Midday Recap:

US stock market unexpectedly drops sharply in the second half of yesterday's trading session after Bank of England Governor Bailey said UK pension funds only have "3 days" to sell and resolve margin call issues while the government intervenes by buying bonds. Selling pressure in a low liquidity environment pushed SPY down to 356 in the afternoon.

However, last night and early this morning US time, multiple sources indicate Bank of England signaled it may accept extending bond purchases to stabilize the market, helping major indices temporarily find support in today's session.

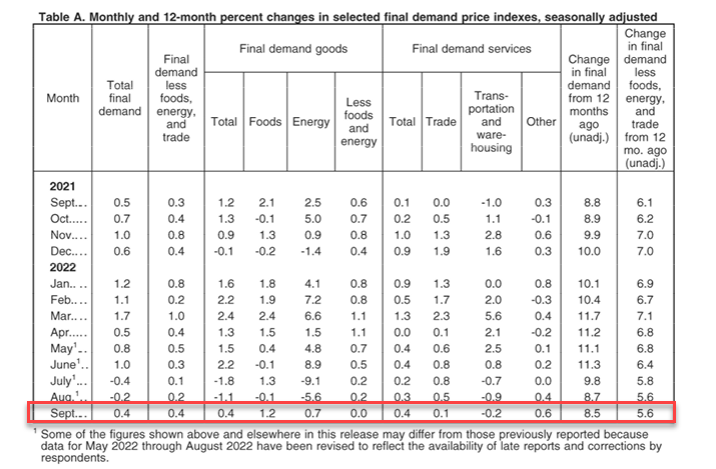

PPI index released this morning shows somewhat mixed signals with producer inflation continuing to rise high in the food sector but stabilizing somewhat in core-PPI.

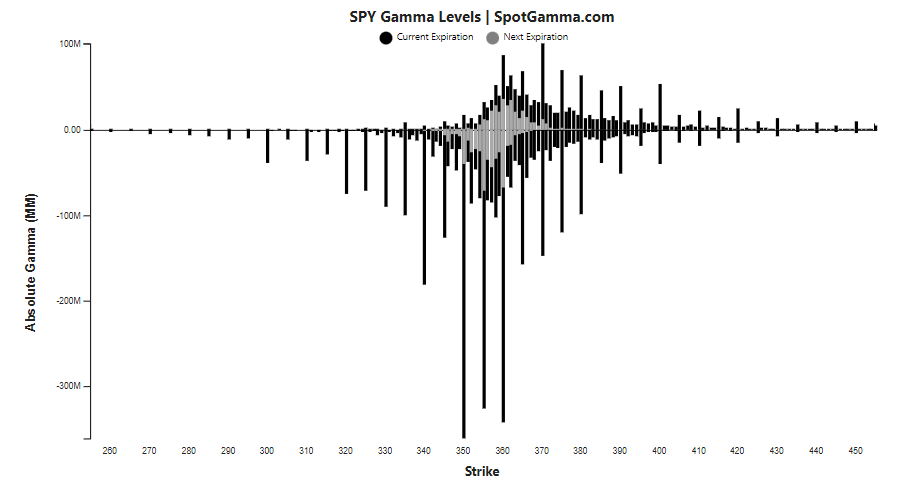

Market pushed down within an hour after PPI data release before finding support near the day's low and starting to recover towards ~360 SPY led by banks. Liquidity generally remains low, indicating investors continue sitting on the sidelines waiting for tomorrow's CPI report. Additionally, the aftermath of yesterday afternoon's hedging demand is evident with put strikes at both 350 and 360 of SPY expanding significantly, putting pressure on the current market but also potentially becoming fuel for a shorts-cover rally if buyers emerge after tomorrow's CPI. Investors should note that low liquidity always makes forecasts less accurate.

On internal flows, other markets mixed today with low liquidity and cash flow evenly distributed across all sectors.

Overall, current data still points to consolidation below 360 from now until end of day with low volatility. However, in a low liquidity environment, any news if it emerges will amplify the entire market's movement.

Comments (0)

No comments yet

Be the first to comment

Login to comment