In the past 2 weeks, a series of macro data released has shown a panoramic picture of the economy: from consumption, inflation, economic growth to the labor market… Therefore, this weekend is an appropriate time for Viet Hustler to sit down and comprehensively evaluate which scenario might occur for the US economy:

Will the Fed achieve soft-landing as expected?

Or hard-landing leading to recession (global)? (If so, which policy direction will the Fed choose?)

Or could it be stagflation that exhausts the economy in the long term?

This week's macroeconomics column of Viet Hustler will summarize the overall picture of the US economy based on the data from the past 2 weeks. From there, Viet Hustler will provide an assessment of the upcoming scenario for the US economy.

Disclaimer: Some opinions below are the subjective opinions of the author - and not investment advice!

I. Overall picture of US economic data in the past 2 weeks

Two prominent developments regarding the economy and labor market in last week's macro data include:

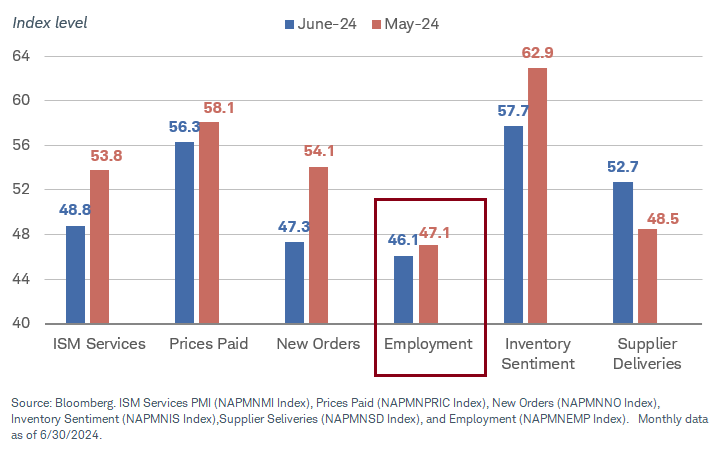

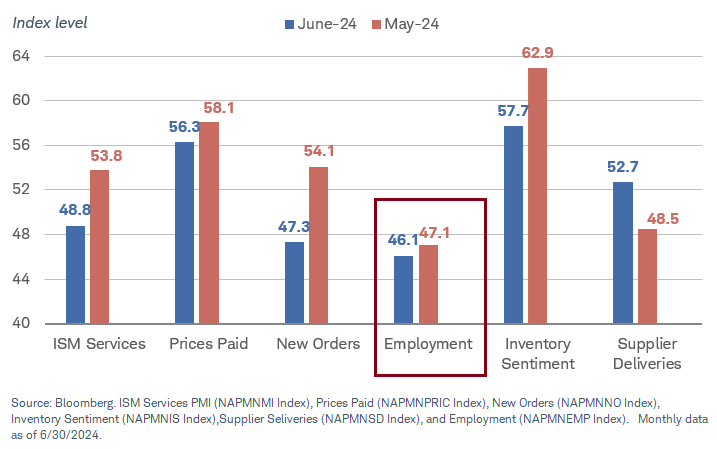

» I.1. The economy is slowing down: the service sector begins to contract

Viet Hustler has emphasized: the US economy is a service economy.

Once service demand begins to decline, recession is near.

And the early indicator of economic activity is PMI index (ISM) reflecting this!

Services PMI has followed the trend of Manufacturing PMI (ISM): dropping below the 50 threshold (contraction threshold) in May.

Periods when both indices are below 50 at the same time signal major economic fluctuations:

July 2008 - 2009 => Recession

April-May 2020 => Recession

December 2022 => small bank crisis in March 2023

Service business activity also fell to contraction threshold (below 50) for the first time since the 2020 recession => service consumption demand is slowing down!

When business activity contracts, the labor market will be the first market affected:

Employment component (Services PMI) is at the most severe contraction level….

…. indicating that service businesses' labor demand has cooled:

» I.2. Labor market “normalizing” on the surface - but reality has turned bad

Details of June Employment Report were reported by Viet Hustler on 07/05.

