Four decades ago, the Plaza Hotel in New York entered financial history. On September 22, 1985, the US government convinced the UK, Japan, Germany, and France to jointly depreciate the US dollar, to boost US industrial competitiveness.

Could this happen again? This idea has been causing endless buzz in financial circles since Trump was re-elected for his second term.

"There have been speculations about a new Plaza Agreement - named the 'Mar-a-Lago Agreement' - to depreciate the US dollar."

Indeed, it is very likely that such an agreement has been initiated, nurtured, and implemented by the top power trio in US financial leadership: President Trump, Treasury Secretary Bessent, and Chairman of the US Council of Economic Advisers (CEA) Stephen Miran.

In today's article, Viet Hustler will dive deep with you to analyze the following aspects:

Bretton Woods Agreement, Nixon Shock, and Plaza Agreement: Historical milestones shaping the modern global monetary order.

The Cost of the World's Reserve Currency Status: The economic challenges the US faces in holding the global central currency role.

Donald Trump's Economic Ideology and the Mar-a-Lago Agreement: A bold new approach to reshape the international financial order.

Implementation Steps of the Mar-a-Lago Agreement: Who is carrying it out, and the behind-the-scenes strategies. What is Trump's next step?

Can the Mar-a-Lago Agreement Succeed in This Era?: Analysis of the agreement's success potential in the current geopolitical and economic context.

1. Bretton Woods Agreement, Nixon Shock, and Plaza Agreement

1.1 Bretton Woods Agreement

As World War II was about to end, the United States emerged as a superior economic power, with most of the world's gold reserves concentrated in this country.

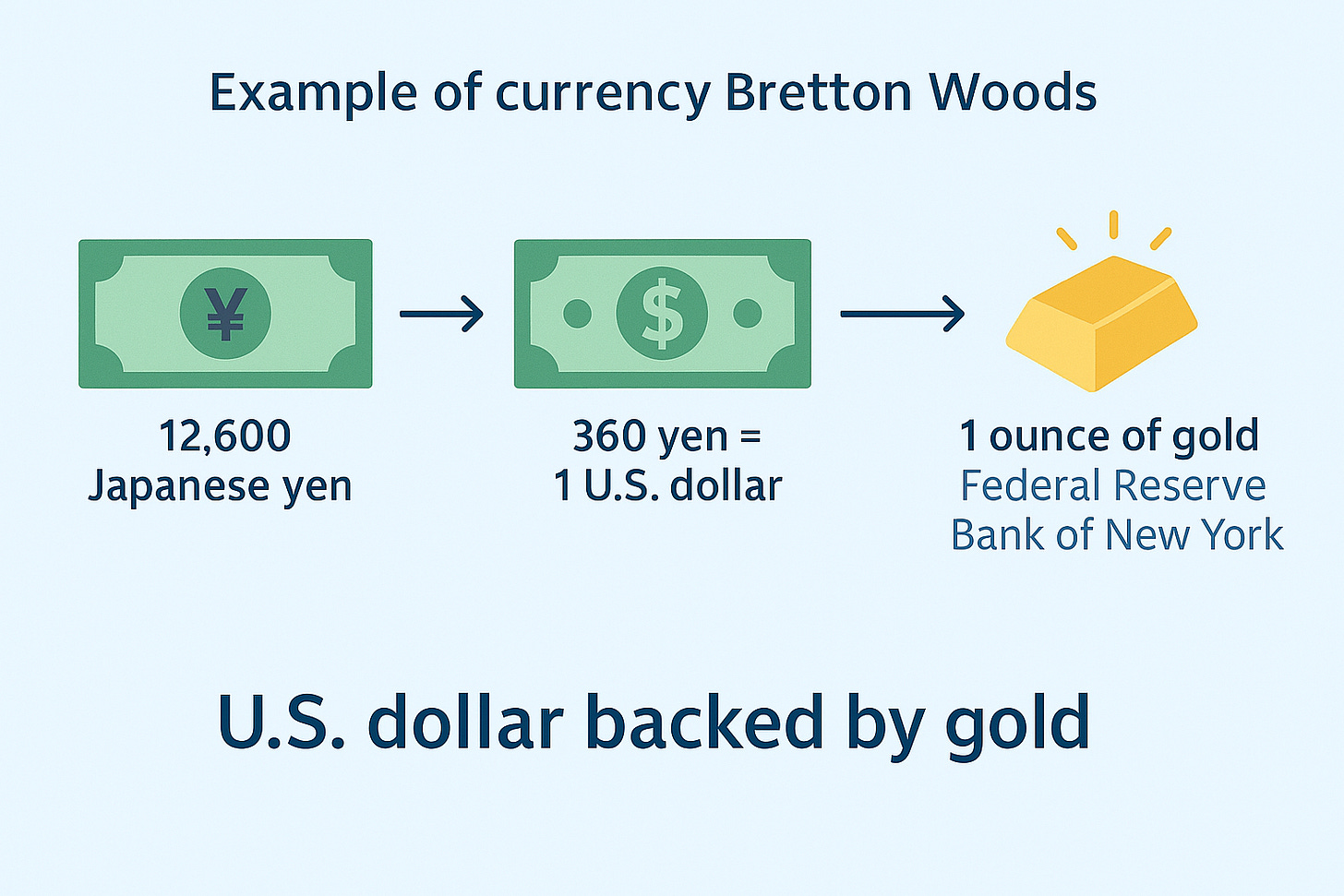

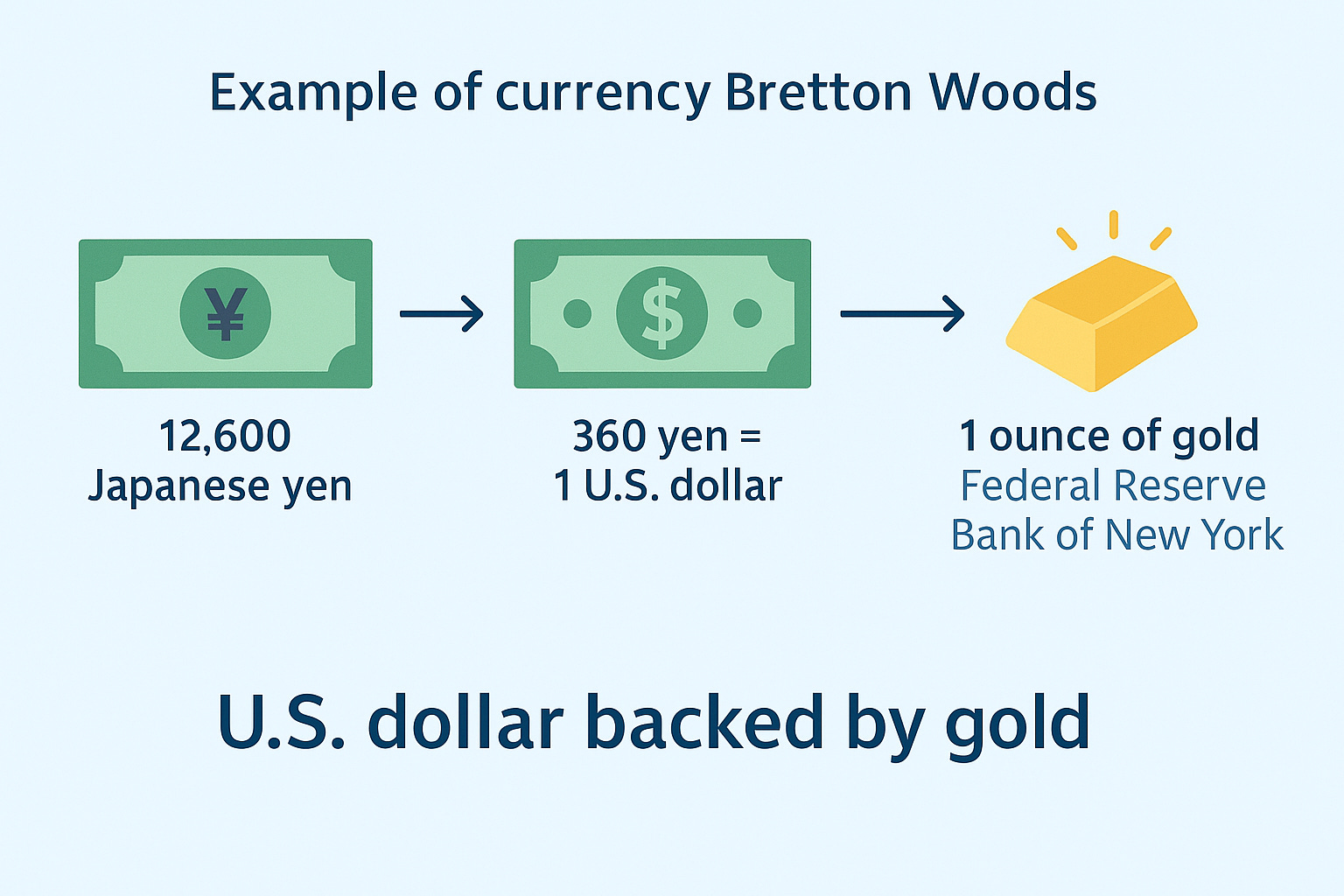

→ This facilitated the establishment of the Bretton Woods Agreement in 1944, whereby member countries' currencies were pegged to the US dollar, and the US dollar was pegged to gold.

→ The US dollar is the global reserve currency.

Example: In the Bretton Woods system, 360 Japanese Yen could be exchanged for 1 US dollar. Therefore, a Japanese person with 12,600 Yen could exchange for 35 US dollars. Then, the Bank of Japan had the right to take these 35 US dollars to the Federal Reserve Bank in New York to exchange for 1 ounce of pure gold from the US gold reserves.

→ The US Dollar is backed by gold

→ The convertibility of US dollars to gold acted as an 'anchor' limiting the amount of US dollars printed, to ensure the currency's value.

Overview: The world gave the US the right to lead the world out of World War II. Bretton Woods was not only a monetary system but also a tool for the United States to establish its economic dominance after World War II.

1.2 Nixon Shock

From the 1960s, the US spent heavily on:

Vietnam War

Social program "Great Society" of President Lyndon B. Johnson

→ To finance, the US borrowed debt and printed more dollars, leading to public debt soaring.

