It has been 10 years since the famous "whatever it takes" statement by former European Central Bank (ECB) President Mario Draghi in 2012, in the battle to defend the Euro and the European Monetary Union (Eurozone). The ECB is once again in crisis as it faces soaring inflation along with rising public debt and Market Fragmentation risk (fragmentation risk).

Can the ECB solve these three problems? This week, Viet Hustler will "change the wind" for readers with analyses of the macroeconomic situation in Europe and the ECB's direction in the fight against inflation and protecting the common currency Euro in the region.

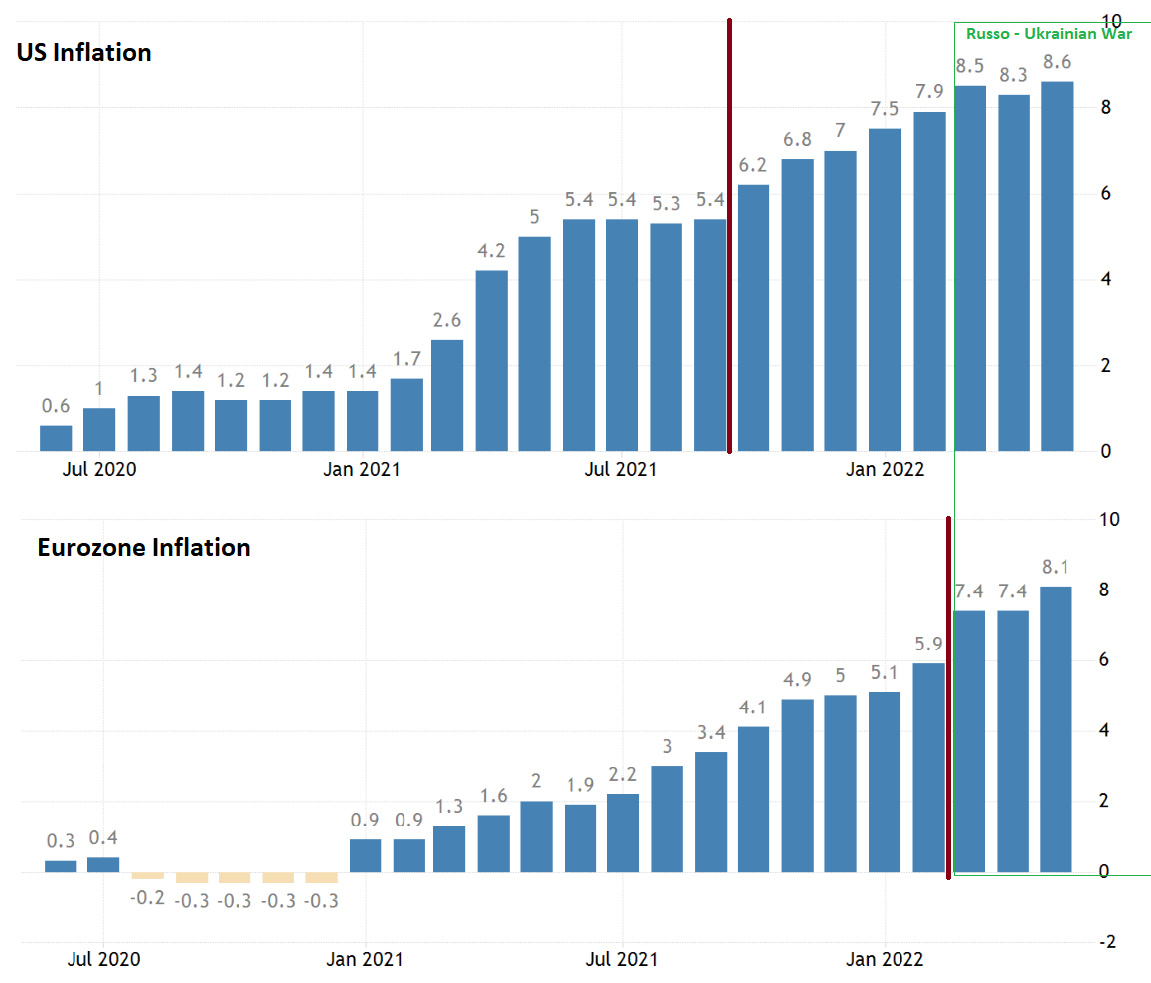

Correlation between inflation in the EU and the US

Differences in the nature of inflation in the US and Europe

Inflation in the US mainly stems from all 3 supply shocks: pandemic, China's Zero Covid policy, and the war between Russia and Ukraine. Meanwhile, inflation in Europe is largely influenced by the Russia-Ukraine war. This is clearly reflected in the components of CPI and monthly CPI growth rates:

Headline inflation in May 2022 was quite similar in both regions: US 8.6%, Eurozone 8.1%. However, in terms of speed:

Inflation in the US exceeded 6% from October 2021, following Biden's delay in deciding to reappoint Powell as FED Chairman.

