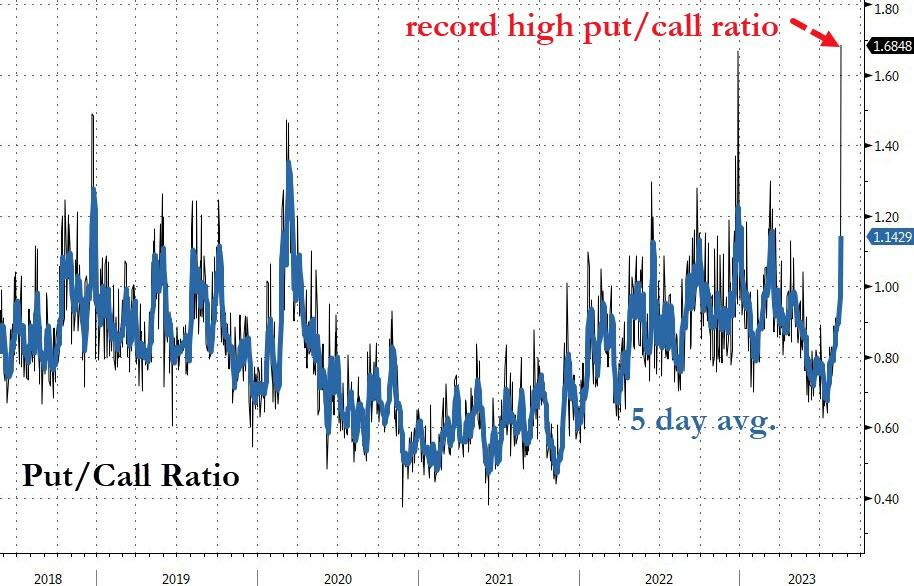

Put-Call Ratio hits all-time high ahead of August OpEx

Worst week overall for S&P500 since the SVB crisis in March with put/call ratio at 1.68 - this is the highest level since data began in 1994.

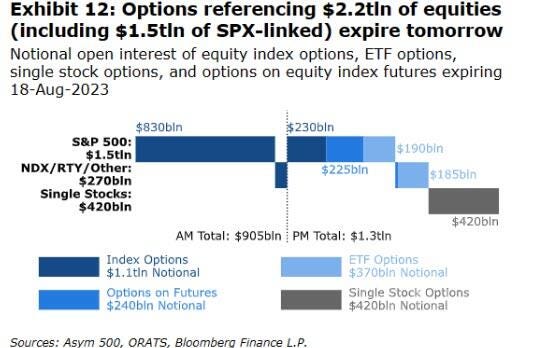

Total of $2.2 trillion notional value (value if settled) of options expiring today with $1.5 trillion from SPX alone

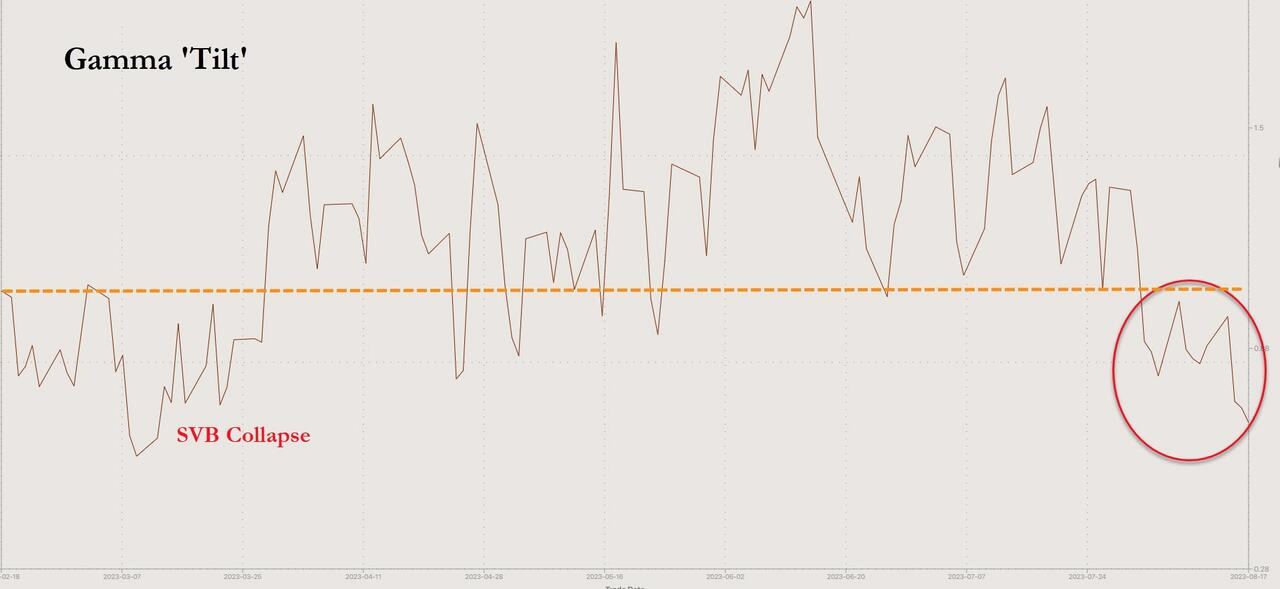

Demand for put hedge and yesterday's 0DTE flow pushed the market completely into a negative gamma environment today with the deepest pressure since March.

Accordingly, the volume of puts expiring today has released a large amount of pressure on the market right from the morning, as market makers who were previously short delta began covering right from the open at the 4350 put wall.