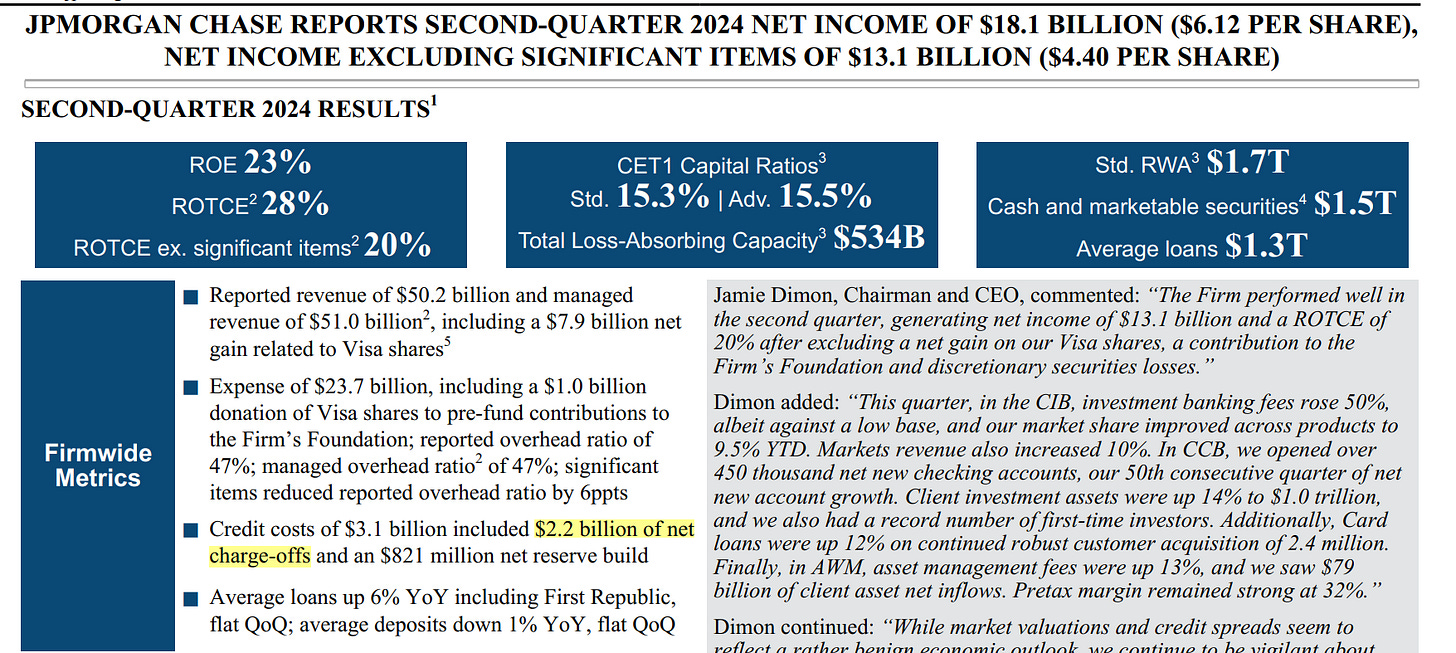

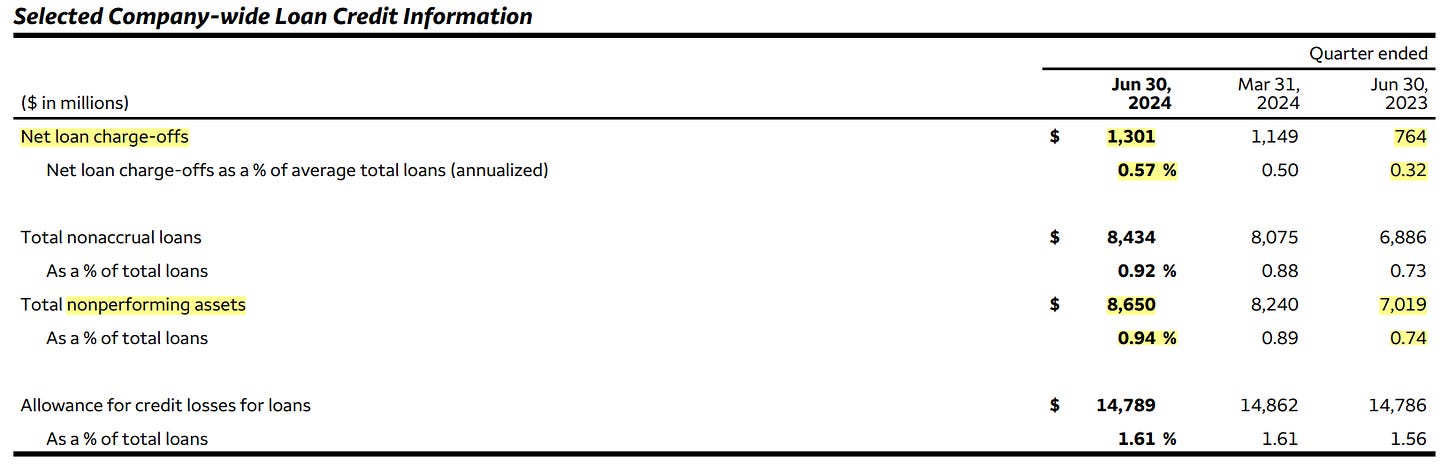

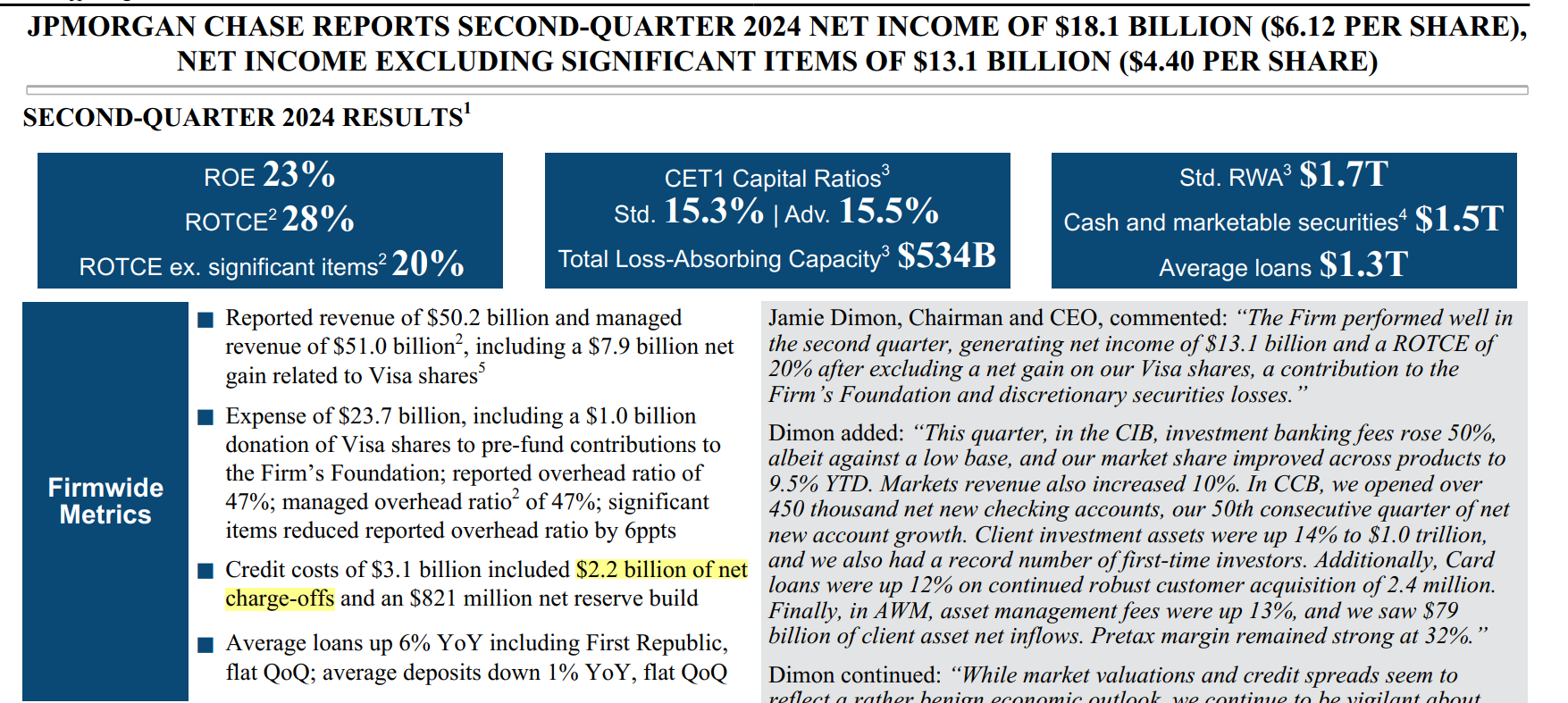

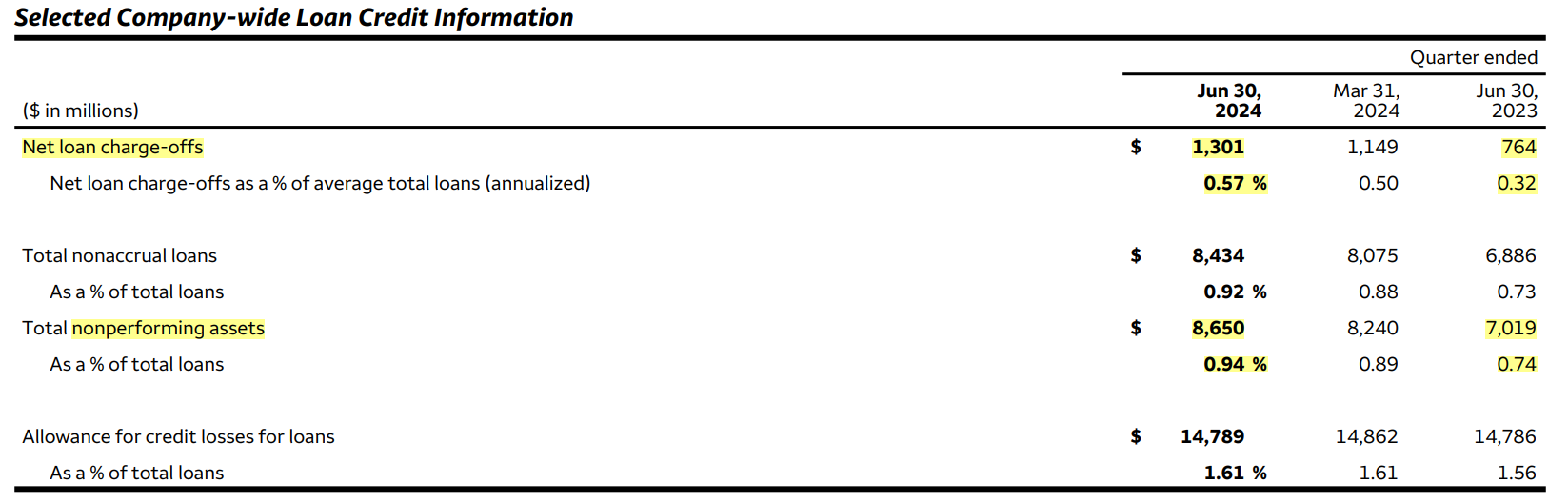

In the Q2/FY2024 earnings report (ER), JP Morgan recognized a USD 2.2 billion bad debt loss not recoverable (net charge-off)…-- up +USD 200 million from previous quarter and + USD 800 million Y/Y.

Wells Fargo recognized USD 1.3 billion in uncollectible debt losses (net charge-off) – up +70% YoY.

Next week, more banks will report Q2 ER: the overall picture will become clearer.

