Last week, a series of protests by Chinese citizens took place to oppose the Zero Covid policy and the government's suppression of freedom of movement and speech. This is considered the greatest challenge to Xi Jinping's administration since the 1989 Tiananmen Square massacre.

Along with that, China's economy is gradually cooling with the decline of a series of PMI indicators, putting pressure on the upcoming Politburo meeting in China next December. In addition, China also faces a public debt crisis with local governments and an ongoing real estate crisis since the second half of 2021.

Viet Hustler will return to China in this week's macroeconomics section!

Positive policy changes in the real estate crisis

The crisis from the real estate (RE) bubble has lasted since mid-2021.

Summary of China's real estate crisis 2021-2022:

Main causes: Uncontrolled real estate growth over decades has made China's real estate market value unreasonably large (accounting for 30% GDP), increasing real estate-related debt and pushing real estate prices to the highest levels in the world.

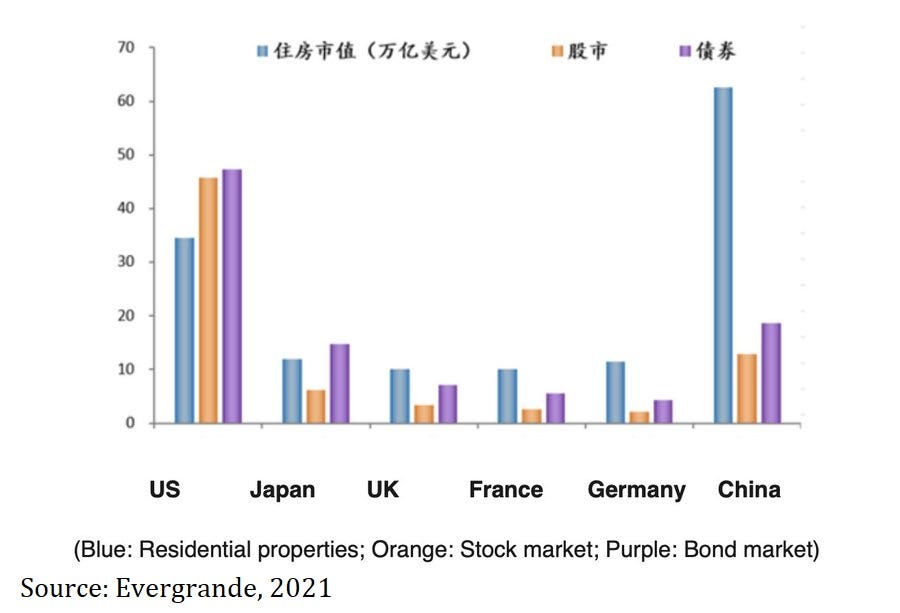

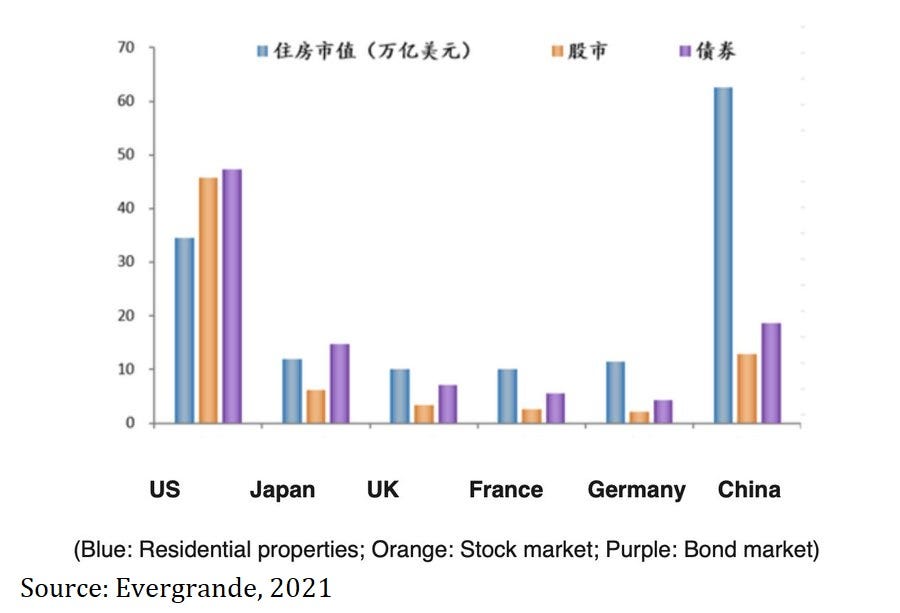

Mid-2021: Estimated value of residential real estate in China was USD 62.6 trillion (blue column). At that time, China's real estate value:

Twice the market cap of the US stock market (USD 33.6 trillion) and 3 major markets in Europe (UK, France, Germany = USD 31.5 trillion).

6 times the Japanese stock market (USD 10.8 trillion).