Meanwhile, inflation in the Eurozone only truly exceeded 6% from February 2022 after Russia officially invaded Ukraine.

Core CPI growth (excluding food and energy) in the Eurozone in May was only at 3.8%, much lower than the US (6.0%)

This shows that inflation in Europe is mostly due to the impact of rising prices of food and energy items

Rising energy prices account for a large proportion in the inflation growth rate in the Eurozone from the beginning of 2022 compared to the US, mainly due to European countries' dependence on Russian energy.

Europe's energy dependence on Russia

The EU's energy dependence issue is truly "new bottle old wine" and is no longer unfamiliar to both the US and countries on the Old Continent.

This cartoon was circulated in the Chicago Sun-Times newspaper in 1982 during the Cold War.

The content of the cartoon mainly serves as a US warning to its allies on this continent that: Europe's energy dependence will provide fuel for the Soviet Union's "war machine."

…. And that is still true to this day.

2020 statistics show that EU countries imported up to 60% of their energy products. Of which, 38% of natural gas and 23% of oil imports into the EU originated from Russia. In particular, Eurozone countries (European common currency area) import 40% - 100% of natural gas for household and production use from Russia.

It can be said that stopping imports of natural gas and energy from Russia is the cause of soaring inflation and economic recession in Europe, because this region is heavily dependent on energy for production and daily life. Energy supply pressure will be even greater for Europe when winter comes.

Countries in this region, especially Germany and Italy, have introduced countermeasures to replace Russian natural gas with liquefied natural gas (LNG). LNG can be imported from other suppliers from the US and Australia…

Rising energy prices are gradually affecting the prices of other goods, not just energy. Mario Draghi, former ECB President, said that the Eurozone is "shifting from energy-dependent inflation to inflation dependent on other goods. Price increases are spreading rapidly across many other product groups."

Has the EU truly entered a Stagflation cycle?

If economists only suspect the risk of Stagflation in the US, then for Europe, they truly believe that stagflation is already in its early stage. If Stagflation is defined by soaring inflation, declining industrial output (economic stagnation), and deteriorating labor market; the Eurozone has all 3 signs.

Manufacturing activity in the Eurozone has entered a recession trajectory:

The PMI Index for manufacturing output has begun to enter a negative cycle.

Meanwhile, industrial manufacturing output growth rate and inventory PMI index have been negative since the beginning of the year, equivalent to previous economic recessions in Europe.