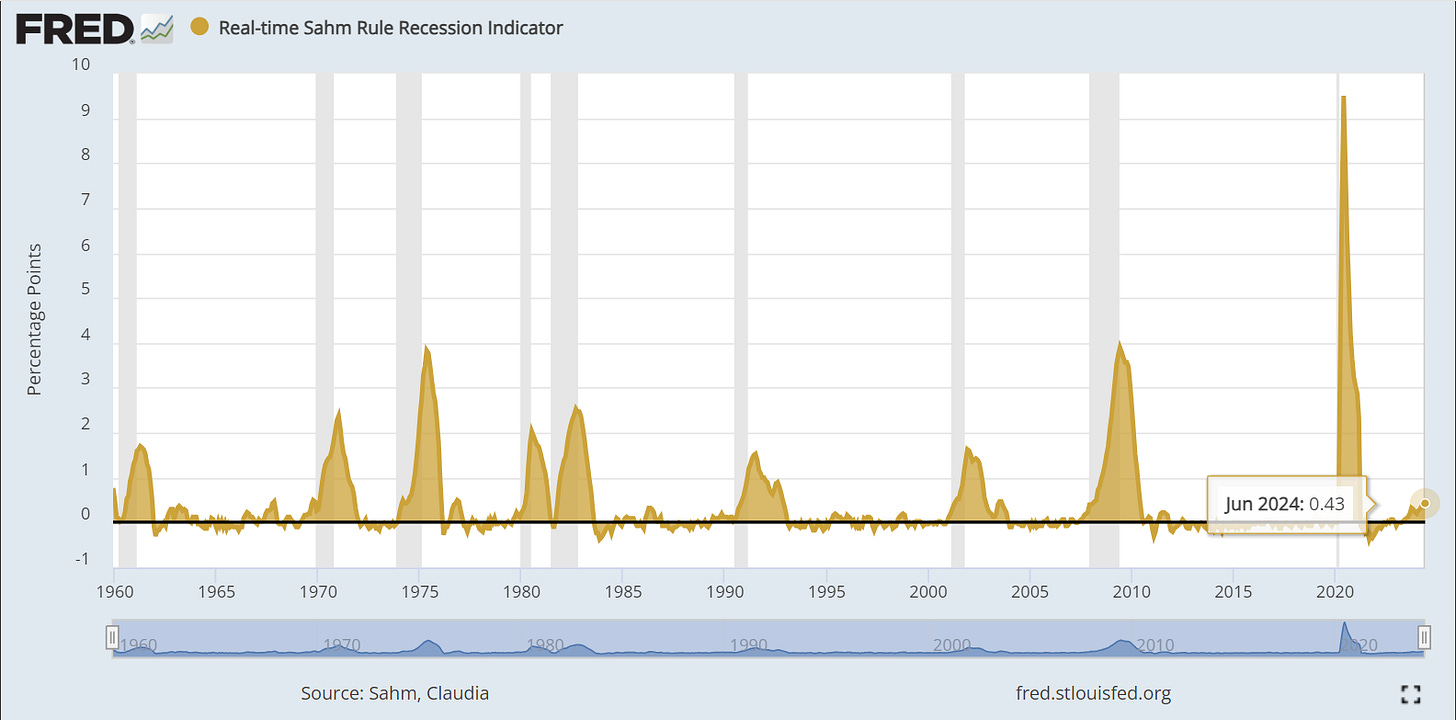

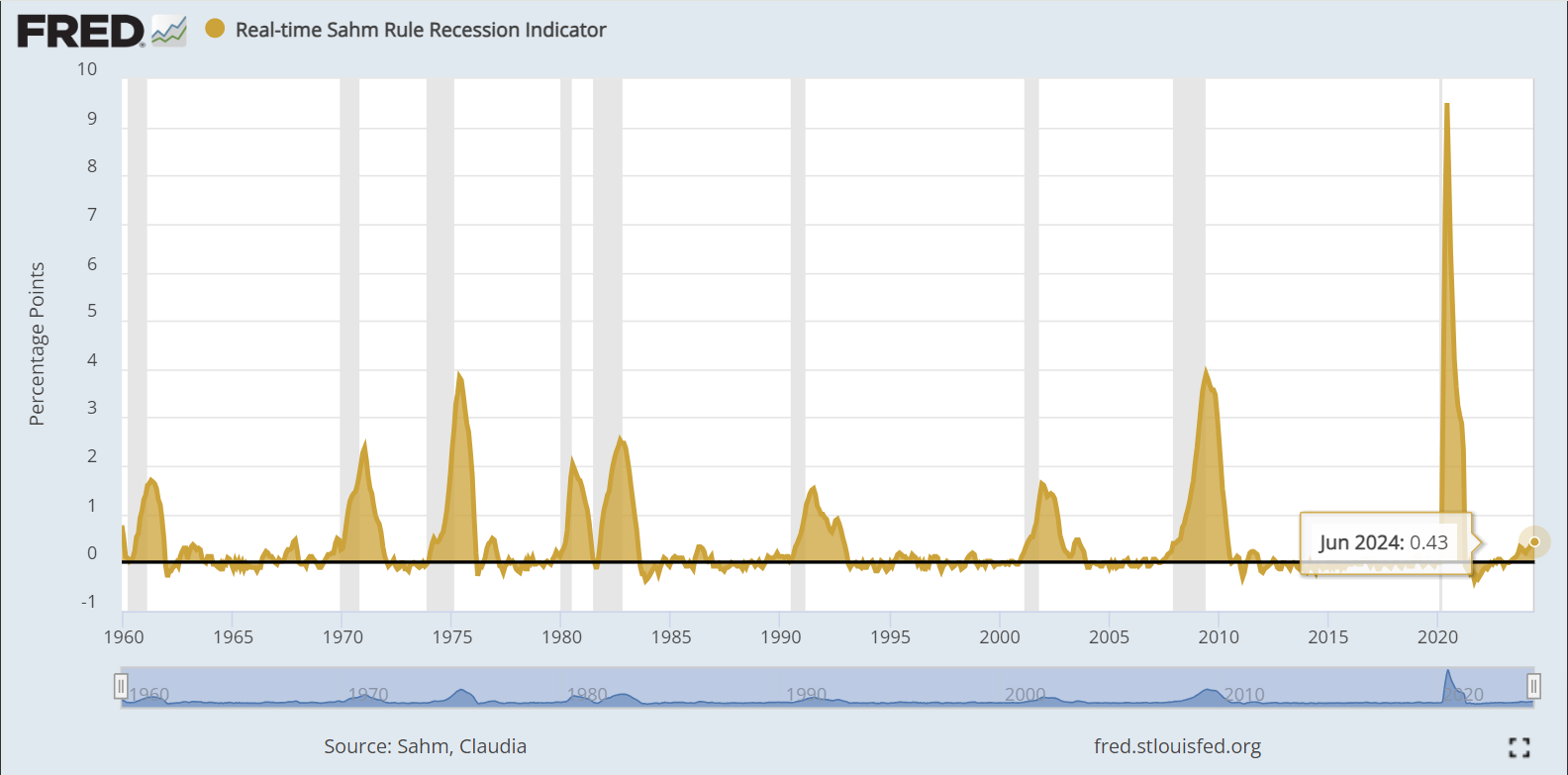

The most notable point of the employment report: unemployment rate rose to 4.1% (> forecast: 4.0%).

With June unemployment rate at 4.1%, the Sahm Rule recession indicator has risen to the threshold 0.43% - very close to the recession alert level (0.5%)

And the Sahm Rule labor recession indicator has never wrongly predicted a recession!

Because the meaning of the Sahm rule is not in the 0.5% number but what it reflects:

“… the growth momentum of unemployment (the increase in the 3-month average unemployment rate) fast enough for unemployment to escalate leading to recession!"

Read more: How to calculate and the meaning of the Sahm Rules recession indicator.

The labor market is still described by the Fed as "normalizing", but in reality economists all know that the labor situation is deteriorating:

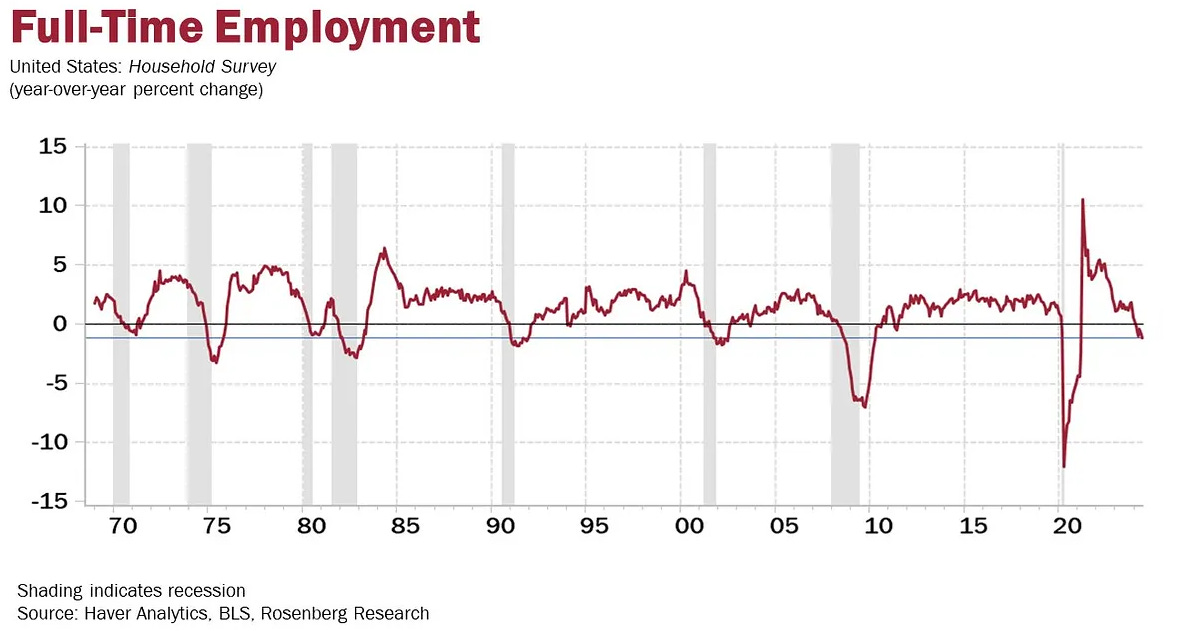

US payrolls in June increased +1.7% y/y - equivalent to pre-Covid growth levels:

=> Evidence that the labor market has officially normalized!

But the actual structure of the labor market has become worse than before:

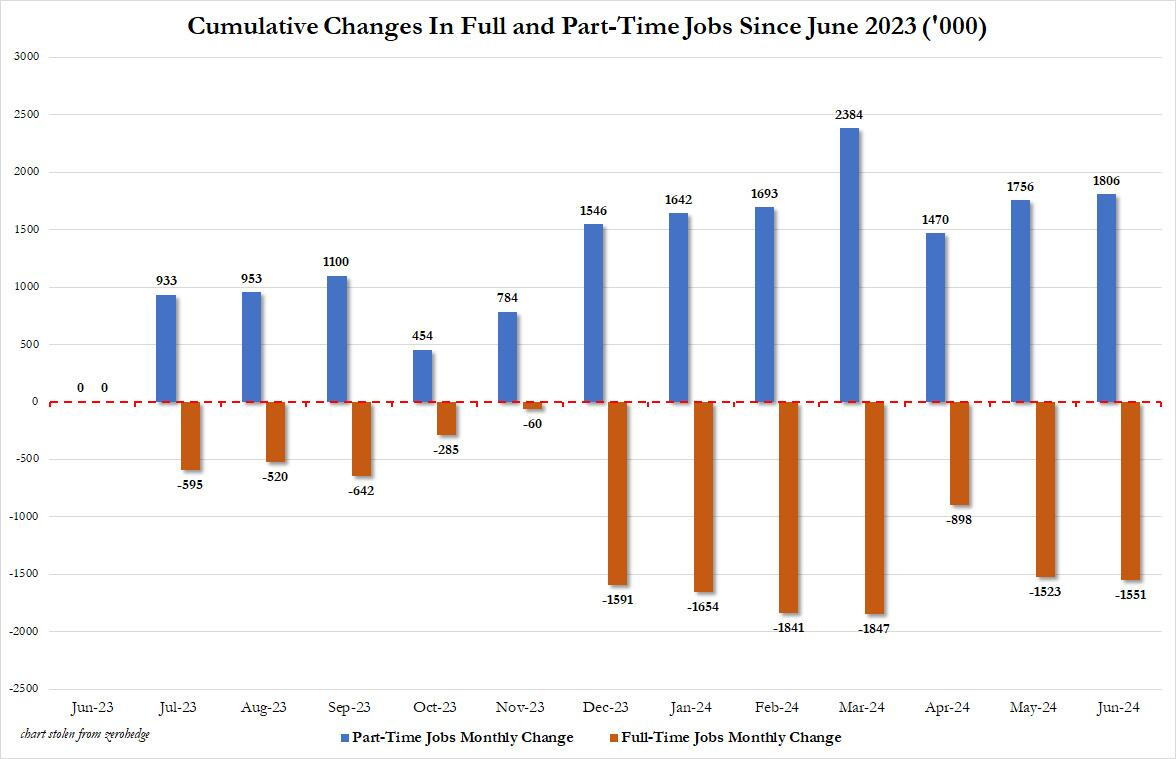

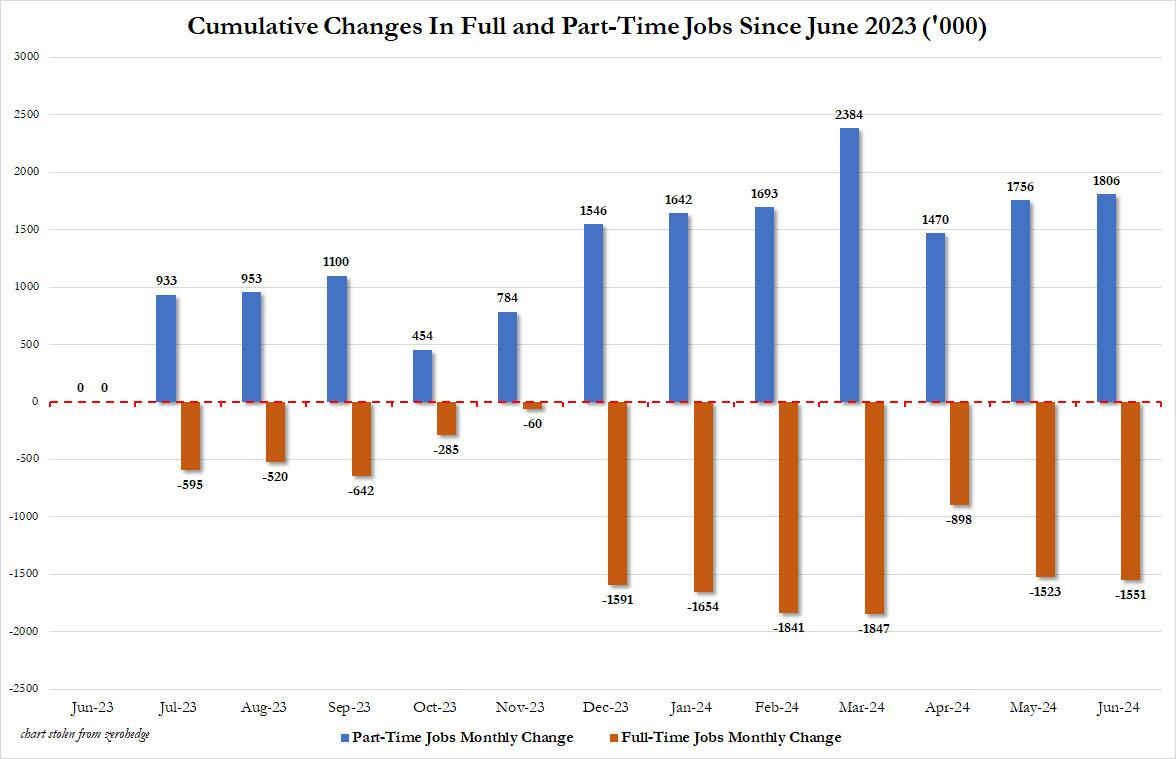

… with over -1.5 million full-time jobs lost in the past 12 months:

… equivalent to negative growth (-1.2% y/y) of total full-time jobs in the market: only occurs during recession periods!