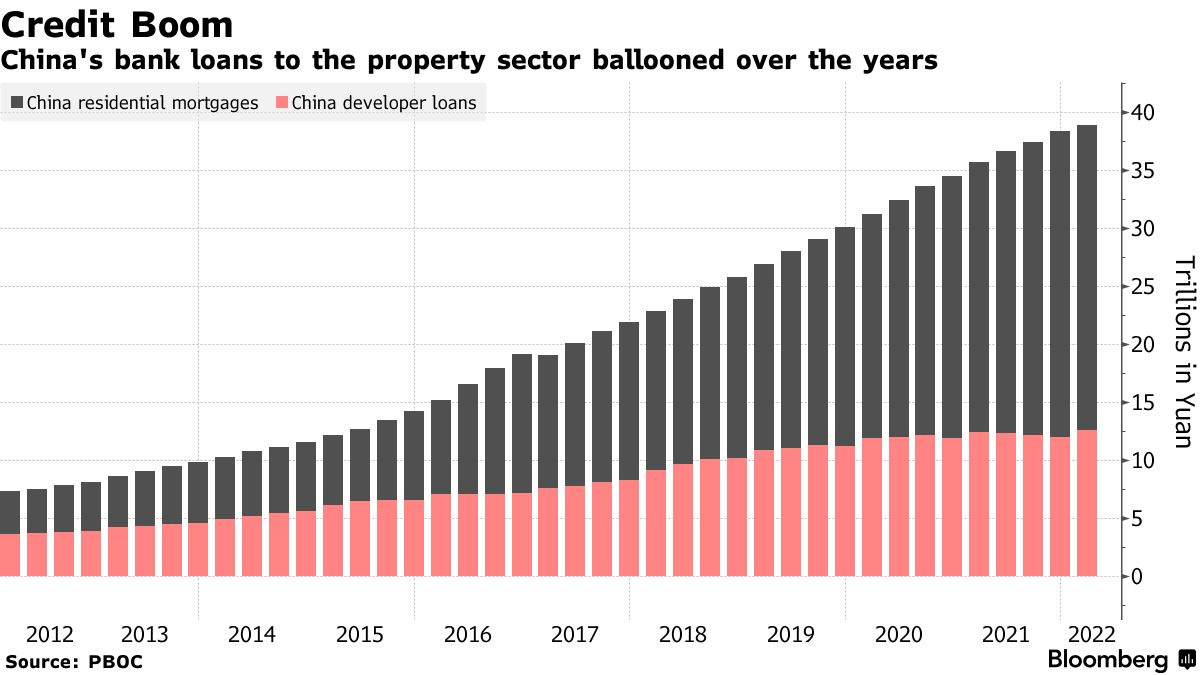

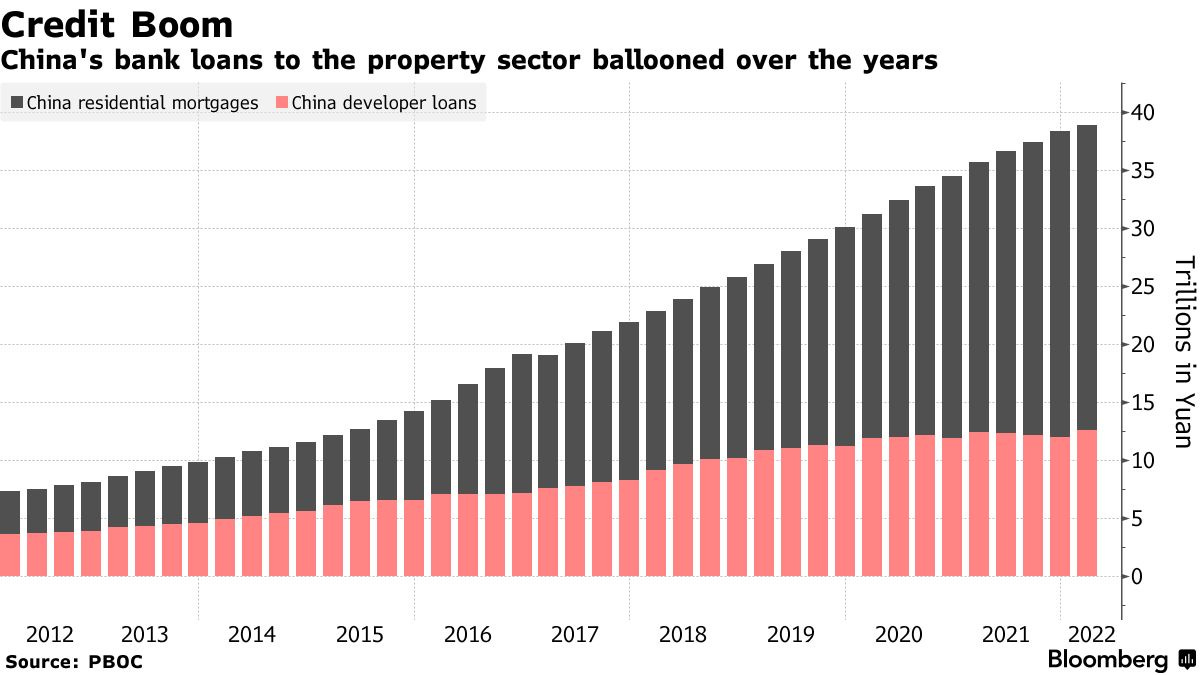

Bank loans to real estate developers and home mortgage debt have continuously increased over the years.

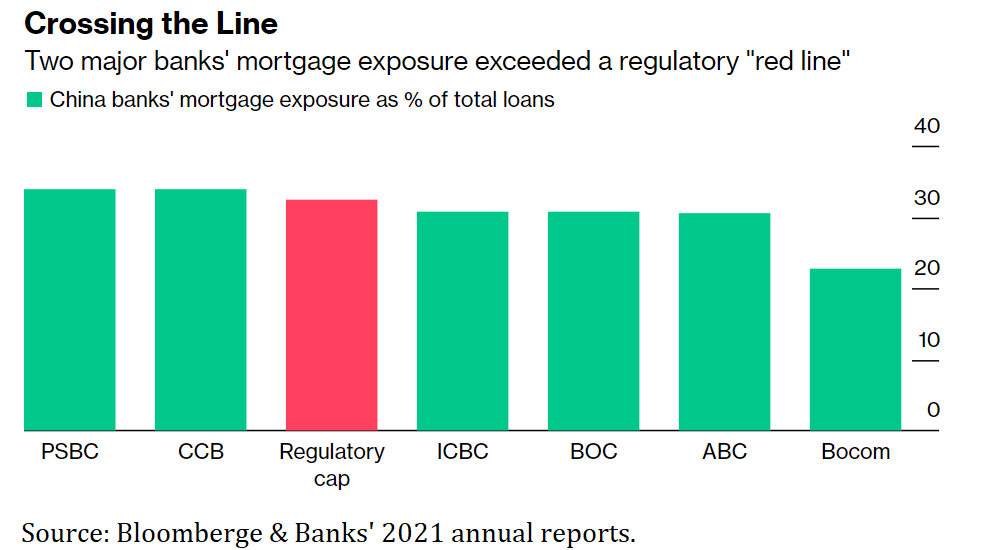

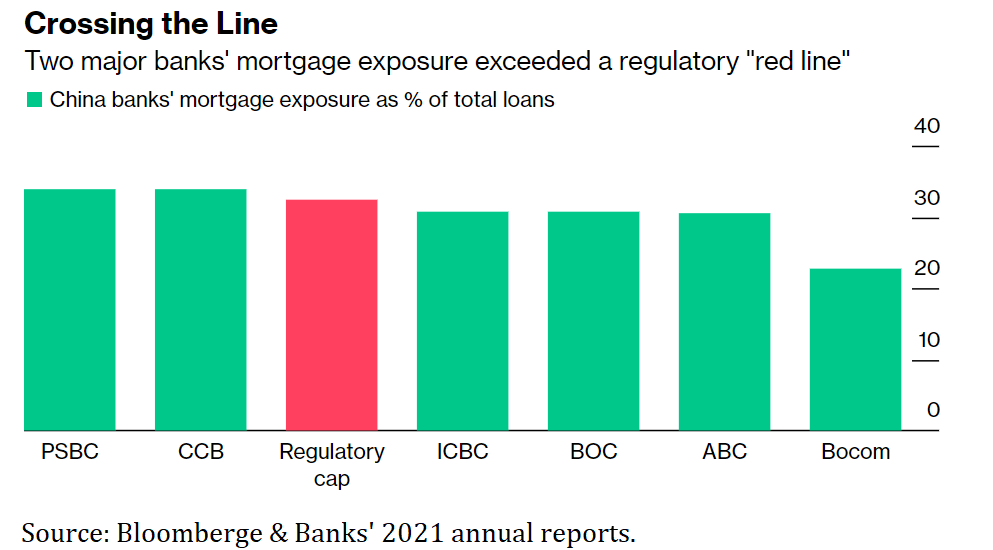

Home mortgage debt accounted for about 34% of total loans at Postal Savings Bank of China and China Construction Bank at the end of 2021, higher than the regulated ceiling of 32.5% (red column) for large banks.