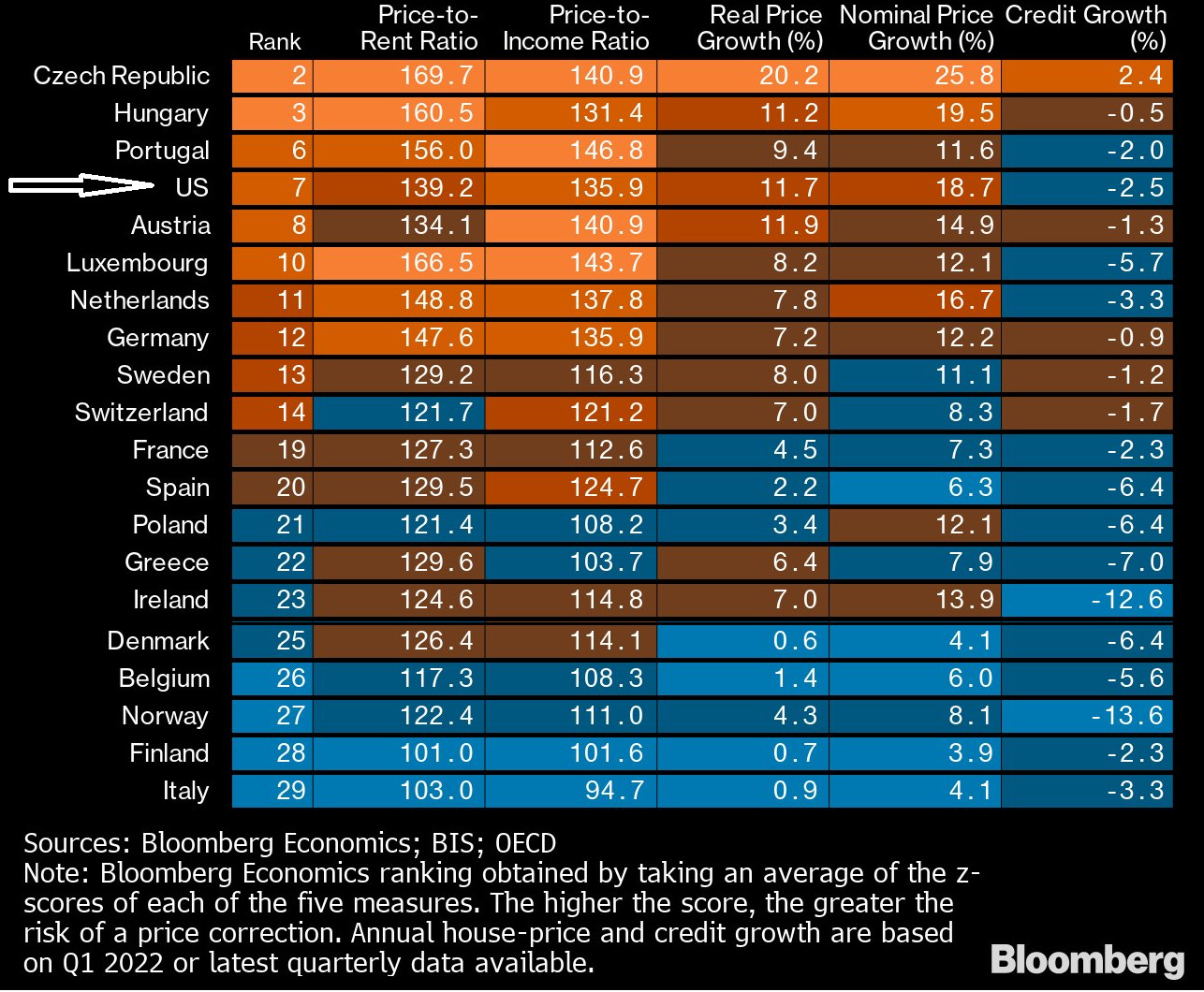

High inflation is leading to rising living costs in Europe: the correlation ratio between prices and housing costs, between prices and income in some European countries is at alarming levels.

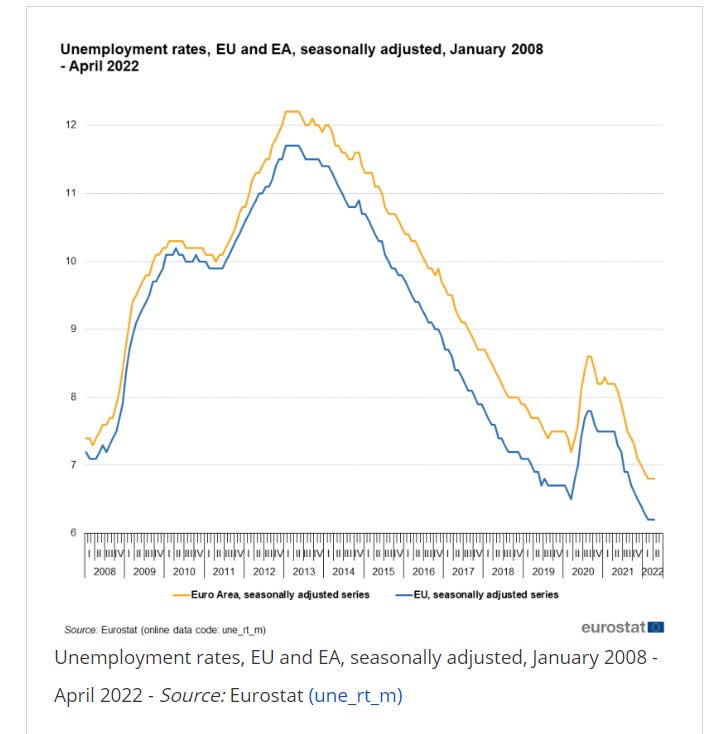

In particular, the European labor market is quite unique: although unemployment is low, it has the appearance of stagflation because workers are always in a dependent position with relatively low wages compared to the UK and the US.