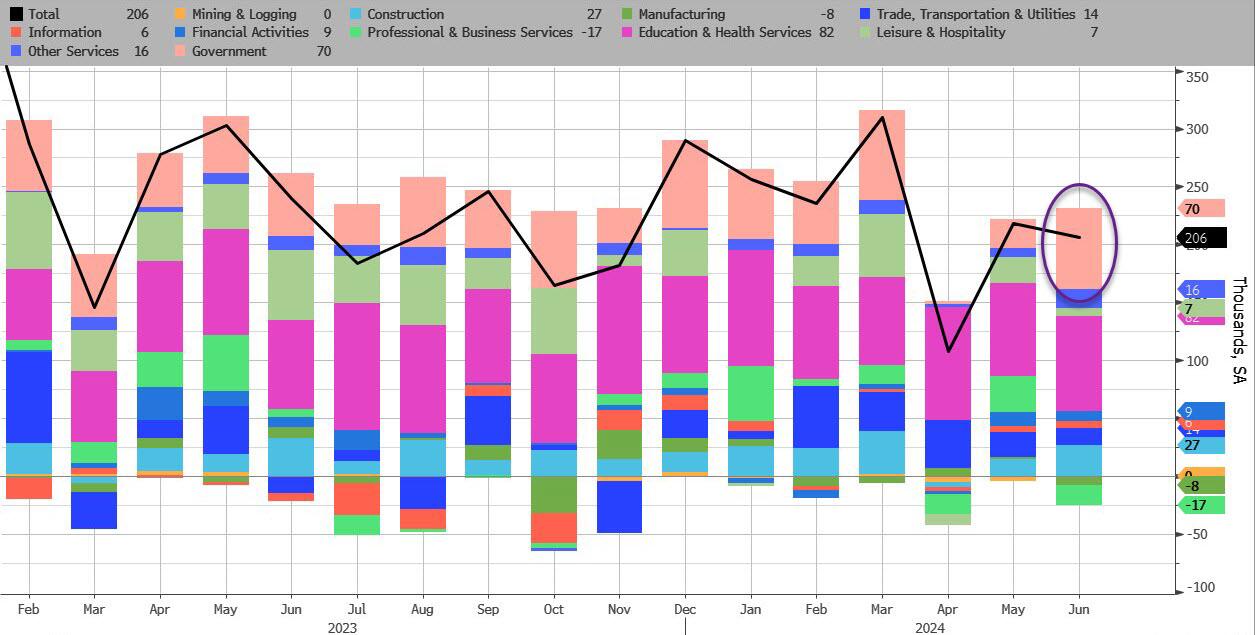

Over ⅔ of new jobs created in June come from the government sector (government) and government-subsidized social welfare services (healthcare and education):

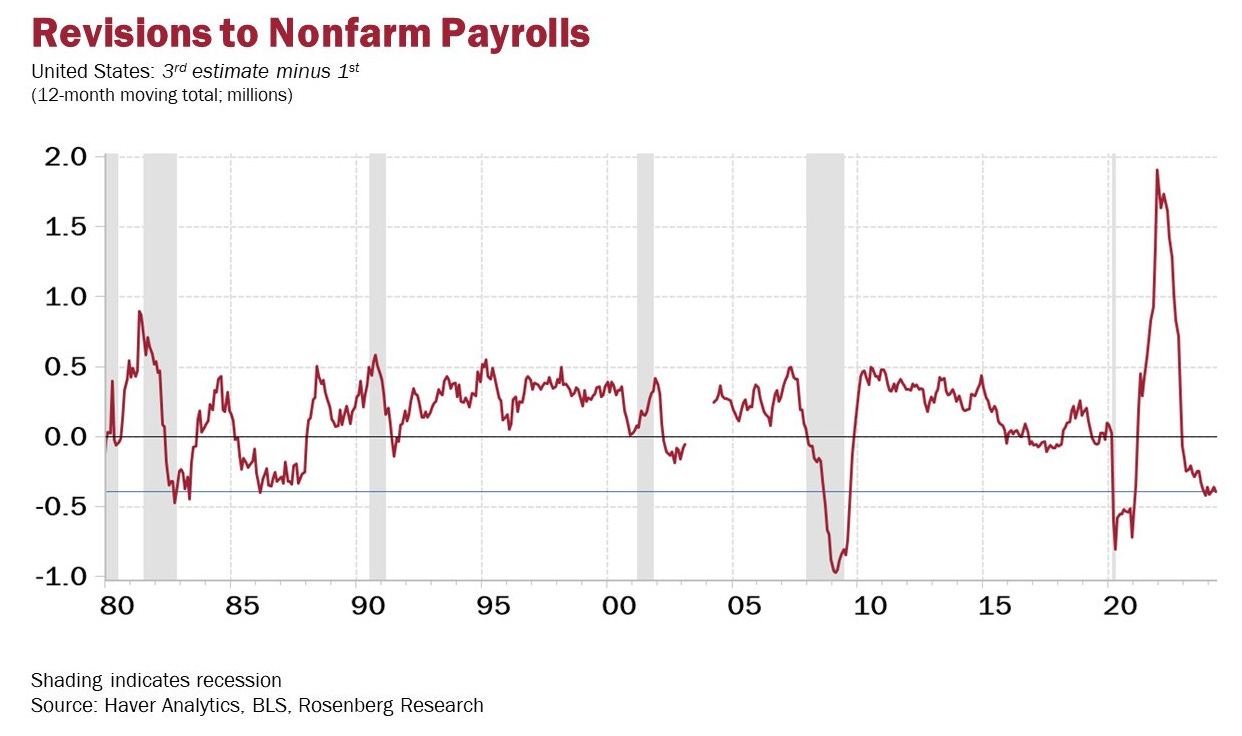

Downward revision -111,000 jobs for April-May/2024 exacerbates the total downward revision of payrolls in the most recent 12 months…

… and also equivalent to the job downward revisions of all previous recessions!

Therefore, the above employment data is equivalent to previous recession periods:

The difference is that in previous recession periods, the number of part-time jobs did not grow too high to maintain people's income as currently.

This is the main reason why this prolonged Fed rate hike cycle has not yet led to a recession.