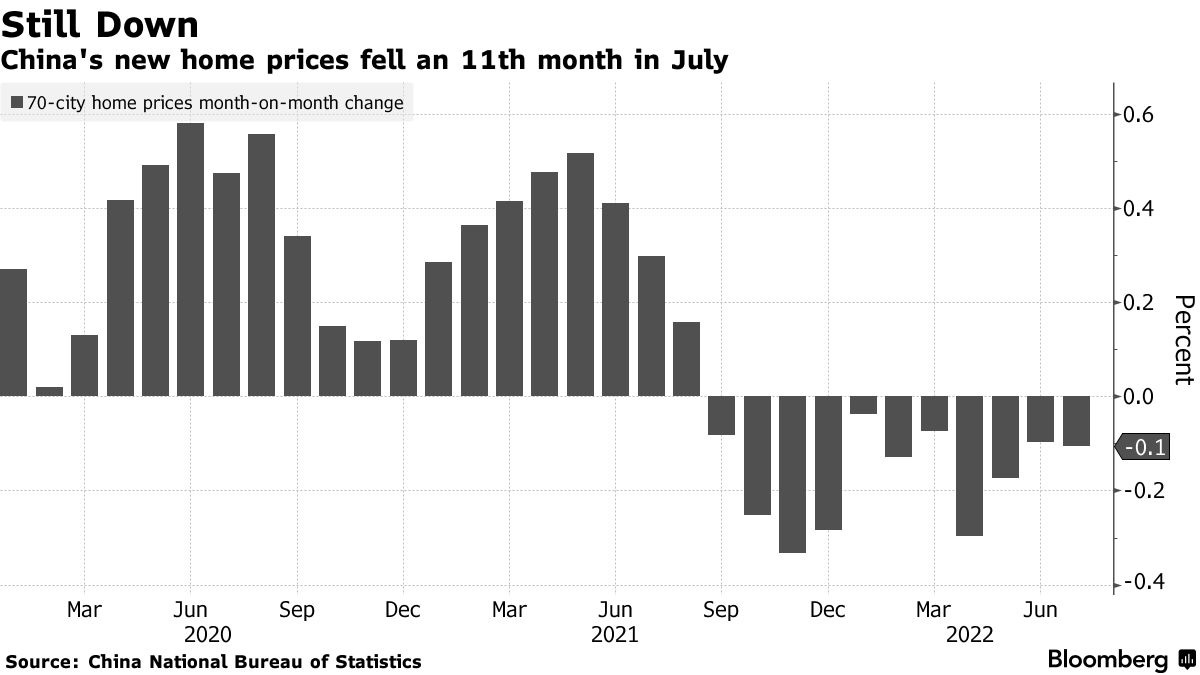

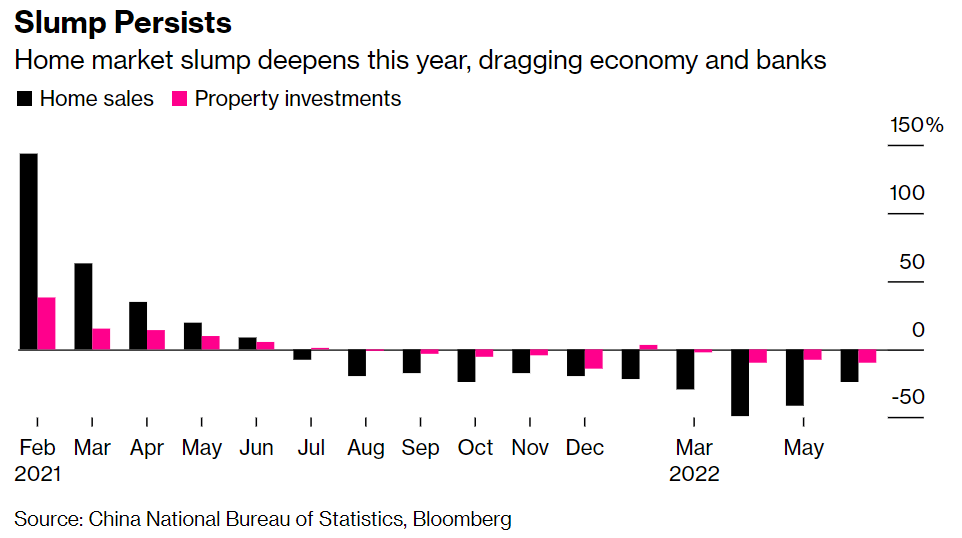

The real estate bubble has "burst" since the second half of 2021:

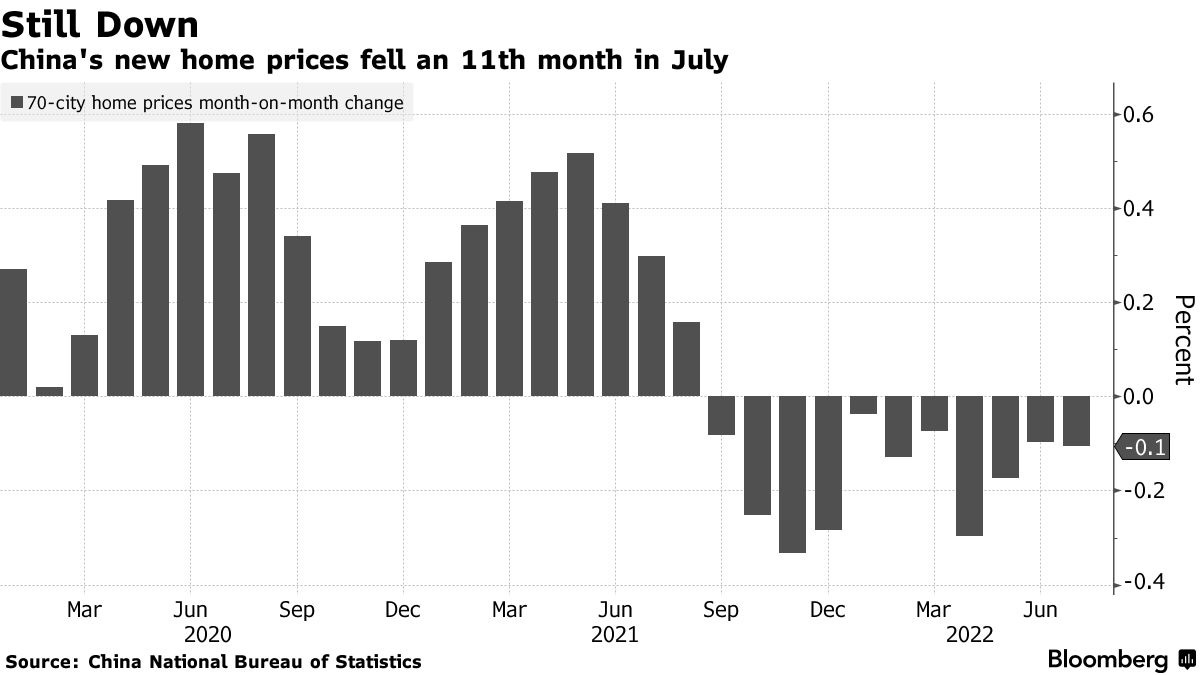

Since September/2021, house prices in China have continuously declined until now.

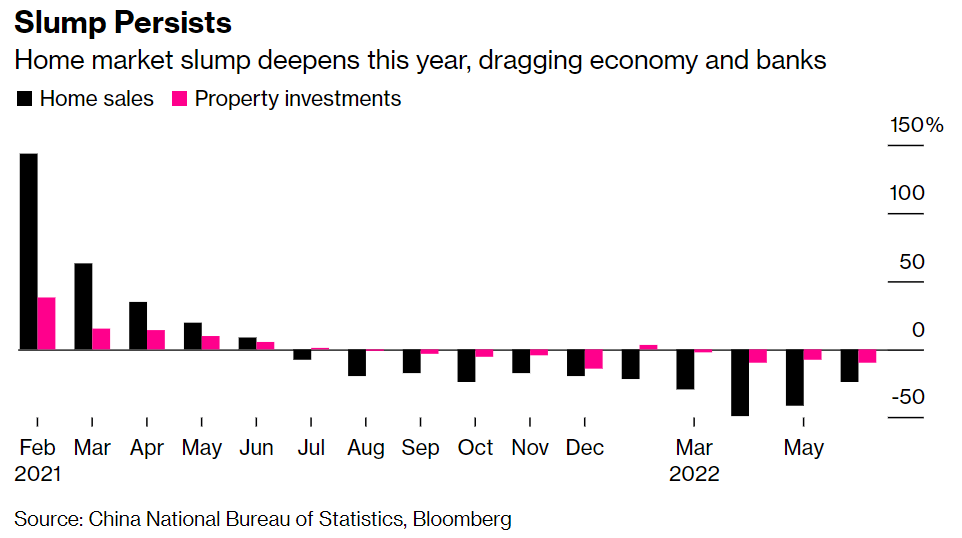

The number of homes sold and investment cash flow into real estate declined, creating significant liquidity pressure for real estate investors.