Those losses are not large, but could cause fear among depositors, especially if more banks face similar issues in next week's ER reports.

The next question to ask is: whether banks can avoid a bank run wave before the Fed cuts rates?

Additionally, in last week's testimony, Powell mentioned that large banks will not be affected by commercial real estate debt (CRE).

But Viet Hustler emphasized that bad debts from CRE affect smaller banks more:

…. market values of small banks are “lagging” behind large banks!

However, with CRE debt partially repaid and no new debt borrowed in a high interest rate environment: the CRE debt to real estate value ratio is quite low.

Therefore, just like the unrealized losses from bonds, banks may still not recognize too many losses from commercial real estate, and hold on waiting for the Fed to gradually cut interest rates or for the situation to improve.

But a quite important factor is that, even though the Fed is highly likely to cut interest rates from September, will the Fed cut interest rates fast enough and deeply enough so that banks do not have to recognize losses?

Is the current disinflation trend sustainable and accelerating?

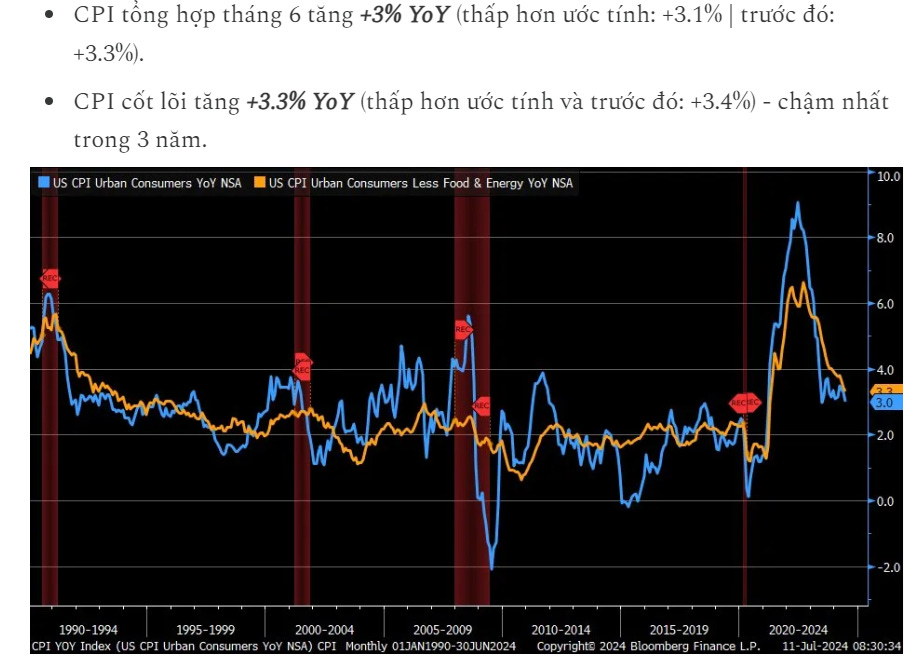

Last week's CPI report showed that inflation fell more than market expectations:

However, CPI had previously dropped from 4.1% to 3% back in June 2023 – when the Fed was near its peak interest rate. But then inflation rose again.

Therefore, many people may doubt whether the current disinflation trend is sustainable?

However, the current inflation situation is different from before:

The disinflation trend has been clearly demonstrated with the monthly growth of supercore CPI at -0.05% MoM in June!

And supercore CPI excludes most volatile factors like food, energy, and lagged factors like housing.