Other countries began to doubt if the US had enough gold to back

When the amount of circulating dollars far exceeded the gold reserves, countries began to lose confidence.

They rushing to exchange dollars for gold → “debt” in dollars exceeds US gold reserves → causing US gold reserves gradually depleting.

→ The US could not maintain the commitment to convert dollars into gold.

August 1971, President Nixon "temporarily" suspends dollar-to-gold conversion – a historic shock called Nixon Shock.

→ The Bretton Woods system officially ends in 1973.

In summary: Public debt increases → US prints money → loss of confidence in the dollar → massive gold withdrawals → Bretton Woods system collapses.

The Nixon Shock dealt a heavy blow to the world's confidence in the dollar, and opened a new era of monetary instability.

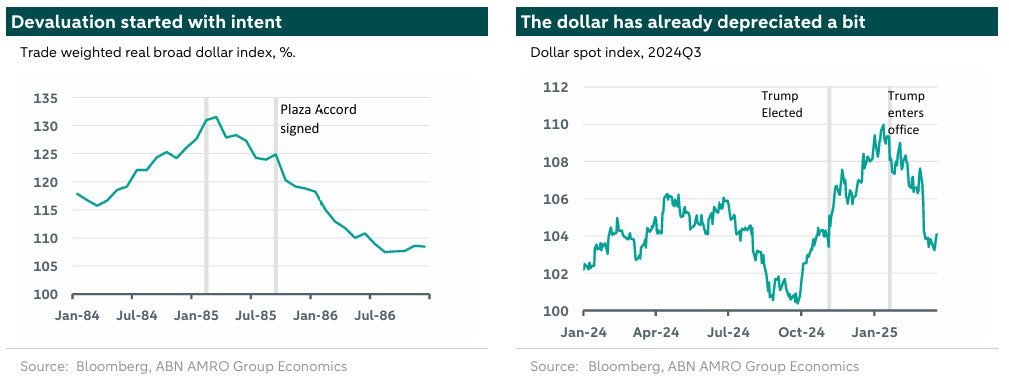

1.3 Plaza Accord

After the Bretton Woods system collapsed in 1971, the world entered a new phase with a floating exchange rate system.

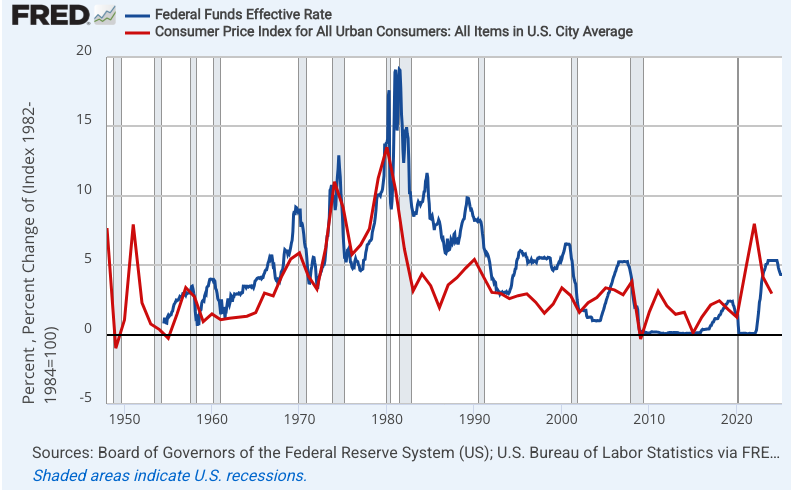

The 1970s witnessed a global inflation surge, partly due to skyrocketing oil prices after the 1973 and 1979 oil crises.

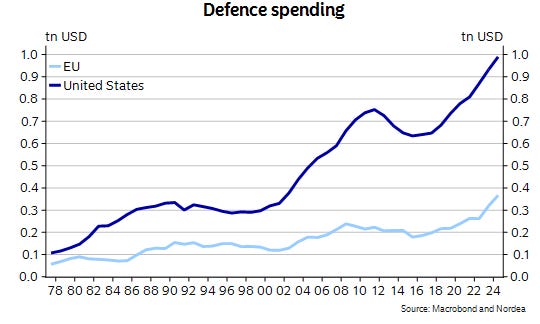

In the early 1980s, the US Federal Reserve (Fed)'s tight monetary policy aimed at controlling inflation, while the Reagan administration pursued "Reaganomics", including tax cuts and increased government spending, especially on defense.

→ The combination of tight monetary policy and loose fiscal policy created an environment of high interest rates and large budget deficits coexisting.

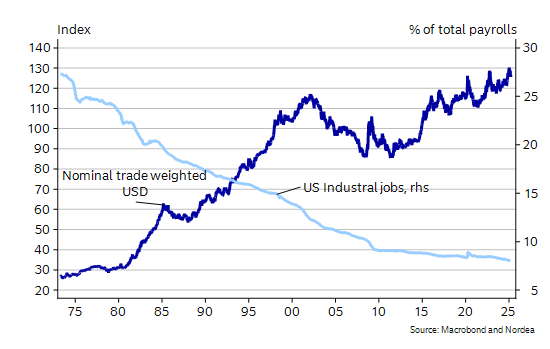

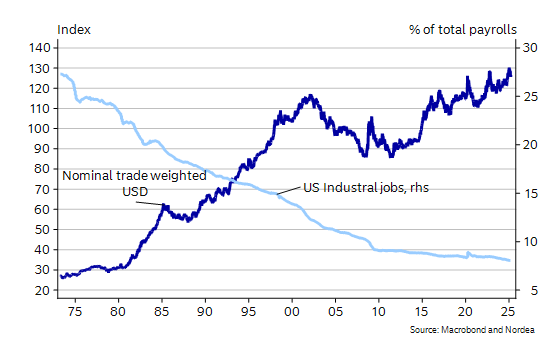

→ Strong appreciation of the US dollar.

→ Causing large US trade deficits, as US goods became more expensive for foreign buyers.

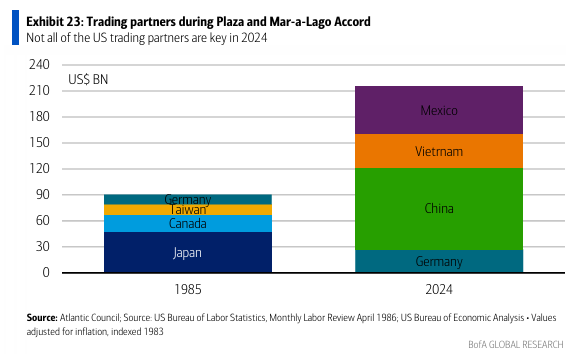

→ In response, in 1985, the world's top five economic powers (G5): US, Japan, Germany (West Germany), France, and UK signed the Plaza Accord in New York. This agreement aimed to depreciate the US dollar through coordinated intervention in currency markets, thereby reducing the US trade deficit.

The Plaza Accord, although successful in reducing the US trade deficit, also contributed to the formation of an asset bubble in Japan.

2. Petrodollar and the cost of the world's reserve currency status

2.1 What backs the Dollar - Bretton Woods 2.0

After the Bretton Woods system collapsed in 1971, the US needed a new "anchor" to maintain its global monetary hegemony. And it found it in oil.

In 1974, amid the oil crisis, the US and Saudi Arabia signed a foundational agreement:

Saudi Royal Family agrees to price and trade oil in US dollars (not exclusively) and reinvest in bonds to buy US weapons

In return, the US guarantees military and political security for this monarchy (unofficially)

When oil-producing countries accept payment in dollars, they unwittingly become "guardians" of this currency's value.

Oil exporting countries sell oil for dollars

→They reinvest this amount of dollars into US Treasury bonds

→ That helps the US finance budget and trade deficits

→ And continue unlimited spending, including global defense spending to maintain hegemonic position and be the world's policeman → increases pressure on public debt

→ In return, the US protects the geopolitical power of oil-producing countries

⮕ Petrodollar Cycle (Petrodollar Cycle) is closed, maintaining the US's hegemonic status.

This creates a cycle in which demand for the US dollar is maintained, and the US can finance its budget and trade deficits.

→ It also allows the US to maintain significant influence over the global energy market and use oil as a geopolitical tool.

This agreement quickly spread to the entire OPEC bloc. Since then, every country needing oil is forced to hold US dollars, turning the greenback into a global means of payment – a new version of Bretton Woods 2.0, no longer pegged to gold, but pegged to "black gold" – oil.

This is the foundation of the Neoliberal world order led by the US from the 1980s to the present, including:

Free trade (reducing tariffs) - however many countries implicitly apply

Free international capital flows,

Flexible exchange rates, no longer pegged to gold,

A global order revolving around the dollar and US influence.

In a world where energy is the lifeblood of the economy, oil naturally becomes "black gold", and the US dollar, dominating global oil transactions, has cleverly turned this "black gold" into an "anchor" for its empire.

