US stock market has a rather dull trading session in the morning with most investors deciding to sit out the market. The index indicators moved lightly from the opening session with liquidity continuing at low levels across all sectors.

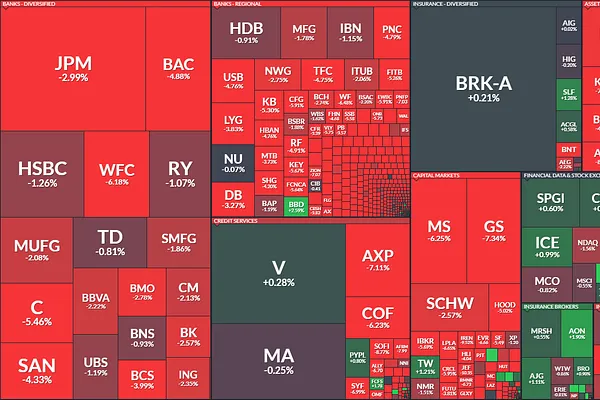

Summary of Bank of America financial report:

Viet Hustler is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.