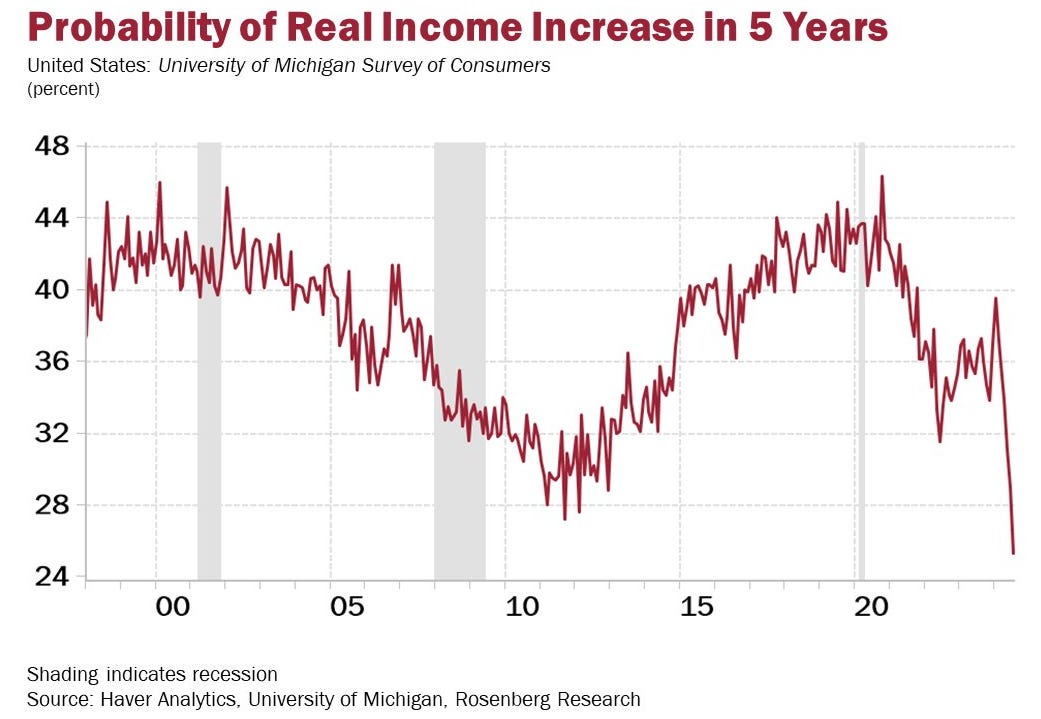

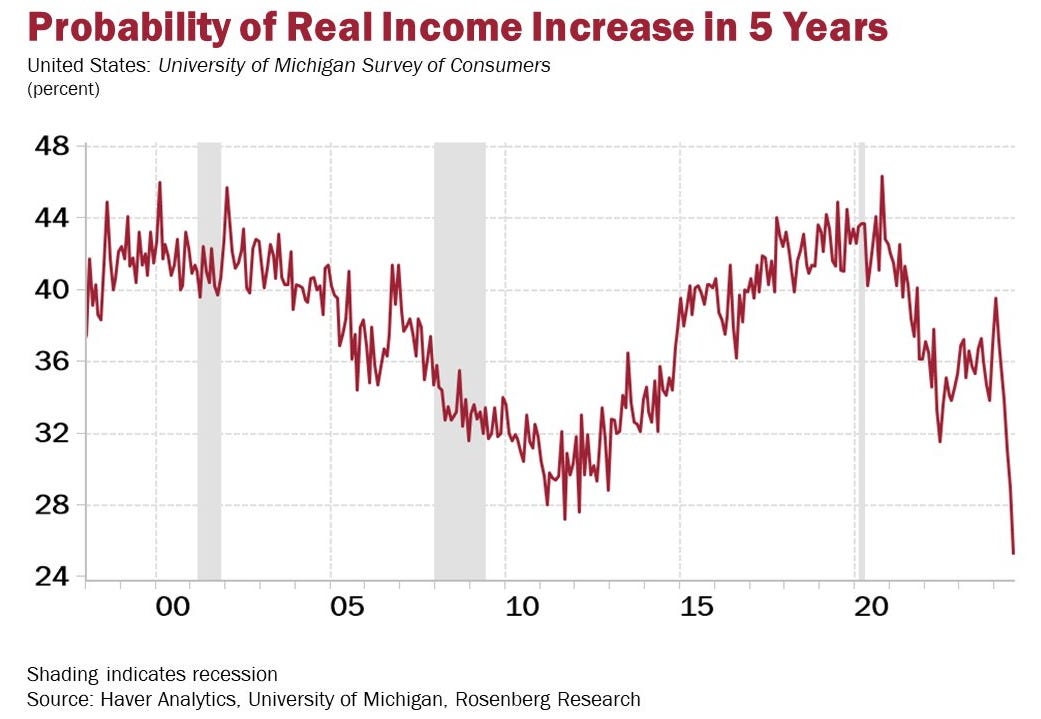

The UMich consumer expectations survey shows a sharp drop in the number of respondents expecting income growth over the next 5 years.