2.2 The cost of the world reserve currency status

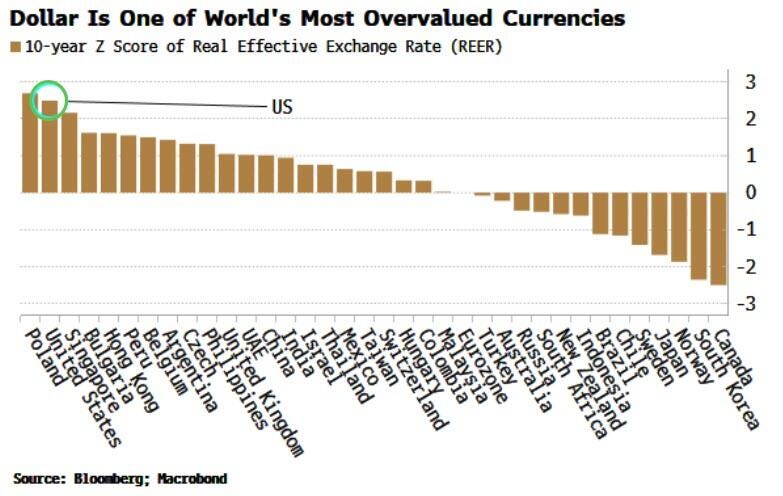

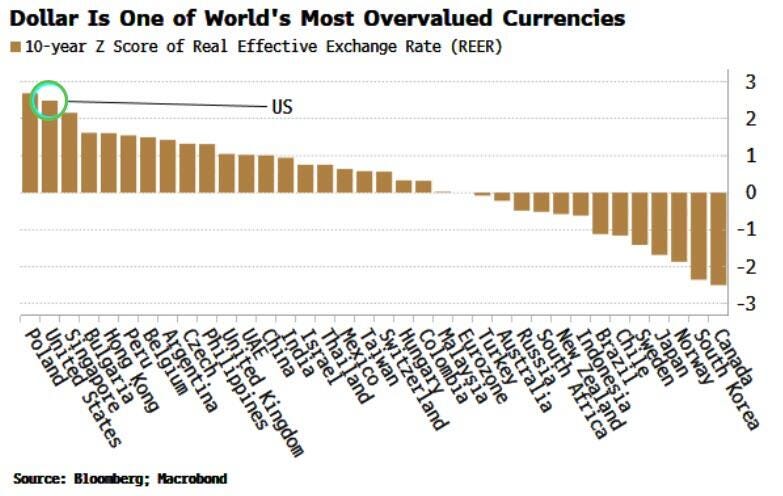

The status of the dollar as the world's leading reserve currency is often called the “exorbitant privilege” (exorbitant privilege) of the United States.

Former French Finance Minister Valery Giscard d’Estaing

The whole world needs dollars for trade and reserves

→ The dollar is used to buy oil, international payments, and as reserve assets for central banks.

→ That means other countries are forced to hold dollars for trade and finance.

But dollars don't naturally appear abroad. Basically, countries around the world only have three ways to obtain US dollars:

→ The US must "pump" dollars into the world through:

Fiscal deficit policy from the US

When the US government spends more than it collects – for example, defense spending, subsidies, relief, economic stimulus, etc.

→ They issue bonds.

→ International investors buy these bonds with dollars → dollar flows abroad, in return the US receives goods, services, and financial assets.

→📌 Strategic role: Budget deficit helps the US “export” dollars – and maintain global demand for USD.

Borrowing through currency swap agreements between central banks

During crises (e.g. COVID-19), central banks outside the US severely short of dollars.

→ Then, the Fed opens “currency swap lines” (swap lines) for some close central banks – like ECB, BoJ, SNB.

💣 But this is a high-risk tool and politically suicidal:

Countries cannot take initiative, but must depend on the goodwill of the Fed. Over-dependence easily leads to currency crisis issues

Swaps are only temporary, usually limited to crises.

If too dependent, a country loses monetary autonomy.

Export to the US – exchange goods for dollars → Earn from trade surplus with the US (and this is the main way) → Trade balance deficit

→ To maintain abundant dollar supply for the international market, the US must accept large trade deficits.

→ Persistent trade deficits for decades to maintain monetary hegemony.

→ Cheap goods from all over the world flood into the US, in exchange for dollar bills accumulated by other countries.

Example: China sells electronics, Mexico sells cars, Vietnam sells textiles – all receive USD and hold it as foreign exchange reserves.

1 strong dollar = Cheap imports, but harmful to exports

Power paradox: The US must... incur losses to maintain dominance

➡️ This is the price to pay to:

Keep USD always used and stored globally

Maintain international financial hegemony

Dominate global payments, investments, and reserve assets

IN SUMMARY, the US not only imports goods – the US exports dollars and influence.

2.3. Wealth inequality

Strong Dollar (USD ↑) → ✅ Attracts global capital flows

However, this capital mainly does not flow into manufacturing or basic technological innovation sectors, but mainly into financial assets - stocks, bonds, real estate - causing the economy to become increasingly financialized.

→ Increases the gap between "Wall Street" (finance elite, speculation - top 1% of America) and "Main Street" (real economy, workers, manufacturing businesses - middle class, American workers accounting for 90%).

3. President Trump's perspective

Economic Nationalism

Neoliberal order - neoliberalism (1980s-2020s) promotes global trade, but weakens the US

Lost 2.5 million jobs due to 'China manufacturing shock'

Fragile supply chains

Strategic industries leaving the US

Wealth gap → Middle class collapse (Trump's main voter base)

Trump wants a weaker dollar = Stronger America, in terms of:

Control currency manipulation:

The US suffers when countries deliberately keep their currency weak to maintain trade surpluses.

Hoarding dollars makes their goods cheaper, while American goods become more expensive.

China was once a major manipulator, but has intervened less recently.

Quick remind: In 2015, China devalued its currency, leading to a sell-off in EM markets

Reviving domestic manufacturing and creating more jobs for the American Dream

Trump believes the American Dream is fading because a strong dollar is destroying U.S. manufacturing, killing high-paying blue-collar jobs. The dollar's status as a reserve currency encourages investment into the U.S., making domestic manufacturing uncompetitive.

When the dollar is weak, American products are easier to export, thereby stimulating demand and creating jobs in key export industries.

For example, the dollar's depreciation helped the U.S. auto and computer manufacturing sectors grow, creating thousands of new jobs. This also helps reduce the unemployment rate and revive domestic industries.