In the Eurozone, costs are rising but workers' wages are not increasing. The reasons are:

Abundant labor supply from immigrants and refugees pulls down the basic wage.

Workers are heavily dependent on businesses to maintain their jobs during the pandemic, so they also find it difficult to demand higher wages when businesses resume production in this phase.

The unemployment rate remains low due to 3 reasons:

Workers in Europe are protected by trade unions, so mass layoffs are quite rare in this region.

Companies are still receiving benefits from low interest rates and support packages during the pandemic to maintain production.

In fact, the European Central Bank (ECB) has 2 options:

Aggressively increase interest rates like the US and quickly curb inflation but push the economy into recession and stagflation risks.

However, for 11 consecutive years, the base interest rate in the Eurozone has always been at 0% or lower. The current interest rate is at -0.5%. A sudden interest rate hike in the bloc will cause a major unpredictable shock to the economy.

Design a more “sustainable” recession path by gradually increasing interest rates.

If following this path, ECB must accept a period of high inflation but the recession impact will be mitigated and not cause too big a shock to the economy.

Based on the press release dated 06/09 about the plan to raise interest rates by 25bps in July and forecasts on growth or inflation, it seems ECB has chosen the second path and accepted the lag of monetary policy compared to the speed of inflation.

However, in reality, ECB's regulation of the European monetary union area is much more difficult than the US FED because Eurozone is an area using a common monetary policy from ECB but affected by different fiscal policies of local governments. Therefore, the transmission of monetary policy from ECB and the impact of these policies on member countries are vastly different.

ECB's press release immediately created the “latent” risk of the Eurozone bloc named Market Fragmentation Risk (Fragmentation risk).

Fragmentation risk – a risk unique to the Eurozone

What is Fragmentation risk? Why is it concerning for Eurozone?

Fragmentation risk has actually always existed throughout the crises of the Eurozone since its inception, however, this risk was first named in ECB's 2021 strategic vision report. Accordingly:

Fragmentation risk is the sudden surge in sovereign bond spread (government bond yield spread) issued by some member states in the European monetary union (Eurozone), even though the fundamental economic indicators (fundamentals) of these countries remain at safe levels.

Bond spread (or credit spread) is the difference in yield of a bond (bond yield) compared to the yield of another standard bond with the same maturity but lower risk.

Bond spread is used to assess the relative risk level of a specific bond compared to a safer standard bond.

In the Eurozone, to assess the risk of government bonds, investors typically use the bond spread between that country's government bonds and German government bonds (German bunds), the leading economy in the Eurozone.

