Last week and in the coming week, US companies will successively announce Q3/2022 revenue. On this occasion, Viet Hustler will delve into analyzing the current macroeconomic situation from the supply-demand balance perspective.

In which, there are 3 main points that will be analyzed in the macroeconomic article below, including:

How changes in consumer sentiment affect the retail industry?

What do sales and profits from US companies indicate about inflation.

And the Fed's attitude towards liquidity pressure in the market.

From consumer behavior to US retail sales

Changes in consumer sentiment

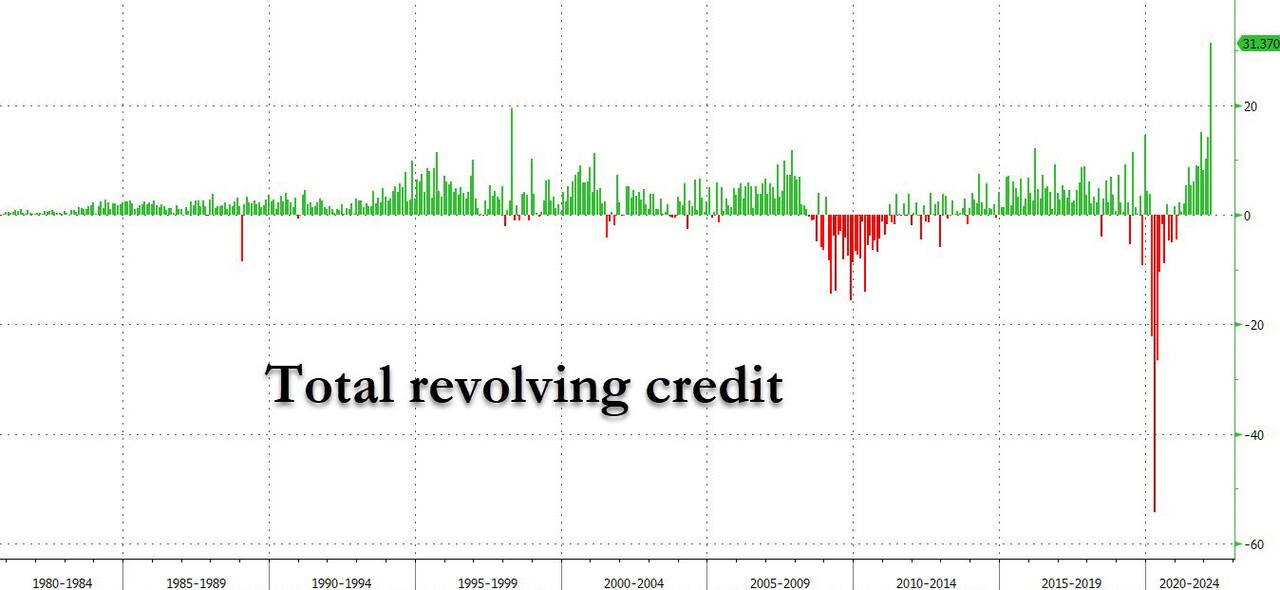

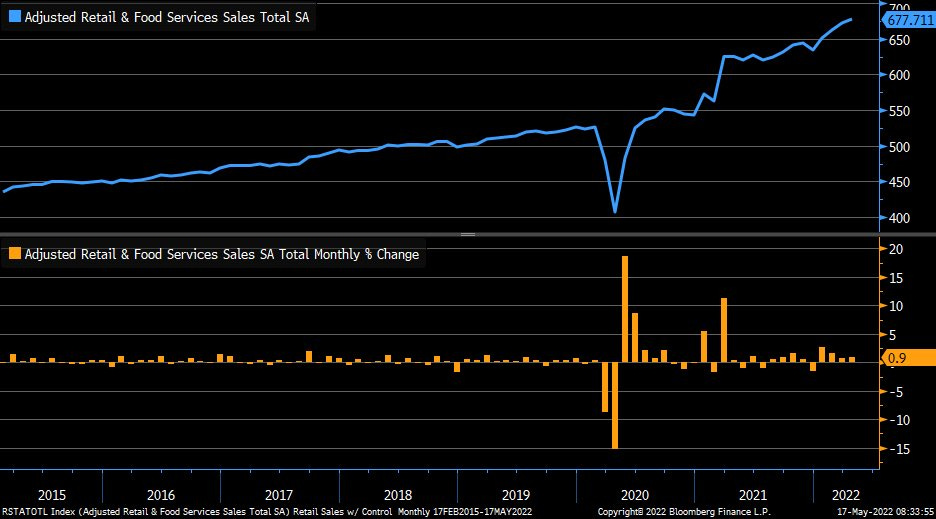

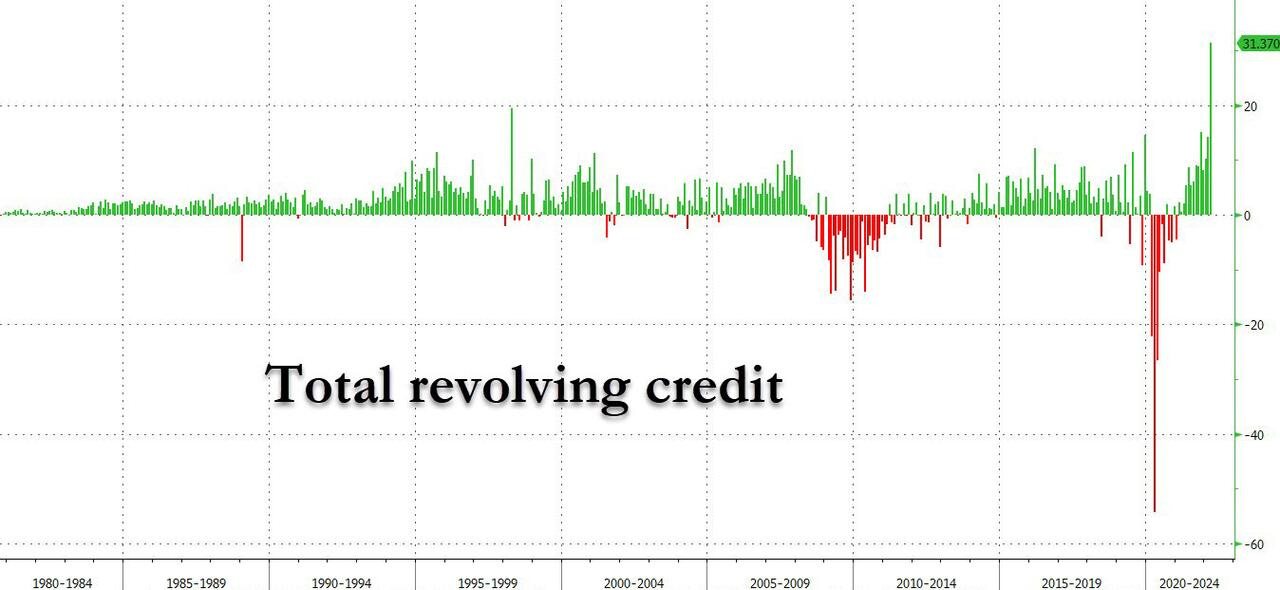

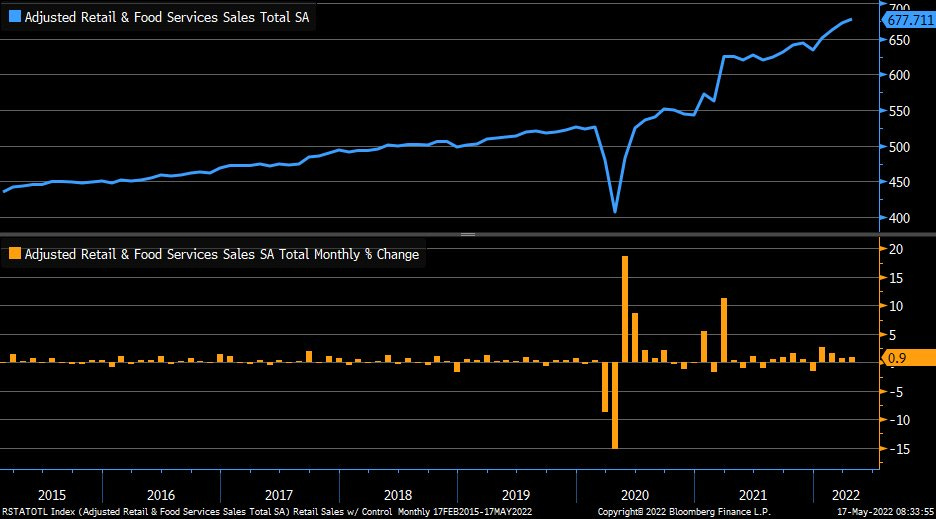

When inflation had not yet peaked in April-May, Viet Hustler analyzed the still quite optimistic consumer sentiment in spending, when they were still willing to buy goods (due to currency devaluation) and max out their credit cards. Data from May 2022:

Revolving credit among the public surged in April-May 2022

Retail data still increased high in May 2022: +0.9% m/m

However, after half a year under pressure from high inflation and Fed interest rate policy, consumer attitudes have significantly changed in shopping habits when reducing spending and choosing cheaper goods. Consequently, retail revenue decreased.