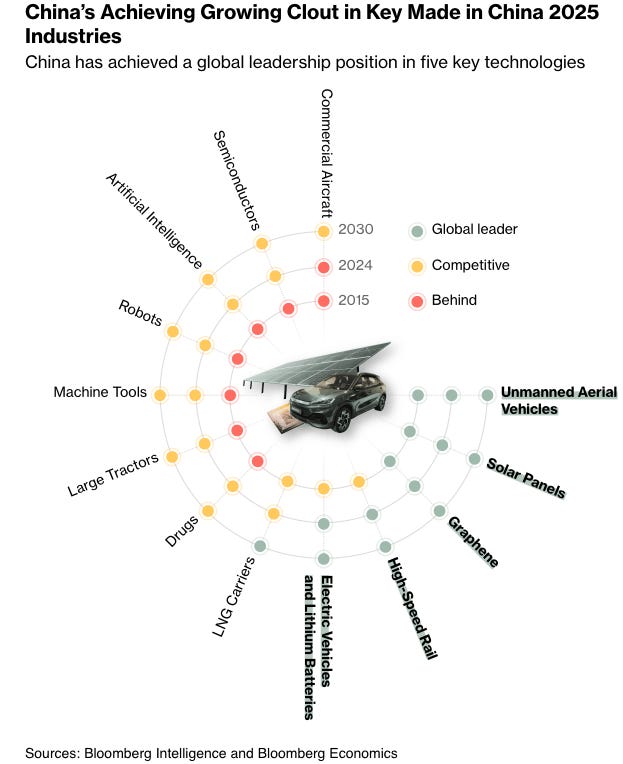

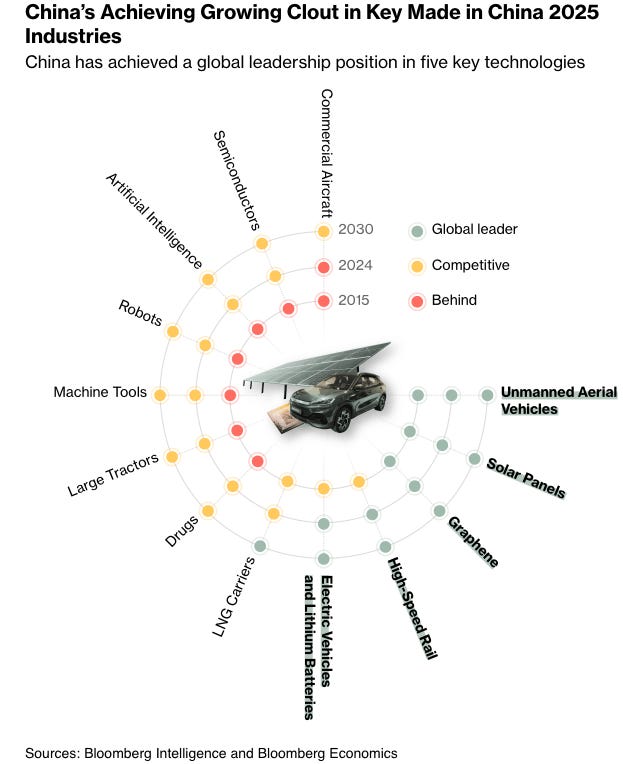

Reviving and developing key industries

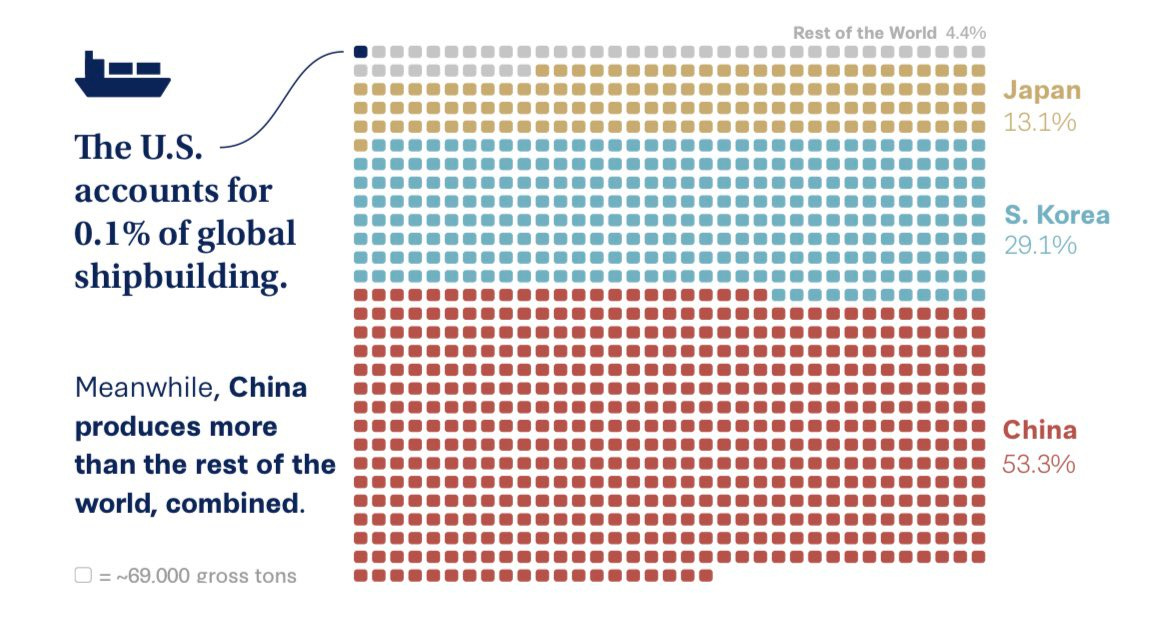

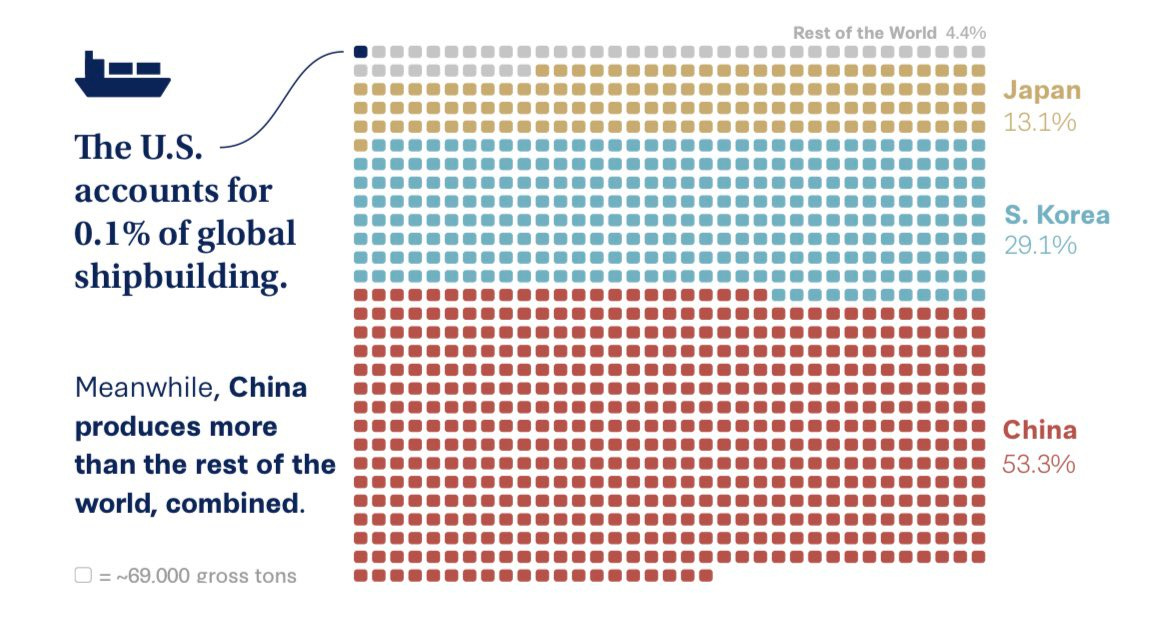

⚓ China builds 1,000+ ships/year

🇺🇸 America builds <10

→ Absence of industry means absence of autonomy, the nation declines

Reducing the trade deficit

A weak dollar also helps reduce the U.S. trade deficit. When the currency depreciates, U.S. export goods become more attractive to other countries, thereby boosting exports.

In summary, Trump's 'America First' ideology, combined with protectionism and unilateralism, has created a completely new approach to international monetary policy."

4. Agreements Plaza Mar-a-lago

OBJECTIVE: America devalues the dollar while allowing it to maintain its status as the world's reserve currency

Name: The term "Mar-a-Lago Agreement" originates from the fact that many informal meetings between former President Donald Trump and international leaders took place at Mar-a-Lago resort which he owns - a symbol of Trump's personal power. Notably, the meeting with Chinese President Xi Jinping in April 2017, where the two sides discussed trade and geopolitical issues, or most recently the golf trip of the Finnish President this March. Some analysts believe Mar-a-Lago has become the "backyard" for important negotiations, and if there is a new international agreement promoted by Mr. Trump - similar to the 1985 Plaza Accord - then Mar-a-Lago is very likely to be the symbol representing the formation of that agreement.

The Mar-a-Lago Plan was proposed by Stephen Miran, currently Chairman of Trump's Council of Economic Advisers, in a report “A user’s guide to restructuring the Global Trading System” last November.

Bước 1. Giải quyết Khủng hoảng nợ – điểm xuất phát của cuộc chơi

→ Government spending is out of control. During the Biden era, primary spending reaches 34% of GDP (for social welfare, Medicare, interest costs, war support costs for Ukraine and Israel) - much higher than the historical average of 21% and on par with . Meanwhile, revenue remains around 18%.

The problem is not 'not enough revenue' – because the U.S. is at a historically fairly high revenue level.

“We don't have a revenue problem-we have a spending problem.”

U.S. Treasury Secretary Bessent

→ The solution is not a European-style austerity shock, but gradual contraction. → Trump does not aim to cut people's welfare, but the bureaucracy: eliminate waste and bureaucracy; end “middlemen” for contractors; and move surplus labor to the private sector-through ambitions to cut cumbersome regulations (deregulation) and loosen business conditions to be more favorable for enterprises.

→ DEPARTMENT OF GOVERNMENT EFFICIENCY - Department of Government Efficiency (DOGE) is established

“DOGE is our greatest hope to fix the bureaucratic system that is flawed and inefficient in running the country.”

BILL ACKMAN

Overview: At this step, we need to link to the following parts in Trump's long-term plan:

Because the government cannot cut welfare → must create new revenue sources → Tariffs (step 2)

Due to fast-maturing debt, high interest rates → must restructure maturities → Century bonds (step 4)

Because budget is locked → must create assets and liquid cash flow → National Asset Fund (step 5)

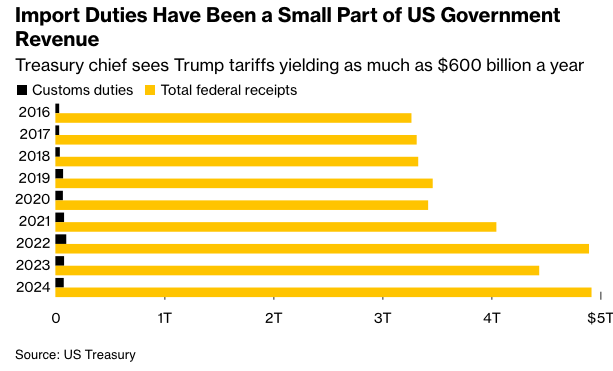

Bước 2. Thuế quan – công cụ đa năng: Từ đòn bẩy địa chính trị đến nguồn thu mới

📌 "I am a tariff man. I love tariffs. We get billions of USD from tariffs – and make China suffer even greater losses."

Trump, 2018

While traditional economists (Keynesian, Neoliberal) consider tariffs as trade barriers, Trump sees tariffs as:

Budget revenue source instead of domestic taxes (income tax)

Geopolitical weapon to pressure foreign countries

Tool to regulate trade balance

Negotiation leverage in FTA agreements and supply chains

Instead of increasing income tax – target imported goods

Government doesn't dare cut welfare (for political reasons).

→ Tariffs as revenue: Idea to establish an “External Revenue Service” (ERS) instead of “National Tax Service” - IRS is being considered.

→ Shift the burden to exporting companies (China, Europe, Mexico...) -a step in the right direction in terms of populism.

However, this import tax revenue may not be significant enough to offset the massive spending from the federal government

Use tariffs to force re-industrialization of America

Goal: force companies to shift production away from China (off-shoring) → to the US or friendly countries (friend-shoring) and near the South American axis, Mexico (near-shoring)

Tariffs create sufficiently large cost differential (145% tariffs on China) to force businesses to reconsider supply chains.

Imported goods become expensive → businesses are incentivized to open factories in the US to avoid tariffs.

Example: Foxconn, Samsung, TSMC have all invested in factories in the US during Trump 1.0 and continued to expand afterward.

With selective tariffs, Trump can protect steel, semiconductors, electric batteries, traditional energy from unfair competition.

→ Prepare for the global leadership race in future industries

Geopolitical weapon to pressure foreign countries

Countries that benefit from the US market must pay the price or meet conditions. If not – close the market, impose tariffs.

→ Tariffs as a bargaining stick: The US can force countries like Mexico (send troops to the border), China (reduce currency intervention), or NATO (increase defense spending, “pay the fair share”) to act if they don't want to suffer painful tariff levels.

Short-term shock – Medicine against speculative bubbles

→ Calculated side effects: Trump and advisors are not afraid of initial market shakes. A short-term shock can lower asset prices (against financial speculation) and promote re-industrialization, especially when the dollar weakens.

Want to change the economic structure → must shake the tree to make the leaves fall

Cannot protect Wall Street while expecting rural Ohio, Rust Belt to be revived.

A weak dollar + falling asset prices + growing domestic production are the three pillars of the “America Returns” strategy.