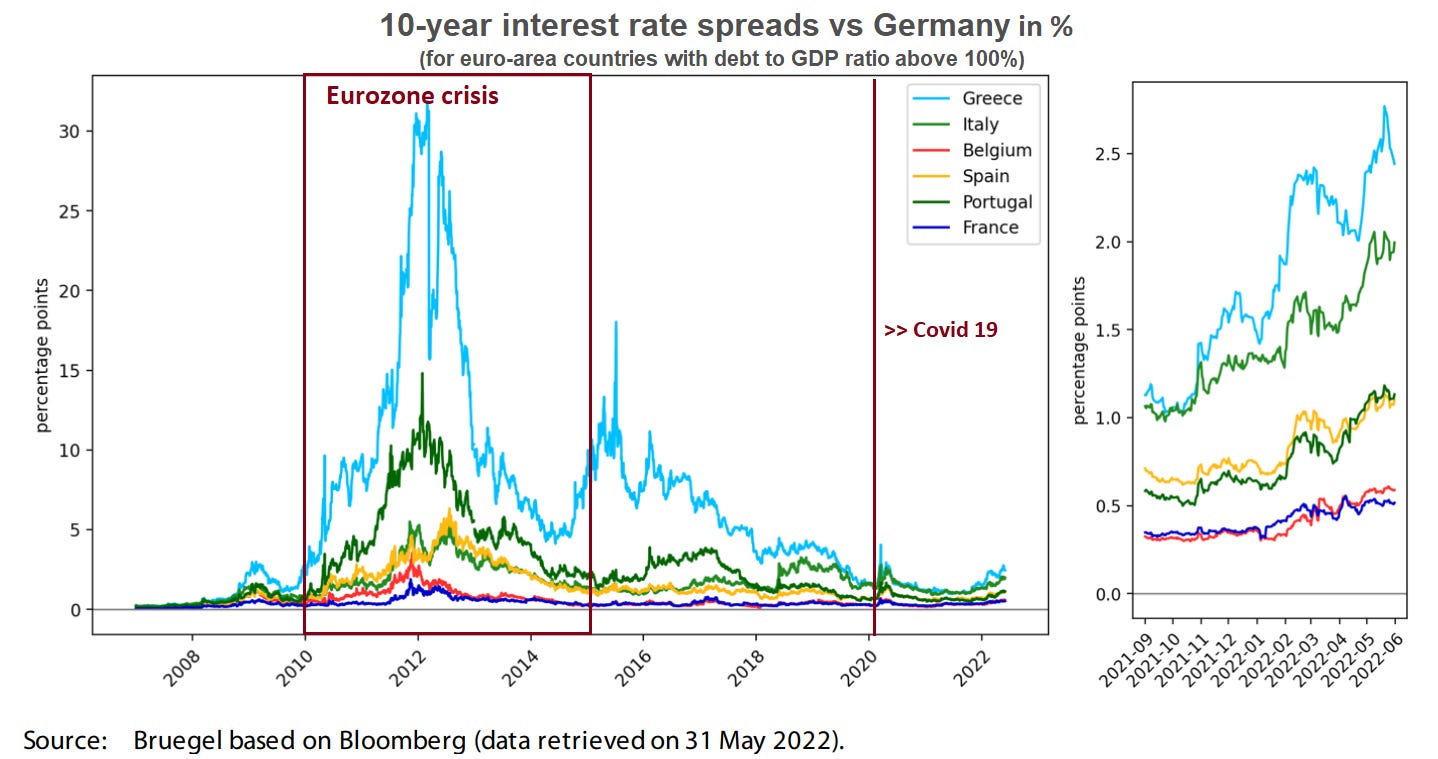

After ECB's press release on 06/09, Italy's 10-year government bond yield rose to the highest level in the past 8 years. Notably, the bond spreads of Italy and Spain (versus German bonds) have risen to record levels, raising concerns about fragmentation risk that will actually become more severe after ECB officially raises interest rates in July.