II. Recession or soft-landing: which direction for the Fed?

» II.1. Recession and the Fed's soft-landing expectations

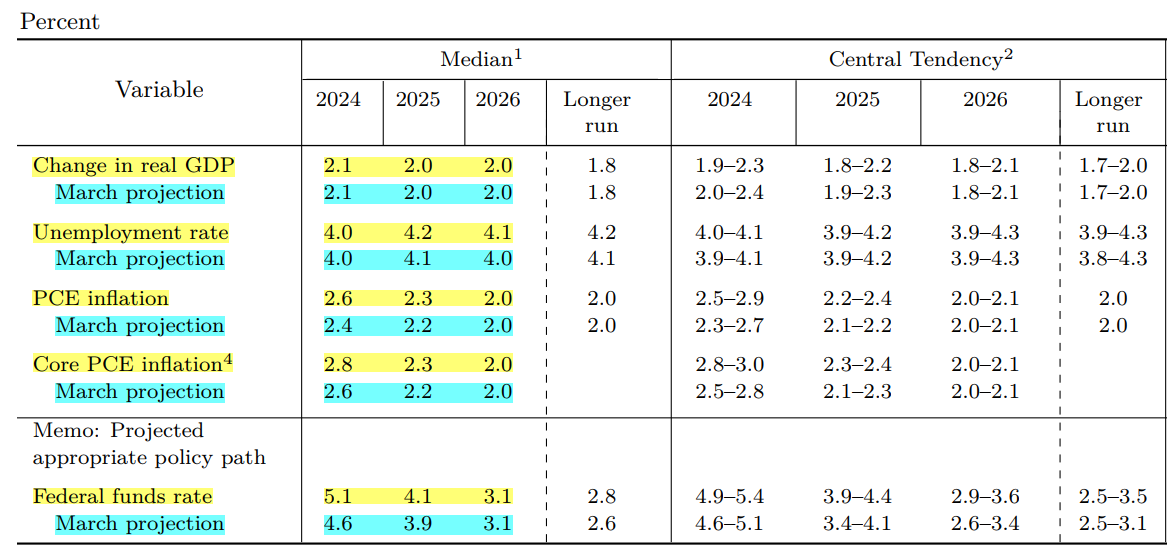

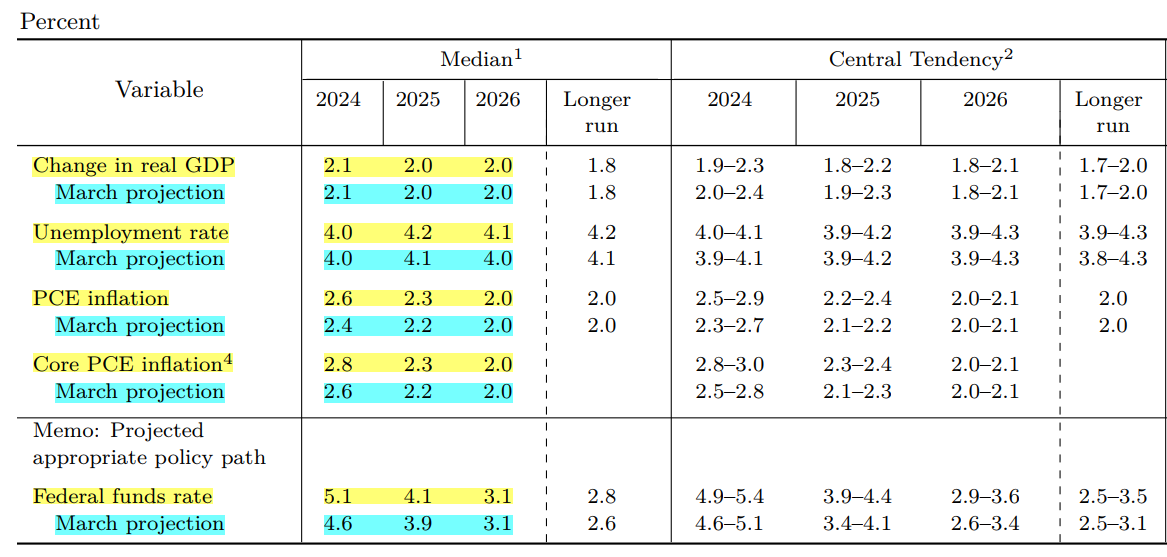

Remember in the June FOMC, the Fed's economic scenario projection was:

Headline PCE 2.6% y/y, Core PCE 2.8% y/y, …

a soft-landing scenario: GDP growth +2.1% y/y | unemployment rate 4.0%

…. by the end of 2024!

But in the first half of 2024, what does the Fed have?

Headline and Core PCE growth (May) both reached 2.6% y/y

⇒ better than the Fed's projection, and PCE is still on a downward trend.

Unemployment rate rises to 4.1% => higher than the Fed's end-of-2024 expectation (4.0%).

Q1 2024 GDP only increased +1.4% (Q/Q - annualized) - lower than Fed's projection (+2.1%)!

=> If the disinflation trend continues, the Fed will exceed the inflation target for the end of this year… but will the Fed achieve soft-landing?

The answer is there might not be a Soft-landing! Due to 2 main reasons:

Reason 1: Inflation, GDP growth, unemployment rate and Fed's interest rate policy form a “balanced model”!

The equations in that balanced model are quite complex, but the theory behind it is as follows:

High interest rate policy => people shift from consumption to saving

=> Consumption decreases => inflation decreases

=> Economic growth weakens (due to decreased consumption) => Unemployment rises sharply (due to businesses scaling back operations) !

Soft-landing only occurs if: inflation decreases => economic growth decreases but slowly + unemployment increases but slowly

and economic growth remains above 0% + unemployment does not rise too high (<5%).

The Fed hopes for soft-landing because it believes inflation will decrease fast enough for the Fed to cut interest rates before GDP growth turns negative and unemployment rises >5%.

But in just the first half of 2024: the above economic variables have already exceeded the balanced levels for the trio: inflation - GDP - unemployment that the Fed projected!

And according to the standard economic balance model:

High interest rates will keep inflation trending down in the second half of this year…

… but also means: GDP growth will go even lower:

FYI: A series of Fed research agencies have simultaneously lowered their forecasts for Q2/2024 GDP:

New York Fed: down from +1.93% to +1.79%

Atlanta Fed: down from +2.2% to +1.5% (a fairly large decrease)

Saint Louis Fed: down from +0.76% to +0.68%

and unemployment will continue to rise!

Reason 2: The service sector is declining, causing labor demand to decrease

Perhaps few people notice, part-time jobs (which drove payroll increases last year) mostly come from the service sector.

And service PMI has officially entered contraction territory!

=> In the near future, the unemployment rate may really rise much higher than the current 4.1% – as service sector inflation decreases!

» II.2. Fed's direction: may cut interest rates in September!

In a previous podcast, Viet Hustler emphasized,

if the labor report worsens or inflation improves, the Fed may cut interest rates starting in September.

otherwise, the Fed will wait until November to cut interest rates.