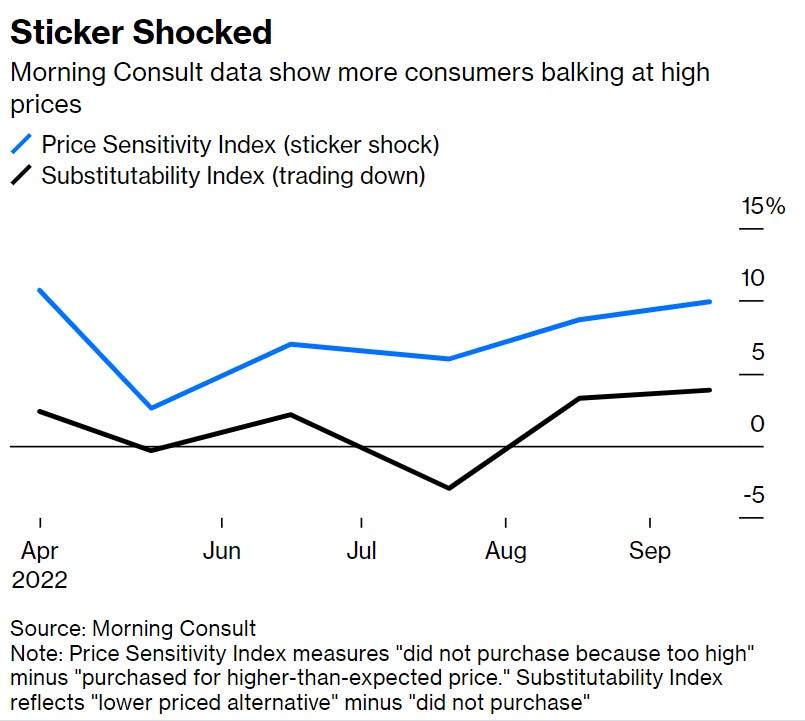

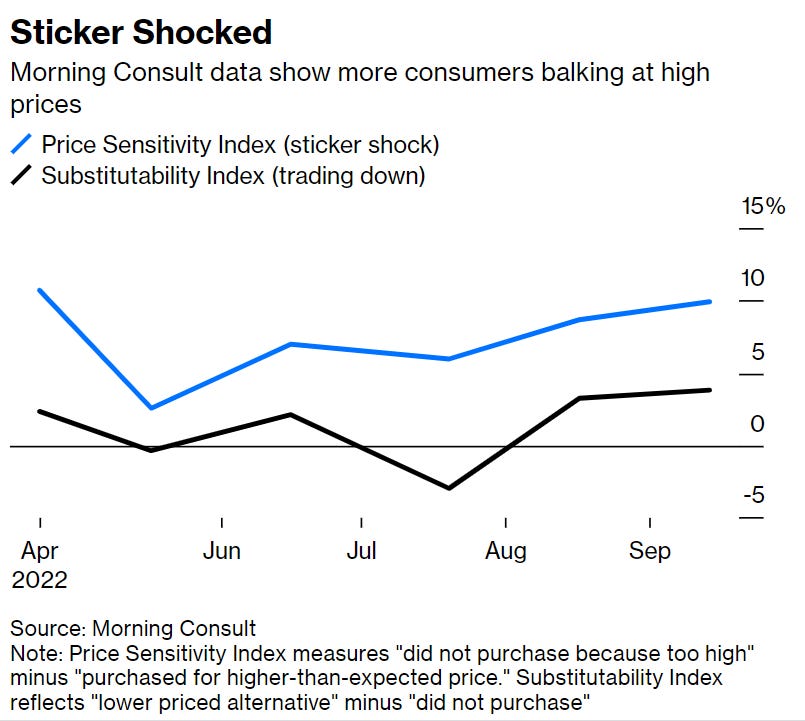

According to Bloomberg and Morning Consult survey:

The composite index of the proportion of price-shocked consumers abandoning purchases (sticker-shocked shoppers) has risen to 9.9% in September (August: 8.7%).

The rate of shoppers switching to cheaper substitute products compared to old brands (trading-down) is also quite high at 3.79% (August: 3.25%)

The trio of pressures on both sellers and buyers

Real personal spending levels (inflation-adjusted) remain high

While consumer purchasing power decreases

Consequently, real retail sales decrease

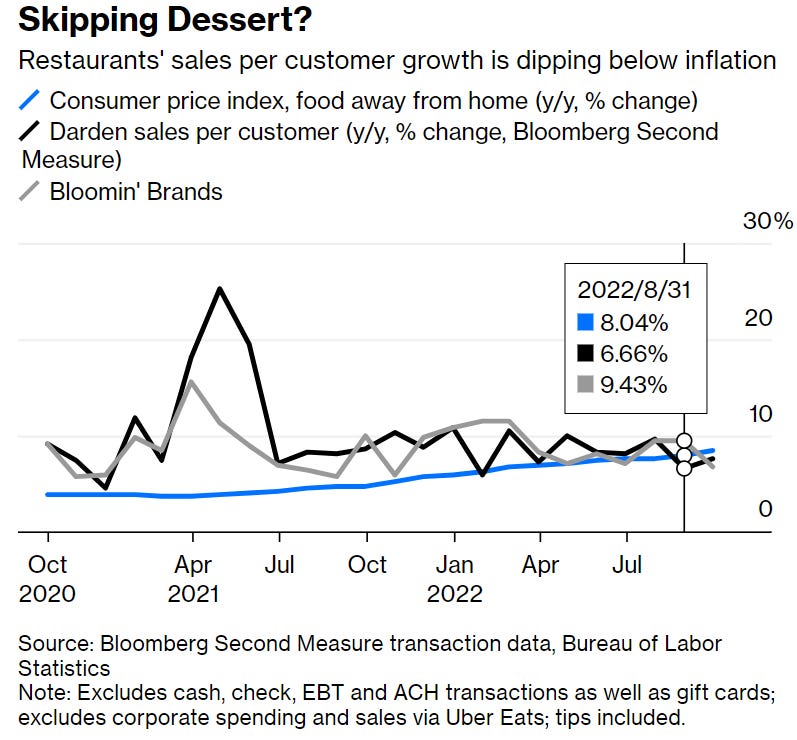

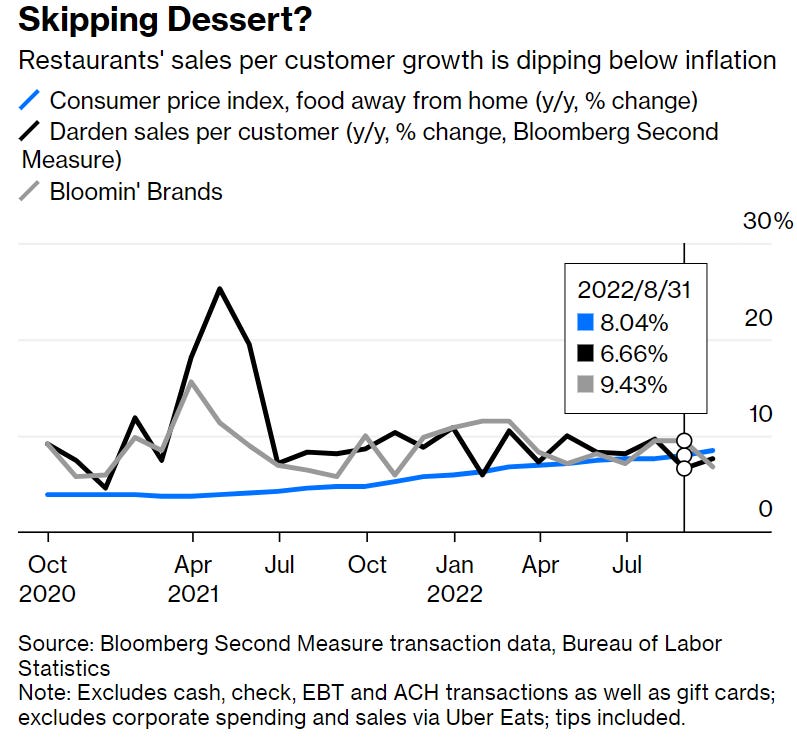

To save, people have cut back on expensive services, for example shifting habits from dining out at restaurants to eating at home. Consequently:

Although dining out costs in the CPI basket remain high, average sales per customer at restaurants have decreased (for example, the figure below shows average sales of Italian restaurant chains owned by Darden and the Bloomin' Brands restaurant group)

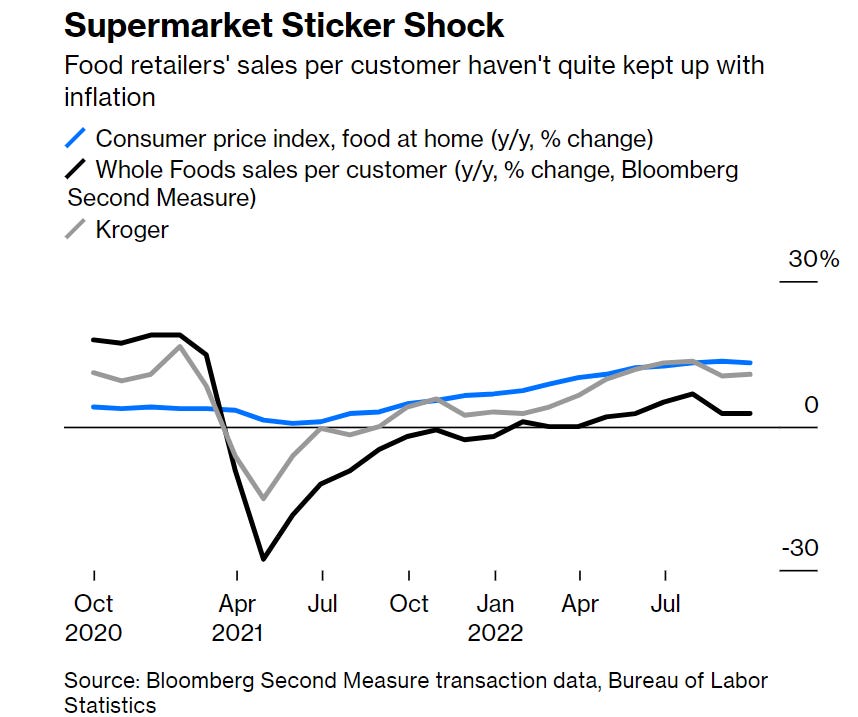

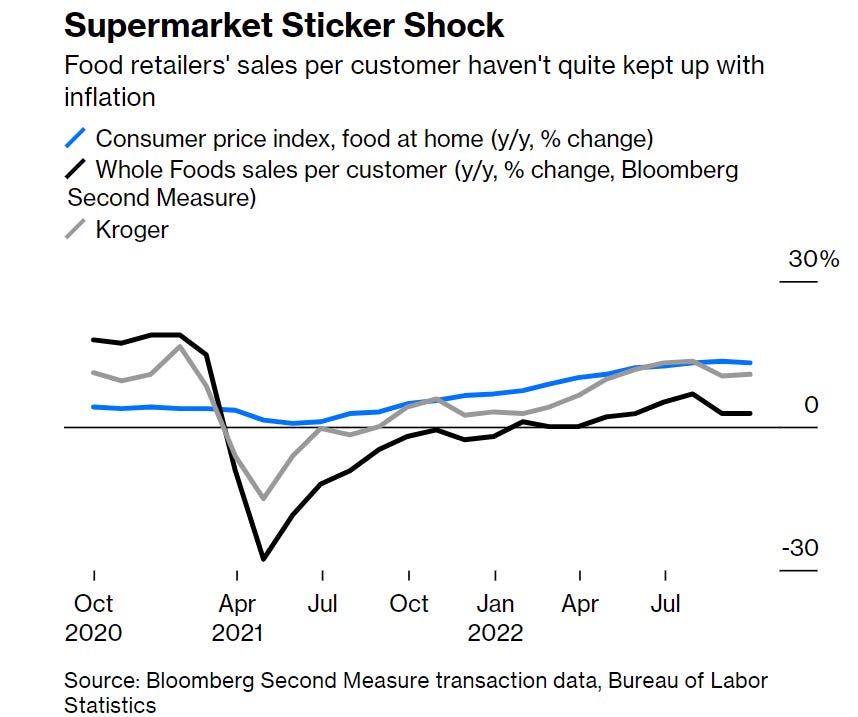

Supermarket food prices are also rising high although the increase has cooled slightly in September

