Market Recap:

Market opened Thursday's trading session in a fairly mixed state with disappointing ER from 2 tech giants. NASDAQ dropped nearly 2% in the futures session before starting to recover right at the open today with VIX back below 30 and creating small short-covering rallies. Investor sentiment also largely continued to be supported by:

Stability in macro policies of FED and ECB, especially European investors on BoE after speech by new UK Prime Minister Rishi Sunak this morning.

Market optimism entering election season, including Q3 GDP report to be released tomorrow morning.

Clarity on corporate earnings outlook.

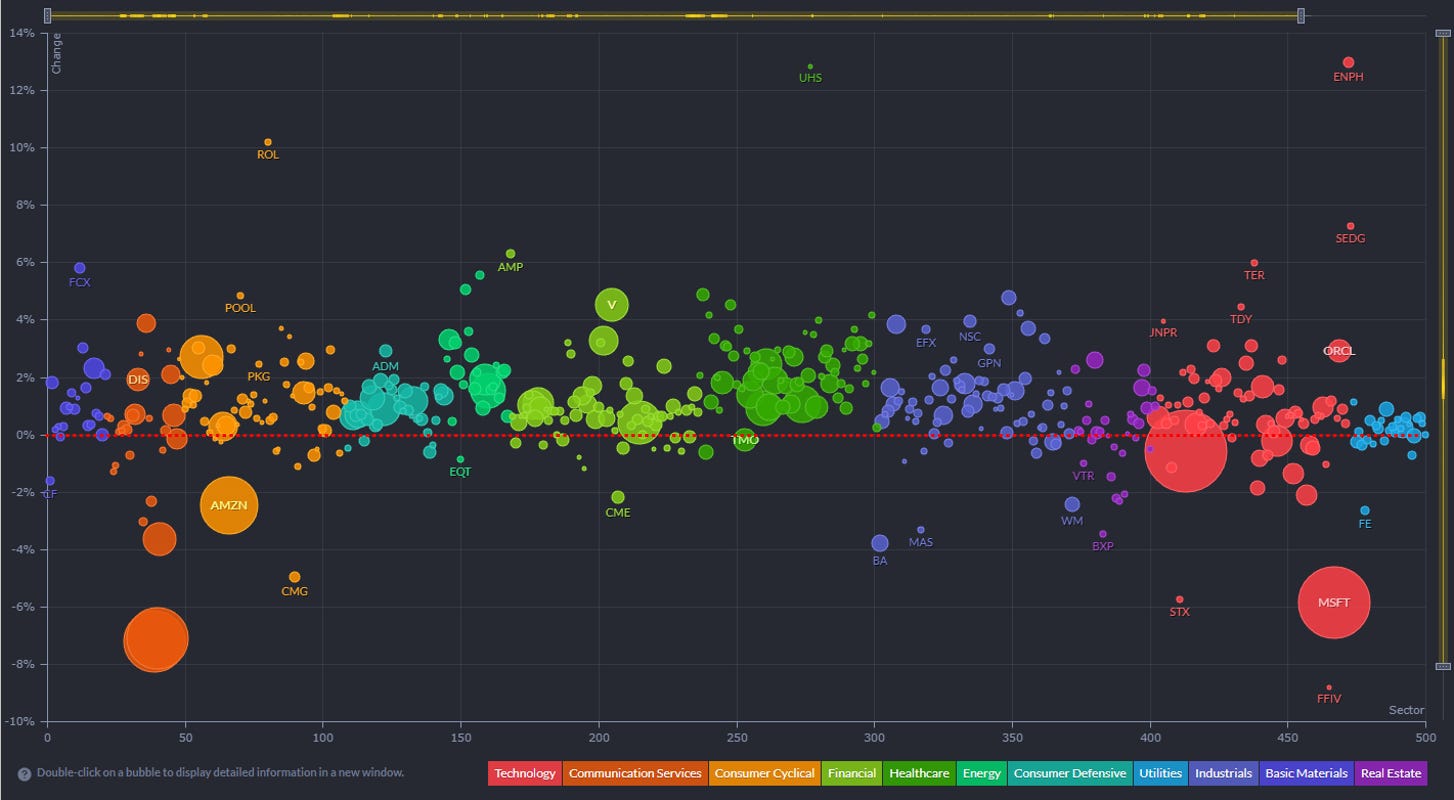

Heat map shows clear allocation of money flows with mega tech dragging the market down in the morning:

Details on yesterday's ER:

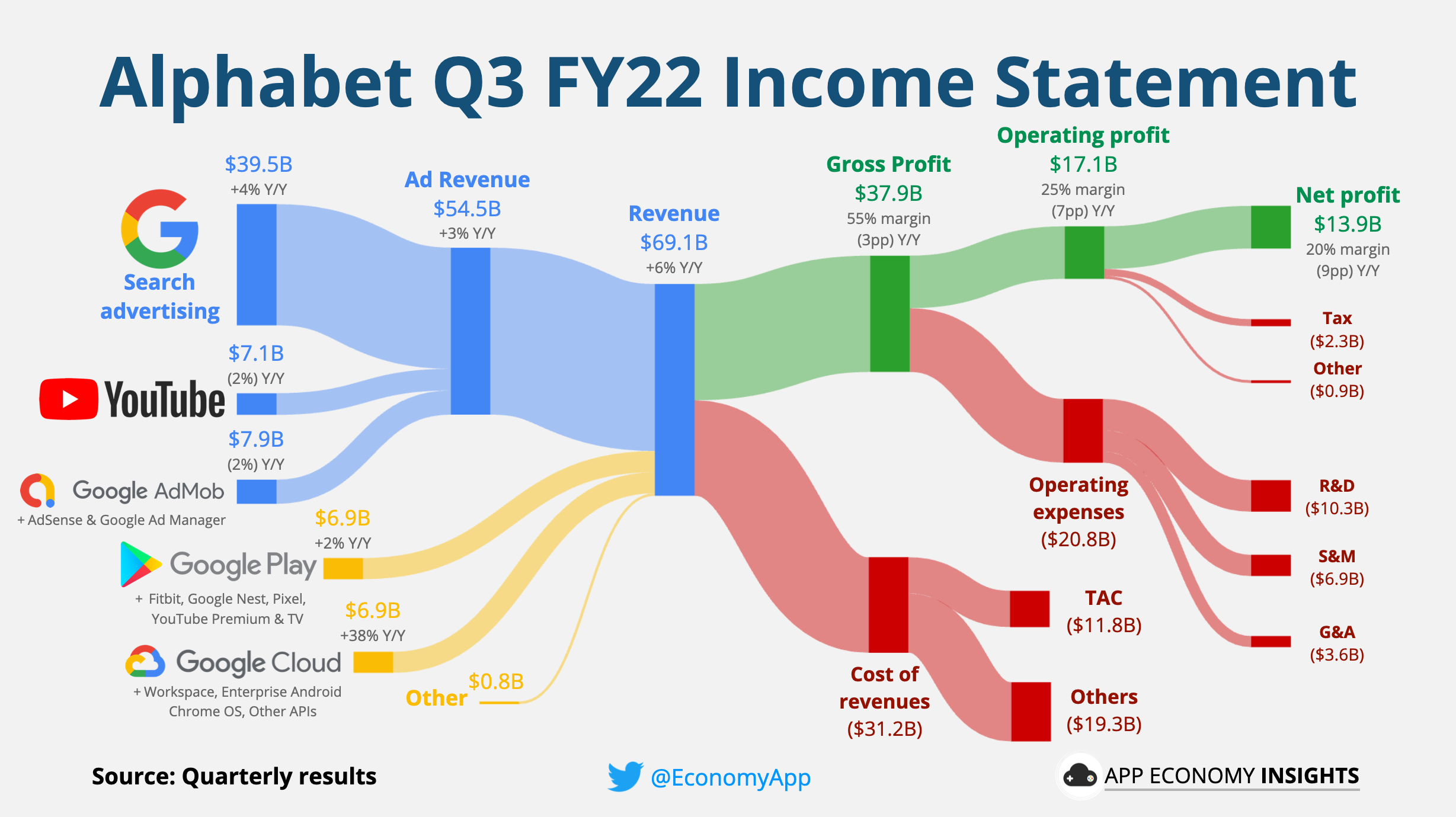

1. Alphabet Q3 FY22

Revenue by segment (growth Y/Y):

Advertising $54.5 billion (+3% Y/Y).

Google Search & other $39.5 billion (+4%).

YouTube ads $7.1 billion (-2%).

Google Network $7.9 billion (-2%).

Google Cloud $6.9 billion (+38%).

Google Other $6.9 billion (+2%).

Other $0.2 billion, and hedging $0.6 billion.

Main highlights:

Revenue +6% Y/Y $69.1 billion / +11% fx neutral (vs. $70.74 expected).

Gross margin 55% (-3pp Y/Y).

Operating margin 25% (-7pp Y/Y).

Cash flow:

Operating cash flow $23.3 billion (34% margin).

Free cash flow $16.1 billion (23% margin).

Balance sheet:

Cash, cash equivalent, and marketable securities: $139.7 billion.

Long-term debt: $28.4 billion.

Comments (0)

No comments yet

Be the first to comment

Login to comment