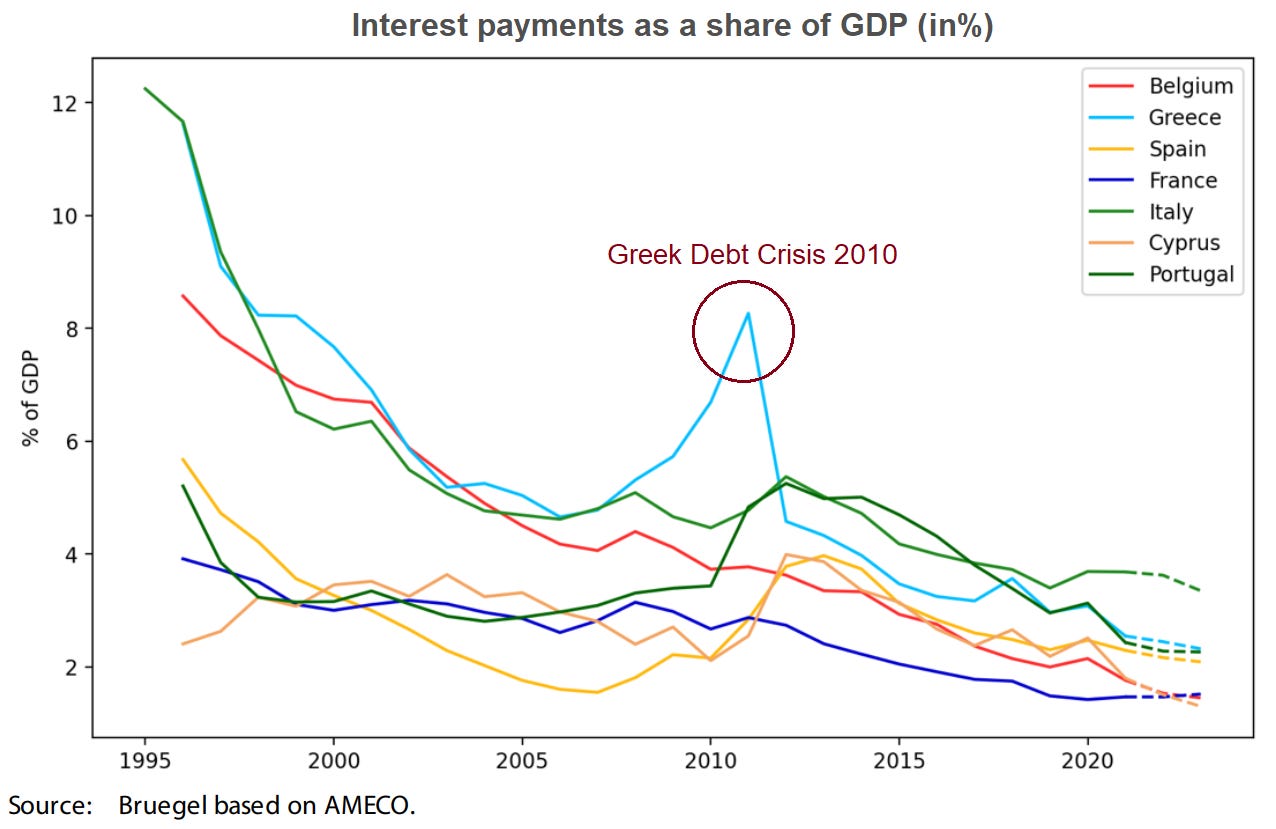

In fact, fragmentation risk always existed throughout the Eurozone's crisis periods because: Bond spreads of the group of countries Greece, Italy, Spain, Portugal, and Belgium always tended to rise during past crises, especially during the European sovereign debt crisis (2012-2015).

Fragmentation risk pushes up the yields of bonds from some Eurozone member countries, making it difficult for these countries to borrow.

In addition, the cost of servicing interest on government debt will increase, leading to default risks for these countries. A typical case is Greece in 2010.

Why does fragmentation risk exist in the Eurozone?

As mentioned above, fragmentation risk is a unique risk of the Eurozone where monetary policy for 19 countries in the bloc is regulated by ECB, while fiscal policy is determined by each member's government. This creates disparities in bad debt risks among some countries.

There are 3 direct causes leading to the rapid increase in sovereign bond spread:

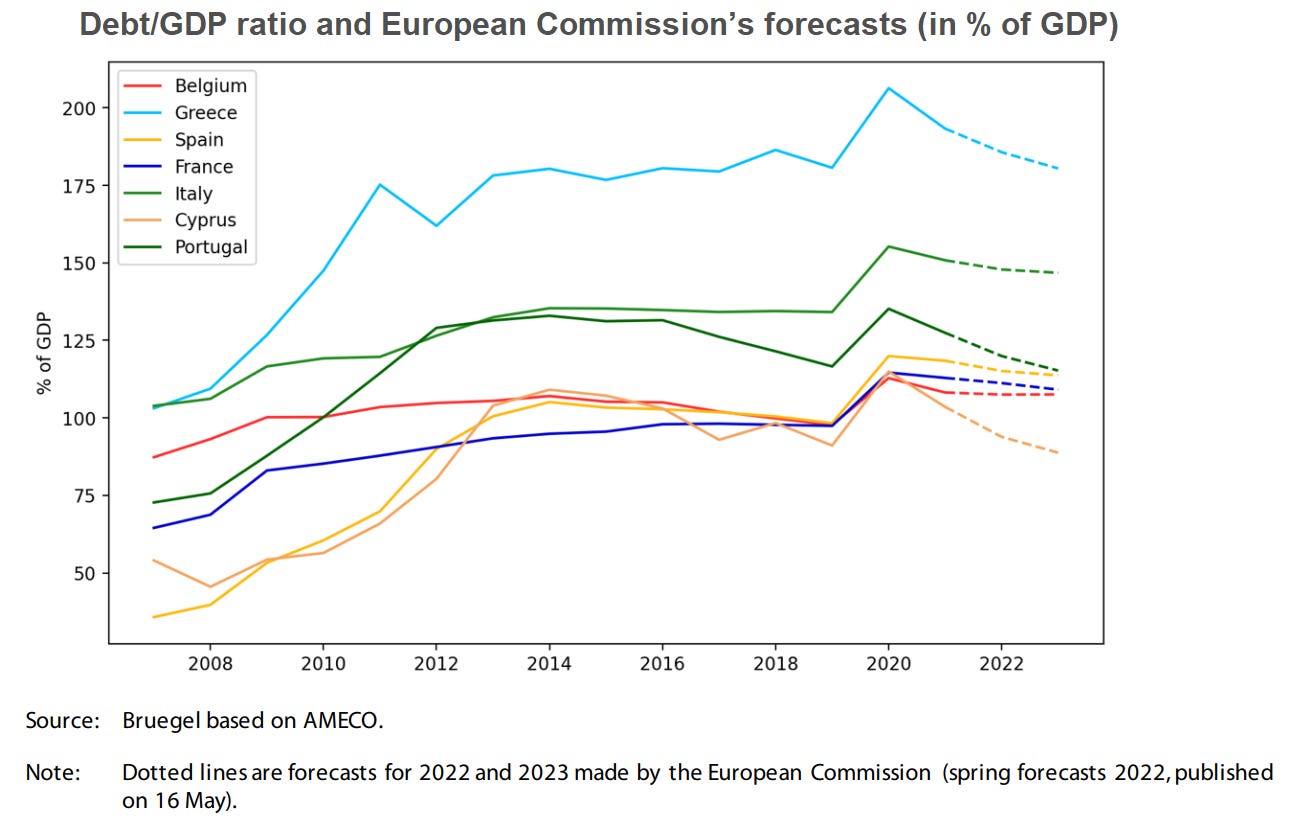

(1) A country's debt ratio (over total GDP) rises high which is both a consequence and a cause of the bond spread increase:

An increase in the debt-to-GDP ratio raises the default probability of that country. This makes bond investors cautious and demand higher yields to compensate for the risk level of these bonds.

Debt ratios of high bond spread “risk” countries like Italy and Greece are always over 100% GDP

(2) Redenomination risk due to the Eurozone breakup risk:

During periods of market stress, the likelihood of the European monetary union disintegrating increases. Euro-denominated debts could be repaid in a lower-value local currency. Therefore, the market demands higher yields for bonds issued by weaker economies in the bloc.

(3) Reason from the Collateral Framework for collateral assets (ECB’s Collateral Framework)

Over 11 years, ECB maintained interest rates at 0 or below and the Eurosystem to create a high-liquidity environment in the interbank market:

Under Eurosystem, commercial banks can borrow from ECB and central banks in member states. However, these loans must be backed by “safe” collateral as stipulated in ECB’s Collateral Framework.

What is “safe collateral”? ECB’s Collateral Framework defines safe collateral if the issuing organization must have a high credit rating, evaluated by independent private credit rating agencies.

This is precisely the key issue causing fragmentation risk because:

Private credit rating agencies tend to downgrade the credit ratings of some countries due to high debt ratios.

However, from a macroeconomic perspective, if economic growth (g) is still higher than the borrowing interest rate (r), then these countries are still in the safe debt zone and should continue borrowing to support growth.

Therefore, the credit rating downgrade of these countries' government bonds does not reflect their actual default risk, but rather the credit rating downgrade itself pushes these countries into a default situation.