With the PCE report better than the Fed's projection + labor report somewhat worsening (especially unemployment rising to 4.1%): the Fed is likely to cut interest rates in September!

III. Recession or Stagflation?

» Another scenario for the US economy:

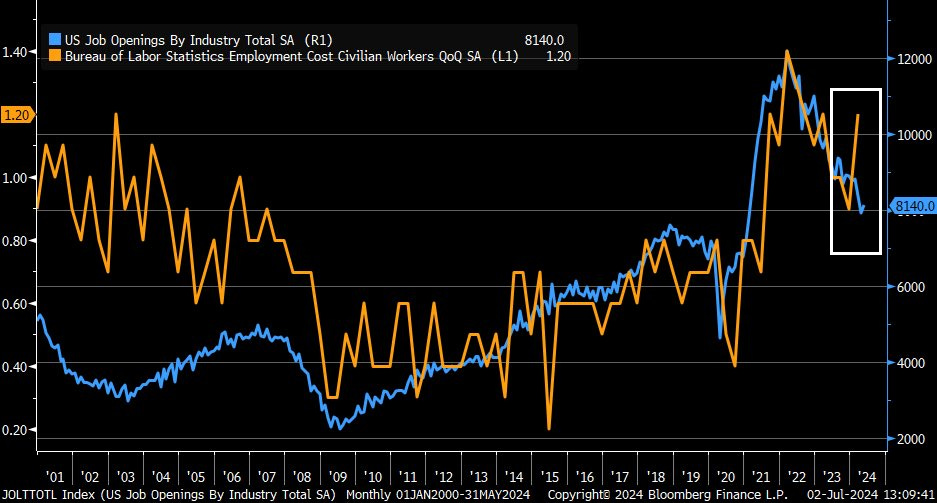

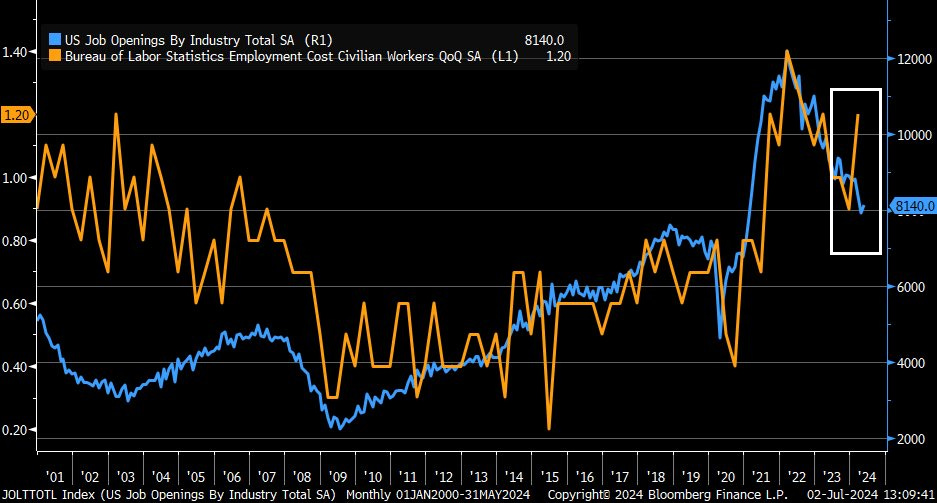

Usually: Number of job openings by businesses (job openings) gradually decreasing is usually accompanied by Labor costs also decreasing accordingly.

But in Q1/2024, labor costs still increased despite hiring cooling off:

And high labor costs ~ high wage increases: could prolong consumer spending growth and inflation.

Economy slows but does not contract (GDP growth still >0%) + prolonged inflation + unemployment on a high growth trajectory

⇒ Is this scenario familiar to Viet Hustler readers?

Not wrong: that's the scenario of Stagflation!

However, Viet Hustler has also emphasized:

Stagflation is only concerning due to the trio: stagnant economic growth (stagnated) + persistent inflation + rising unemployment “over a long period” exhausting the economy!

⇒ Therefore, stagflation cannot be identified “in the short term”.

But if inflation remains high for a longer period:

long enough for GDP growth to fall below the 1% threshold long-term and unemployment to rise to the 5% threshold…

… the Stagflation scenario could fully occur!

» So what factor could cause inflation to persist like that?

The answer lies in simple economic theory:

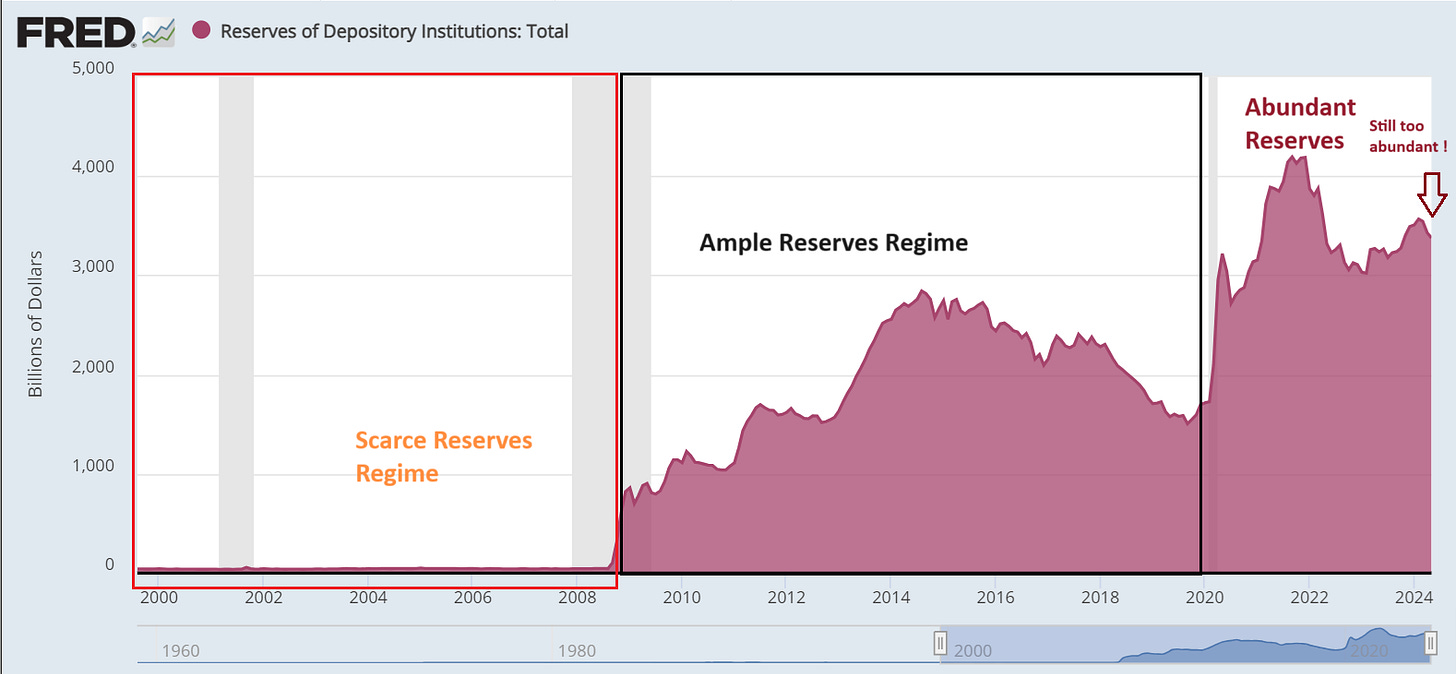

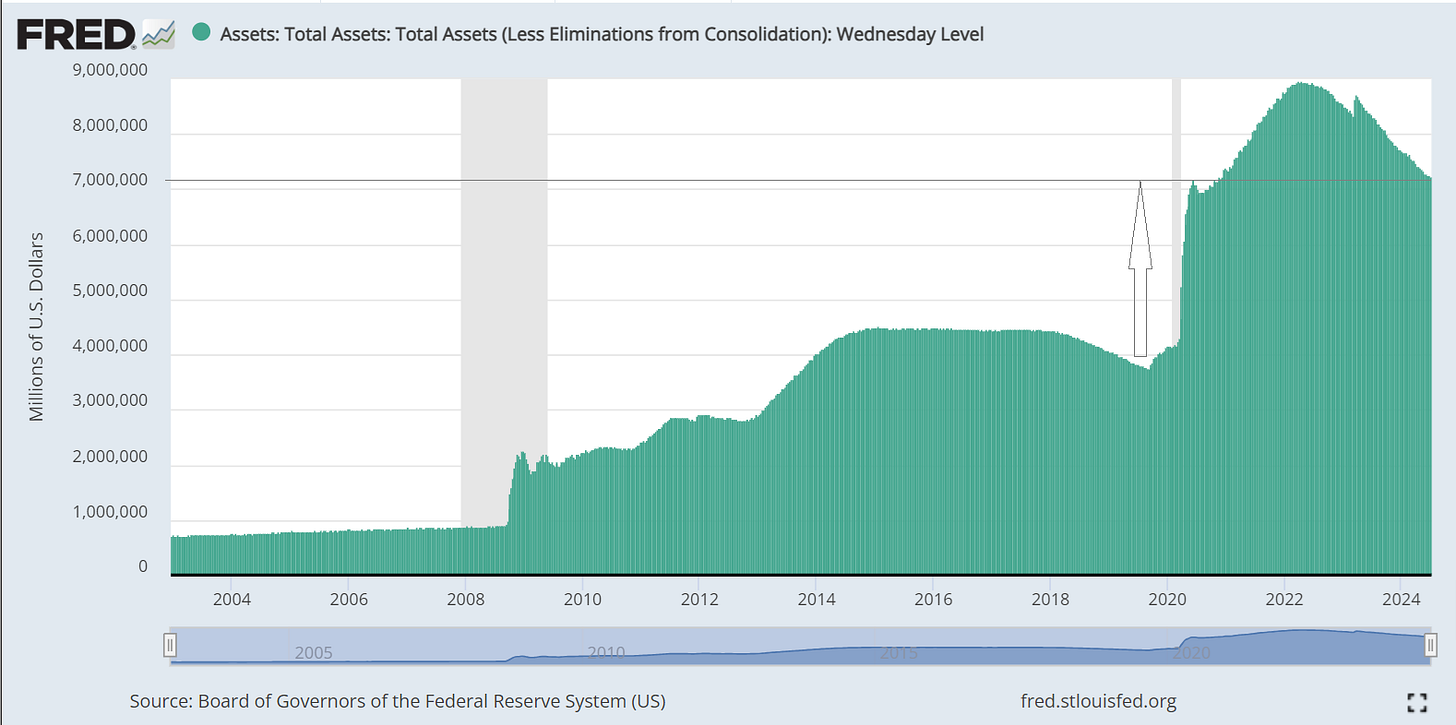

… Because market liquidity is still abundant…

And abundant liquidity & money supply is the cause of every inflation cycle!

Evidence that liquidity is still abundant:

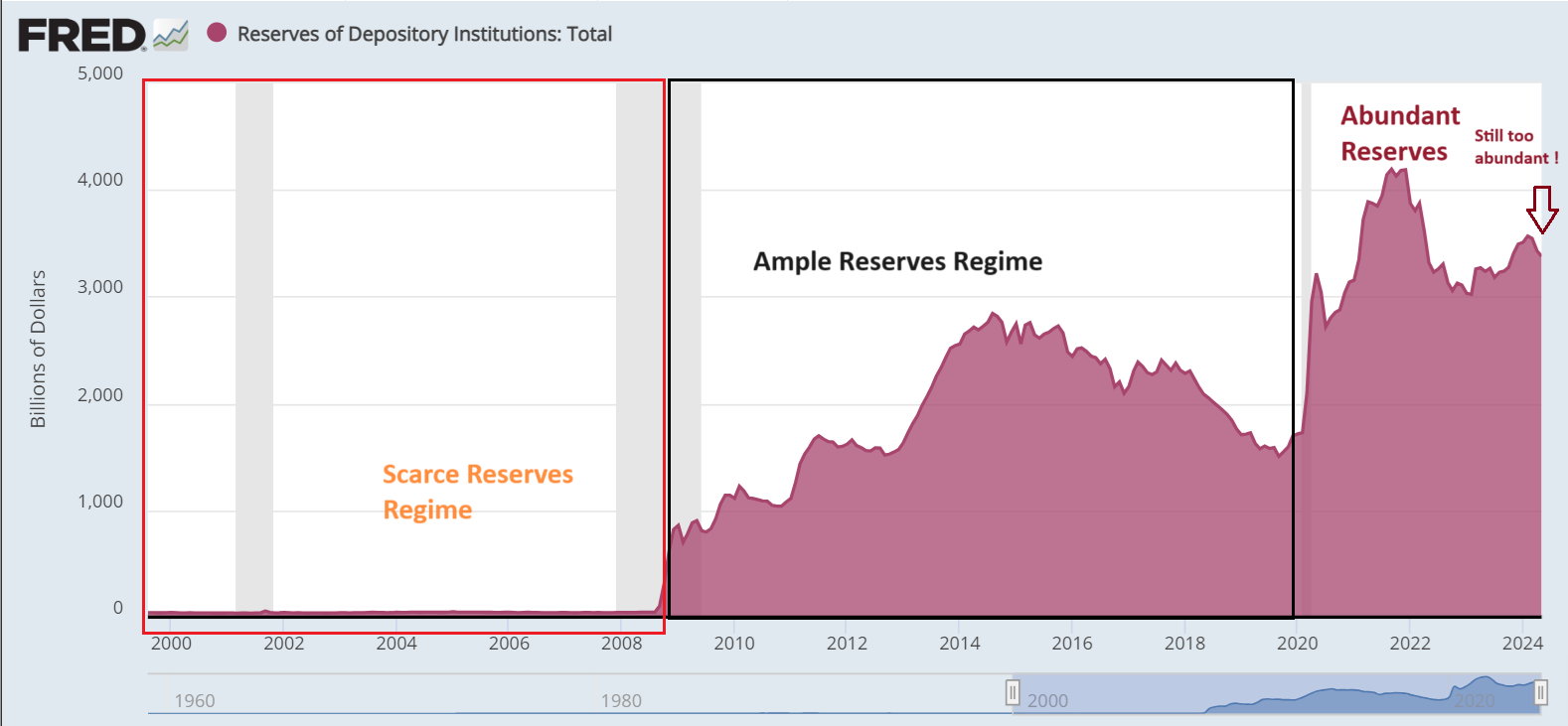

Banks' cash reserves at the Fed: although significantly reduced since the Fed implemented QT, still much higher than pre-Covid levels.

Read more: The relationship between the trio: inflation - bank monetary reserves - Fed's monetary policy

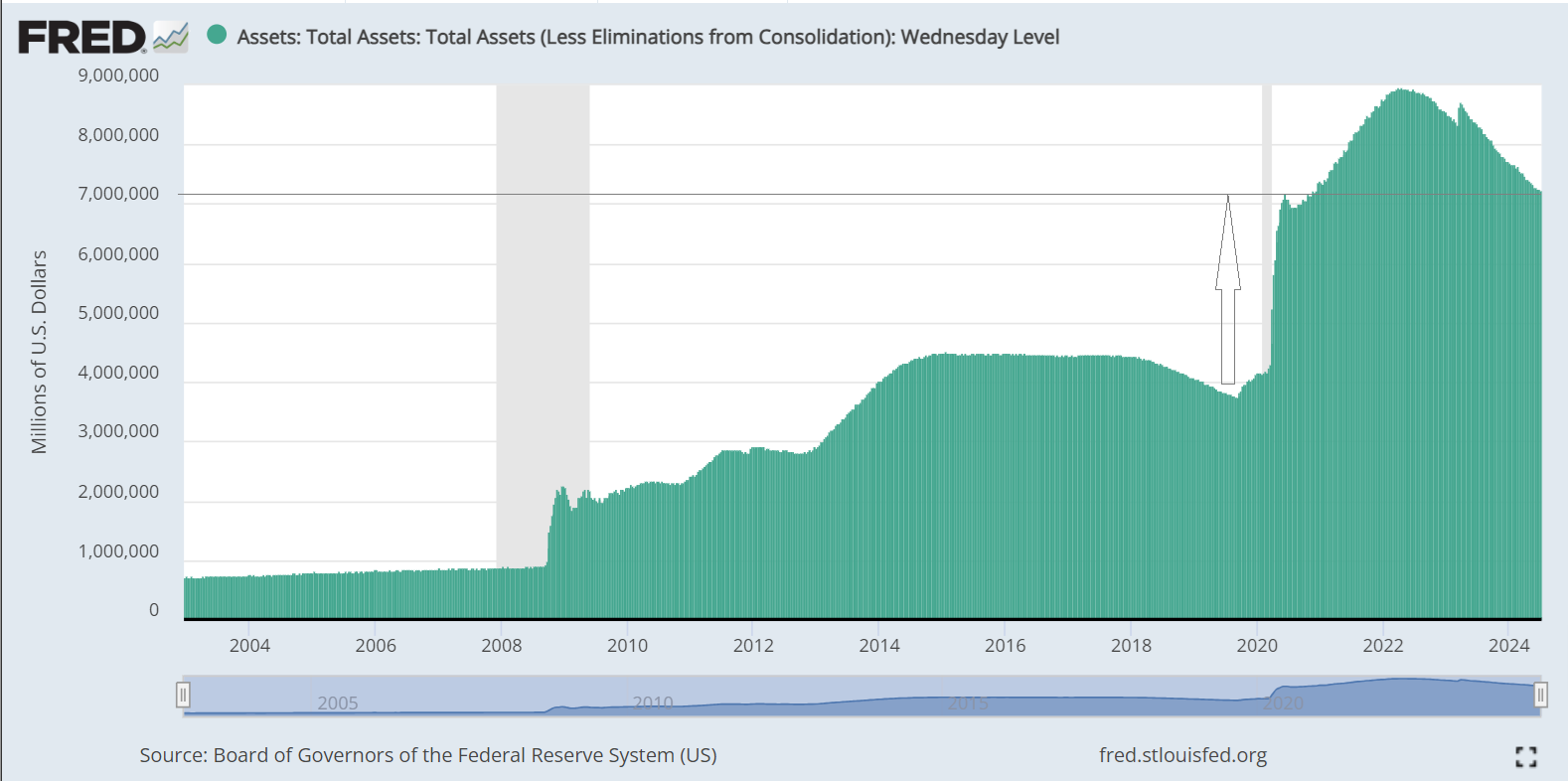

QT policy is still quite “superficial” as the Fed's balance sheet has shrunk but not back to pre-Covid levels.

The BTFP program that the Fed offers preferential loans to commercial banks has not been reversed,

… even banks are still delaying repayment to the Fed.

All the above issues reflect that market liquidity is still much higher than pre-Covid

=> Naturally, this will prevent inflation from returning to initial levels!

And the longer inflation persists, the higher the risk of stagflation for the economy!

CONCLUSION

Last week's economic data shows 2 prominent trends:

Economic activities are slowing down: especially the services sector is declining

this will help reduce the pressure of services inflation…

but it means that the growth of the US “services economy” will worsen!

The labor market has deteriorated markedly!

As the number of full-time jobs in the first half of this year has all decreased by a large figure compared to last year.

Unemployment rate 4.1% and is on an upward trend (as shown by the Sahm Rules indicator).

… even though payroll numbers are still increasing!

With the trio: PCE inflation (+2.6% y/y) + GDP growth (+1.4% Q1/2024) + unemployment rate (4.1%) developments outside the Fed's expectations in the June FOMC; very likely:

Fed will not achieve soft-landing as expected!

Of course, the Fed will face greater pressure to cut interest rates in September.

Therefore, the recession scenario for the economy is entirely possible: and could occur in the second half of this year or early 2025 (post-election).

However, all liquidity data shows: inflation may anchor higher than the 2% level for longer due to money supply still higher than the pre-Covid period. And if inflation doesn't decrease fast enough, but GDP growth weakens and unemployment rises high: Stagflation scenario for the US economy could also occur!

{kind=link}