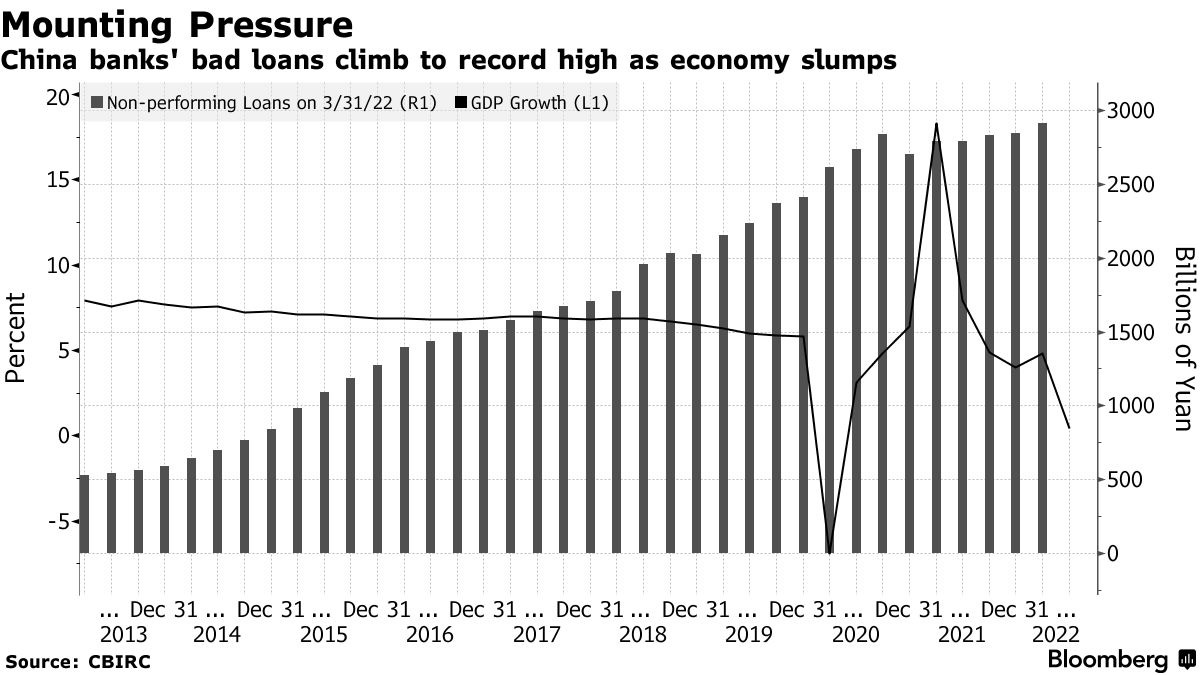

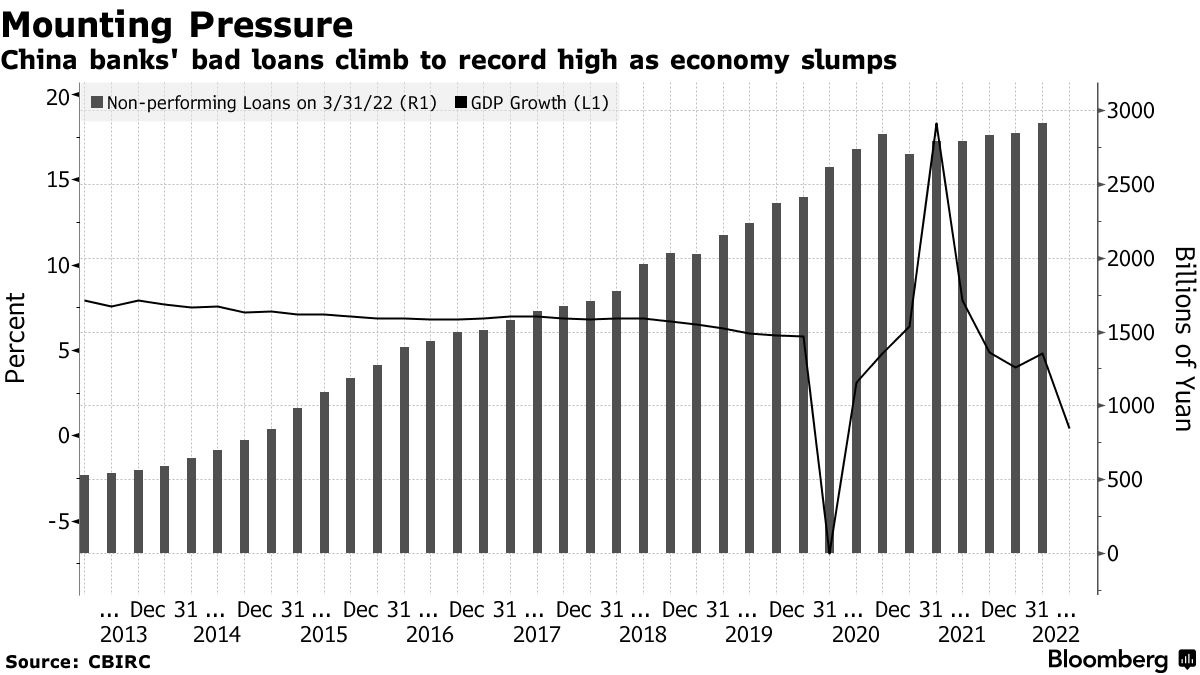

Chinese banks face losses equivalent to USD 350 billion from mortgage debt and loans to real estate developers.

Recent positive changes to the real estate situation

Last week, China has taken positive measures to temporarily stem this RE crisis:

For the first time since 2015, China will allow real estate builders (developers) to raise capital through selling shares to local investors.

This resolves the funding issue for real estate development businesses and reduces their debt burden.

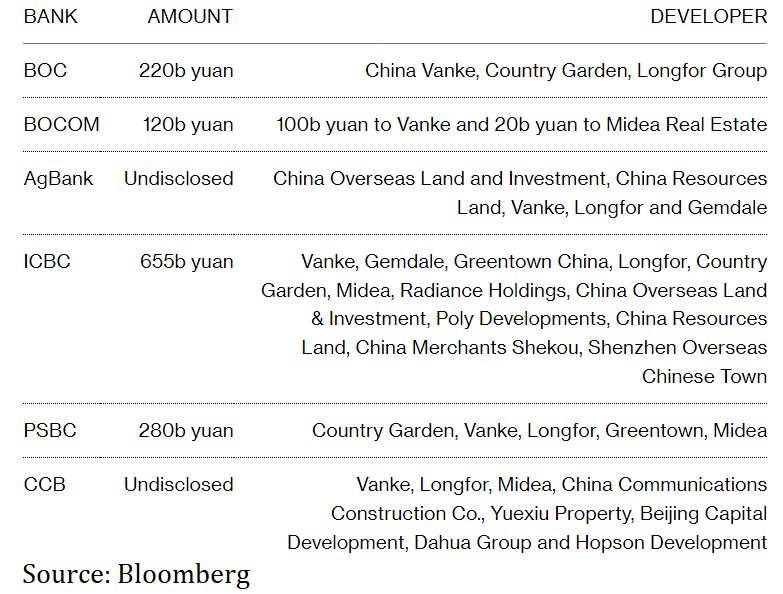

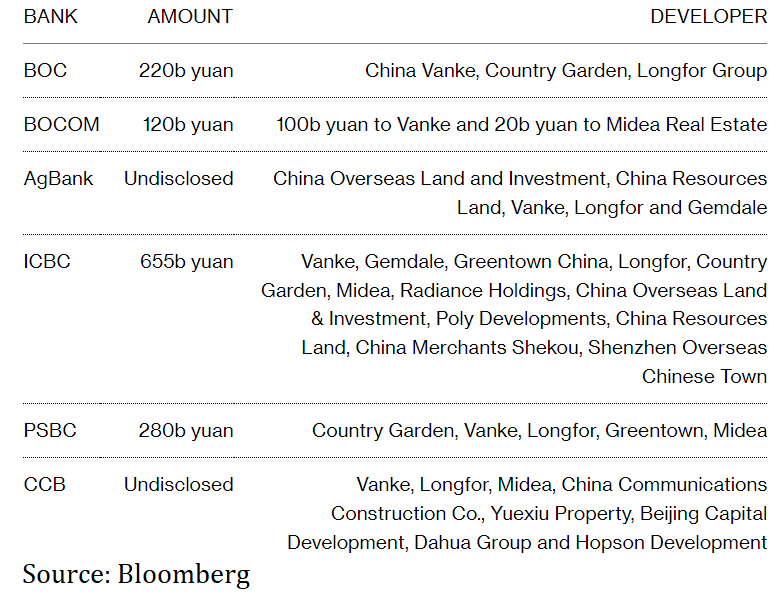

Major Chinese banks are expected to provide USD 162 billion in credit (~1% China's GDP) to real estate developers.

This eases the liquidity burden of the crisis they face.

ICBC leads the credit package with a limit of up to CNY 655 billion (~USD 93 billion) for 12 real estate developers - excluding Evergrande and Sunac which are in crisis.

Evergrande plans to propose debt restructuring after December, after being urged by foreign creditors to liquidate assets to repay USD 2 billion in maturing debt.

Evergrande bonds fell below 10 cents/bond. Evergrande's debt restructuring plan includes exchanging bonds for shares of the group.