When people do not expect income growth, naturally they will not consume but instead save (or pay off previous credit debt)…

=> …this is precisely the driving force behind the disinflation process.

Personal saving rate rose slightly in May - though still at the lowest level in over a decade

The slight increase in the saving rate also reflects the effect of the Fed's interest rate-monetary policy in guiding people: from consumption to saving.

Meanwhile, businesses are increasingly feeling the impact of declining consumer demand:

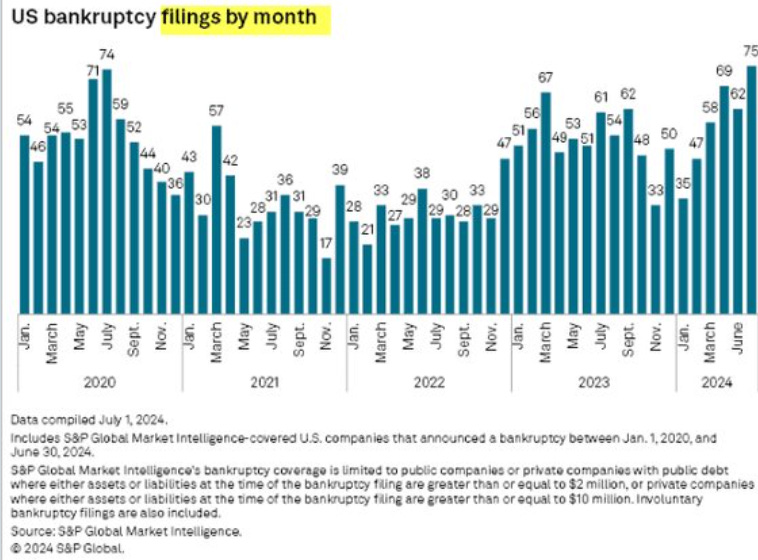

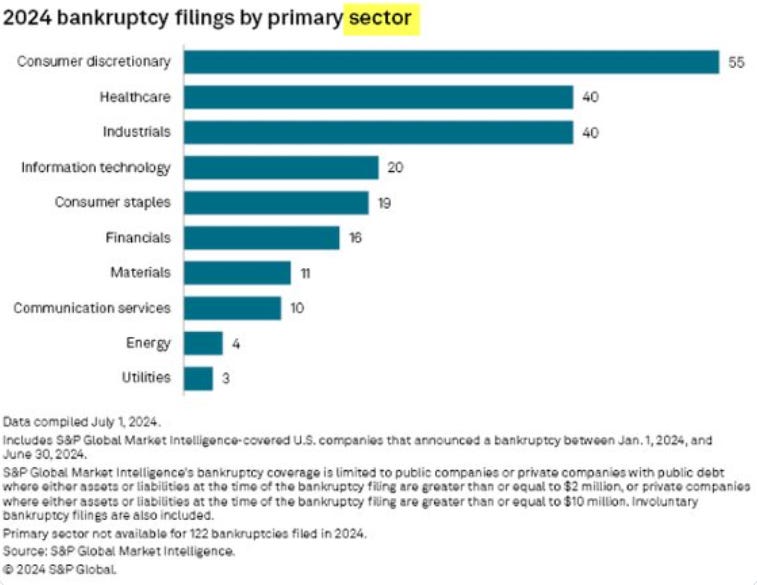

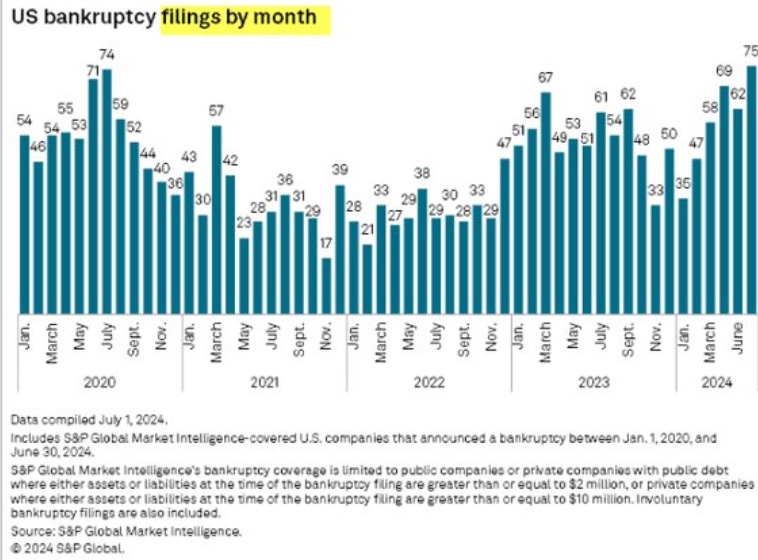

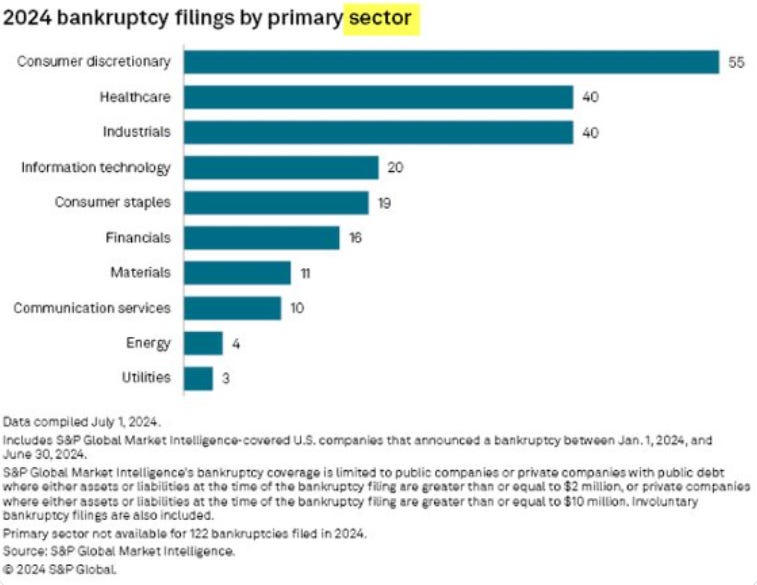

The number of corporate bankruptcies in the past 3 months has risen rapidly:

And consumer goods companies are leading the “bankruptcy” group this year.

This is only statistics for companies that have issued debt and stocks on the public market.

The situation may be worse for small businesses that only rely on bank loans.

Therefore, from now until September, the Fed may see greater disinflation speed to gain momentum for rate cuts.

CONCLUSION

Viet Hustler mostly makes assessments based on economic data. And the inflation and employment data over the past 2 weeks all point to a high likelihood that the Fed will cut interest rates from September. Especially since the signs of the current disinflation trend are quite solid - not ambiguous like before.

Meanwhile, the banking system is still holding out without recognizing unrealized losses (unrealized loss), waiting for the Fed to cut interest rates this year. However, last week's reports from JPM and Wells Fargo show that many of their losses “could not wait” and had to appear on financial statements. These losses are small, but they warn of greater losses from the banking system if the Fed does not cut rates soon enough… and fast enough, deeply enough.

In the corporate bond debt market, investors are still aggressively locking in high yields before the Fed cuts rates - while companies continue to ramp up debt issuance at low risk premium levels. In the stock market, high service company earnings have created confidence for investors to keep buying, despite recession risks. So, is the high profit cushion of companies enough for them to withstand the approaching recession?