→ Trump is ready to let Wall Street “hurt a bit” – as long as Main Street can “come back to life"

Tariffs are "the most beautiful word in the dictionary", theo Trump – không chỉ vì chúng bảo hộ sản xuất nội địa, mà vì chúng còn là vũ khí mặc cả và nguồn thu mới cho ngân sách liên bang. Tóm lại, khi đặt nó vào bối cảnh khủng hoảng tài khóa (đã phân tích ở bước 1), thuế quan không còn là "hành vi bảo hộ ngu ngốc", mà là một dạng , according to Trump – not only because they protect domestic production, but because they are also bargaining weapons and new revenue sources for the federal budget. In short, when placed in the context of the fiscal crisis (analyzed in step 1), tariffs are no longer "stupid protectionism", but a form of "strategic revenue tax"

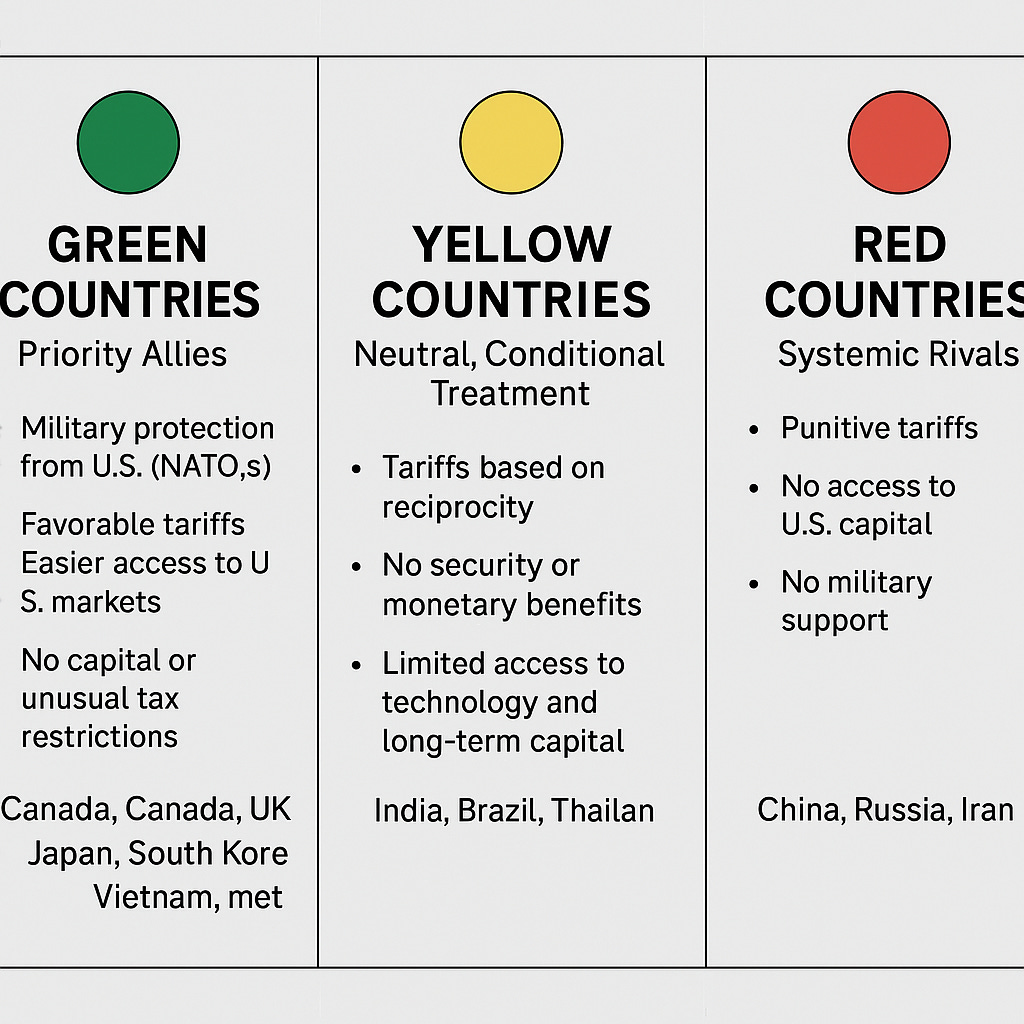

Bước 3. Đàm phán Đèn giao thông - Xanh Vàng và Đỏ

– increasing budget revenue, rebuilding industrial position, and restructuring the global supply chain. In the proposal of Miran and supported by Treasury Secretary Bessent, the new trade order is built no longer based on multilateral agreements full of goodwill and common rules (like WTO or TPP), but shifts to a classification model pragmatic and conditional – according to.

. 🟢

GREEN COUNTRIES – Priority allies

Countries that are close allies, strategic, or have key roles in the US supply chain.

Benefits: Military protection

from the US (NATO, AUKUS, etc.)Tariff preferences

, easier access to the US market

Not subject to capital controls or abnormal tax rates

In return, these countries must commit to increasing their own military spending

Examples: Canada, UK, Japan, South Korea, partly Vietnam (if the US sees a role compensating for China)Ultimate goal: Build an alliance of 20+ countries

, forcing them to peg their currencies to the USD. Use trade and military agreements to bind them. Controlled weakening of the USD with allies to avoid international collapse. 🟡

YELLOW COUNTRIES – Neutral, conditional treatment Countries that are not clearly allies or adversaries. May be large trading partners but.

. Treated according to the principletit-for-tat (reciprocity)

:

The US imposes equivalent tariffs to those that country imposes on US goods

No security or currency privileges

Limited access to technology and long-term capital

Examples: India, Brazil, Thailand 🔴

RED COUNTRIES – Systemic adversaries Countries whose behaviors or policies are viewed as.

.

Punished by:

Punitive tariffs (punitive tariffs)No access to US capital markets Withholding tax on bonds (via IEEPA)

No military support

Example: China, Russia, Iran

Bước 4. Trái phiếu thế kỷ và hoán đổi nợ – trò chơi dài hơi trên sân khấu toàn cầu

Trump's idea: "If I can borrow money to build skyscrapers for 50 years, why can't America do the same?"

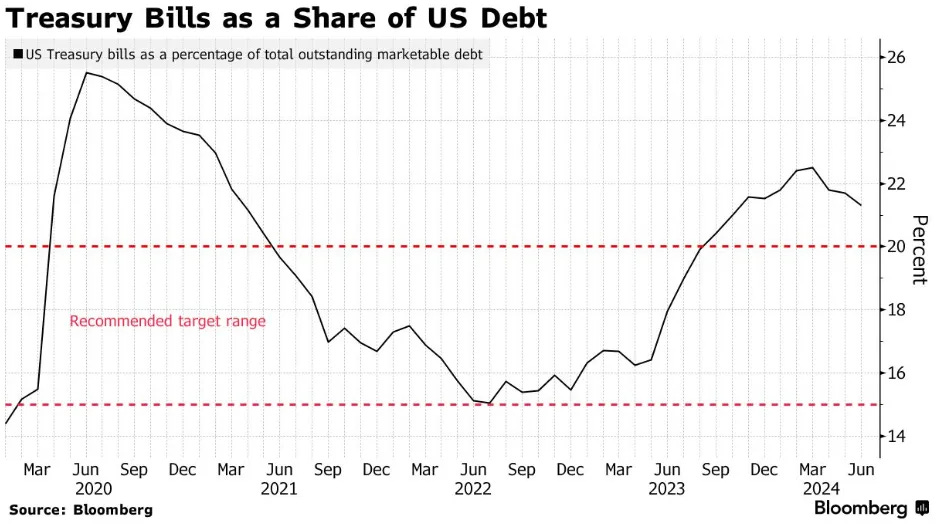

Problem: US public debt is not only large – but also 'short-term' and vulnerable

One of the strategies implemented by the former Treasury Secretary under Biden - Yellen - was to increase the issuance of short-term bonds, especially Treasury bills.

→ Reduce pressure on the long end of bonds

→ Stimulate the economy, support the Democratic Party's strategy for the November election

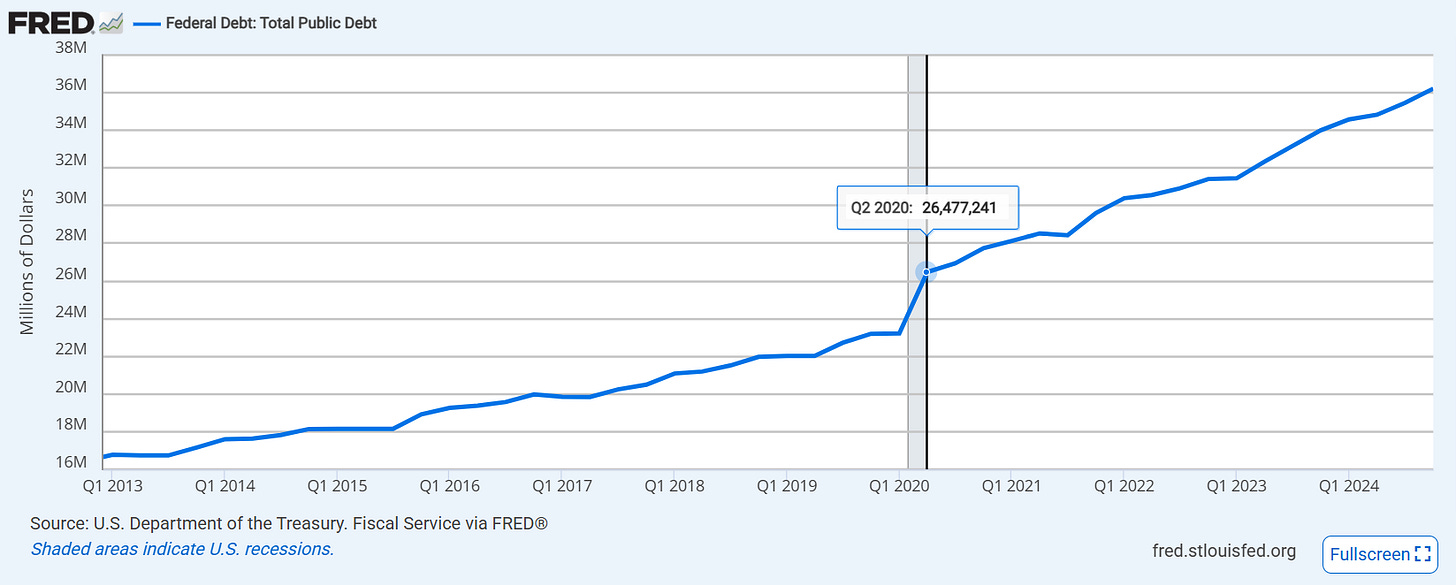

However, the cost is that the plan doubles the US debt interest burden in 4 years even though public debt only increases 38%

→ In 2020, when Trump left office, interest costs accounted for only 13% of government fiscal spending compared to 24% currently, although total federal debt only increased from 26 trillion to 36 trillion.

→ Trump enters the White House with more than 50% of US Treasury debt having maturities under 5 years – meaning continuous refinancing is required. This year alone, 2025, according to Bloomberg estimates, the US needs to refinance nearly 7 trillion dollars due to poor public debt management from the previous administration.

This makes US bonds very vulnerable to market punishment by the market if macroeconomic risks increase (war, recession, technical default).