Cooling production, slow growth and government debt burden

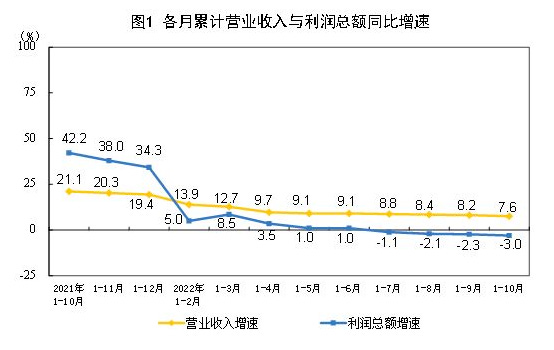

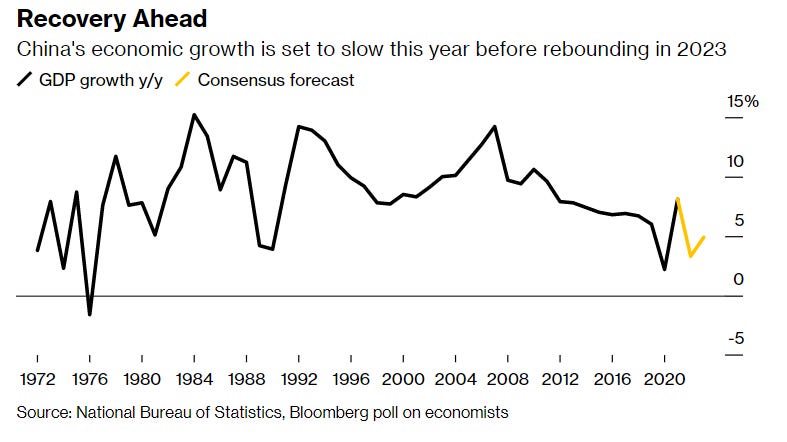

PMI down, GDP below average

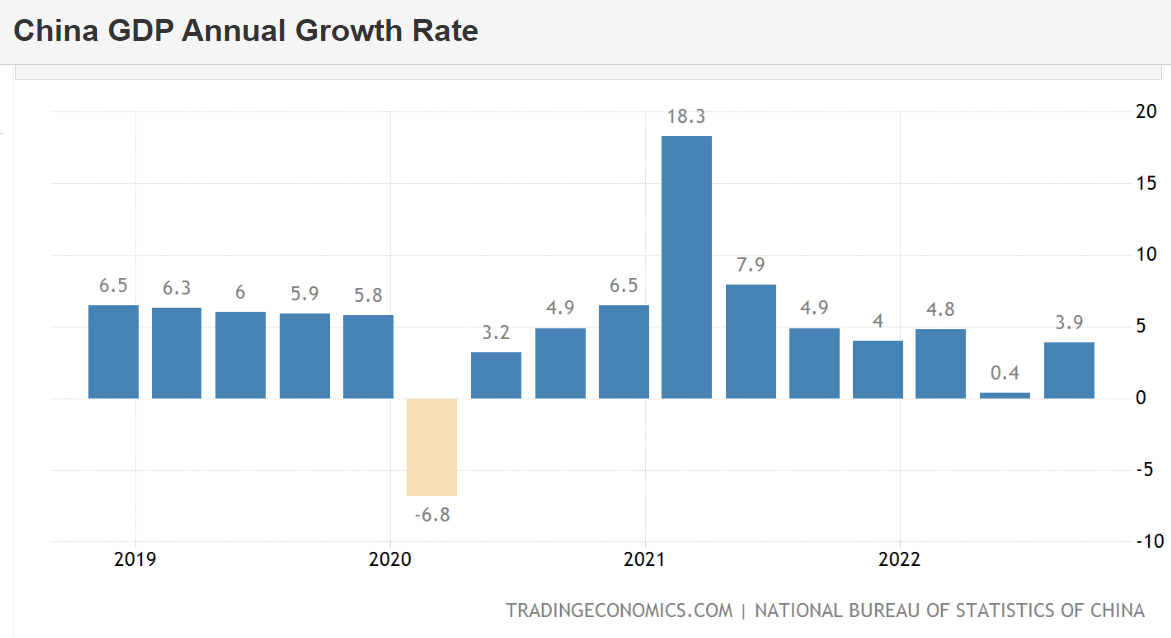

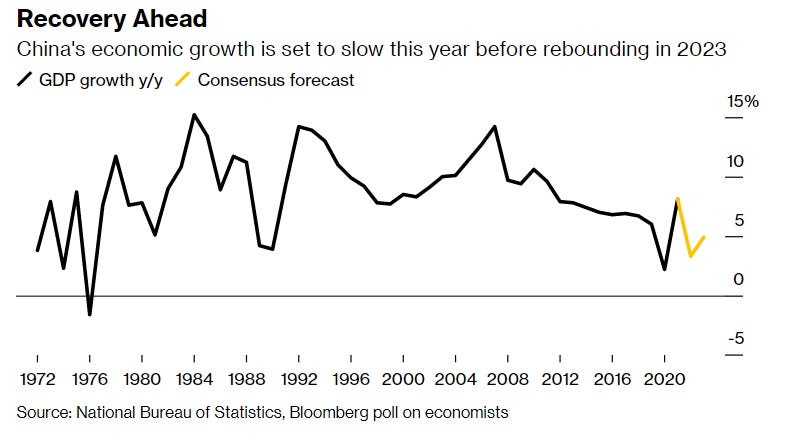

In October 2022, China's economic growth situation was more optimistic though still low: Q3 GDP growth (Y/Y) at +3.9% higher than forecast (+3.3%) and Q2 (+0.4%)