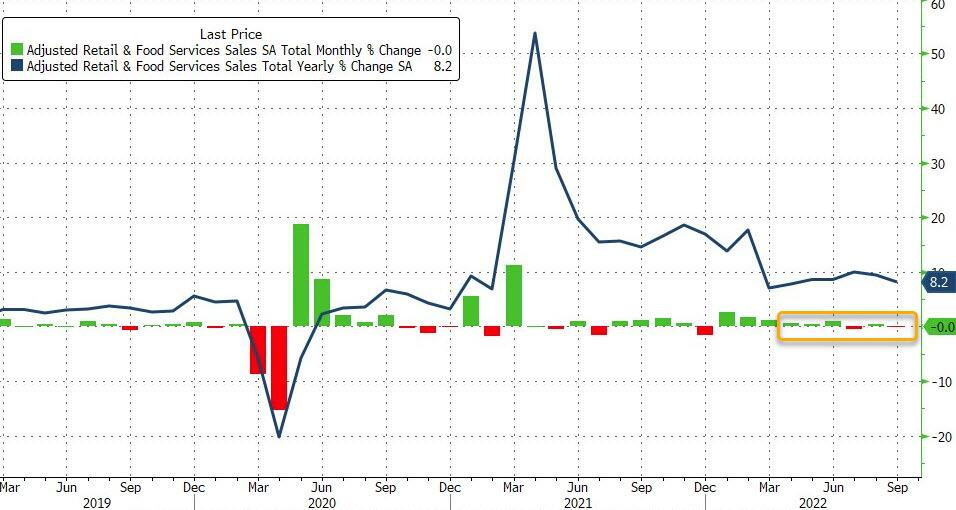

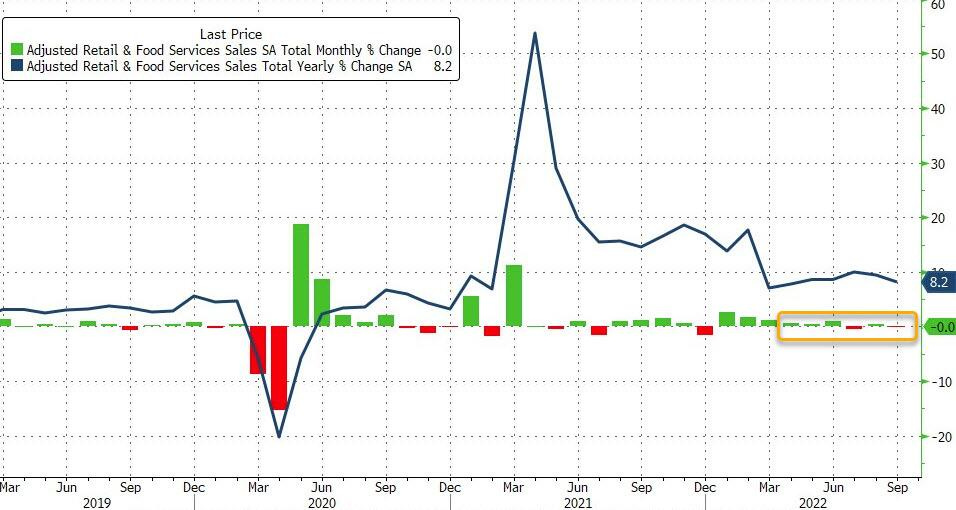

Impact from consumers on retail sales

US retail sales held flat from August to September (lower than the expected +0.2% m/m).

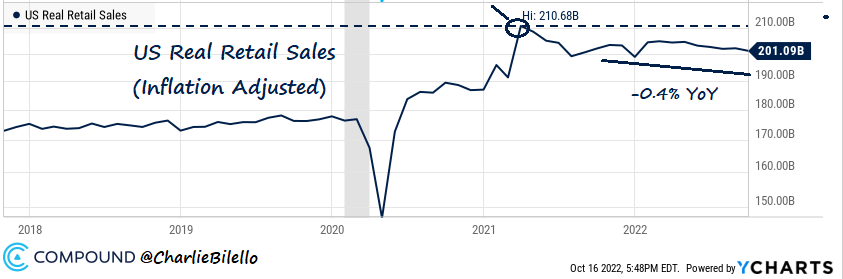

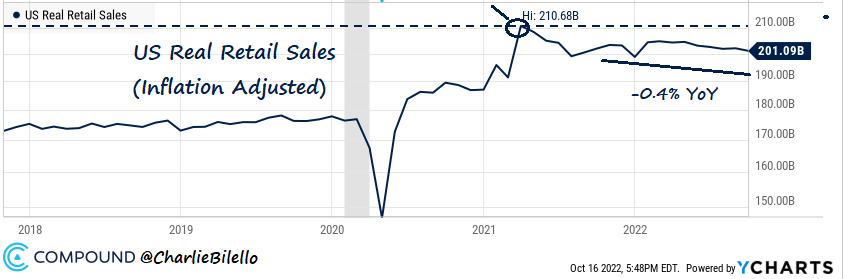

Nominally, US retail sales appear high at 8.2% y/y (figure above). But after inflation adjustment, real retail sales peaked in March 2021 and is now down -0.4% y/y.

Brick-and-mortar retail stores (excluding online sales) saw sales drop sharply -2.5% m/m. This is the largest m/m decline since May 2021.

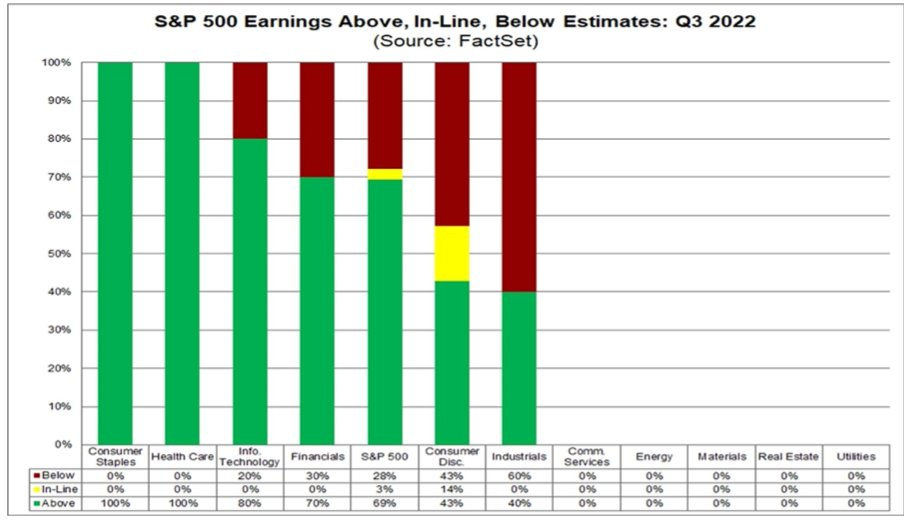

Revenue and profits of large enterprises

Inflation sentiment in businesses is keeping inflation high: Businesses continue to raise prices, leading to surging profits this year despite inflation and recession.