Trump sees this weakness clearly – and his next step is century bonds, to lock in long-term debt costs.

Goal: Reduce public debt without "blowing up".

No one wants to disrupt the world's balance sheet. US Treasury bonds remain the backbone of global finance.

Bessent's desire is to maintain a flat yield curve (flatter yield curve), i.e., keeping long-term interest rates low even when short-term rates rise. This helps US businesses and consumers easily borrow for long-term investments, promoting domestic economic growth

→ Solution: Convert short-term borrowing into illiquid long-term borrowing. Convince allied countries (like NATO) to swap short-term bonds for long-term bonds (e.g. 100 years, even perpetual).

Tactic: "Those who don't play are enemies". If you are an ally, you will bear part of the global security costs. If not, you choose to stand outside the system.

Incorporate into bonds clauses adjusted to GDP growth → if the economy is good, the US pays higher interest, if recession, pays lower → like "Countercyclical" bonds.

📌 This is Trump-style "financial leverage" mindset: Turn fixed obligations into flexible ones, leverage America's reputation to borrow long-term and spend big.

→ This allows the US to devalue the USD without market punishment. As Bessent says: "A weak dollar and hegemony are not contradictory."; "The US is the only country that can print money to pay global debt without losing credibility."

→ This is the strategic pillar to reshape the Bretton Woods 3.0 system – in which the US reduces its reluctant role as a short-term borrower, becoming the chosen issuer of long-term debt.

Summary: Don't be bound by traditional budget cycles – think like a real estate developer: "Build big, borrow long, pay slowly."

Bước 5. Quỹ tài sản quốc gia – từ bảng cân đối chết sang tài sản sống

"Why doesn't America – the country with the most assets in the world – leverage those assets to generate cash flow like a business?"

Bold idea: Mobilize national assets to rebuild the future. Not just reduce debt-Trump wants to create real assets with liquid cash flow for Americans.

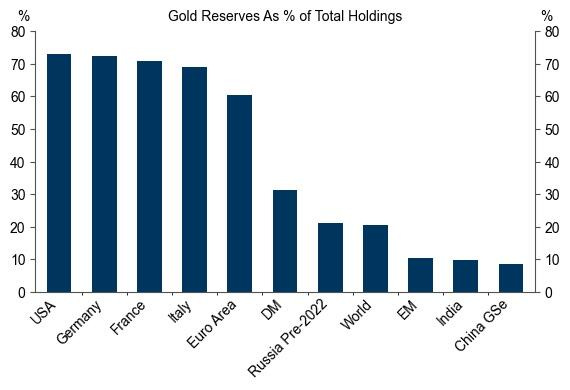

Mobilization channels: Revalue US gold reserves, lease federal land, exploit domestic energy resources.

America's gold reserves

Federal land (over 640 million acres – equivalent to the area of 16 Germanys combined).

Federal Lands in the American West - The Atlantic")

Seaports, infrastructure, mineral resources, television spectrum, etc.

Equity in state-owned or semi-state-owned companies (such as Amtrak, USPS...).

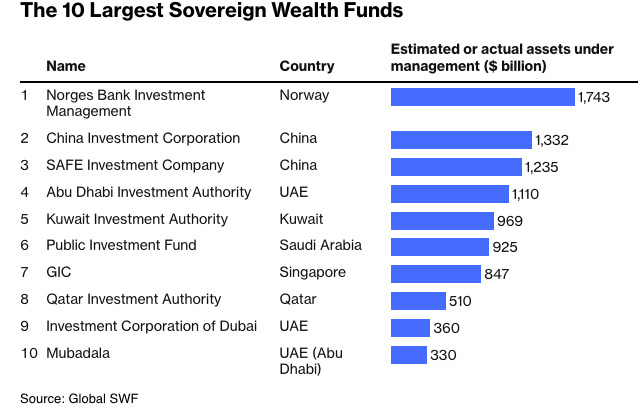

Although it sounds bold, the US currently has 23 state-level sovereign wealth funds managing approximately $332 billion in assets, according to data from Global SWF.

Alaska Permanent Fund – the largest and most famous – invests profits from the state's oil and currently manages $78 billion. In 2024, the fund distributed a “dividend” of $1,702 to each resident of Alaska.

Federal Lands in the American West - The Atlantic")

Applications: Establish a sovereign wealth fund, issue baby bonds for each newborn child, use assets instead of debt to fund long-term investments.

→ A semi-independent federal entity, similar to the model of sovereign wealth fund (SWF) such as in Norway, UAE, or Singapore.

Objective: Restructure, lease, or sell inefficient public assets to:

Reinvest in strategic sectors.

Pay down national debt.

Generate cash flow to support tax cuts.

From 'spending government' to 'owning government'

This is a shift from the mindset of budget distribution to asset management.

With Trump, America is not just a government – but a corporation with the world's largest assets. And since they are assets, they must generate returns.

→ “Make America Great Again – by making America's balance sheet great again.” - Trump

Bước 6. Chiến lược ba mũi nhọn 3-3-3:

“Increase 3 million barrels of oil per day in the US, growth real GDP 3%, and budget deficit 3% - if we achieve all three, the US economy will be in a very good position.”

- Treasury Secretary Bessent

Cheap energy

Reduce input costs for domestic manufacturing → attract companies back to the US.

Create jobs for the middle-class working class in the Midwest – Trump's key voter group.

Increase geopolitical power: The US can use LNG exports to replace Russia in Europe or as a bargaining tool with Asian countries.

“We will drill, we will mine, and we will regain economic control with American energy.”

Deregulate to expand credit

Promote private investment in manufacturing and infrastructure – instead of relying solely on government spending.

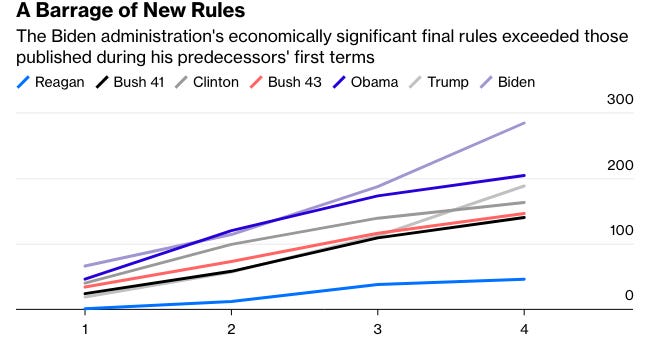

FYI: Under President Joe Biden, federal agencies have issued new regulations at an unprecedented rate in history. 284 major economic impact regulations have created serious burdens, causing many businesses to file mass lawsuits, many of which have won.

Unlock capital flows for domestic businesses, especially small and medium-sized enterprises (SME) – the backbone of US manufacturing.

Reduce compliance costs, helping businesses increase profit margins, encouraging more job creation.

“More production, not regulation” - Trump

Support Main Street instead of Wall Street

Trump publicly criticizes the Fed's monetary policies under Obama – which mainly saved Wall Street but abandoned ordinary people. Under Trump, policies focused on:

Cutting personal income and small business taxes

Increasing spending on infrastructure, manufacturing, and “real” jobs instead of financial bailouts for Wall Street

Limiting the influence of financial “giants” on monetary and trade policies

→ Shifting policy focus from financial assets (financial assets) to physical production, creating real value (GDP)

→ Truly re-industrializing America.

→ Populist image: Protecting the working-class voter base, not the Wall Street financial elite.

All aimed at a “soft landing” for the US economy: reducing inflation, increasing investment, re-industrialization-without sacrificing growth.

America must devalue the dollar to boost competitiveness and ease of doing business with other countries and attract factories back to America, strengthen domestic production capacity, promote American industry, create jobs

→ The agreement is a subtle but profound step to shift America's role in the global financial system. No longer a country that “prints money unlimitedly,” America under Trump seeks fairer payment for hegemony-and make allies pay their share.

5. Will the Mar-a-Lago Agreement succeed?

5.1 Lack of ally cooperation:

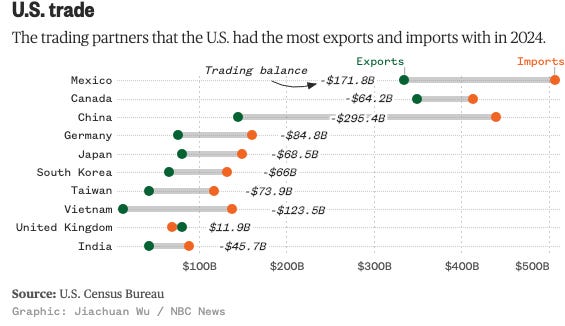

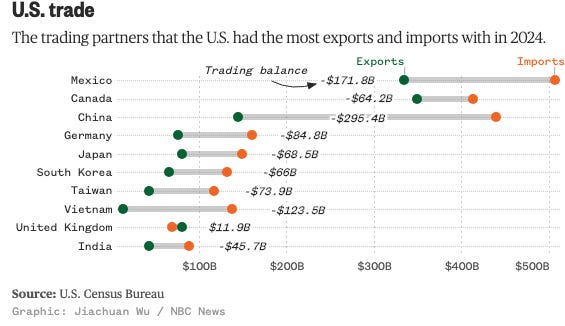

The Plaza Accord in 1985 succeeded in part because it was signed between close allies: US, Japan, Germany, France, UK. But today, America's key trading partners like China, Vietnam, Mexico are not strategic allies, making any coordinated USD devaluation effort lack political basis.

But this very thing highlights the structural changes in globalization, and simultaneously creates bargaining leverage for the US.

The US has large trade deficits with these countries

→ those countries must accumulate USD

→ in the position of sellers, they need the US more than the US needs them.

→ Trump can leverage this to restructure the global financial system in a direction beneficial to the US.