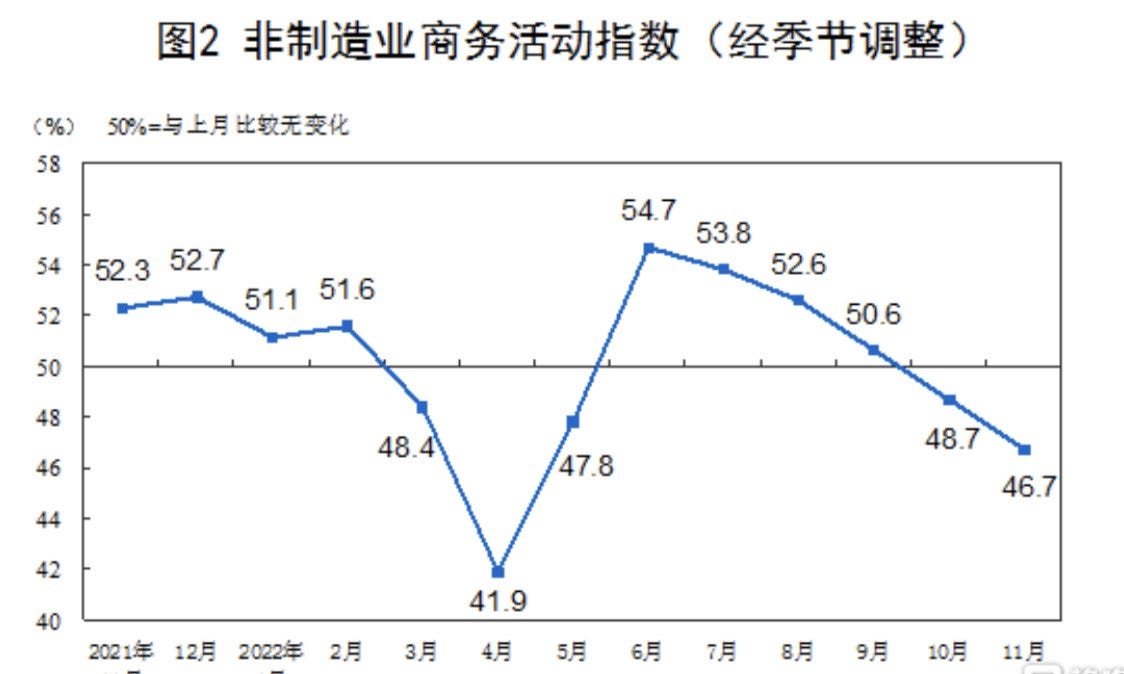

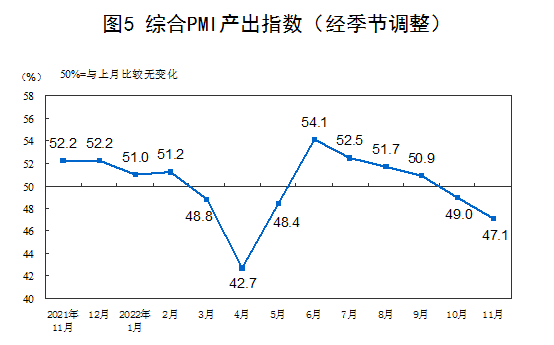

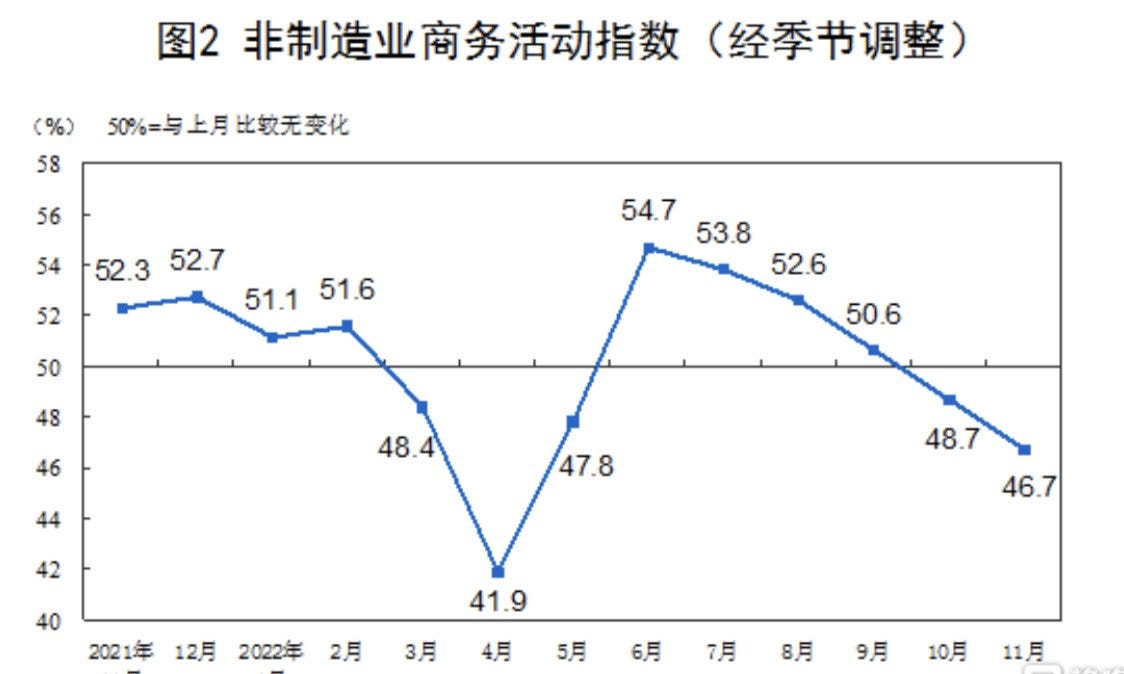

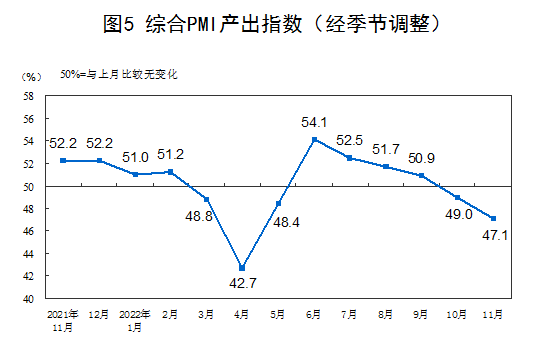

However, China's PMI data last week was alarming: China's manufacturing and non-manufacturing activities continued to contract in November.

Manufacturing PMI: 48 (down from forecast: 49.0, October 2021 data: 49.2)

Non-manufacturing PMI: 46.7 (down from forecast: 48.1, October data: 48.7)

Composite PMI: 47.1 (down from forecast: 48.1)

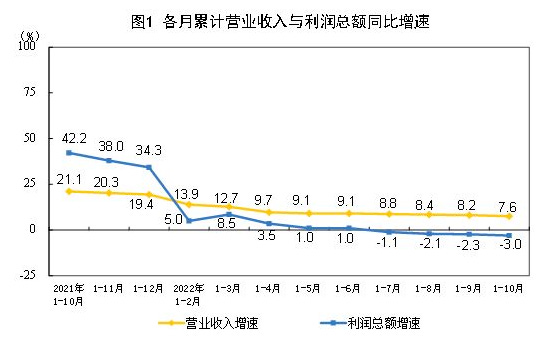

China's industrial profits for January-October 2022 fell -3.0% year-over-year.

Causes: Due to the recent surge in the epidemic negatively impacting operations of some businesses, production activities stalled, and product orders declined.

According to China's National Bureau of Statistics: 46% of medium-sized enterprises and 58.8% of small enterprises reported financial difficulties and lack of market demand.

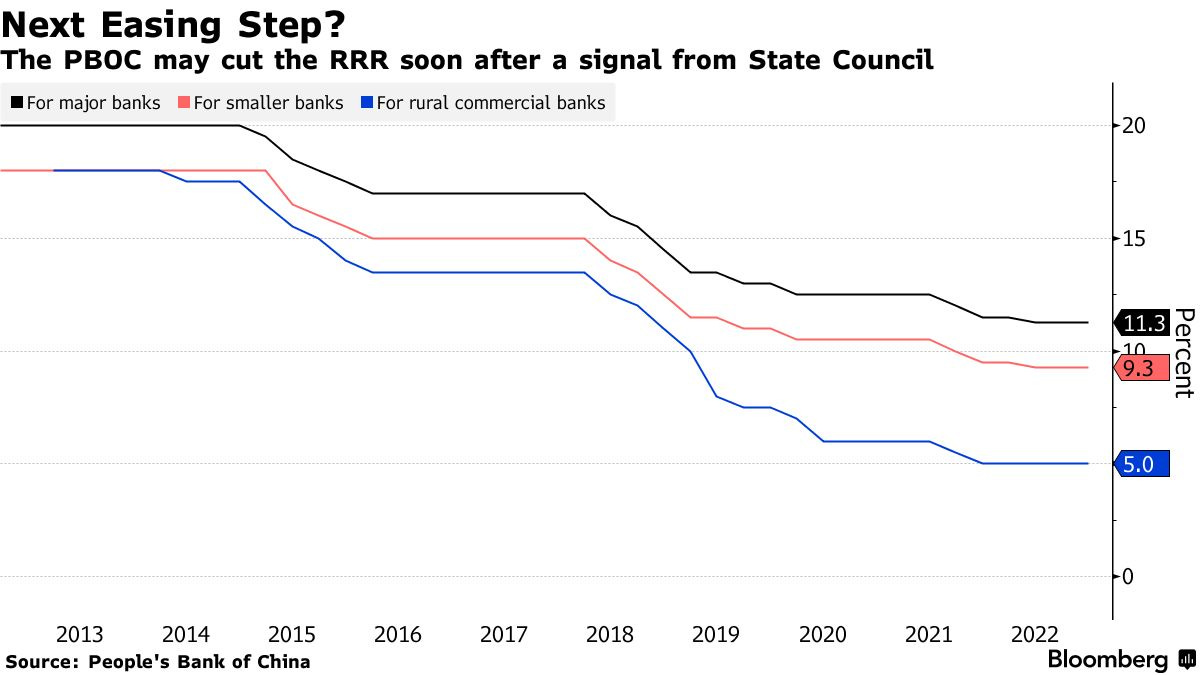

Amid the cooling economy, the People's Bank of China (PBOC) will soon inject liquidity into the economy via RRR cuts - reserve cash of commercial banks - following signals from the PBOC board last week.

However, cash release will not stimulate credit demand side in China. Borrowing in the "Zero Covid" economy remains subdued regardless of how cheap borrowing is.

Next December, China's Politburo, the nerve center of the Communist Party, will meet to issue general guidelines for next year's economic policy.

November PMI decline indicates the focus of this meeting will be promoting economic growth.

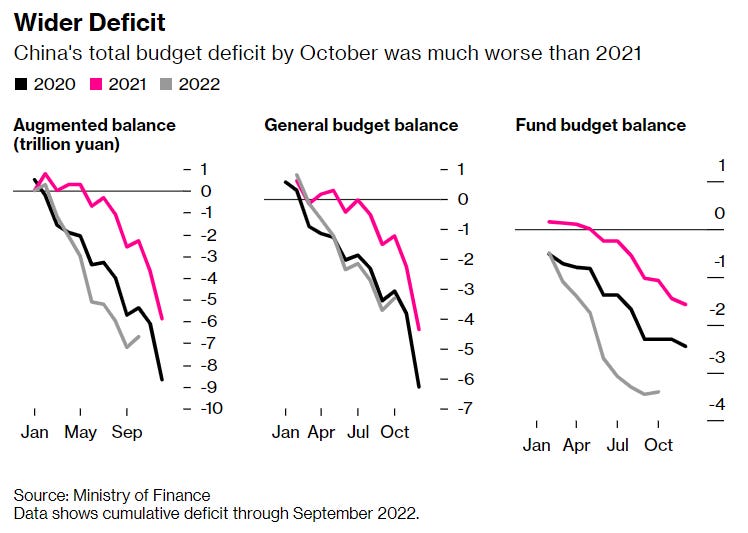

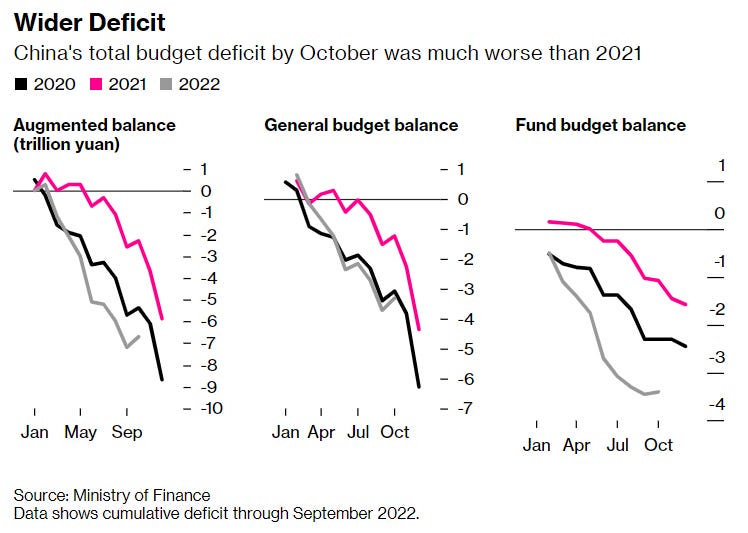

Meanwhile, the fiscal spending deficit of the Chinese government is widening.