Perhaps, this is also one of the reasons why corporate hiring remains high relative to the current inflation situation.

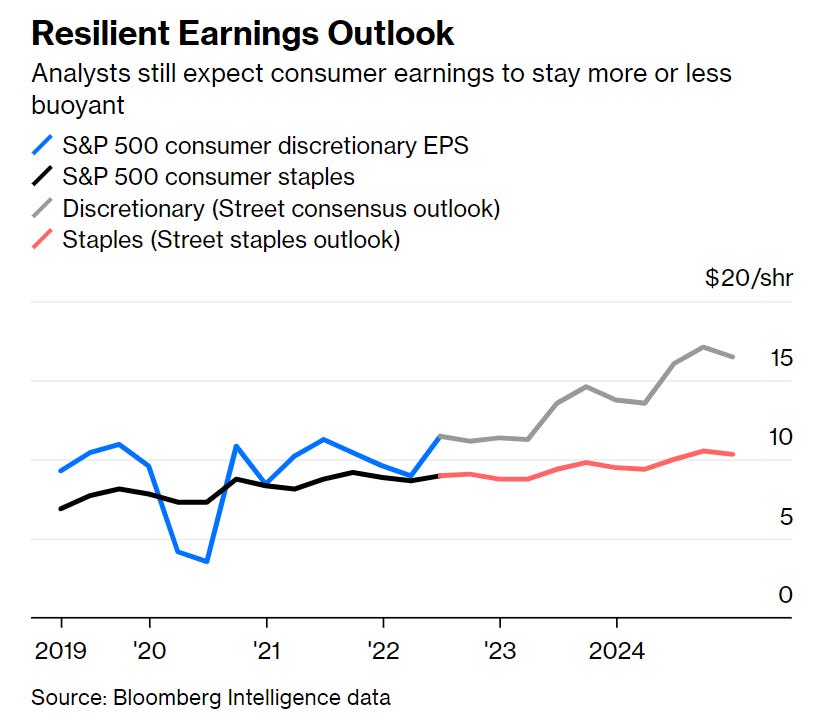

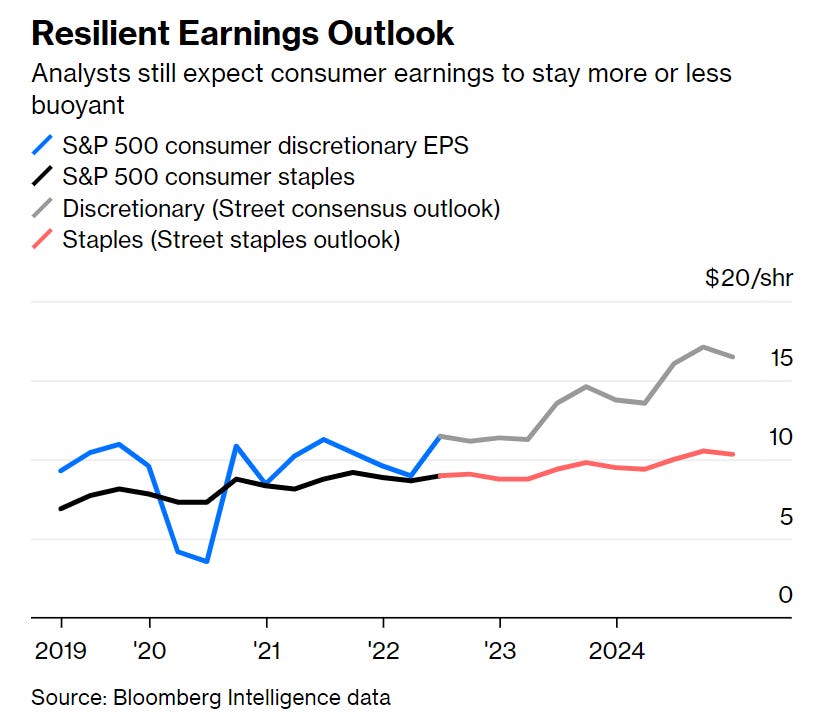

Amid inflation, Wall Street continues to announce optimistic earnings outlooks for S&P 500 companies next year, including sensitive businesses in essential consumer goods.

US corporate profits surged, with the largest increase since 1950, wherein after-tax profits of US companies rose 10.4% in Q2/2022.

Last week, Q3 revenue for some large tech companies was announced with quite positive figures exceeding expectations. Next week, other tech companies will also successively report Q3 revenue

IBM: $14.1B (+6% y/y)