However, Trump may realize that today's linkages do not need to rely on political allies, but on vulnerabilities in the global supply chain network. The Mar-a-Lago Accord could function as a coercive “implicit agreement,” rather than a voluntary pact. (China and Vietnam heavily depend on exports to the US, Taiwan depends on US security commitments, and Mexico is bound in the North American supply chain)

Additional notes on China:

5.2 Extending public debt maturities could impact credibility

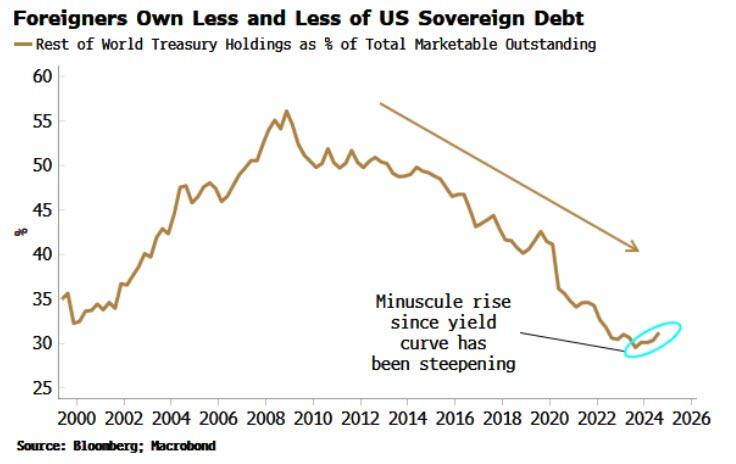

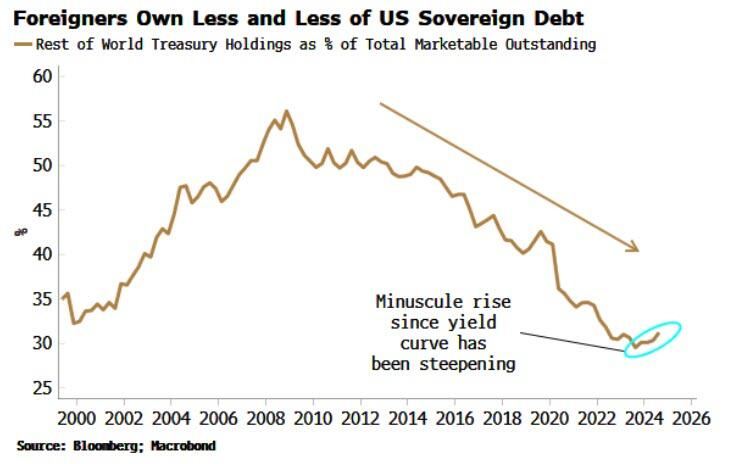

US short- and medium-term Treasury bonds have the world's deepest secondary market – allowing any country or institution to easily withdraw capital if needed. Countries hold USD and US bonds like “liquid gold,” because they are both safe and highly convertible.

→ This very liquidity underpins the power of the US dollar, because it allows the US to finance large deficits without market punishment – an “exorbitant privilege” (exorbitant privilege) that no other country has.

→ Long-term bonds have weaker liquidity, higher interest rate risk, and are no longer suitable for reserve roles. For central banks or sovereign wealth funds, holding illiquid assets poses systemic risk.

➡️ Consequence: They will seek alternatives – such as gold, euro, RMB, or even physical assets.

While countries like the UK have been “punished” by markets for undisciplined fiscal policies

Example: The Truss shock - when UK 10-30 year bond yields (gilts) skyrocketed after the government's fiscal spending announcement, forcing Prime Minister Liz Truss to resign just 49 days into her short tenure in October 2022.

Foreign investors, especially Japan and China, are reducing holdings of US bonds. Central banks are also cutting USD reserves since the Ukraine war, due to fears of asset freezes.

Risks from the Mar-a-Lago Accord strategy (selective trade restructuring, ally categorization) further reduce demand for US bonds due to long-term uncertainty.

However, long-term bonds are not new: Argentina, Austria, and some European countries have issued 100-year bonds. Austria is a prime example of this success:

5.3 A weaker USD could cause capital outflows

Especially amid overvalued US stocks, capital flight would cause sharper price drops.

However, if the USD weakening process is coordinated through 100-year bond issuance and strategic capital controls (IEEPA), then a weak USD will not cause panic but become a controlled export stimulus policy → US manufacturing firms will record higher profit margins →

If the US continues renegotiating agreements (as Trump often does), partners will lose trust and reduce USD dependence.

→ This accelerates the deglobalization process, causing long-term harm to US businesses.

Re-trading is not bad, if it resets the balance of interests based on new geopolitical power. In the Mar-a-Lago Accord model, countries are classified by a traffic light system (green, yellow, red) and treated accordingly – not based on goodwill, but on their position in the value chain and degree of alignment with the US. Alternatives to the US are limited. Most global supply chains still depend on US finance, technology, and security.

5.4 Economic Recession

JOLTS Quit Rate (voluntary quit rate) is low → Workers lack confidence to switch jobs → Labor market not as strong as NFP reports.

Counterargument - Reduce public, increase private: However, reducing public sector personnel (public servants) accompanied by fiscal loosening for the private sector will create a productivity shift effect – workers encouraged to move to goods production or private technology sectors. And if paired with increased public investment spending (through the national asset fund), demand for technical, construction, and industrial labor will absorb some unemployment

In addition, a weakening dollar will directly reduce US consumers' purchasing power - a particularly concerning factor amid widespread pessimistic sentiment about economic prospects.

Note that the US economy relies heavily on domestic consumption, and any decline in household spending could lead to serious consequences for overall growth.

Another serious risk is policy uncertainty-especially regarding interest rates, taxes, regulations, and trade policy-causing businesses to enter a state of uncertainty in long-term planning.

In such an environment, capital investment decisions (capex) will stall due to uncertainty in cost of capital, output markets, and policy incentives.

Many businesses choose to delay or cancel major projects, from investments in production infrastructure, research and development (R&D), to supply chain expansion.

→ Corporate investment pace declines, causing a domino effect on the labor market, value chain, and national productivity

→ When businesses dare not expand, hire more people, or upgrade technology, the economy loses intrinsic growth momentum. In worse conditions, this could lead to a recession cycle, not from financial shock, but from paralysis of expectations and confidence.