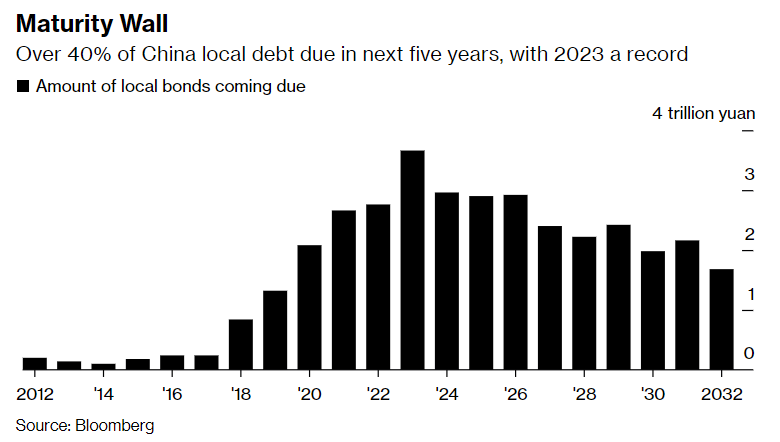

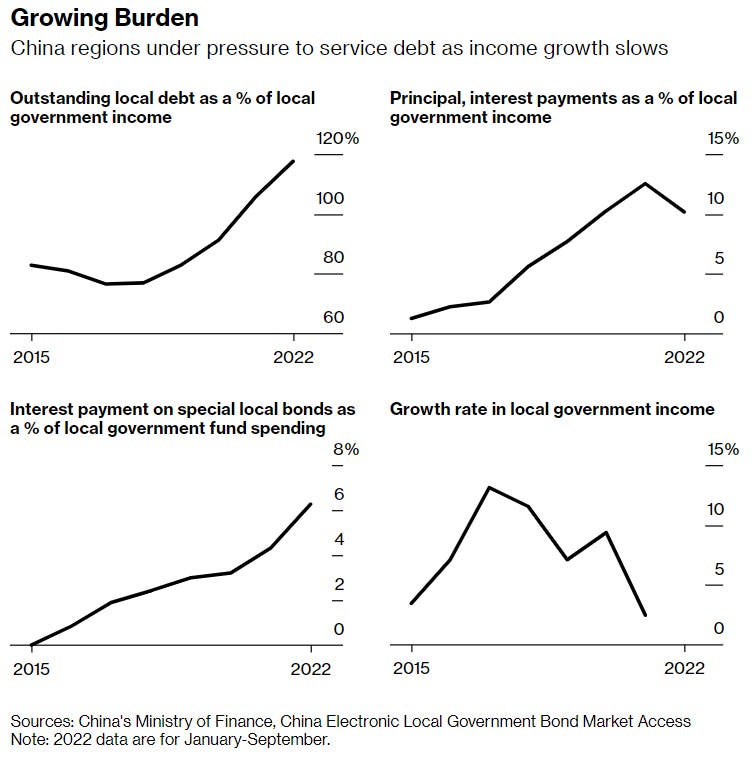

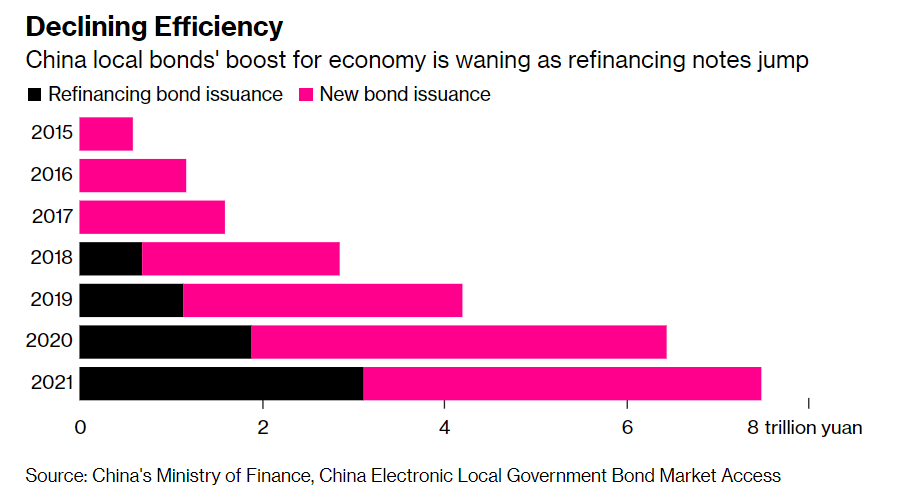

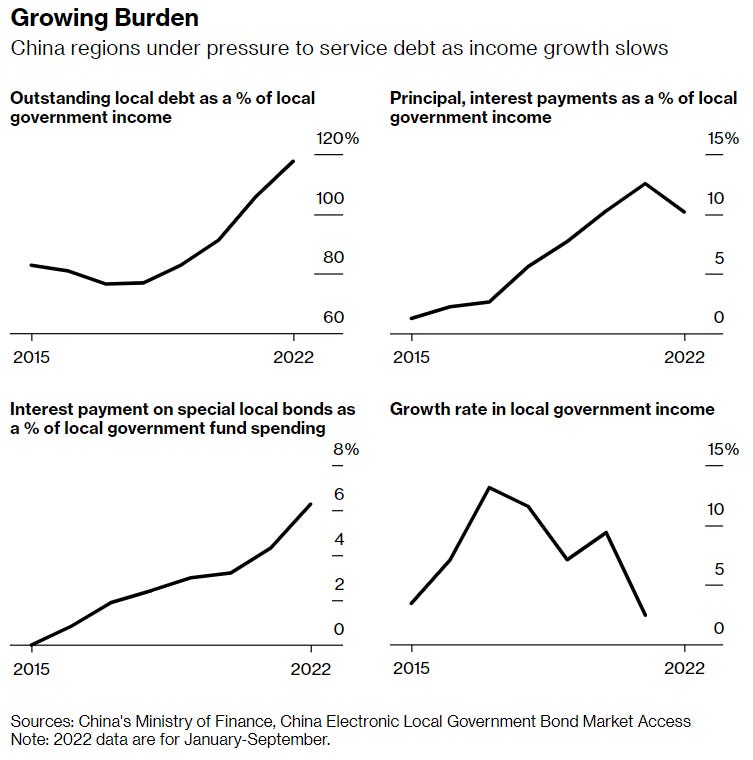

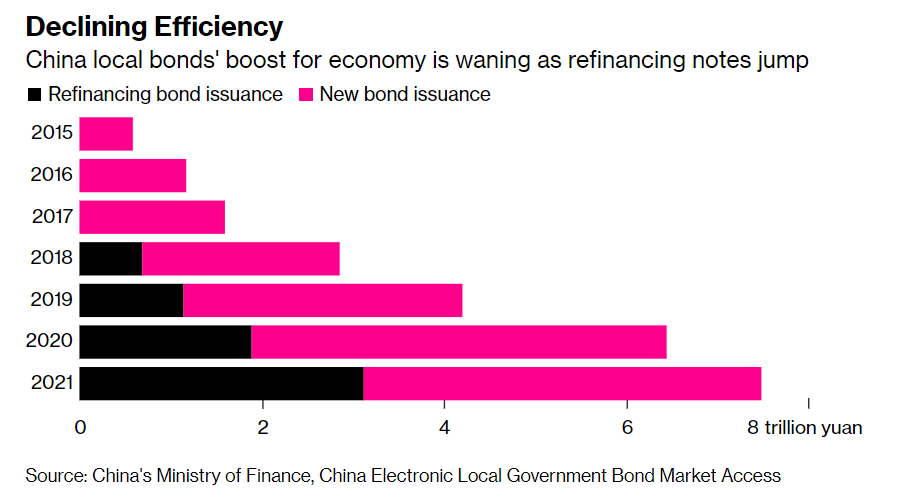

Local Chinese governments face a high risk of a public debt crisis.

Local governments of 31 provinces in China face debt pressure from bonds worth nearly CNY 15 trillion (~USD 2.1 trillion), maturing within the next 5 years.