Tesla: $21.5B (+56% y/y)…

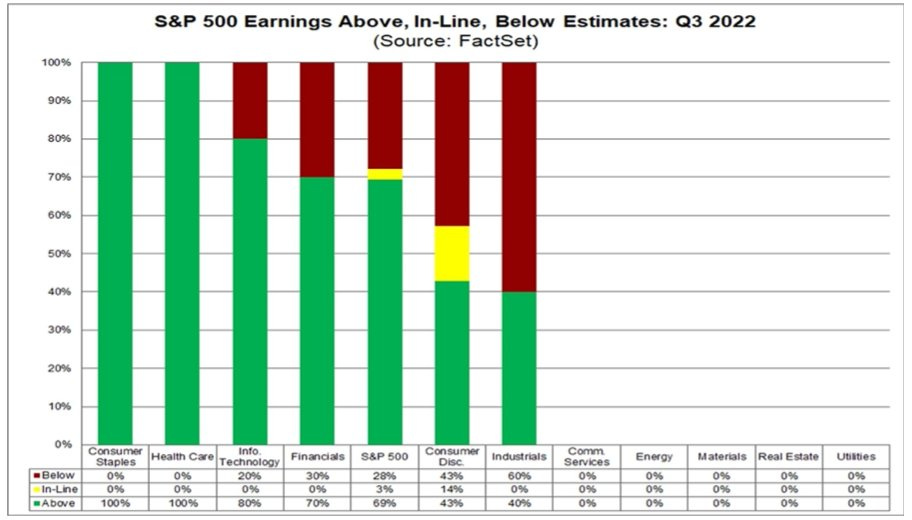

Previously, predictions for Q3 revenue of S&P 500 companies

Next week, other large enterprises will also successively announce Q3 revenue.