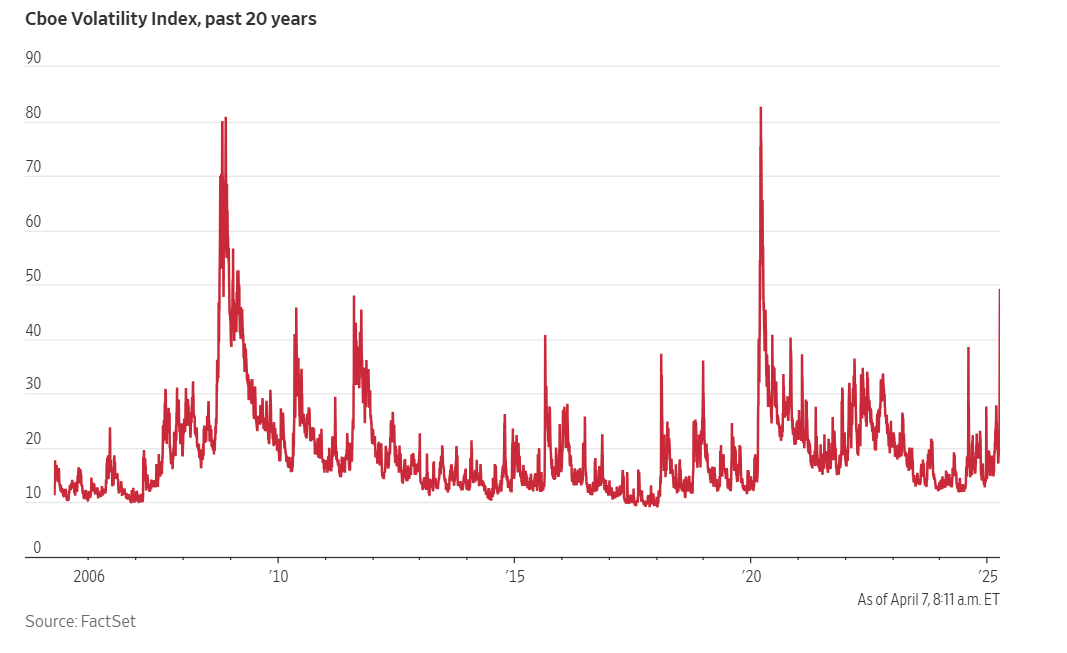

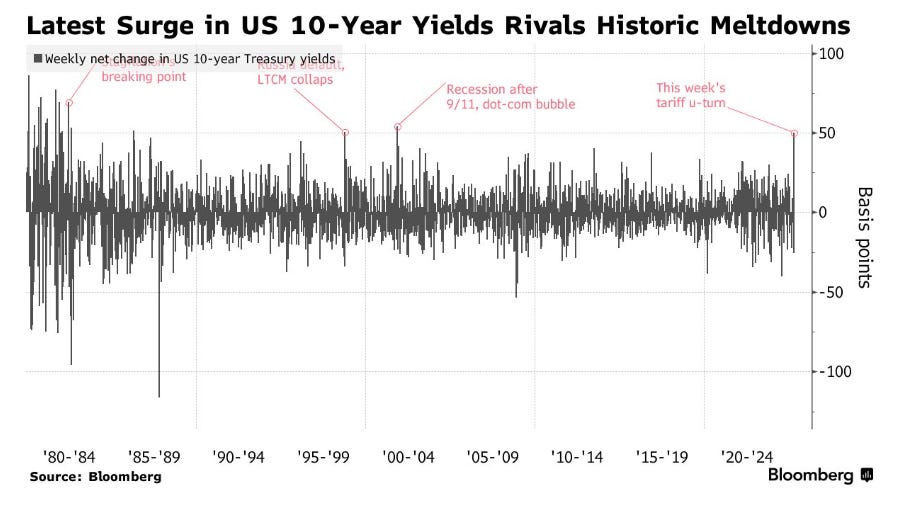

5.5 Market Instability

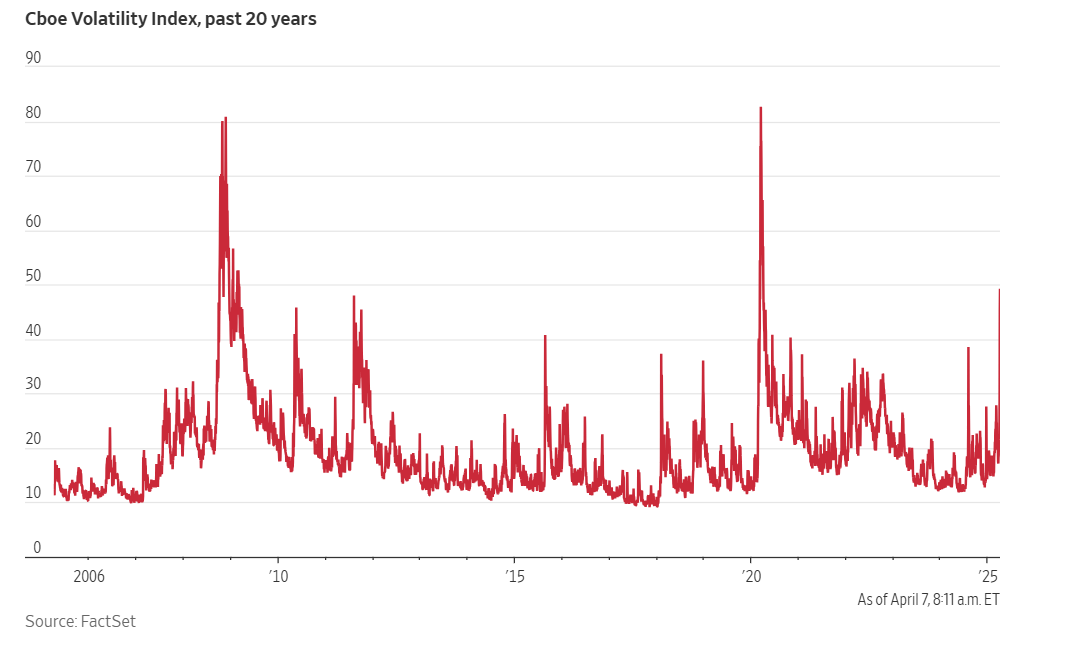

In recent days, after Trump announced tariff packages on the world, amid rising recession fears, market panic has surged, mainly due to concerns about credit, geopolitics, and systemic risks.

→ US stocks sold off alongside fear index surge

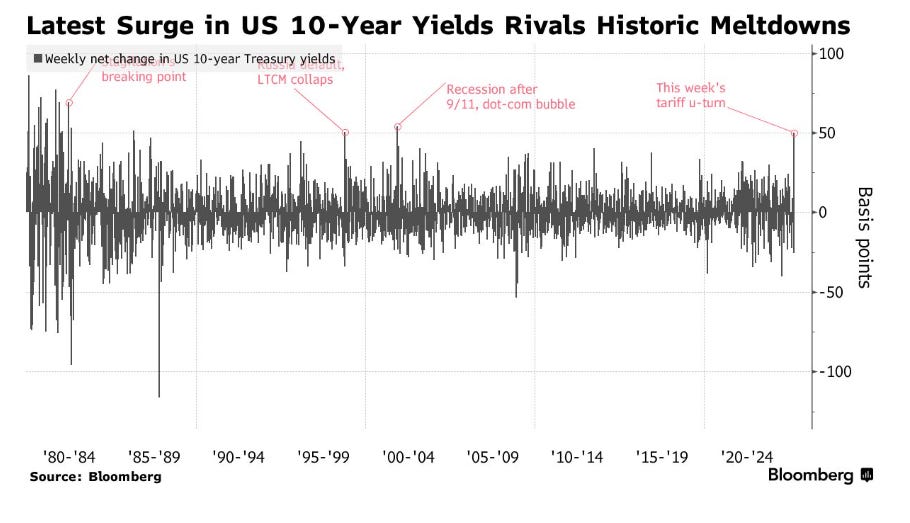

US bonds, which are often viewed as "safe haven" – safe haven in crises, are under severe pressure. Long-term bonds dumped en masse, pushing yields to surge – reflecting investors fleeing US debt assets. Some key indicators:

US 10-year bond yield climbs faster than during 9/11, Dotcom, and 2008 crises

Yen, euro, and Canadian dollar all strengthening: high likelihood foreign capital fleeing US bonds, switching to other assets.

About $1.000 trillion stuck in basis trade strategies – and if market loses liquidity or spreads fluctuate sharply, highly leveraged hedge funds forced to exit positions, causing "fire sale" of bonds.

=> Nowhere "safe" in the US anymore – both stocks and bonds lose confidence.

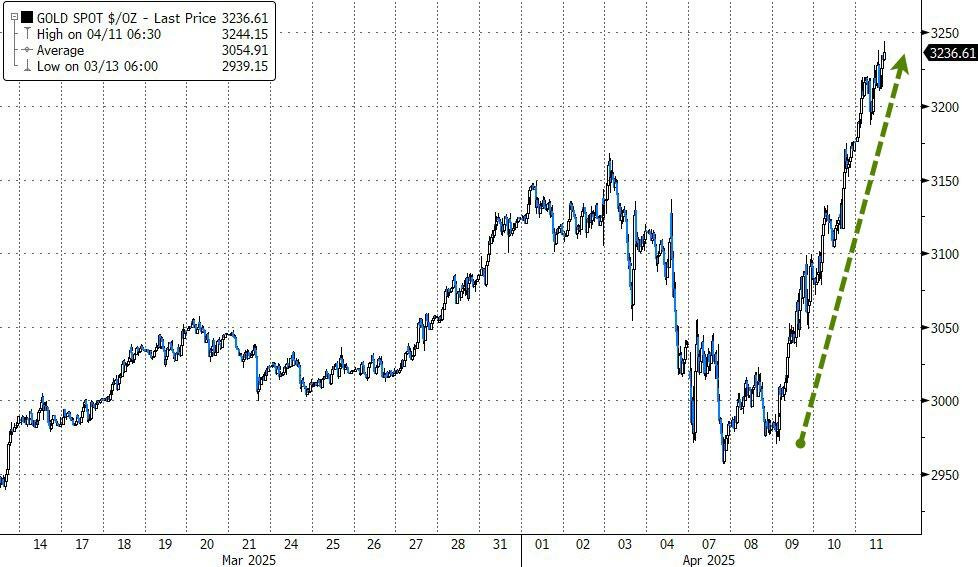

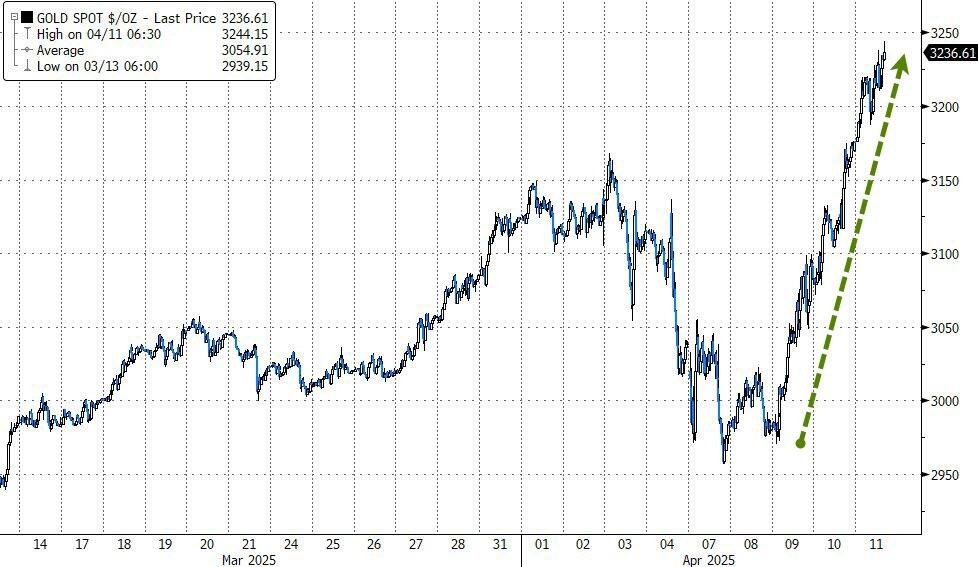

→ Investors may shift to gold, Swiss franc, yen, or German bonds, i.e., other higher-safety assets.

However, Fed caught between two opposing risks – called policy dilemma:

Fed intervenes = Easily seen as bailing out stock market (Fed Put) when economy itself shows no signs of cracking

→ undermining independence credibility of Fed

→ Market believes upcoming policy driver under political pressure, then all Fed actions no longer credible.

→ Each interest rate decision no longer rational policy signal, but product of term pressure.

→ Risk of dollar sell-off fleeing US more severe and more negatively impactful on current situation

Inflation risk from tariff war persists → Fed dares not ease

Fed's strategy at this time: "Let the market feel some pain"

To force legislators, administration, market, and businesses back to economic reality and de-escalate tensions.

Fed playing role of "adult in the room", not rescuing every dip, preserving its credibility and independence

Fed still has "secret weapons" ready to deploy if “game” goes out of control:

Standing Repo Facility (SRF) - Ready to inject temporary liquidity into banking system when needed.

Temporarily exempt Treasuries from SLR (Supplementary Leverage Ratio) – as done in 2020.

Adjust Reverse Repurchase Agreement - RRP to absorb short-term pressure.

Interim conclusion

Ultimately, a too-strong dollar does not reflect the strength of the US economy, but exposes an ironic reality: America is living beyond its own production capacity. Chronic trade deficits and public debt growth twice as fast as GDP growth show that Washington has long been spending based on the forced savings of the rest of the world – through the global foreign exchange reserve system tightly tied to the US dollar.

The combination of populism, geopolitics, and public asset management shows that Trump is not simply someone who wants “Make America Great Again”. He is building a new doctrine – where the state owns instead of spends, where supply chains are weaponized, and where the USD can be controllably devalued to serve reconstruction. In a world moving away from globalization, the Mar-a-Lago strategy is a survival blueprint for America.

Mar-a-Lago is not just a place – it is a survival blueprint for America in the multipolar era. And perhaps, the world has begun to understand that: the dollar is weakening, not only because America chooses to change, but possibly because the world is choosing to shift, quietly diversifying reserves and gradually abandoning the "dollar anchor".