Actions of the European Central Bank

Addressing inflation: Moderately tight monetary policy

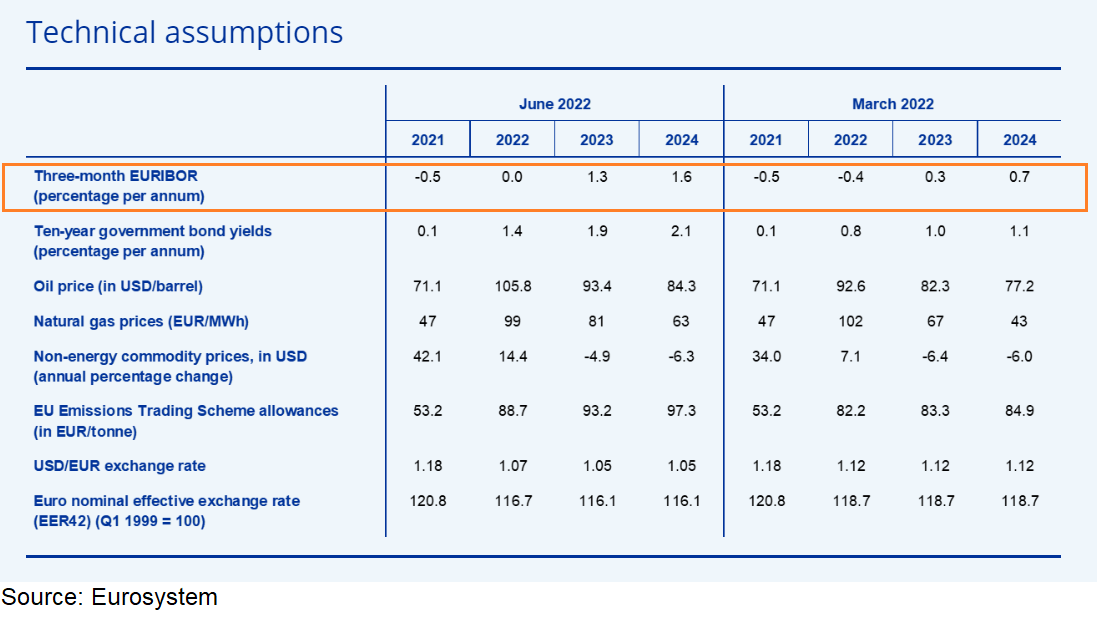

ECB announces expected 25bps rate hike in July and is considering a 50bps rate hike in September.

ECB also raises expected interest rates to 0 by the end of this year, 1.3 and 1.6 in 2023 and 2024, much higher than the March forecast.

ECB also lowers the real GDP growth forecast and raises the inflation forecast compared to March 2022

In addition, ECB is also ending loose monetary policies, including the Public Sector Purchase Program (PSPP) at the end of Q3 this year and the Pandemic Emergency Purchase Program (PEPP) last March

PSPP is the program to purchase government bonds of ECB member countries, launched in 2015 to counter deflation risk (negative inflation).

PEPP allows ECB to directly purchase various assets in the financial market, providing direct capital to businesses and governments facing difficulties during the pandemic period.

Comments on ECB's interest rate policy and its impact on the market

The above policy shows that ECB plans to gradually increase interest rates to avoid too large a shock to the economy. In exchange for time for corporate financial adjustments, ECB accepts “living with inflation” this year and lowers the growth target.

However, as mentioned above, ECB's rate hikes increase concerns about market liquidity, making the Eurozone highly likely to quickly fall into fragmentation risk:

The gap between Forward contract rates (Forward Rate Agreements, FRA) and overnight SWAP rates (OIS) is widening, reflecting investor pessimism ahead of the Eurozone's fragmentation risk.

Facing Fragmentation Risk: Waiting for a new tool

Facing the risk of Fragmentation Risk due to Italy's bond spread surging last week, ECB took quick action to address the issue by:

Buying Italian government bonds to reduce the yield demanded by investors for this bond.

Selling German bonds to ensure liquidity balance (avoiding injecting large amounts of liquidity into the market).

However, this is only a temporary measure to soothe the market. ECB cannot implement this if all countries at risk of Fragmentation Risk increase their bond spreads. Moreover, selling German bonds faces strong opposition because Germany's 10-year bond yield rose immediately after:

In the emergency meeting on 06/15, ECB signaled its determination to find a tool to resolve the fragmentation issue without affecting liquidity and the impact of the rate hike policy at the upcoming 07/20-21 meeting.

Many economists have proposed that ECB reactivate the Outright Monetary Transaction (OMT) program, a tool used before the Eurozone crisis phase in 2012.

OMT, proposed by former ECB President Mario Draghi, with the famous quote “whatever it takes”, by any means to save Europe's common currency during the 2012 crisis.

OMT allows ECB to directly purchase short-term government bonds (maturities of 1-3 years) from countries at high default risk.

Liquidity injected into the market will then be withdrawn by “any means necessary” ("by any means necessary").

The tool used to withdraw liquidity from the market during the 2012 period was auctioning corresponding one-week deposits at ECB.

CONCLUSION

The macroeconomic situation in Europe can be summarized in 3 points:

Inflation in Europe is mainly due to Europe's dependence on energy.

However, monetary policy is difficult for ECB to implement easily due to the fragmentation risks of the monetary market composed of 19 member countries with different political institutions and fiscal systems.

The market is awaiting ECB's solution direction at the upcoming July meeting for fragmentation risk

The reactivation of the OMT program is expected to resolve the bond spread issue, helping transmit ECB's interest rate policy evenly to member countries without affecting market liquidity. However, OMT previously faced opposition from the German Central Bank. Jens Weidmann, then president of the German central bank, argued that ECB's intervention would erode "the will of Eurozone member countries to implement public debt reforms". Germany's Supreme Court also ruled that OMT violates the Treaty on the Functioning of the European Union (EU Treaty) and the German Constitution.

To conclude this week's macroeconomic article, Viet Hustler sends readers the comic image below that fully depicts Germany's opposition to the OMT program in 2012.

Comments (2)

Bài viết rất thú vị, làm tốt lắm Linh!

Haha, I love you Bea.

Login to comment