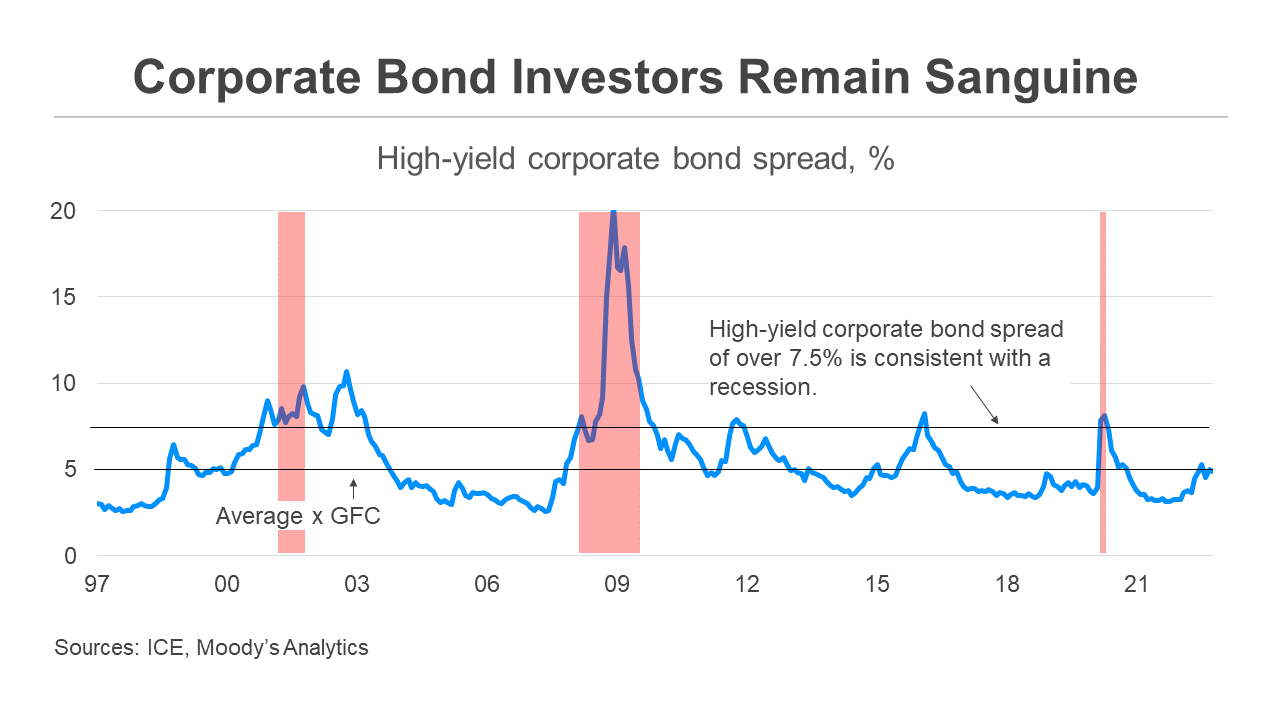

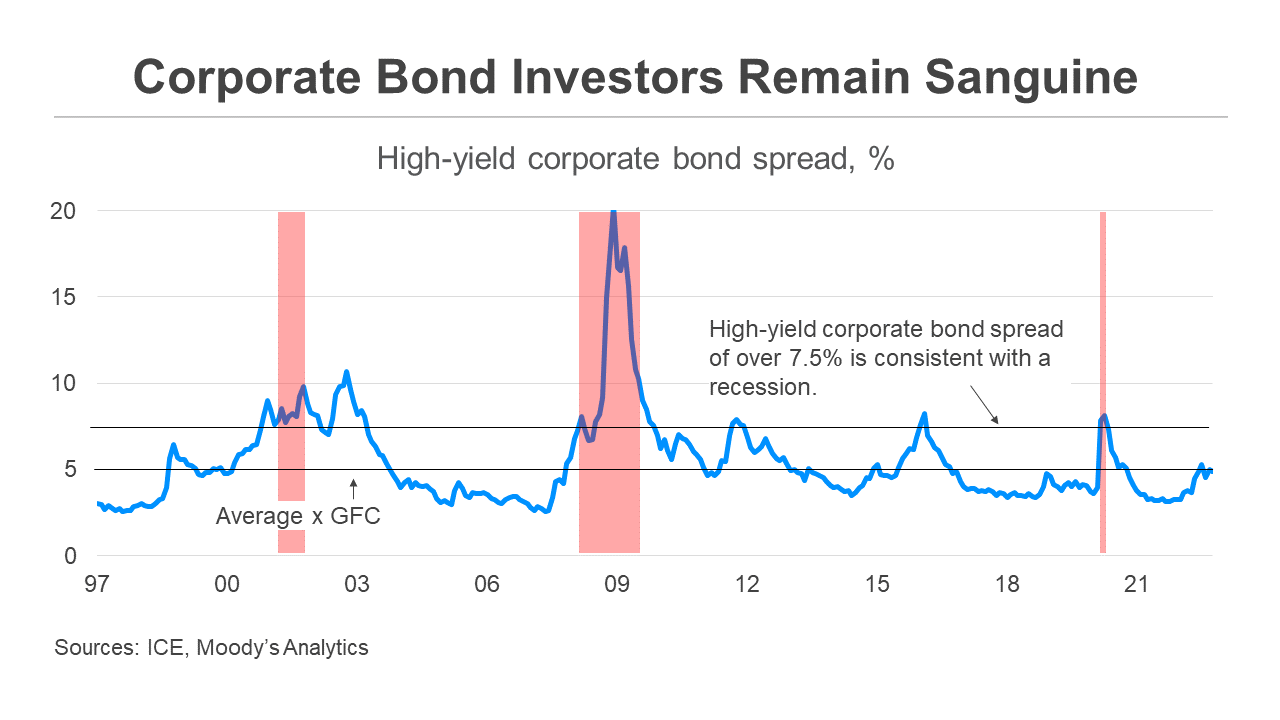

Yields on “young” corporate bonds (high-yield bond) remain at ~5%, much lower than the recession warning level (7.5%).

Normally, ahead of recession risks, besides stock declines, yields on young corporate bonds also rise as they are high-risk assets next to bonds.

However, the above data shows that corporate bond investors are not very concerned about recession risks.

Latest update on Fed's attitude towards market liquidity

The Fed's sale of assets on its balance sheet, especially Reverse Repos, has made market liquidity increasingly tighter.

The liquidity crisis from Reverse Repo was forecasted by Viet Hustler 1 year ago in the video below:

Last week, amid pressure from the financial markets, Mary C. Daly, President of the San Francisco Fed, said that the Fed will consider reducing the interest rate hike to 0.50% - 0.25% per hike.

The market expects the Fed to start easing next year, but in reality, the Fed's interest rate policy has not yet caught up to curb inflation, so the Fed's monetary policy easing will also carry many risks.

In addition, monetary policy needs time to impact the entire economy.

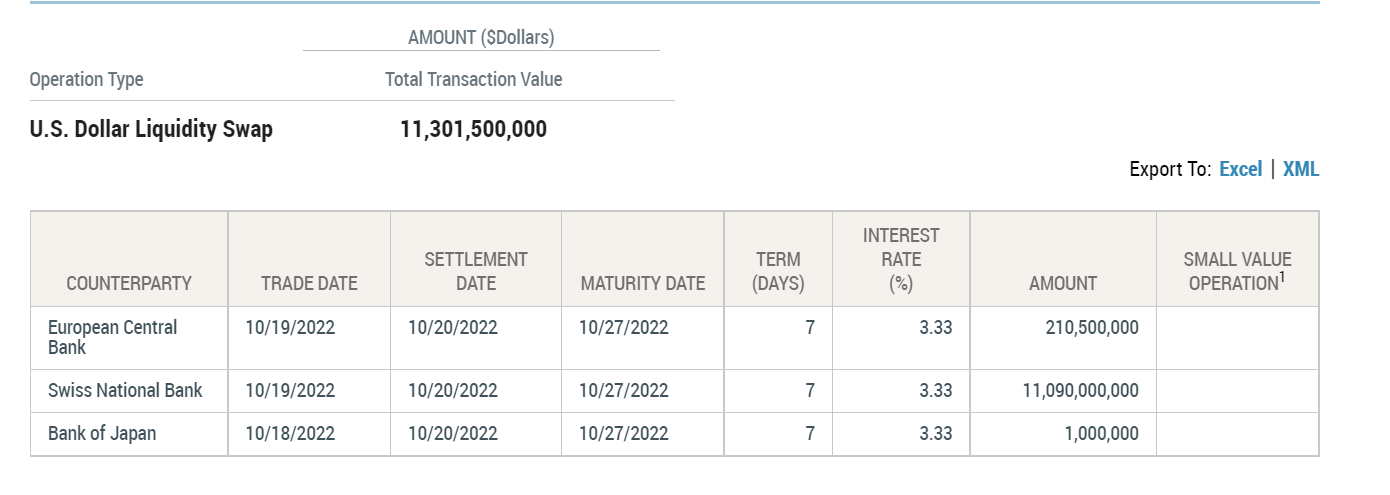

In addition, facing the pressure of a possible banking crisis from the collapse of large banks (currently with the highest risk from Credit Suisse), the Fed is forced to implement liquidity swaps, sending an additional 11.3 billion USD to Europe and Japan.

This is to protect liquidity in foreign markets to avoid the collapse of the global banking and forex system, however it will make the USD even scarcer in the domestic US market.

Articles explaining the crisis situation in Europe and Japan.

CONCLUSION

There are 3 main points in this week's macroeconomic article

(1) Facing prolonged inflation pressure, consumers have changed their shopping habits. This directly affects US retail sales.

(2) However, revenue and profits of US businesses remain very promising. This keeps investor sentiment from being significantly affected. However, the excessively high profits of companies selling essential goods serve as a warning bell that inflation may persist due to inflationary mindset from the businesses themselves.

(3) The FED has begun to clearly recognize the pressure in the financial markets and its impact on businesses. Therefore, the Fed may be considering slowing down the pace of interest rate hikes.

However, with its position steering the world's largest economy, the Fed also has another concern called “banking crisis” on a global scale.

Comments (0)

No comments yet

Be the first to comment

Login to comment