These debts account for more than 40% of their total outstanding debt.

While revenues and economic growth have slowed due to Zero Covid policy: debts have reached 120% of local governments' revenues.

Debt rollover and new debt issuance will face difficulties as cumulative debt has hit record highs.

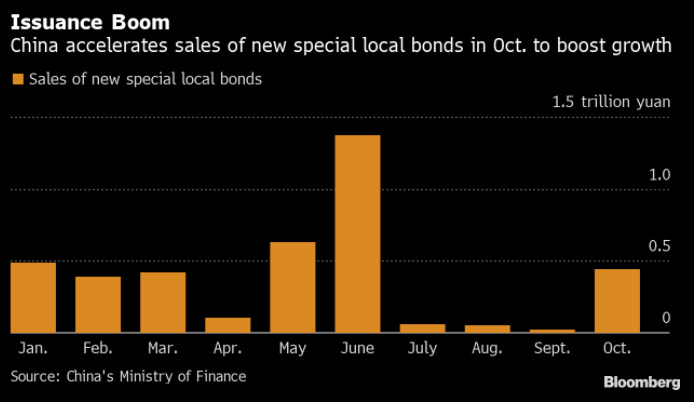

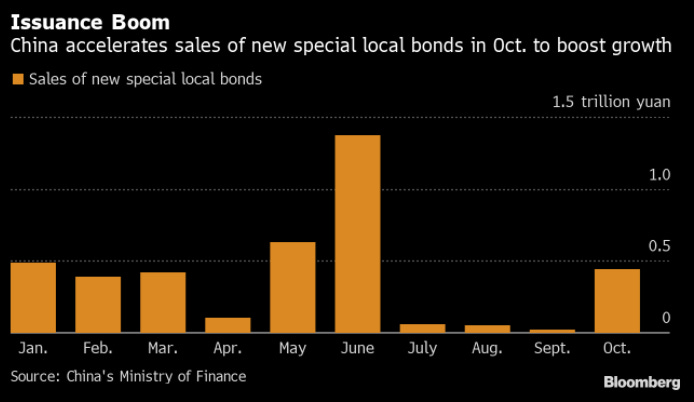

Chinese provinces in October issued the highest amount of new special bonds since June, to meet Beijing's deadline to use up the CNY 500 billion (70 billion USD) additional debt quota to boost economic growth.

Protests against Zero Covid policy and concessions from Xi Jinping's administration

Protests broke out across provinces and cities in China following a series of public dissatisfactions due to rigid Zero Covid policies.

Some key events that sparked the protests:

The Urumqi apartment fire that killed many people. The cause was the building being locked and sealed off due to Covid, preventing victims from escaping and no one being able to enter to rescue them (including firefighters).

Ordinary people being forcibly sent to quarantine areas without any signs of Covid infection…

Suspicions that the Chinese government changed people's codes from green (normal) to yellow and red on the Covid control App to prevent people from traveling and participating in protests.

Protests at the Apple factory (where 80% of Apple's tech products are produced) were suppressed.

The nationwide protest movement is the biggest challenge for the Chinese government since the Tiananmen crisis. How Xi Jinping responds could play a pivotal role in the country's future. Especially as this protest movement erupted during China's national mourning period.

National mourning: Jiang Zemin, former General Secretary of the Chinese Communist Party after the 1989 Tiananmen Square massacre, passed away at age 96 last week.

During his tenure, China reclaimed Hong Kong from the UK, experienced extraordinary economic development in the 2000s, and improved international relations with other countries.

Jiang Zemin's national mourning period (and the end of his era of rule) also heightened concerns for the Chinese government, as people would have a reason to gather and protest amid simmering dissatisfactions over freedom of speech and Zero Covid policies.

Beijing has reasons to worry following a series of similar historical events:

The death of Zhou Enlai caused public faith in Chairman Mao's government to collapse in 1976,

Student protests at Tiananmen following the death of Hu Yaobang in 1989…

The Beijing government has adopted a combined approach of suppression and concessions:

Heavy police presence on the streets, checking Chinese people's use of VPNs.

Combined with a more conciliatory tone from the government to prevent people from taking to the streets again this week.

Chinese health agencies and state media are changing their propaganda to make Covid seem less scary.

Local governments that impose excessive extreme Covid restrictions will be “criticized”.

Due to protest pressure, measures to ease the Zero Covid policy are being implemented:

Chengdu residents no longer need a negative PCR test to enter shopping malls and supermarkets.

China is targeting vaccinations for the elderly and low-risk patients in Beijing's most populous district and allowing home quarantine.

Previously, Bloomberg Intelligence forecasted the losses China might face when abandoning the Zero Covid policy: 363 million infections, 5.8 million ICU cases, and nearly 620,000 deaths.

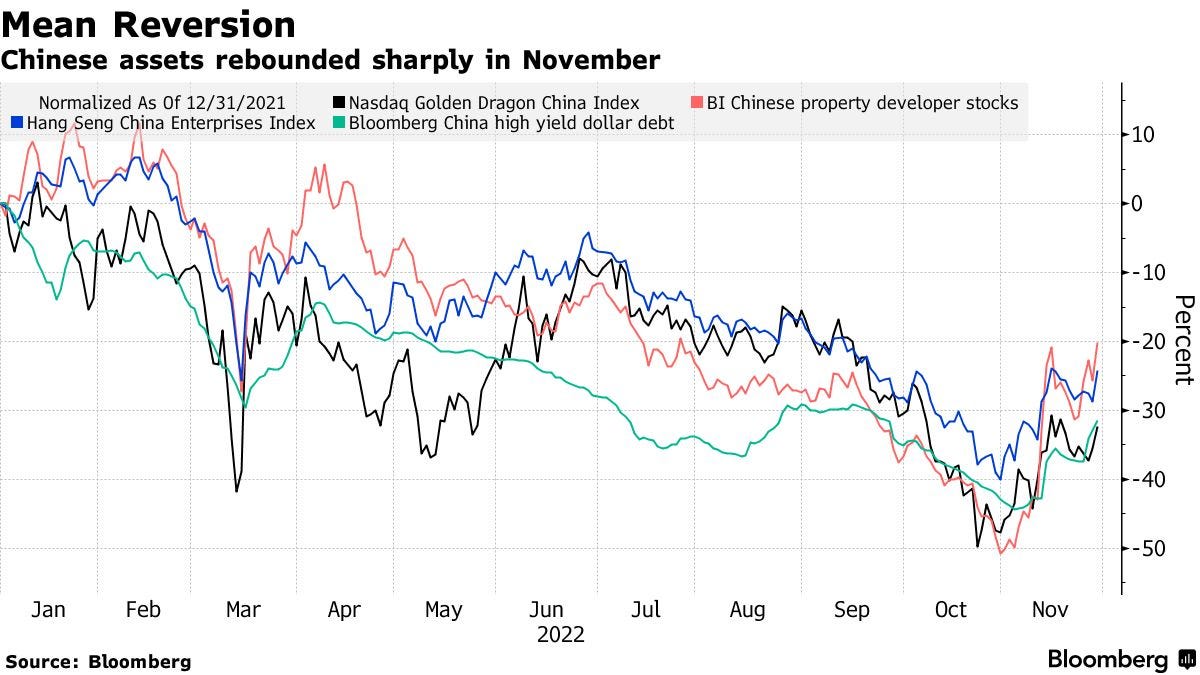

Investors have regained confidence in investing in China following the government's policy changes on two issues: easing regulations on funding sources for real estate developers and easing the Zero Covid policy.

Real estate stocks in China rose 61%. In the US, Nasdaq Golden Dragon China index rose 41%. The HSCE index on the Hong Kong exchange in November also rose at the fastest pace since 2003.

CONCLUSION

The Chinese government is expected to ease the Zero Covid policy due to pressures from last week's protests. The response from Xi Jinping's administration at this time plays a key role in determining whether these protests will be defused or escalated to a climax.

One consequence of the Zero Covid policy is that China's economy is cooling with stagnant manufacturing activity. The Central Bank wants to inject liquidity into the economy to stimulate demand for production and investment capital. However, the solution from the capital demand side of enterprises will not be thorough when consumer demand declines and factories close due to the epidemic.

However, the market has welcomed more positive news as major Chinese banks have actively participated in providing capital to real estate developers, along with easing policies from the government on capital mobilization in this sector. The Beijing government has also relaxed the Zero Covid policy. This has caused the Chinese stock market to recover rapidly in the late November period.

Comments (0)

No comments yet

Be the first to comment

Login to comment